For the first time since summer 2021, I believe bonds are looking like a decent risk/reward investment here.

And if that’s true, many other asset classes will behave differently too.

Accordingly, last week I have made some important changes to my book.

A thread.

1/18

And if that’s true, many other asset classes will behave differently too.

Accordingly, last week I have made some important changes to my book.

A thread.

1/18

For decades, bonds have been a beautiful asset to own in a diversified portfolio: a positive carry, return generating asset class with the ability to dampen equity market drawdowns.

An excellent asset to own.

But does this hold true in every macro regime?

2/

An excellent asset to own.

But does this hold true in every macro regime?

2/

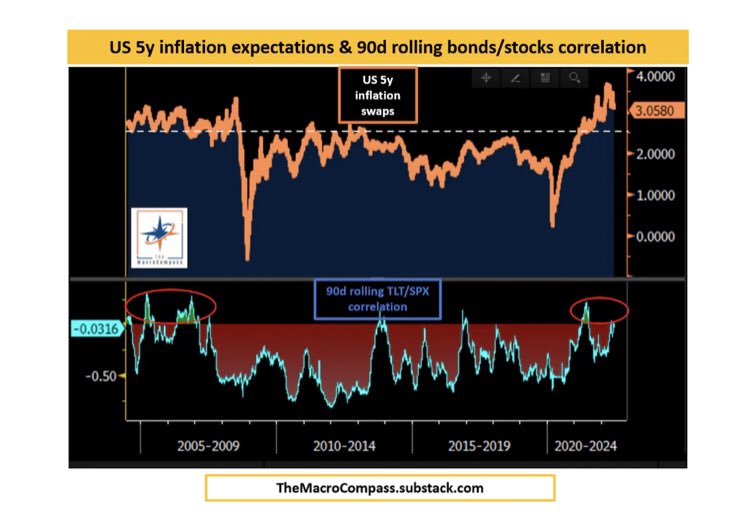

Not really.

The chart below shows that once you cross the 2.5% threshold in 5y inflation expectations, the negative correlation property quickly disappears.

When below 2.5% expected inflation, bonds retain their magic portfolio properties.

3/

The chart below shows that once you cross the 2.5% threshold in 5y inflation expectations, the negative correlation property quickly disappears.

When below 2.5% expected inflation, bonds retain their magic portfolio properties.

3/

Once inflation expectations surpass the CB’s objective (2%), when equity markets experience a drawdown policymakers are faced with a hard choice.

- accommodate conditions to stop the market bleeding

OR

- stay the course & preserve credibility

Not a slam dunk for bonds

4/

- accommodate conditions to stop the market bleeding

OR

- stay the course & preserve credibility

Not a slam dunk for bonds

4/

So, what about today?

Wen bonds?

Amongst many other things, I like to see 3 conditions achieved before entering bullish trades in fixed income.

5/

Wen bonds?

Amongst many other things, I like to see 3 conditions achieved before entering bullish trades in fixed income.

5/

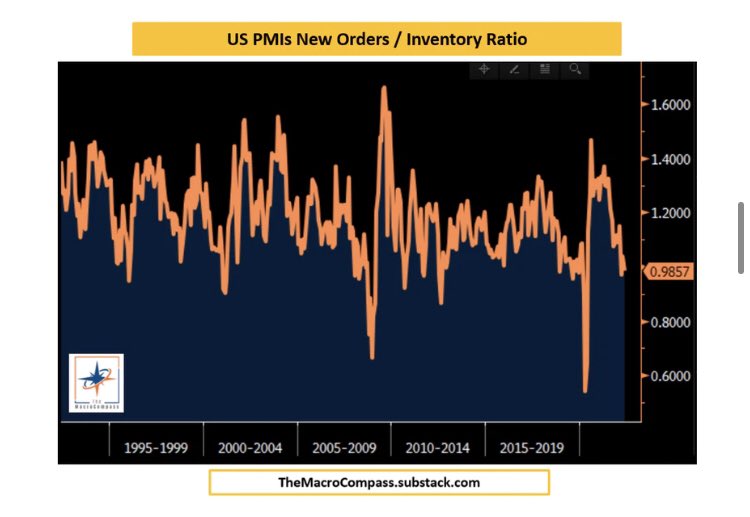

1. Is the momentum of growth slowing?

Yes.

Forward looking indicators have been pointing down for quarters.

PMIs orders/inventory at very low levels for example.

6/

Yes.

Forward looking indicators have been pointing down for quarters.

PMIs orders/inventory at very low levels for example.

