A 🧵 to understand the thesis & the risks of the latest entrant in my portfolio Tinna Rubber 👇

20-25% grower, 20% ROE, around 15 P/E (with competitive advantages) is a recipe for wealth creation.

20-25% grower, 20% ROE, around 15 P/E (with competitive advantages) is a recipe for wealth creation.

Q1: What does Tinna Rubber do?

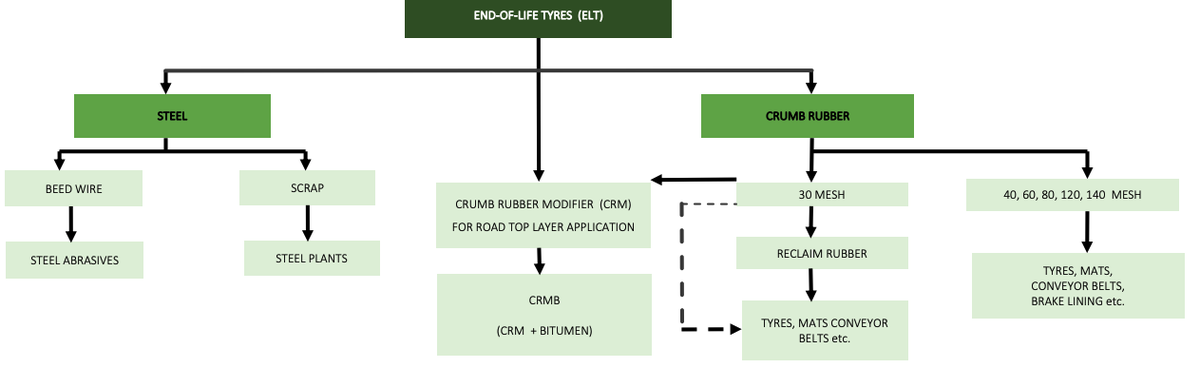

A: Tinna is in the circular economy space. It buys used rubber tyres, breaks the tyres into its components (the rubber part, the steel wire part) & recycles both of them: Crumb rubber Modifier (CRM), Micronized Rubber powder (MRP), steel abrasives

A: Tinna is in the circular economy space. It buys used rubber tyres, breaks the tyres into its components (the rubber part, the steel wire part) & recycles both of them: Crumb rubber Modifier (CRM), Micronized Rubber powder (MRP), steel abrasives

Tinna's products find applications in a wide variety of end applications like

Roads, tyres, Rubber Droppers, Conveyor belts, Rubber Mats.

What causes 🤯 is that same rubber tyre goes into making the road & the tyre that runs on the road. Beautiful.

Roads, tyres, Rubber Droppers, Conveyor belts, Rubber Mats.

What causes 🤯 is that same rubber tyre goes into making the road & the tyre that runs on the road. Beautiful.

Tinna's Focus is on enabling circular economy by recovering 99.5% of all the material in an End of Life Tyre & converting it into specialized mixers/modifiers.

ESG ✔️✔️

ESG ✔️✔️

Q2: But sahil, what incentive do rubber or road makers have to use Tinna's products?

A: Great question! A Crumb Rubber modifier costs one fourth or one third the cost of Bitumen from which roads are made.

A: Great question! A Crumb Rubber modifier costs one fourth or one third the cost of Bitumen from which roads are made.

In addition, it results in saving 60% of the CO2 emissions which the process of making the road makes!! Whats more? These roads also last 100% more.

ESG ✔️

Cost advantage ✔️

Prolonged Lifetime ✔️

Tinna Rubber has saved 8L tons of CO2 till date.

ESG ✔️

Cost advantage ✔️

Prolonged Lifetime ✔️

Tinna Rubber has saved 8L tons of CO2 till date.

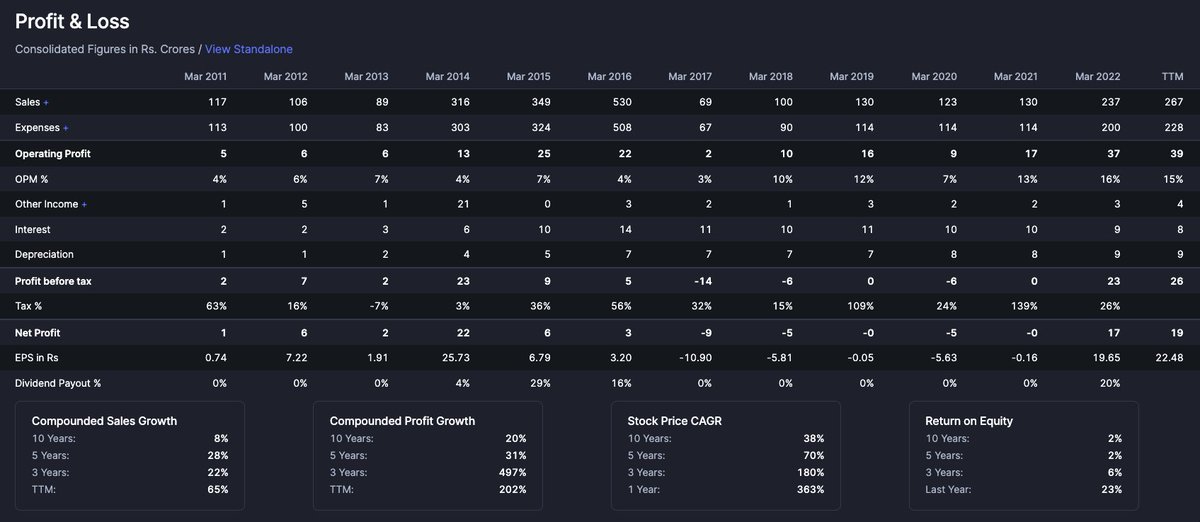

Q3: Okay, this sounds interesting. But this is all theory. If the product market fit is so brilliant, shouldnt the topline growth numbers talk?

A: Yes, they should. And, they do.

Tinna's topline has grown by 65%, 22%, 28% in the last 1/3/5 years.

A: Yes, they should. And, they do.

Tinna's topline has grown by 65%, 22%, 28% in the last 1/3/5 years.

What is really heartening to see is the margins inch upwards. Why has this happened?

