A bank writing off a loan by giving another loan is common - with a new promoter, they are lending to a different entity, and they are accepting that the new promoter won't come in unless loans are reduced. Happened in Bhushan with Tata steel also.

SEBI doesn't allow promoter to own>75%. But this was an utter mess: Bhushan's resolution had Tata Steel own 95%+ but only 75% in equity, rest through convertible debt! SEBI realized futility of this, and relaxed rules for all bankruptcy resolutions.

SEBI allowed promoters to reduce to 75% within 3 years. But with 99% of shares held by promoter, there was a huge supply and demand issue, and share price just zoomed up!

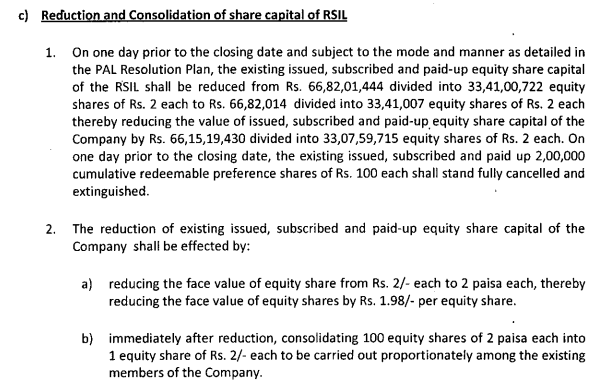

Existing shareholders got one share for every 100 they owned. Low float, prices will go up.

Existing shareholders got one share for every 100 they owned. Low float, prices will go up.

The stupidity: Banks didn't take any shares in the company. This is strange because the company was to stay listed. However, banks can at best request, can't force an acquirer to give them shares. (Acquirers usually happy to give, banks want higher money)

If banks had taken, say 5% of the company, they would have recovered more of the loans they wrote off. But there would probably have been lower upfront cash in that situation, and banks don't like that.

Anyhow the price went berserk. It was 3.5 rupees (effectively 350, since 100 shares became one). That 350 has, in three years, become 1100 or so. For a loss making company growing to 880 cr. profit, it's not bad, but it's not REAL either. Why?

Because massive new supply of shares had to come, sometime. The 25% regulation will apply, so promoters have to dilute. They're doing it now, for an issue of about 4350 cr. with a follow on public offer.

The money will give them enough to pay off their debt.

The money will give them enough to pay off their debt.

If what @maheshperi is saying is correct, then the 4350 cr. for 20% of NEW money means that the current valuation of the co is 17,400 cr. (Math: post issue 21750 cr. minus the new cash they will get = current valuation)

That's about Rs. 600 per share.

That's about Rs. 600 per share.

Consider that profits could go to say 1000 cr. (no interest to pay next year) and the valuation of 21,000 cr. is a p/e of 21. A tad expensive perhaps, but nothing spectacular.

Patanjali took the risk and turned the co around. Their cash is now worth like 17-20x. Risk paid off.

Patanjali took the risk and turned the co around. Their cash is now worth like 17-20x. Risk paid off.

If you don't want a fresh promoter to earn this kind of reward, then yes, liquidate the company. But if you want a successful resolution, you have to be willing to give the reward to the new person that comes in. (Want a piece? Take equity)

I respect reasoned debate but a lot of the comments are politically motivated, praise a government, blame some other etc. I don't endorse any of these comments - I am not pro-X or pro-Y, this is an economic discussion. It would be the same regardless of who is in power.

Counters and replies:

Loading suggestions...