Delhivery has been at the forefront of transforming the e-commerce business in India.

The company is set for an IPO from May 11.

Here is a short thread🧵and if you should subscribe tip the IPO or not.

Hit "Retweet" to educate maximum retail investors

Lets go👇

(1/24)

The company is set for an IPO from May 11.

Here is a short thread🧵and if you should subscribe tip the IPO or not.

Hit "Retweet" to educate maximum retail investors

Lets go👇

(1/24)

So what does Delhivery(DL) do?

DL is an emerging leader in fully integrated logistics services.

DL provides supply chain solutions to a diverse base such as e-commerce marketplaces, direct-to-consumer e-tailers, and enterprises and SMEs across several verticals.

(2/24)

DL is an emerging leader in fully integrated logistics services.

DL provides supply chain solutions to a diverse base such as e-commerce marketplaces, direct-to-consumer e-tailers, and enterprises and SMEs across several verticals.

(2/24)

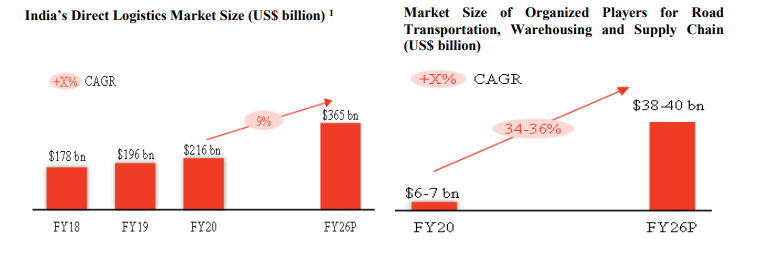

Sector Analysis:-

So how big is the logistics sector?

The logistics sector is one of the largest in the world and presents a large addressable opportunity,of US$216 billion in Fiscal 2020.

The sector is expected to grow to US$365 billion by Fiscal 2026 at a CAGR of 9%

(3/24)

So how big is the logistics sector?

The logistics sector is one of the largest in the world and presents a large addressable opportunity,of US$216 billion in Fiscal 2020.

The sector is expected to grow to US$365 billion by Fiscal 2026 at a CAGR of 9%

(3/24)

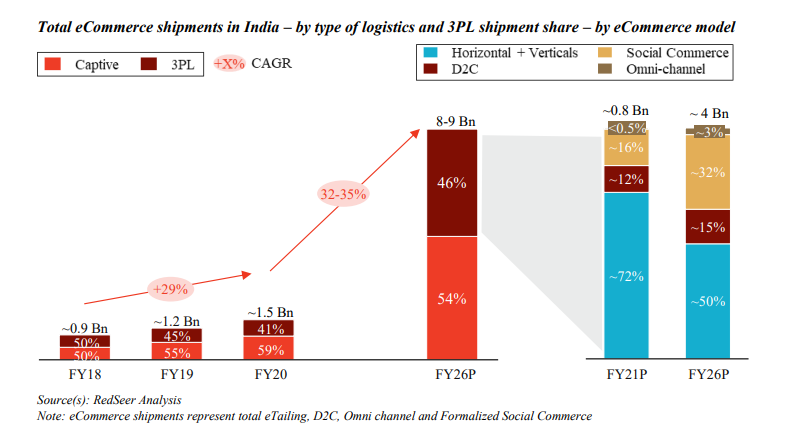

Express Delivery is growing fast:-

These are typically e-commerce

orders, with standard turnaround times of 3-4 days.

The express parcel delivery market was at ~US$2.3 billion in size in 2020,is expected to reach ~US$10-12 billion by 2026 at a CAGR of 28-32%.

(4/24)

These are typically e-commerce

orders, with standard turnaround times of 3-4 days.

The express parcel delivery market was at ~US$2.3 billion in size in 2020,is expected to reach ~US$10-12 billion by 2026 at a CAGR of 28-32%.

(4/24)

Market share in express delivery

41% of the market is handled by organised players:-

16% of this market was handled by Delhivery

Express Delivery forms 69% of the revenue for the company.

(5/24)

41% of the market is handled by organised players:-

16% of this market was handled by Delhivery

Express Delivery forms 69% of the revenue for the company.