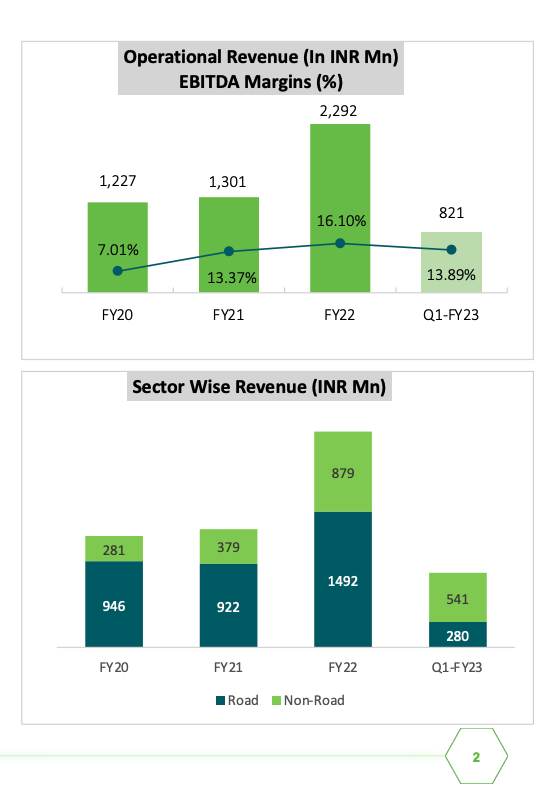

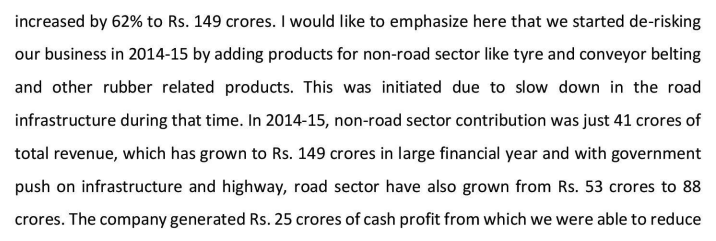

The biz is divided into 2 parts. The road segment & the non road segment (tyres, rubber belts, conveyer belts, dropper caps).

The biz is divided into 2 parts. The road segment & the non road segment (tyres, rubber belts, conveyer belts, dropper caps).

The scale up of non-road segment has been exceptional scaling up from 41cr in Fy15 to 200cr runrate in Q1FY23. Almost 5x scaleup in 7 years. That's a cool 26% CAGR.

Added advantage of higher value added product mix driving EBITDA margin improvements.

Added advantage of higher value added product mix driving EBITDA margin improvements.

Q4: Yaar all of that is backward looking, what kind of growth can they do in the future?

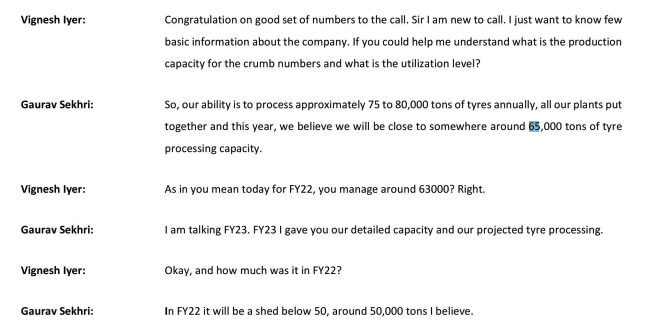

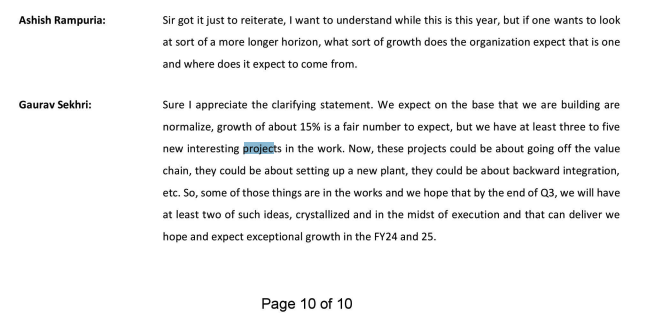

A: At time of writing AR their conservative guidance is for 20-25% growth. In the Q1 Concall, they guided for capacity sold to go up from 50k ton in Fy22 to 60k-65k ton in FY23.

A: At time of writing AR their conservative guidance is for 20-25% growth. In the Q1 Concall, they guided for capacity sold to go up from 50k ton in Fy22 to 60k-65k ton in FY23.

That's a cool 20-30% volume growth. If 10% volume growth is good, what is 20% volume growth?

Longer term guidance of 15% growth (very conservative guidance IMO).

Longer term guidance of 15% growth (very conservative guidance IMO).

Q5: Given the past fast growth, I am skeptical how large the market is & how much they can grow.

A: Let us analyse the Road & Non-Road segments separately.

India uses 7 million ton of Bitumen annually. This can use 12-14% blending. So the TAM here is around 9 lakh tons.

A: Let us analyse the Road & Non-Road segments separately.

India uses 7 million ton of Bitumen annually. This can use 12-14% blending. So the TAM here is around 9 lakh tons.

Current demand & supply is around 2 lakh ton. The potential to grow is around 5x (of course this needs creating awareness, creating the market, educating the infra & construction cos on the benefits of blending CRM with bitumen).