6/

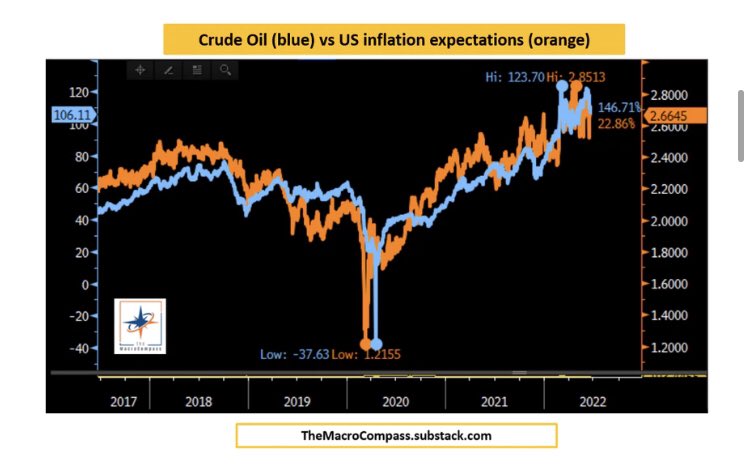

2. Is the momentum of inflation slowing?

Meh…we might be getting there. Look at commodities.

We also discussed how for bonds to regain their magic portfolio properties, we need 5y inflation expectations to drop below 2.5%.

This commodity drawdown might help.

7/

Meh…we might be getting there. Look at commodities.

We also discussed how for bonds to regain their magic portfolio properties, we need 5y inflation expectations to drop below 2.5%.

This commodity drawdown might help.

7/

3. Are Central Banks (directly or indirectly) giving us the green light to buy bonds?

Indirectly: yes.

The Direct green light is the 1st phase of monpol accommodation: when they explicitly pivot dovish or they engage in QE, they are giving us a direct signal to lift bonds.

8/

Indirectly: yes.

The Direct green light is the 1st phase of monpol accommodation: when they explicitly pivot dovish or they engage in QE, they are giving us a direct signal to lift bonds.

8/

Ofc not the case today.

But we are getting instead the Indirect Green Light

CBs have tightened policy hard enough for long enough to basically guarantee a sharp economic slowdown

As they are enhancing the probability of nominal growth reverting to weak structural trends…

9/

But we are getting instead the Indirect Green Light

CBs have tightened policy hard enough for long enough to basically guarantee a sharp economic slowdown

As they are enhancing the probability of nominal growth reverting to weak structural trends…

9/

…they are also increasing the appeal of long-term bonds.

An indirect green light signal to buy bonds

When monetary policy becomes restrictive for long enough (red box) or sharply moves from very accommodative to tight (red arrows), our credit-addicted priv. sector suffers

10/

An indirect green light signal to buy bonds

When monetary policy becomes restrictive for long enough (red box) or sharply moves from very accommodative to tight (red arrows), our credit-addicted priv. sector suffers

10/

In other words, the distribution of outcomes for future nominal growth becomes more predictable: once enough short-term damage is done, long-term growth is almost guaranteed to disappoint.

And in turn that means long-term bonds are more attractive.

11/

And in turn that means long-term bonds are more attractive.

11/

As we are ticking 2-and-a-bit of the 3 boxes, it’s time to adjust portfolios accordingly

My changes have been:

- I’ve taken profits on the SPX short

And I have added:

- 2x short Russell vs 1x long Nasdaq

- 2s10s curve flattener in US

- Some TLT for the long-term book

12/

My changes have been:

- I’ve taken profits on the SPX short

And I have added:

- 2x short Russell vs 1x long Nasdaq

- 2s10s curve flattener in US

- Some TLT for the long-term book

12/

Powell told us he isn’t gonna dial back his hawkish stance despite clear signs of demand destruction emerging in both forward-looking indicators & now also in several macro asset classes.

13/

13/

As time goes by, this is going to increase the probability of a recession & the attractiveness of long-term bonds

Yield curves should meaningfully invert: recession warnings keep flashing in the back-end & Powell forces the front-end to reflect his unchanged hawkish stance

14/

Yield curves should meaningfully invert: recession warnings keep flashing in the back-end & Powell forces the front-end to reflect his unchanged hawkish stance

14/

Flatteners and short bond vol are my preferred expressions, but I also started accumulating some TLTs (yet leaving some room to add).

In equities instead, something interesting might happen.

15/

In equities instead, something interesting might happen.

15/

The long-end bond stabilization might spur a tentative bid in tech while US small caps are likely to disproportionately suffer from an earnings slowdown

I want to capture the relative value there but I want to keep my net equity short exposure: long 1x QQQ, short 2x IWM

16/

I want to capture the relative value there but I want to keep my net equity short exposure: long 1x QQQ, short 2x IWM

16/

As always I can be wrong: if the economy picks up or the Fed is keen in keeping yield curves (temporarily) steeper (active QT selling of long bonds) I will be wrong and stop out accordingly.

Overall though I feel a macro regime shift is undergoing.

17/

Overall though I feel a macro regime shift is undergoing.

17/

If you liked this thread, you are going to enjoy my free newsletter TheMacroCompass.substack.com where I deliver macro insights and often post about portfolio construction too.

We are 62,000+ strong, come have a look: it’s free :)

18/18

We are 62,000+ strong, come have a look: it’s free :)

18/18

Loading suggestions...