(5/24)

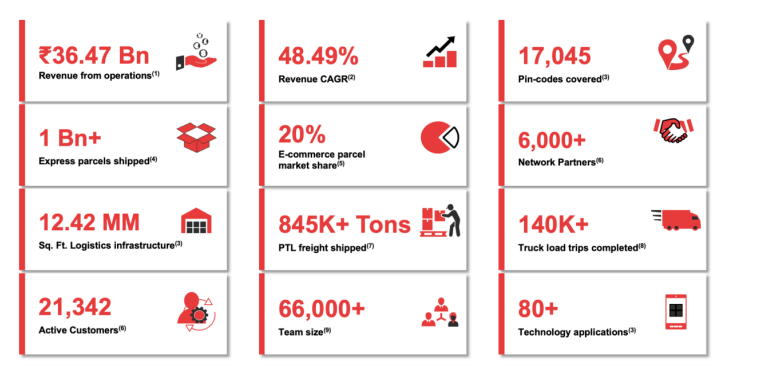

Rapid rise of Delhivery:-

DL is the largest integrated,fastest growing fully integrated logistics services player in India by revenue as.

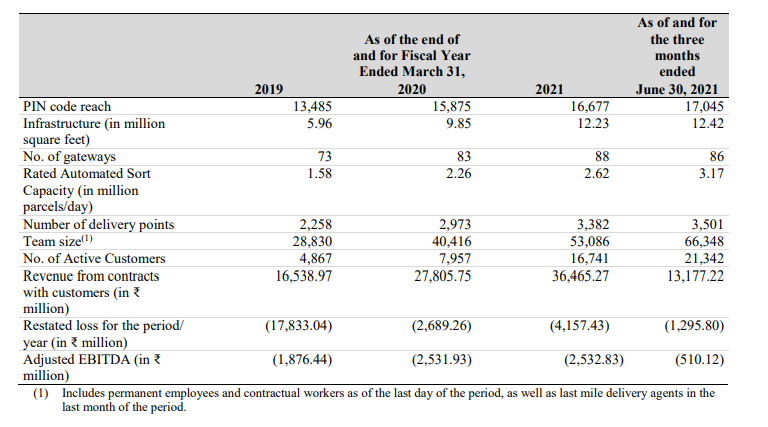

Revenue from contracts with customers has grown from ₹1,653.90 crore in 2019 to

₹3,646.53 crore in 2021, or a CAGR of 48.49%.

(6/24)

DL is the largest integrated,fastest growing fully integrated logistics services player in India by revenue as.

Revenue from contracts with customers has grown from ₹1,653.90 crore in 2019 to

₹3,646.53 crore in 2021, or a CAGR of 48.49%.

(6/24)

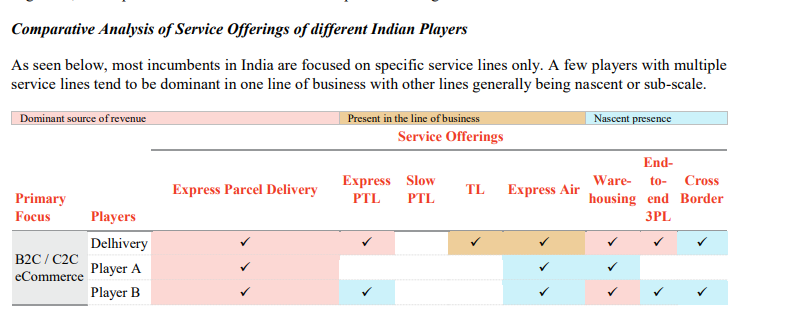

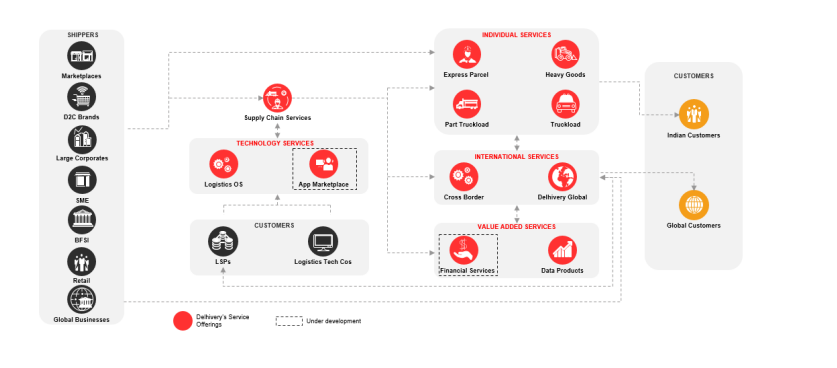

Business of the company:-

1. Express Parcel

2.Partial Truck Load(PTL) Frieght

3.Truck Load Frieght

4. Supply chain Services

5. Cross Border Services

(7/24)

1. Express Parcel

2.Partial Truck Load(PTL) Frieght

3.Truck Load Frieght

4. Supply chain Services

5. Cross Border Services

(7/24)