Src: youtube.com

Src: youtube.com

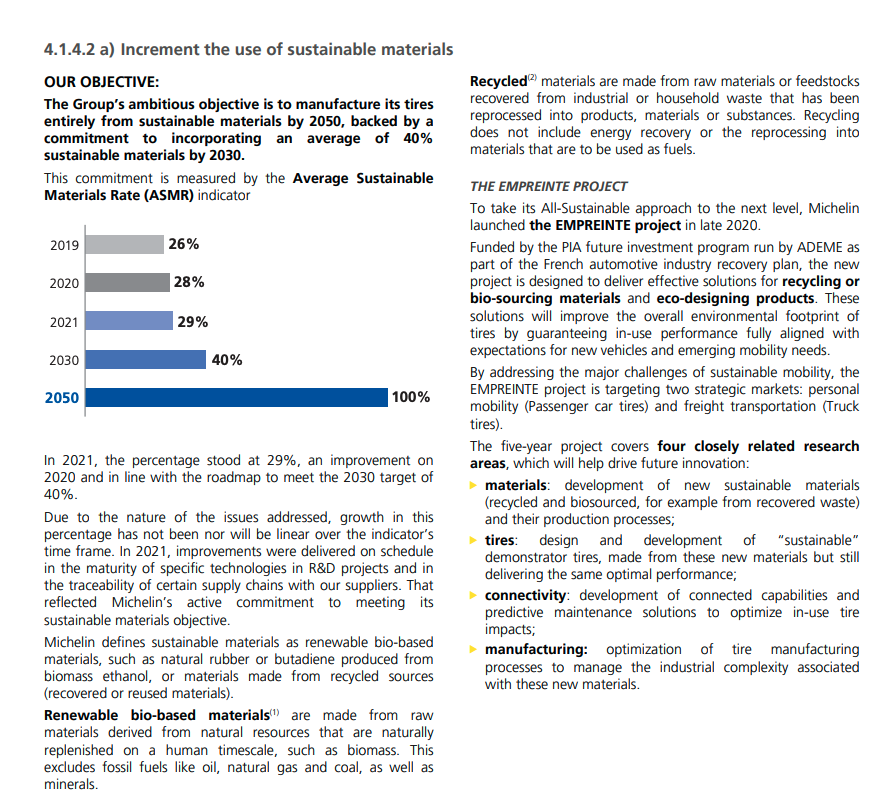

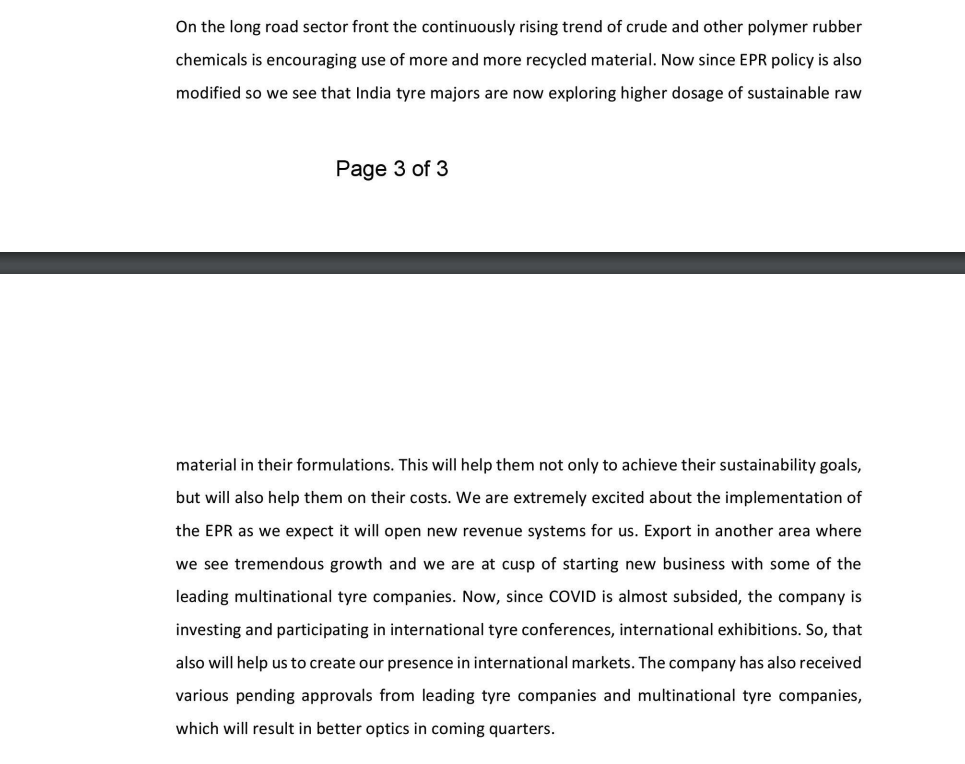

On the tyre side (a large part of non-road segment), Michelin, one of largest tyre makers of the world. By 2030, Michelin is committed to achieving on average 40% sustainable materials in its tires. By 2050, this level will reach 100%.

Indian tyre makers are currently around 3%-5% so there is a huge headroom to blend recycled materials like MRP (mnicronized rubber powder) or CRM (Crumb Rubber Modifier) into their tyre in order to increase the sustainability, reduce the cost.

Q7: Okay, but what concrete steps is Tinna taking to realize the growth? What is the growth bridge?

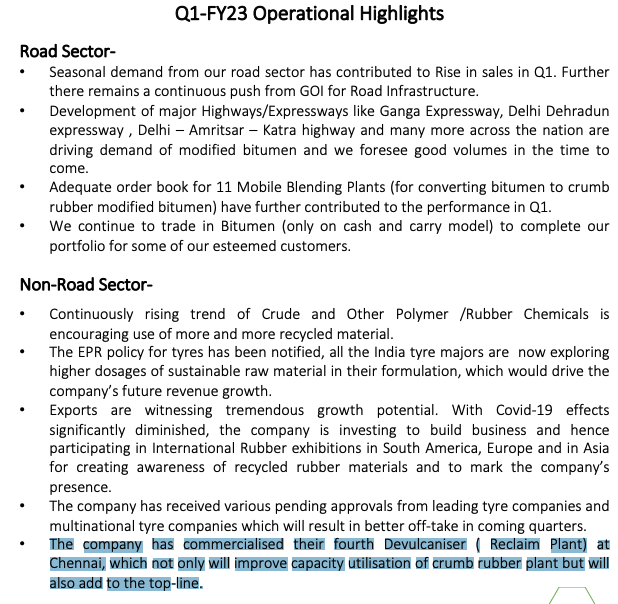

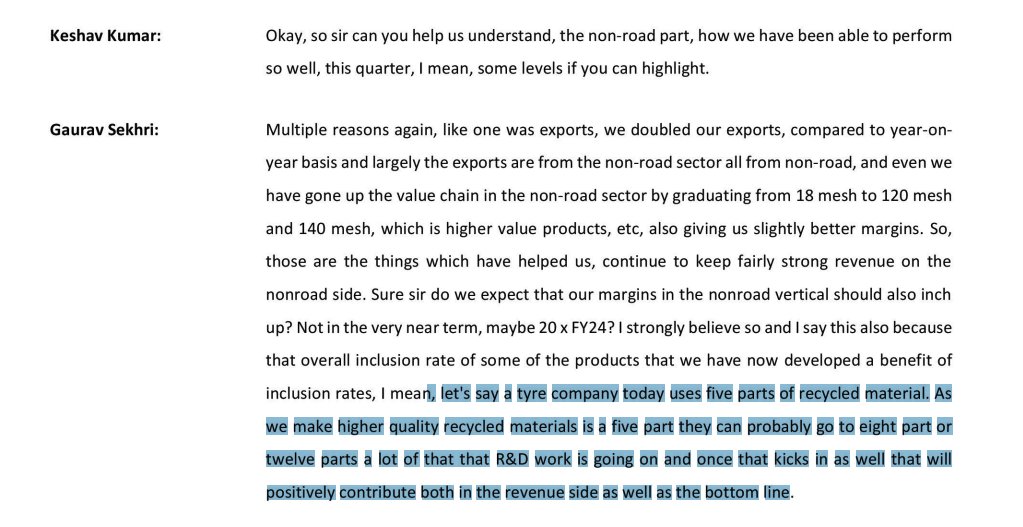

A: i. Exports. Currently 5% of topline, growing 100% right now. Co has recently received 2 pending approvals from leading global tyre manufacturers.

