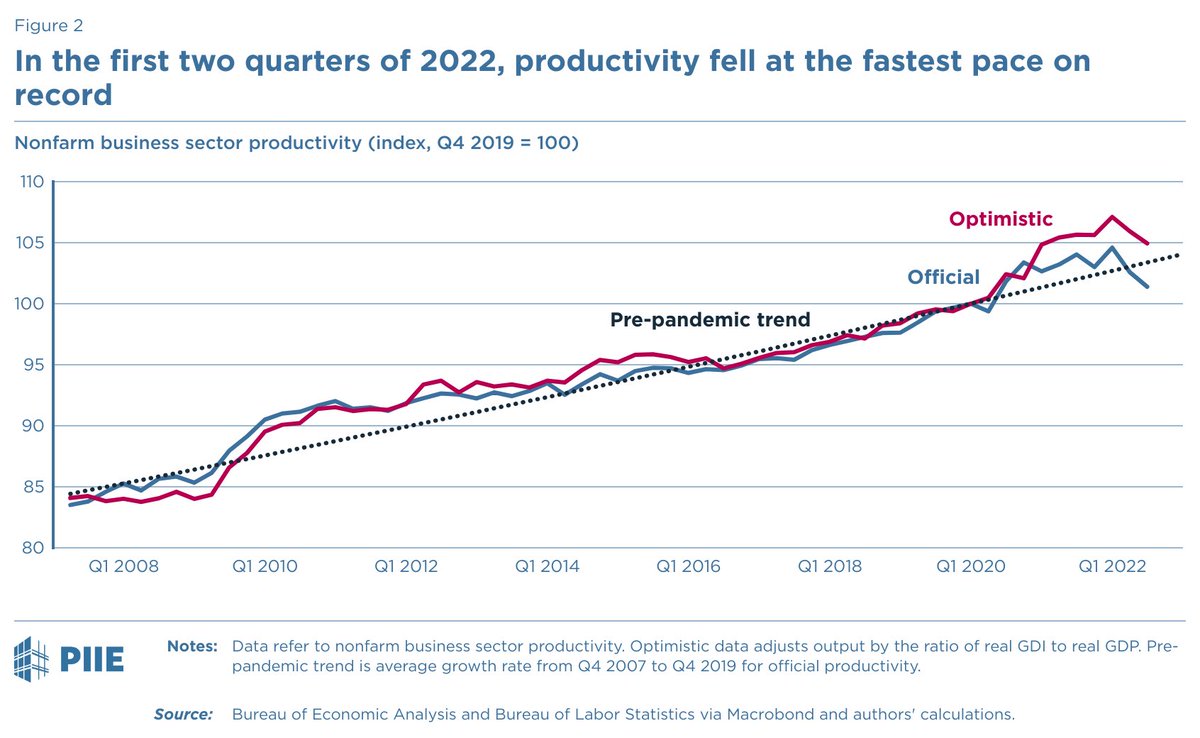

Productivity data is out for Q2 showing (no surprise) the largest two-quarter decline on record. This is true even with a much more optimistic path for output.

This is a risk for inflation and also potentially job growth.

Preview 🧵 of Willie Powell & my forthcoming blog.

This is a risk for inflation and also potentially job growth.

Preview 🧵 of Willie Powell & my forthcoming blog.

