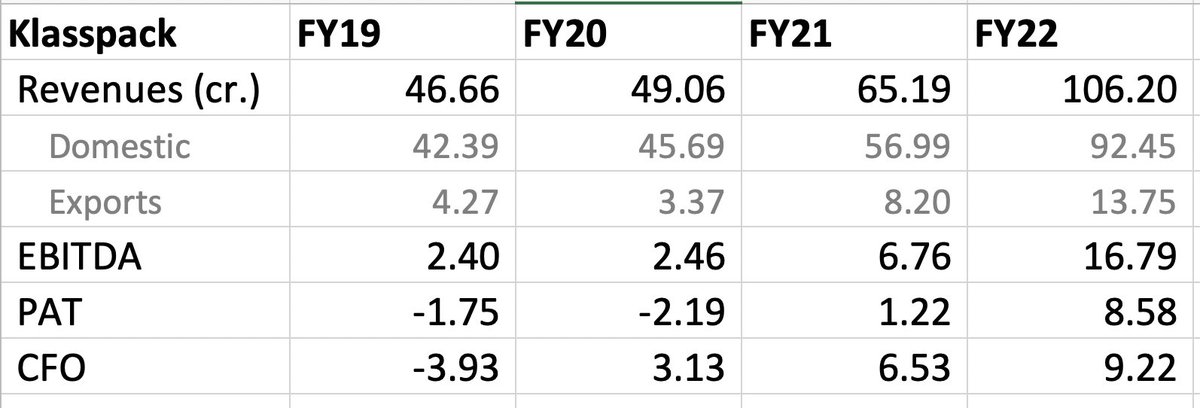

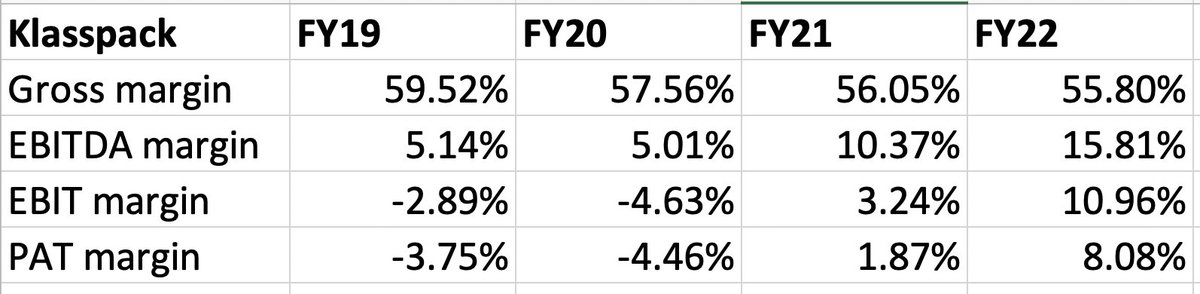

Borosil has scaled up their packaging division (Klasspack) very well, EBITDA margin has reached 15% and in on-track to reach 20% in the next few years.

