Financial Analysis Post 5: Analyzing Impact of IND AS 115 on financial statement for the companies which engages in long term contracts with its customers.

Case Study: Mahindra Holidays & resorts (1/n)

Case Study: Mahindra Holidays & resorts (1/n)

Please read our previous post to understand the effects of revenue recognition policy changes here:

This post has been dedicated to analysing accounting standard change (IND AS 115 introduced by ICAI & it’s impact on financial statements).(2/n)

This post has been dedicated to analysing accounting standard change (IND AS 115 introduced by ICAI & it’s impact on financial statements).(2/n)

In FY19, we saw a change in revenue recognition policies of all firms as AS corresponding to revenue recognition were revised. Ind AS 115 (old) focuses on the control approach to determine revenue recognition as against the risk and rewards model under Ind AS 18 (new).(3/n)

All of the companies had to change their revenue recognition policies under the new accounting standards & this transition had a significant impact across telecom, information technology, engineering, real estate & construction i.e. businesses involving long term contracts. (4/n)

Case Study: Mahindra holidays & Resorts

Mahindra holidays sells holiday packages to its clients with a tenure of almost 25 years! Mahindra saw a drastic impact due to the AS changes for Revenue recognition. (5/n)

Mahindra holidays sells holiday packages to its clients with a tenure of almost 25 years! Mahindra saw a drastic impact due to the AS changes for Revenue recognition. (5/n)

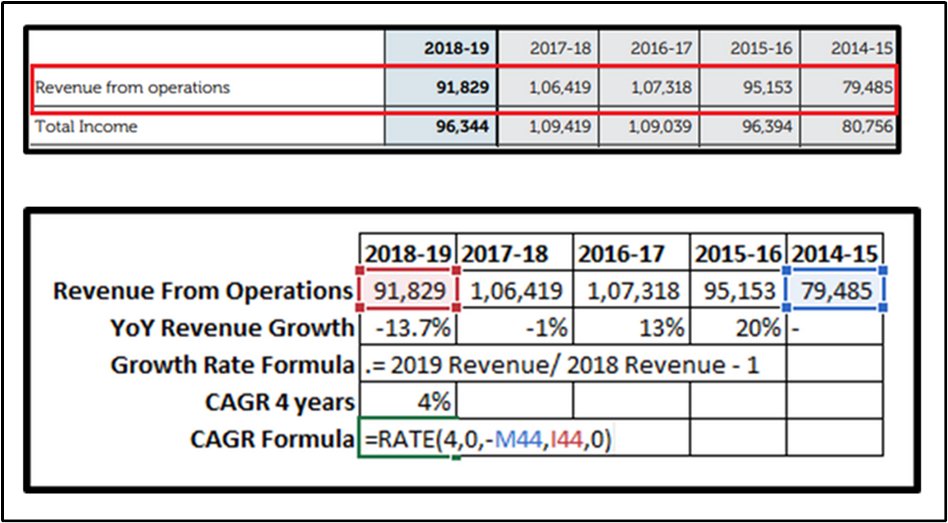

Looking at time series Revenue figures reported by the firm, you will observe 14% dip in revenues of FY19 shown in the snapshot below! (6/n)