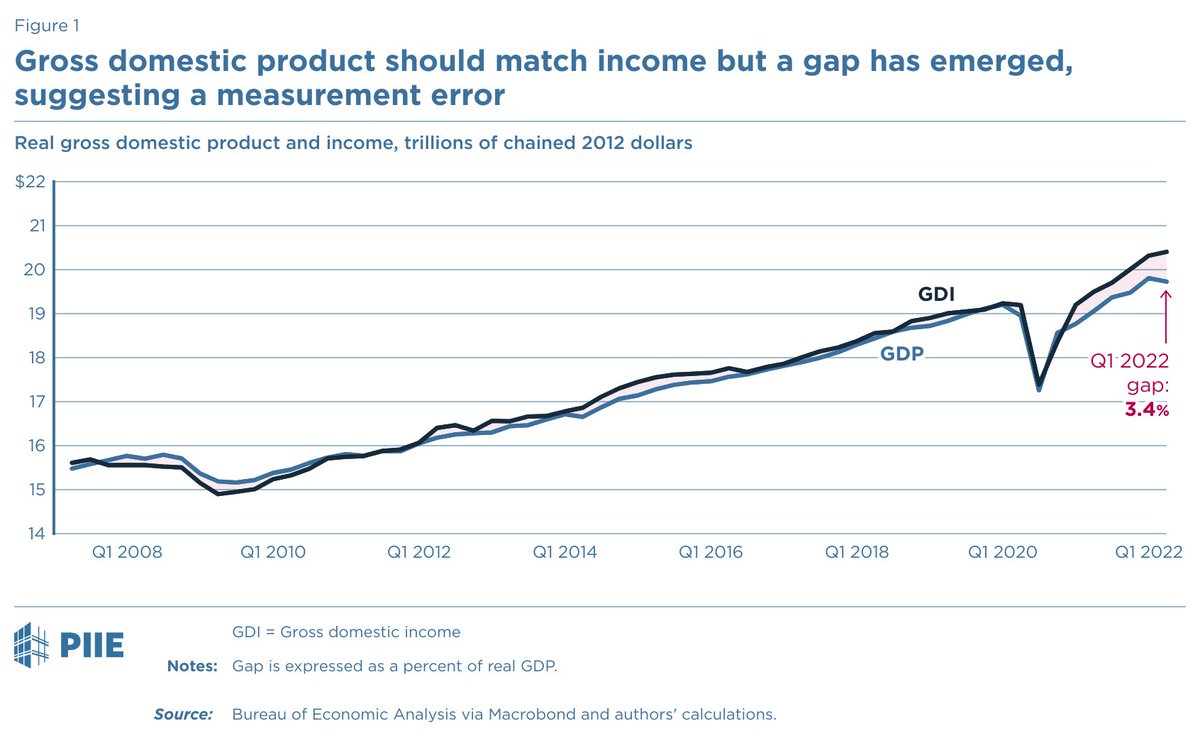

First a caveat: It is unclear if output has been rising or falling because GDP says one thing, GDI says another, and there is a record 3.4% gap between them. My "optimistic" scenario is based on GDI through Q1 and assumed GDI of 0.0% in Q2.

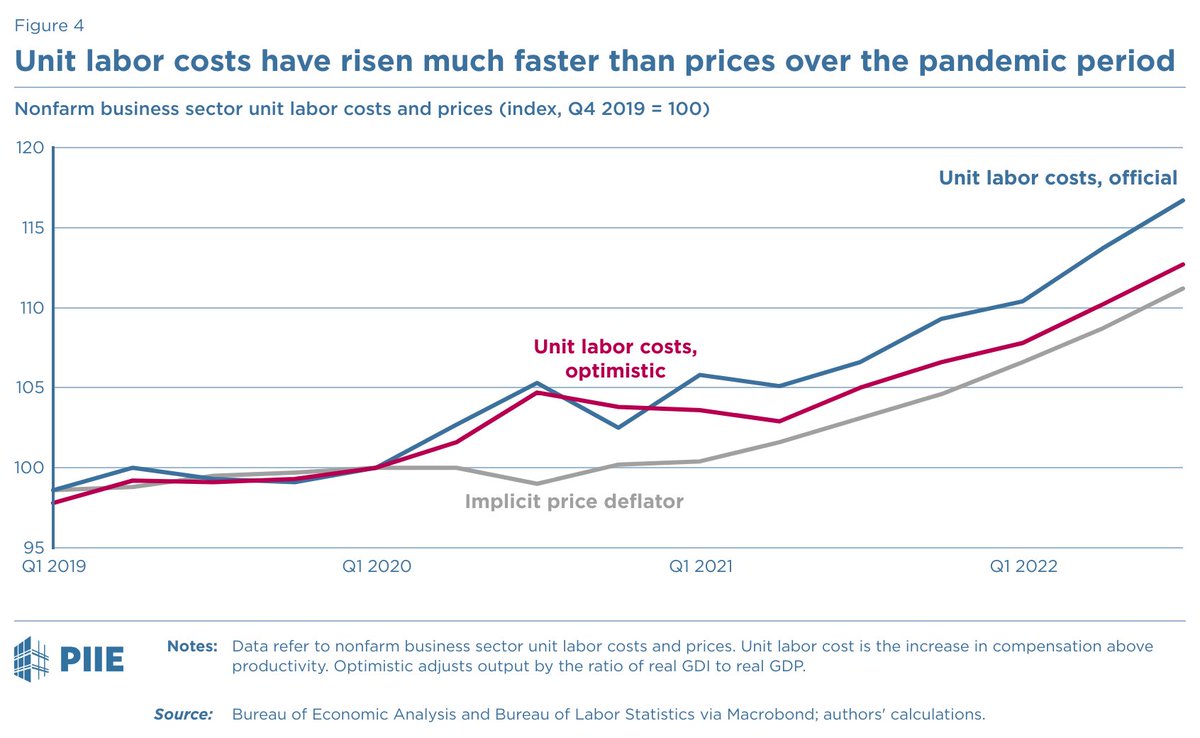

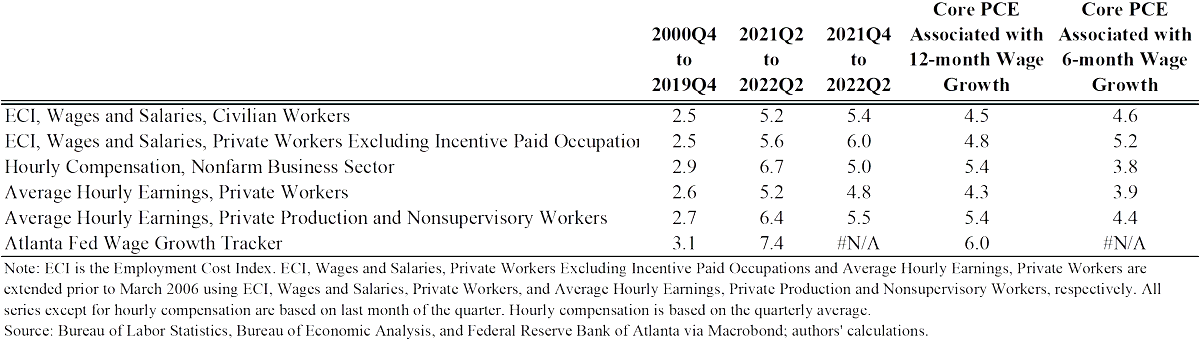

The most worrying fact is that under either measure labor costs (compensation minus the portion of that covered by productivity) have been outstripping price growth.