A: i. Exports. Currently 5% of topline, growing 100% right now. Co has recently received 2 pending approvals from leading global tyre manufacturers.

ii. commercialised fourth Devulcaniser ( Reclaim Plant) at Chennai, which not only will improve capacity utilisation of CRM plant by adding to the topline

iii. Co is working on 3-5 new projects: new geo launches, new clients, new value added products, even evaluating setting up brownfield or greenfield capacities.

Reminds me of amazon. Try N different experiments.

Reminds me of amazon. Try N different experiments.

iv. Most imp point. As co does more R&D, they unlock larger TAMs. If a tyre co today uses 5% recycled material. As tinna makes higher quality recycled materials 5% can go to 8 or 12%. Benefits topline (TAM) & bottomline (margins) both.

Q7: If the space is so good growth, what stops competitors from coming in? What are tinna's competitive advantages?

A: i. It takes 3-5 years for tyre manufacturers to approve your material. That acts as an entry barrier.

A: i. It takes 3-5 years for tyre manufacturers to approve your material. That acts as an entry barrier.

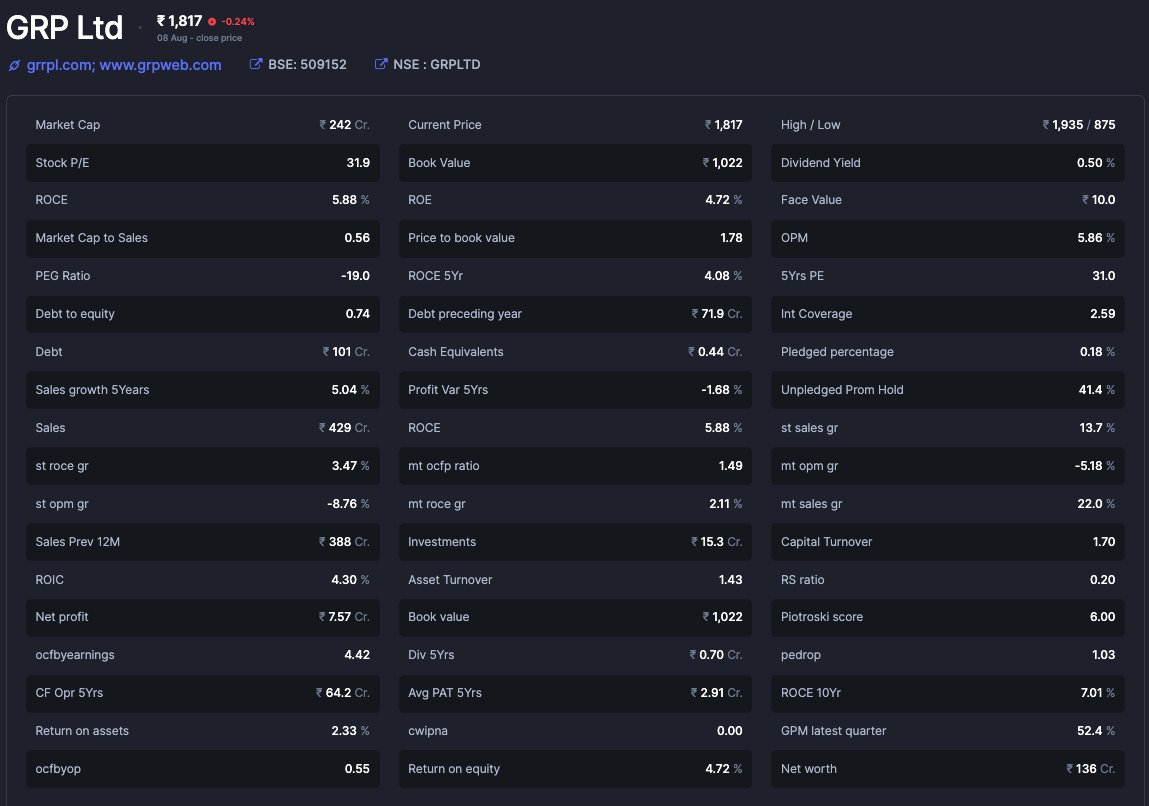

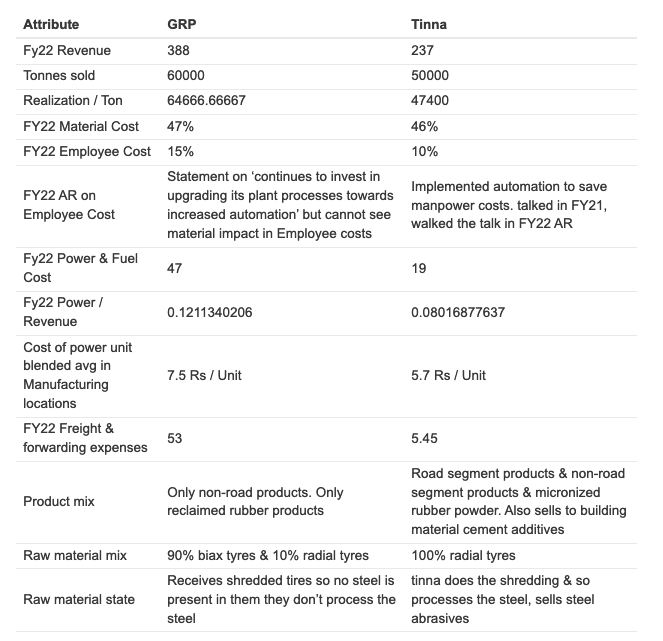

ii. Tinna does have a listed competitor called GRP. GRP has much poorer performance than Tinna. A Debt laden balance sheet, high power & labor costs, no topline growth.

Why? What are the differences b/w GRP & Tinna?

Why? What are the differences b/w GRP & Tinna?

Please be prepared for a mini-diversion into why Tinna might have succeeded where GRP has not.

1. Tinna is more forward integrated: Please see from 56:10 (youtu.be). He tells diff between grp & tinna.

1. Tinna is more forward integrated: Please see from 56:10 (youtu.be). He tells diff between grp & tinna.

Grp is only into non road segment, tinna gets 40% or so from road segment Also, grp only makes rubber reclaim products, does not make micronised rubber powder (MRP). No mention of MRP in its investor presentations, Concalls or annual reports.