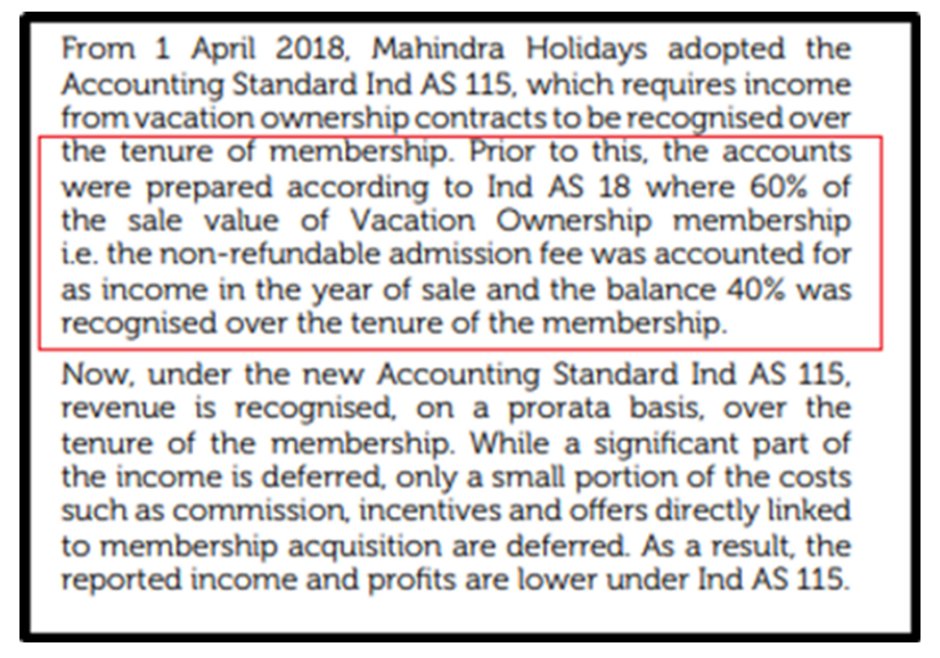

Taking a closer look at the revenue recognition policies, we observed that there has been Accounting Standard changes. Below is the explanation for the same by the Chairman of Mahindra Holidays. (7/n)

Earlier-Revenue from sales of vacation ownership were 60% recorded upfront as it was non-refundable & the rest 40% was recorded over the tenure of membership. Post IND AS 115, as you can see above, it is now prorated equally across the entire tenure. (8/n)

Applying it numerically, if a 25-year membership was sold for 3 Lakh rupees in FY 2018, Earlier, 60% of 3 Lakh would have been recognized in FY18 (1.8 Lakh) itself & remaining 40% were to be equal for the remaining 24 years (1.2/24 lakh per annum). (9/n)

However, since the company is now reporting under new AS, all new contracts sold in FY 19 will see a revenue recognition of 12 thousand per annum (3/25, equally split across 25 years). (10/n)

Adjustment for Previous years: The old contracts have been adjusted with a retrospective adjustment directly to equities without impacting income statement. Hence a significant drop in revenues! (11/n)

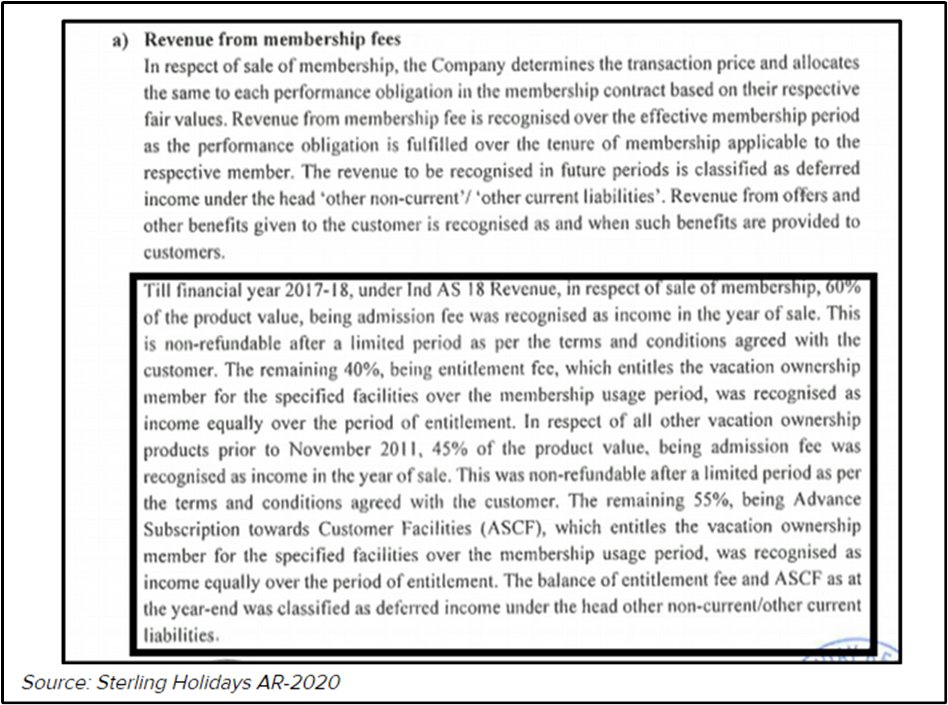

An analyst also needs to check revenue recognition policies even within the industry the company is part of. This is only to get a sense of judgement how the other industry partners are recognizing revenues & identify if our company is being aggressive or at par with them.(12/n)