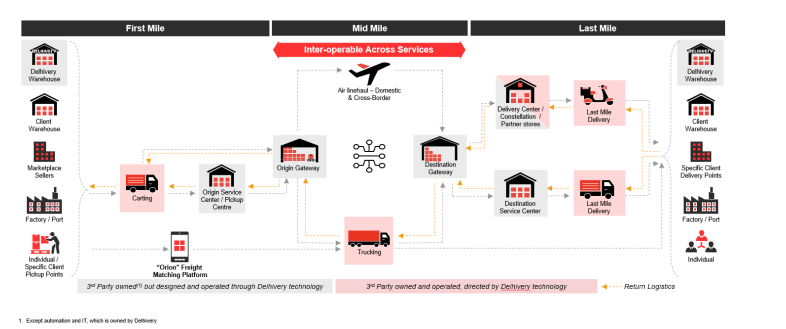

How does Delhivery deliver so flawless?

Gateway and Automated sort center facilities sort the parcel properly for onward journey to delivery or service centres from where parcels are delivered.

Technology plays a very vital role in making sure deliveries are flawless

(8/24)

Gateway and Automated sort center facilities sort the parcel properly for onward journey to delivery or service centres from where parcels are delivered.

Technology plays a very vital role in making sure deliveries are flawless

(8/24)

Strengths:-

1.Integrated solutions

Provides full range of services, like express parcel delivery,heavy goods delivery, PTL freight, TL freight, warehousing, supply chain solutions, along with value-added services such as ecommerce return services,payment collection etc

(9/24)

1.Integrated solutions

Provides full range of services, like express parcel delivery,heavy goods delivery, PTL freight, TL freight, warehousing, supply chain solutions, along with value-added services such as ecommerce return services,payment collection etc

(9/24)

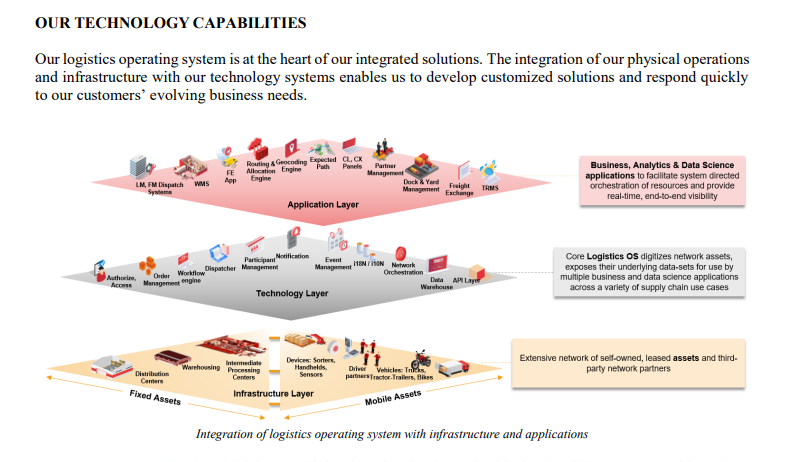

2. Automation and World Class operating system

In-house logistics technology stack is built to meet the dynamic needs of modern supply chains

Logistics solutions can be customized as per customer requirements.

(10/24)

In-house logistics technology stack is built to meet the dynamic needs of modern supply chains

Logistics solutions can be customized as per customer requirements.

(10/24)

DL operates 20 fully and semi-automated sortation centres and 86 gateways across India

as of June 30, 2021.

Automation, combined with system-directed floor operations, path expectation algorithms and machine-vision guided truck loading systems, improves efficieny.

(11/24)

as of June 30, 2021.

Automation, combined with system-directed floor operations, path expectation algorithms and machine-vision guided truck loading systems, improves efficieny.

(11/24)

Technology is the key to making sure deliveries are on time.

The company has 80 self built applications

The company uses about 500 engineers to constantly innovate.

(12/24)

The company has 80 self built applications

The company uses about 500 engineers to constantly innovate.

(12/24)

Vast Reach:-

The company operates in about 17,045 pin codes.

Data intelligence together with Automation helps the company in the flawless execution of 1000s of parcels.

(13/24)

The company operates in about 17,045 pin codes.

Data intelligence together with Automation helps the company in the flawless execution of 1000s of parcels.