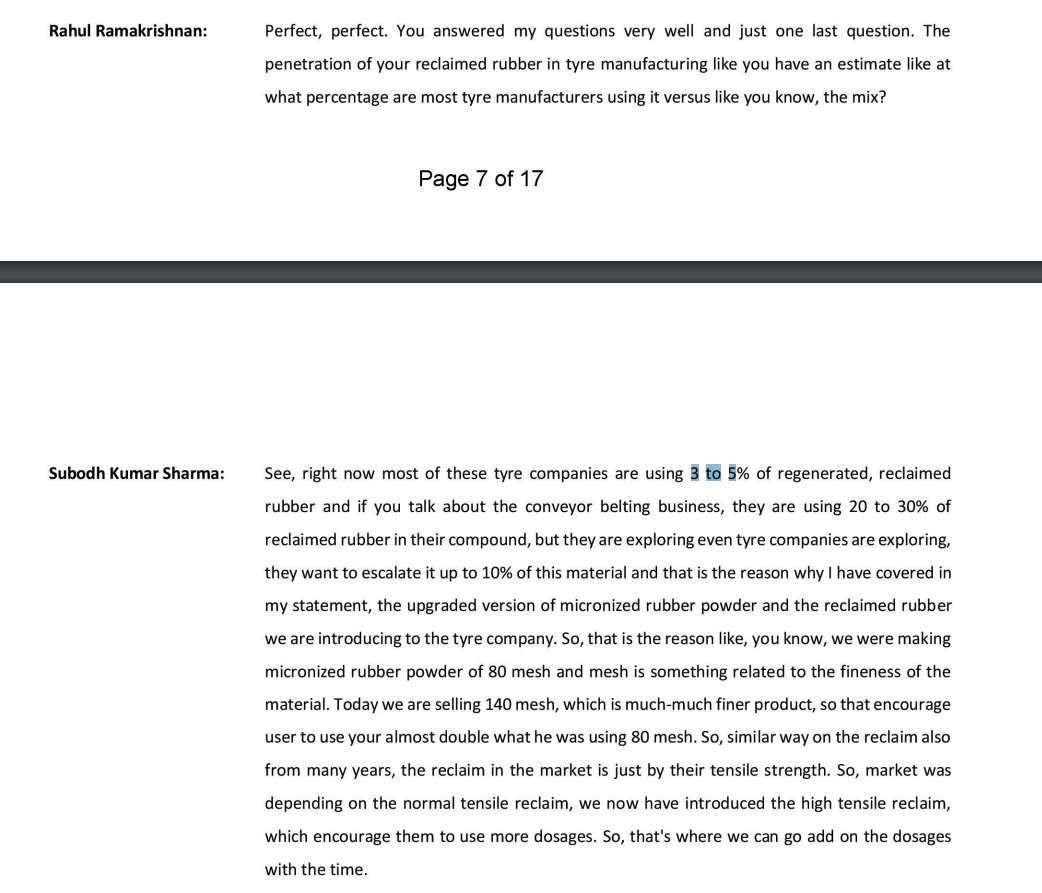

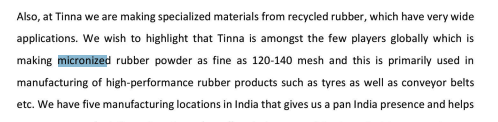

Tinna on other hand is among one of only MRP producers in the world (from tinnas Q1fy23 concall):

Tinna CEO also explains what the diference between CRM & MRP is. MRP is just a finer/smaller version of CRM. CRM are large rubber chunks.

^ The one on extreme right (above 120 MESH) is MRP.

^ The one on extreme right (above 120 MESH) is MRP.

Expectedly CRM would not bond or dissolve easily with bitumen or virgin rubber of the tyre (he explains that here: youtu.be).

This is why MRP is a superior product (easier & more structural integration with virgin rubber or bitumen).

This is why MRP is a superior product (easier & more structural integration with virgin rubber or bitumen).

Tinna did 10000 ton of MRP in FY22 (source: youtu.be)

That is roughly 20% of their volume output (must be higher % of value output).

That is roughly 20% of their volume output (must be higher % of value output).

Could be part of the reason why GRP has not been able to grow its topline is it possible that MRP usage increase is causal or correlated with CRM usage plateauing?

2. Tinna is more backward integrated: One more key difference which came out in grp concall : grp receives shredded tires so no steel is present in them they don’t process the steel Tinna receives ready made tyres which have steel in it & tinna produces steel abrasives out of…

…the steel wire present in the tyre & sells it as well.

3. Tinna works with a larger supply base: 90% of sourcing for GRP is biax tyres only 10% is radial tyres. Tinna 100% is radial tyres. According to both GRP & Tinna concalls, Radial tyres are growing much more rapidly than biax types.

Tinna also says in their concalls that radial tyres are higher quality & enable them to make higher quality products.

4. Tinna employee costs are around 9-10% compared to 15-17% for GRP. Even Tinna used to be around 15-17% mark until fy21, only fy22 onwards, employee cost fell sharply to 9%.

We find the reasons in FY22 & Fy21 annual reports: excerpts below:

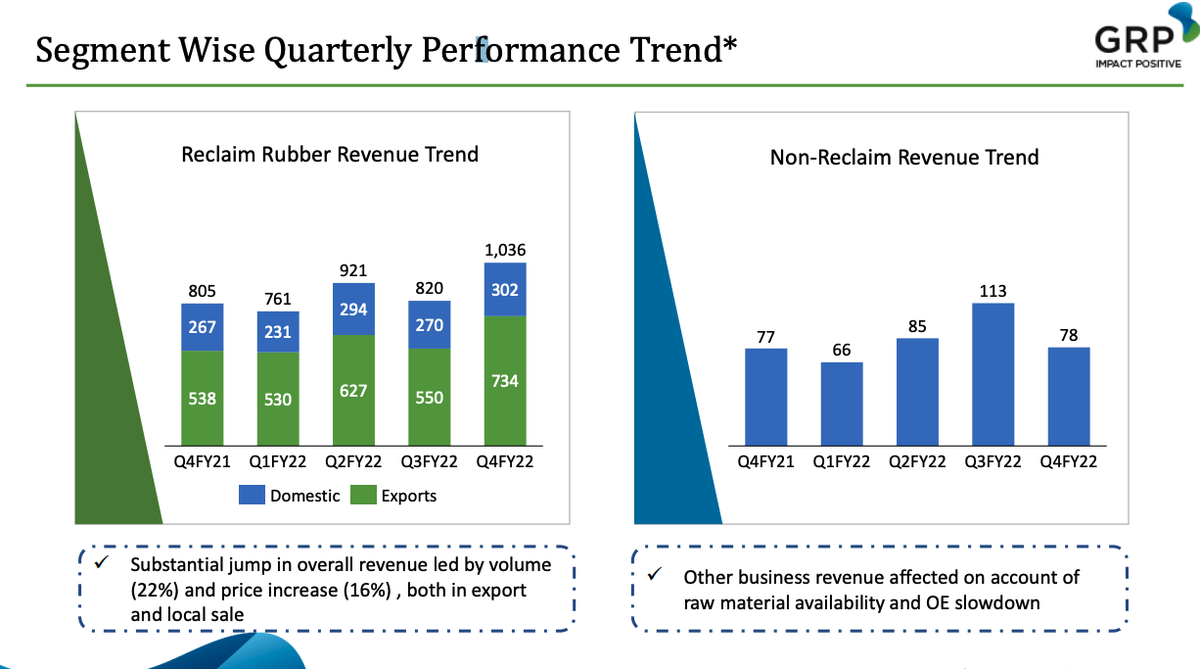

5. GRP has higher % of exports (40%). But, On EBITDA margins, GRP freight costs is massive at 50cr, so we have to validate whether export is really high margin for them (ex of the freight costs),

Tinna in comparison being largely domestic focussed has negligible freight costs (Tinna gets 5% from exports, GRP gets 40% from exports)

6. Material cost: wise both are neck & neck, around 45% material costs in FY22 for both of them.

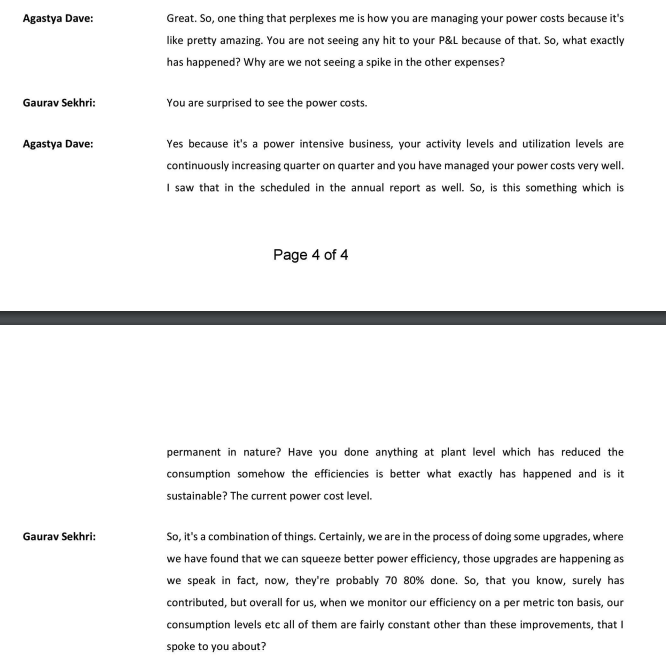

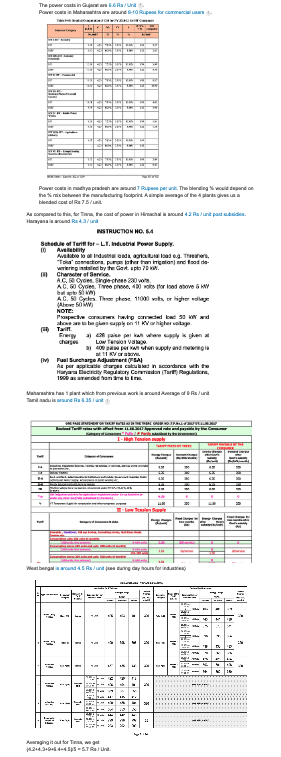

7. Power costs: Even on power costs Tinna has some details in Concall though not very satisfactory. Let us examine.

This is a little bit vague & i would love to ask Tinna management what these exact upgrades are which enable higher power efficiencies.

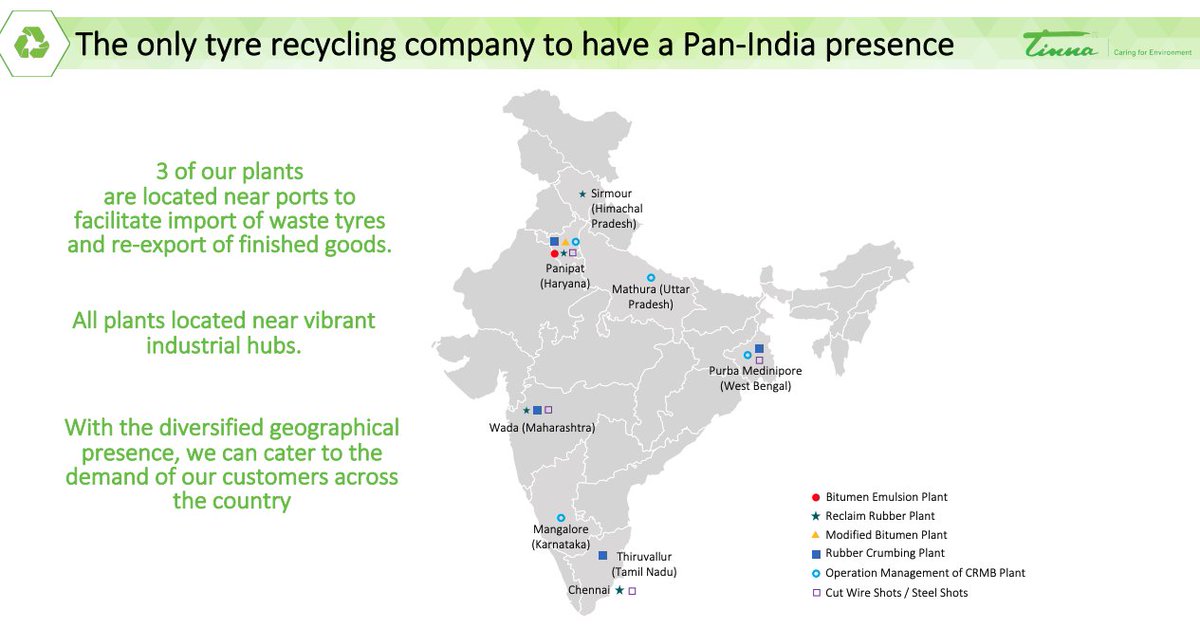

One thing to note here is that Tinna has a more diverse manufacturing footprint with plants in Himachal, harayana, Maharashtra, Tamil Nadu & West Bengal