We also looked at Sterling holidays, its peer, We found it had a similar revenue recognition policy, giving us a sense of comfort that the company we are analyzing was not applying something out of the blue but at par with industry practices.(13/n)

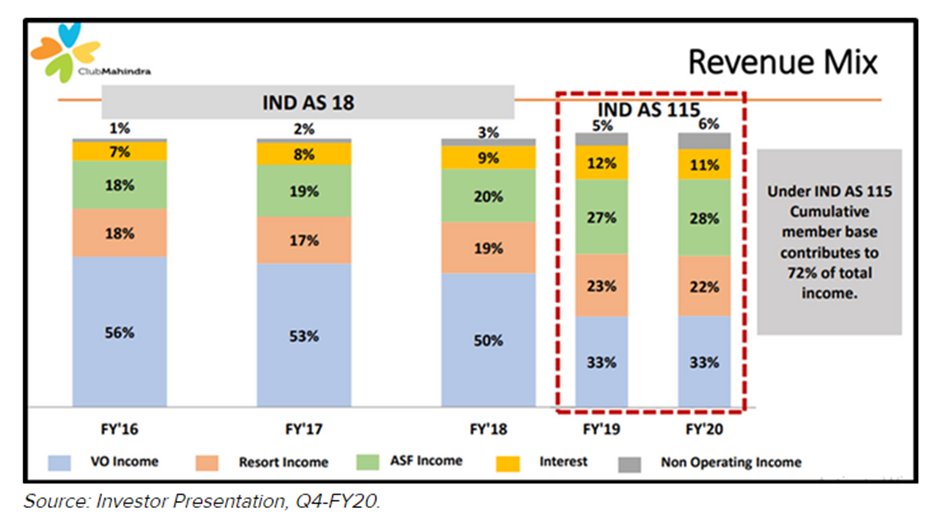

Composition of revenues have changed post the AS change naturally since the majority of the revenue of Vacation Ownership sales which was earlier being recorded upfront is now being prorated across the tenure shown in snapshot below.(14/n)