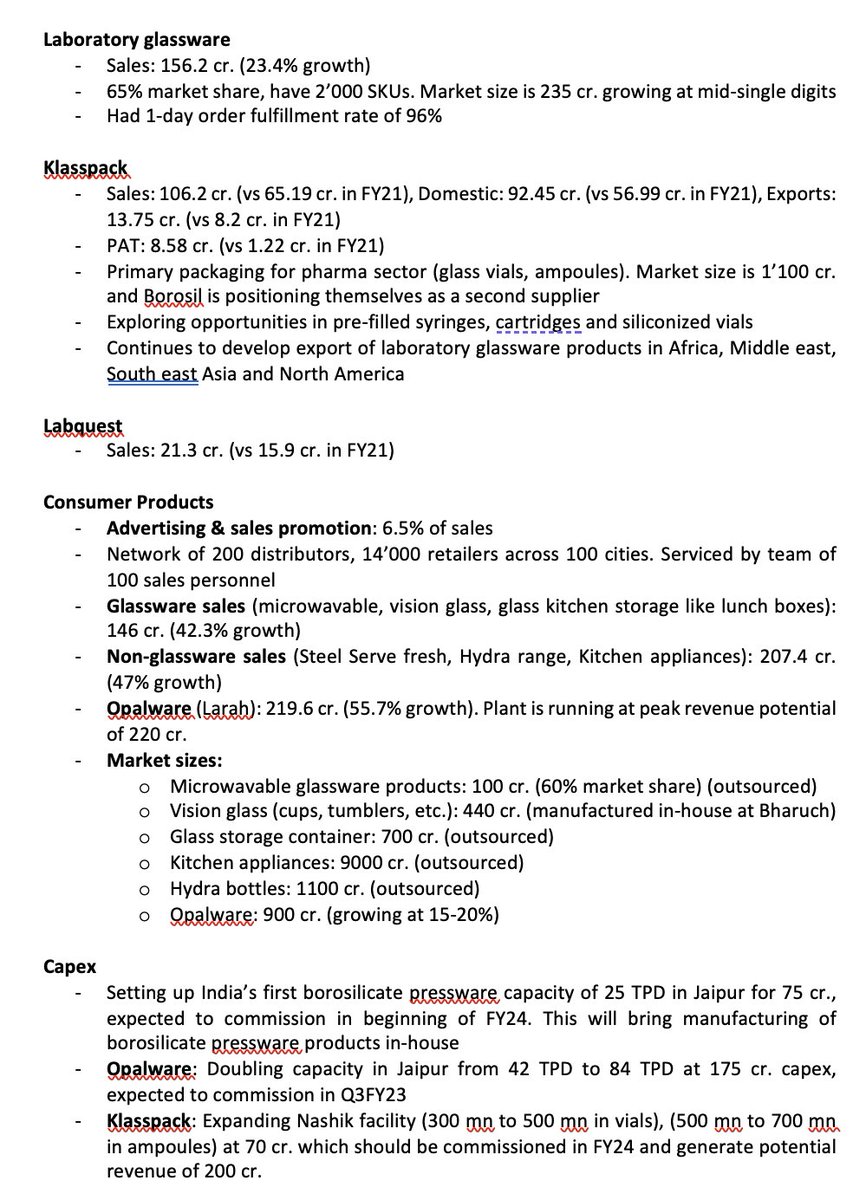

AR22 notes from Borosil, company is going on a massive capex which should come onstream in FY24. Company is expecting to scale consumer business to 1000 cr. by FY26

Borosil scientific division is super innovative and keep on coming up with niche products with limited competition. One example is filter paper which has only 1 other manufacturer, and this is currently outsourced (and will be brought in-house if sales scale)