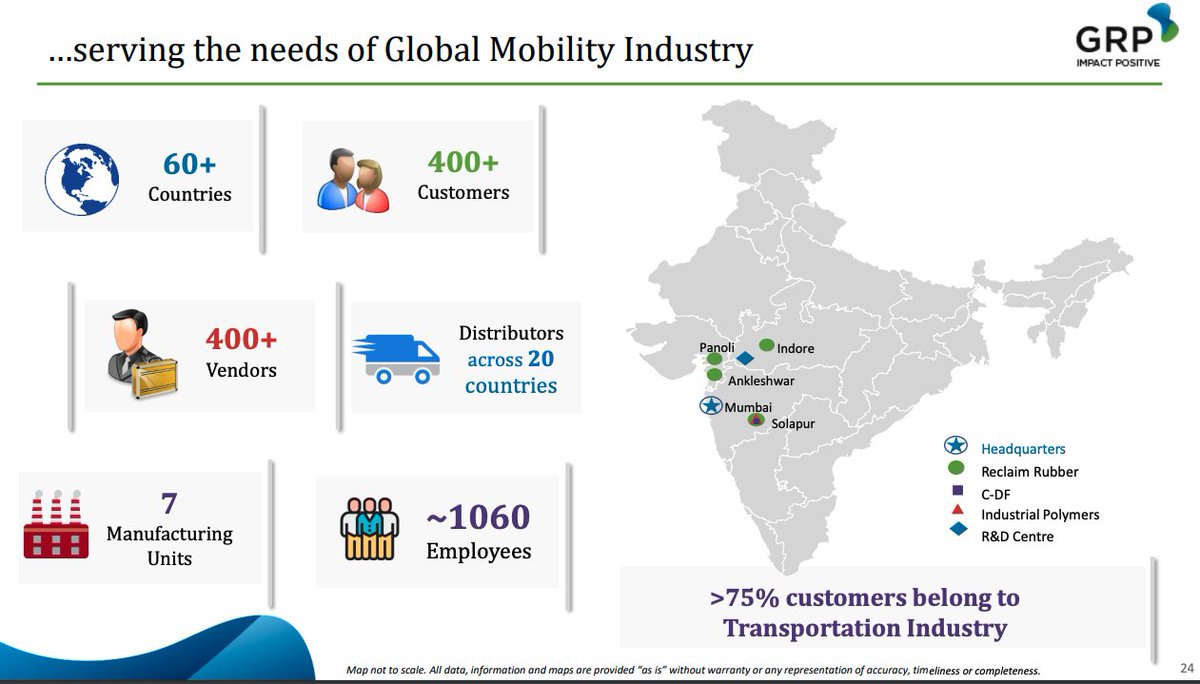

As opposed to GRP which has its manufacturing footprint concentrated in West India (Gujarat, Maharashtra, MP).

I then proceed to analyze the power costs in each of the states where GRP or tinna plants are. Long story short, it might be the case that Tinna buys its electricity up to 30% cheaper than GRP due to better locational advantage (specially north india plants).

Here is a summary of a competitive analysis of GRP & Tinna.

iii. (competitive advantages): Tinna is largest & only scaled producer of micronized rubber powder in india. 85-90% market share. Not the largest one, the only one. As @Amit_Jeswani1 sir says. Also one of largest tyre recyclers in india.

(next only to GRP but i expect tinna to overtake GRP in next 2 years).

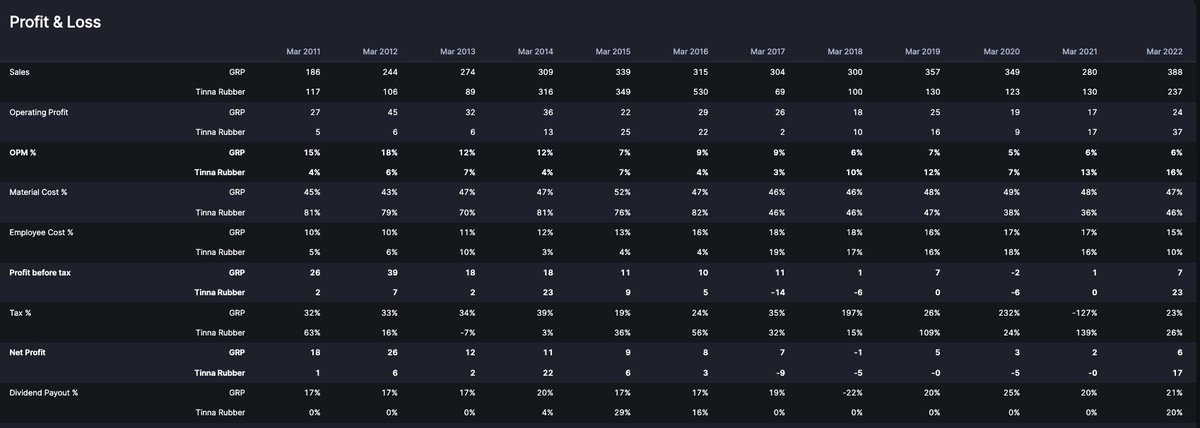

Q9: What about profitability?

A: A picture is worth a thousand words.

A: A picture is worth a thousand words.

Q10: Seems like the kind of co you'd want to own. What is the valuation you are paying?

A: when i started buying tracking quantities last week, it was around 17x TTM earnings. Co has guided to do similar to Q1 for rest of FY23. At that point i was looking at a FY23 P/E of 13.

A: when i started buying tracking quantities last week, it was around 17x TTM earnings. Co has guided to do similar to Q1 for rest of FY23. At that point i was looking at a FY23 P/E of 13.

Since then, price has gone up 25% so P/E have also inflated to TTM P/E of 21 & FY23 P/E of 16.

Given the competitive advantages, growth (20-25%), opportunity size (at least 10x TAM imo), competitive positioning (largest player in most imp components), I think it is still a bit undervalued though it was too cheap last week.