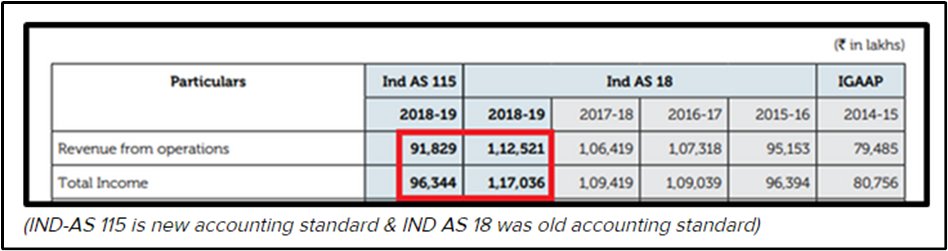

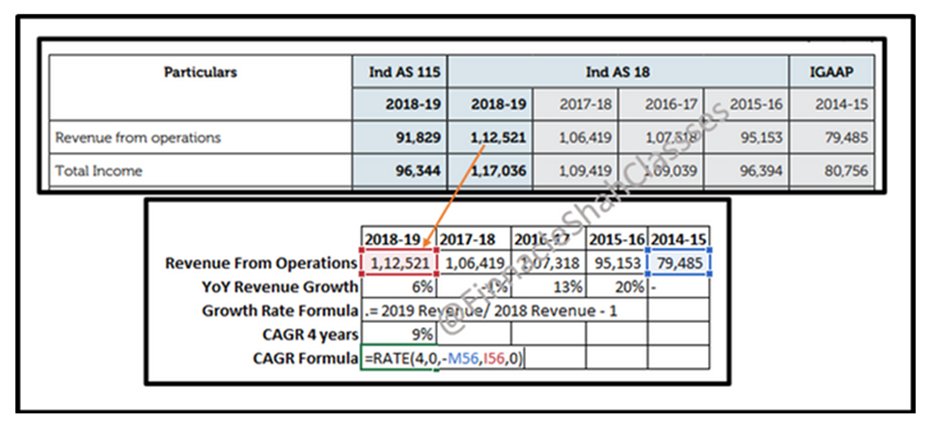

Below is the disclosure provided by the company for the AS changes & its impact, in its AR2019 describing if IND AS 18 were to be applied to FY19, company's revenues would have been 1125.2 Cr instead of 918.29 Cr (which is as per IND AS 115) (15/n)

To calculate actual YoY growth rate, we should be using IND AS 18 figures of FY19 & compare them to FY18 figures to get an understanding of actual business growth rather than using IND AS 115 FY 19 figures. This gives us a growth rate of 6% instead of -14%.(16/n)

This way, we segregate the impact & judge the true business growth. For next year YoY figures, you will have to compare both new AS figures & let go of old figures for the two years as both year figures correspond to the new Accounting Standard.(17/n)

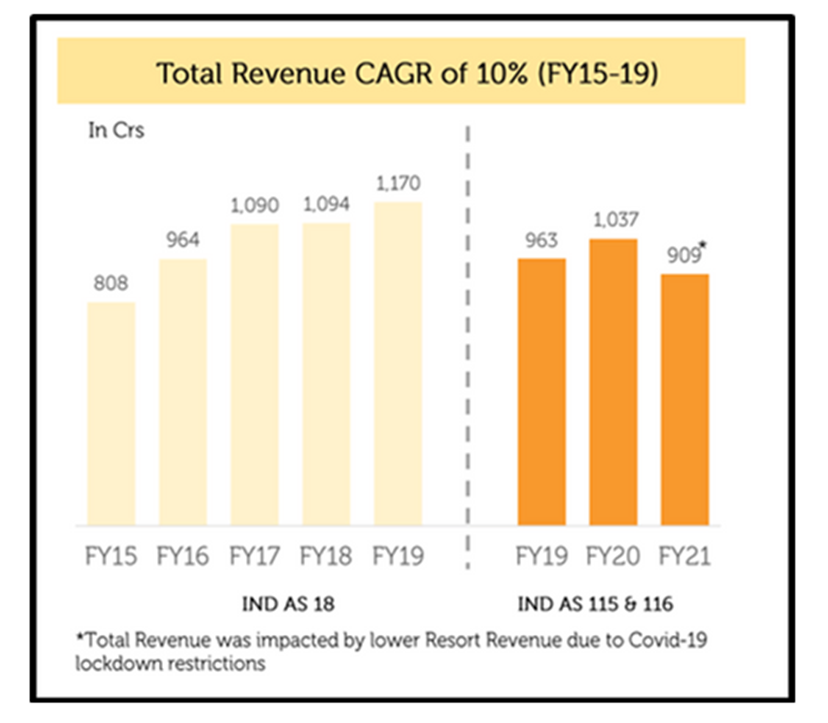

As time proceeds, We will have more & more Revenue figures corresponding to New AS, then we would be able to compute multiple year CAGR accordingly. A similar analysis has been already done by Mahindra Holidays in their Investor Presentation of Q2 FY21 shown below.(18/n)

Thought you might find it interesting @ashwinidamani @ZerodhaVarsity @Dhruvapandey @amitmantri @PuneetK009 @amey_candor @abhymurarka (19/n)

Read Entire Post here: finnacleshahclasses.com

Watch our YouTube video here: youtu.be

Readers on @MultipieSocial can read the same here: multipie.co

To continue your learning & fun with finance follow us on Instagram: instagram.com (20/n)

Watch our YouTube video here: youtu.be

Readers on @MultipieSocial can read the same here: multipie.co

To continue your learning & fun with finance follow us on Instagram: instagram.com (20/n)

Loading suggestions...