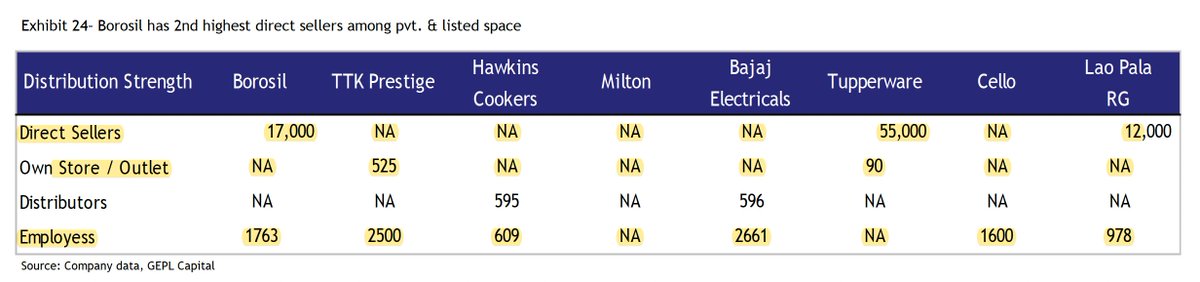

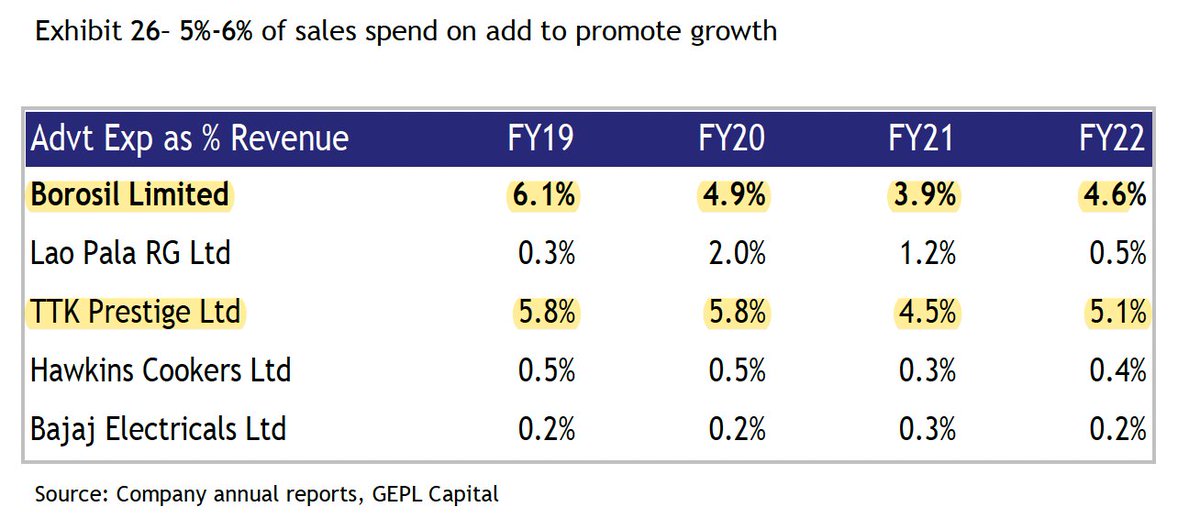

Borosil has one of the highest seller network after Tupperware, spends one of the highest on ads vs peers and is focused on growing through internal accruals with a massive capex of ~500 cr. Source: GEPL capital

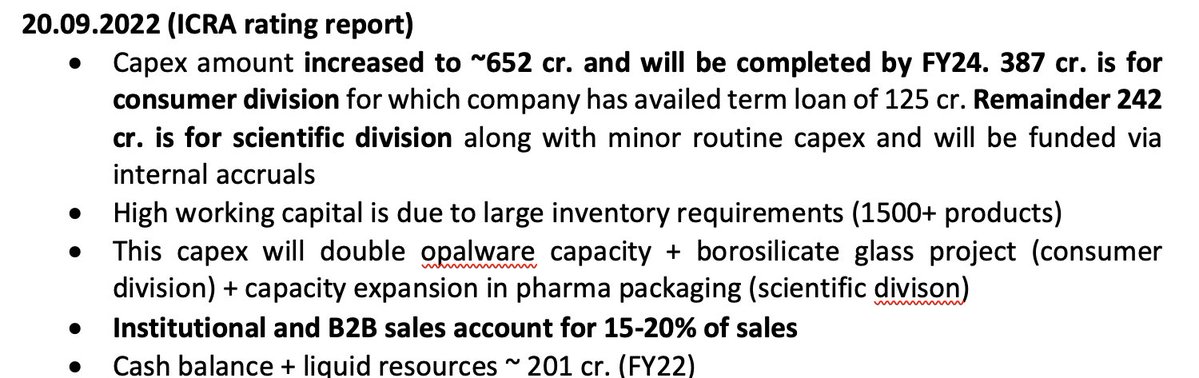

Very insightful ICRA ratings report for Borosil. Capex amount has increased to 650 cr. and will be partly funded through term loan of 125 cr. for consumer division

Borosil is targeting 20%+ EBITDA margins in consumer division while maintaining 20%+ sales growth. Margin pain will persist for 1 more quarter due to delay in capex commisioning

youtube.com

youtube.com

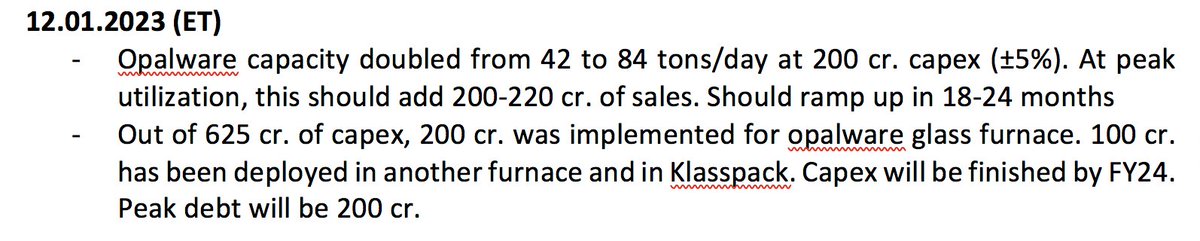

Borosil opalware capacity should fully ramp up in 18-24 months, half of the 625 cr. planned capex has been finished with remainder projected to be finished by FY24. Notes from @ETNOWlive interaction below

Loading suggestions...