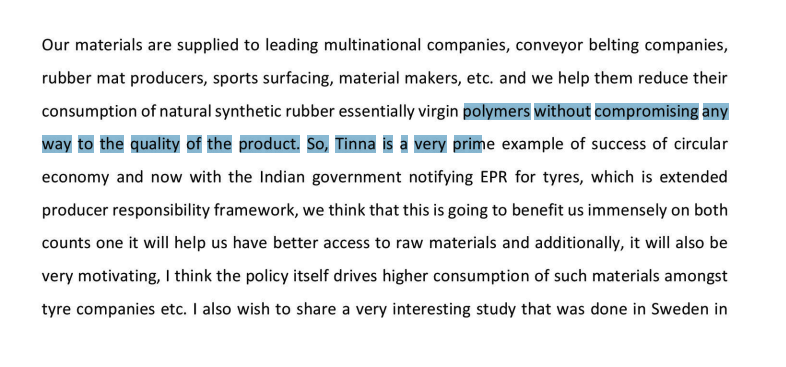

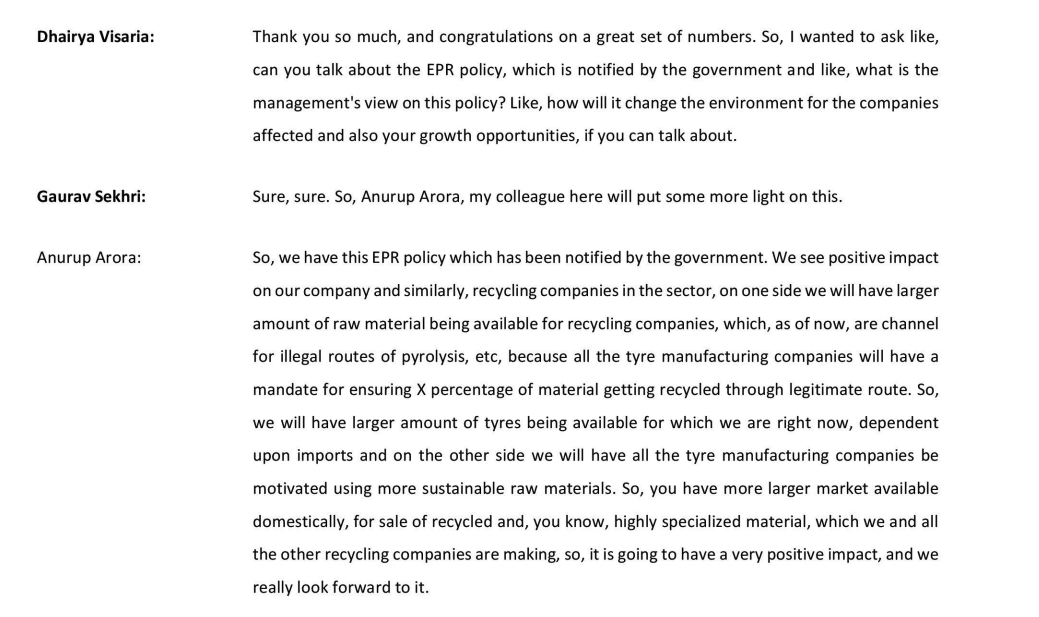

Q11: Given the great ESG positive nature of industry what is government doing here?

A: Enter, EPR: Extended producer responsibility.

thepolicytimes.com

India actually generates 15-18 lakh ton!!!

A: Enter, EPR: Extended producer responsibility.

thepolicytimes.com

India actually generates 15-18 lakh ton!!!

of waste tyres but there is no policy structure to ensure that these get disposed or reused in ways which are good for the environment. A whole lot end up getting burned (pyrolysis) which is a worse process because of pollution it causes.

EPR will benefit Tinna & industry on both supply side & demand side. Producer will have more responsibility for tyres they make. The producers will have a policy framework to give factory or quality discards to tyre recyclers like Tinna.

Tyre manufacturers will also be incentivised to include more recycled material in the cycles they make. In this way, EPR will create both demand & supply thus allowing higher value creation.

Q11: Gotcha. What are the gotcha? what are the risks?

A: i. However much we might harp on ESG, companies have a profit motive. Without doubt the recent increase in rubber prices has caused tailwinds for tinna (reclaimed rubber would be cheaper).

A: i. However much we might harp on ESG, companies have a profit motive. Without doubt the recent increase in rubber prices has caused tailwinds for tinna (reclaimed rubber would be cheaper).

So, rubber prices can act as a headwind as well.

ii. If GRP gets their act together & becomes an efficient competitor then tinna could be forced to grow slowly or drop margins. Need to track GRP closely.

iii. Are the margin gains sustainable?

ii. If GRP gets their act together & becomes an efficient competitor then tinna could be forced to grow slowly or drop margins. Need to track GRP closely.

iii. Are the margin gains sustainable?

Will they revert to pre-covid levels? Product mix is better now so they shouldnt but one cannot be sure.

iv. Any delay in notification of EPR will adversely impact tinna's growth rates.

iv. Any delay in notification of EPR will adversely impact tinna's growth rates.

If you find the thread useful, considering following @sahil_vi for similar threads in the future. Please consider retweeting the 1st tweet too. It helps educate more investors.

A thread of all my long analysis threads:

A thread of all my long analysis threads:

Finally, a disclaimer: I am invested & biased. Do your own due diligence before taking any investment decision. I am not a sebi registered advisor. This is not a buy or sell reco. I am free to update my views in real time as facts change without updating anyone.

If i found a better co, id sell tinna tomorrow.

<End of thread, Enjoy your day>

<End of thread, Enjoy your day>

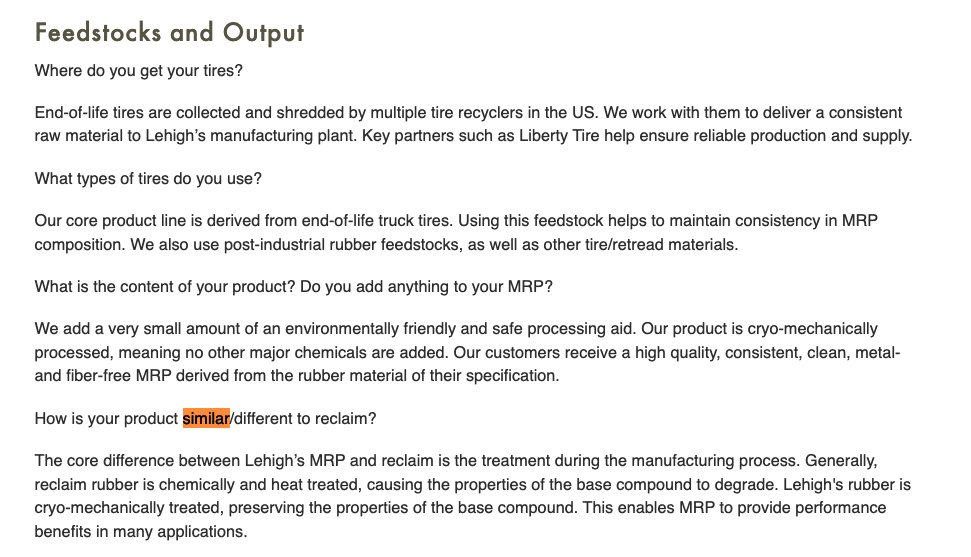

Some interesting differences b/w reclaim rubber & MRP:

lehightechnologies.com

src: vp: forum.valuepickr.com

lehightechnologies.com

src: vp: forum.valuepickr.com

Loading suggestions...