(13/24)

Strong relationships with a diverse customer base:-

The company has a diverse base of 21,342 Active Customers across e-commerce, consumer durables, electronics,lifestyle, FMCG, industrial goods, automotives, healthcare and retail, in the three months ended June 30, 2021

(14/24)

The company has a diverse base of 21,342 Active Customers across e-commerce, consumer durables, electronics,lifestyle, FMCG, industrial goods, automotives, healthcare and retail, in the three months ended June 30, 2021

(14/24)

Weaknesses:-

The company uses technology heavily to carry out day-to-day operations.

Any disruptions there will be a cause of concern for the company,

(15/24)

The company uses technology heavily to carry out day-to-day operations.

Any disruptions there will be a cause of concern for the company,

(15/24)

Over-reliance on e-commerce:-

Revenue from parcel services of e-commerce contrinuted about 60% of the Revenue.

Any slowdown in these services could be a problem for the company.

(16/24)

Revenue from parcel services of e-commerce contrinuted about 60% of the Revenue.

Any slowdown in these services could be a problem for the company.

(16/24)

Fragmented+competitive Logistics Market:-

The company operates in a highly competitive industry.

Many segments have low barriers to entry,

resulting in a highly fragmented market.

Increased competition could lower profit margins or market share.

(17/24)

The company operates in a highly competitive industry.

Many segments have low barriers to entry,

resulting in a highly fragmented market.

Increased competition could lower profit margins or market share.

(17/24)

Customer Concentration:-

Top 5 customers of the company contribute 40% of the total revenue.

Any problem in any one of those could cause revenue loss for the company.

(18/24)

Top 5 customers of the company contribute 40% of the total revenue.

Any problem in any one of those could cause revenue loss for the company.

(18/24)

Financials:-

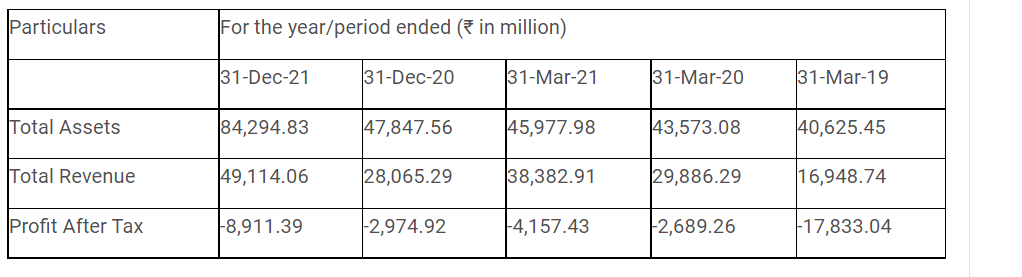

For the period ended Dec'21 the company reported a revenue of 4911cr.

The loss has expanded to 8911cr.

(19/24)

For the period ended Dec'21 the company reported a revenue of 4911cr.

The loss has expanded to 8911cr.

(19/24)

Objects of the Issue:-

Unlike most of the other IPOs here the money raised is being used to fund future growth

The objects of the offer are:

Funding organic growth.

Funding inorganic growth through acquisition and strategic initiatives.

(20/24)

Unlike most of the other IPOs here the money raised is being used to fund future growth

The objects of the offer are:

Funding organic growth.

Funding inorganic growth through acquisition and strategic initiatives.

(20/24)

Valuation:-

The company’s market value on a post-dilution basis will be Rs 35,284 crore at the upper end of the price band of Rs 462-487 per share.

(21/24)

The company’s market value on a post-dilution basis will be Rs 35,284 crore at the upper end of the price band of Rs 462-487 per share.

(21/24)

So what to do on the IPO?

The fully integrated model+technology stacks make the deliveries seamless.

From a business point of view,it is solving major logistics problem for e-commerce companies.

It has the potential to do exceptionally well over the next 5-10 years.

(22/24)

The fully integrated model+technology stacks make the deliveries seamless.

From a business point of view,it is solving major logistics problem for e-commerce companies.

It has the potential to do exceptionally well over the next 5-10 years.

(22/24)

However the company is still not profitable and is working hard to turn around the bottom line.

Delhivery IPO price has cut from Rs 900 to about Rs 450 which was the correct move.

The business is exceptionally good for the company.

(23/24)

Delhivery IPO price has cut from Rs 900 to about Rs 450 which was the correct move.

The business is exceptionally good for the company.

(23/24)

Long-term investors and highly risk-seeking investors can keep the company on watch.

Turnaround from loss to profit and high growth will be key triggers.

Disclaimer:-

Consult ur financial advisor before taking any investment decision.

(24/24)

Turnaround from loss to profit and high growth will be key triggers.

Disclaimer:-

Consult ur financial advisor before taking any investment decision.

(24/24)

Loading suggestions...