This suggests we may not have seen the full passthrough of wages to prices yet.

This suggests we may not have seen the full passthrough of wages to prices yet.

This goes the opposite of what many seem to think (which is it is likely to have additional wage growth to make up for inflation). Three issues with that view:

1. Prices measured in a methodologically consistent way for nonfarm business have increased less than the CPI.

1. Prices measured in a methodologically consistent way for nonfarm business have increased less than the CPI.

2. The predictions of wage catchup ignore the fact that labor costs greatly outstripped price growth in 2020 and early 2021. Prices have still not "caught up".

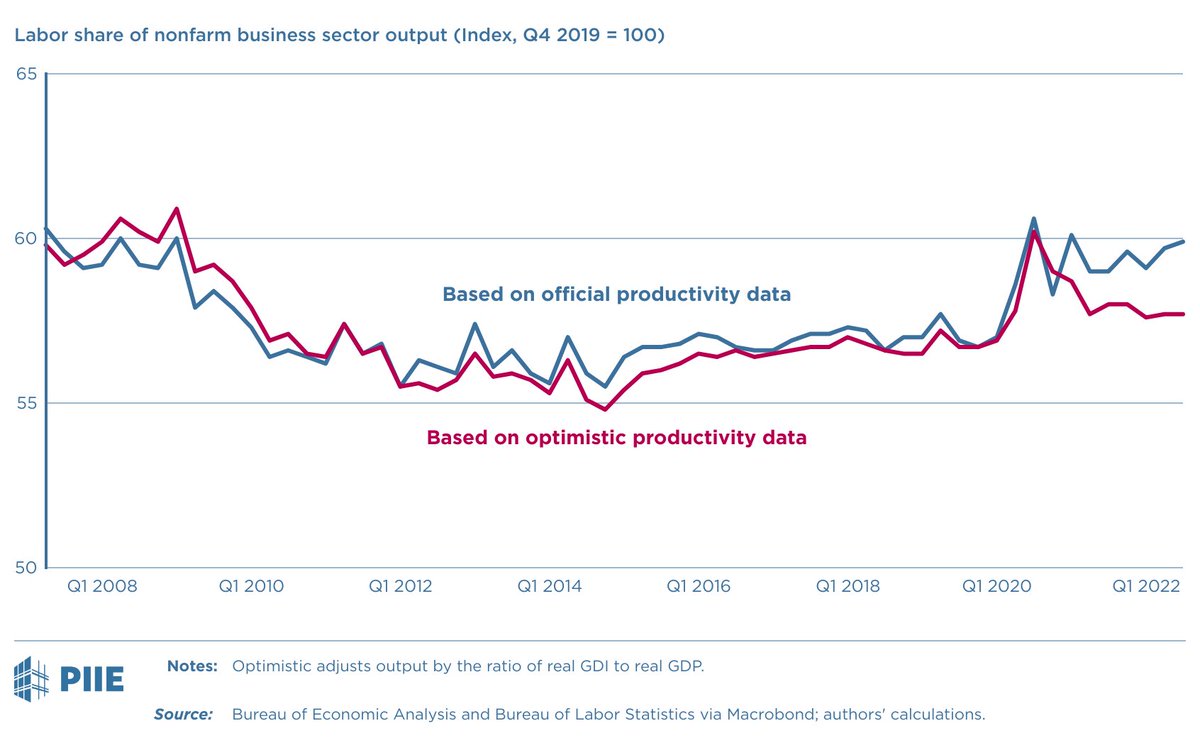

3. The labor share is actually higher than it was prior to the pandemic, possibly by a lot.

3. The labor share is actually higher than it was prior to the pandemic, possibly by a lot.

I would love the labor share to increase but it just is not my best prediction. If anything, it is more likely that the labor share falls as price growth outpaces labor costs for some period going forward.

IF productivity resumes its pre-pandemic pace and the labor share has its pre-pandemic trend and nominal compensation/wage growth stays the same then would expect core PCE inflation of about 4.5 percent, plus or minus.

Any of these assumptions could (and likely will) be wrong. But I fear more likely that productivity is lower than higher. And more likely that wage gains fall further below prices (measured this way) than vice versa. So could be worse.

Back to the productivity numbers, a lot of the big gyrations (big increase in 2021 and big decline in 2022) tell you less about the economy's underlying pace of innovation and more about "residual productivity" as output and hours are moved separately. nber.org

I'm not sure of the exact magnitude of the decline in the first half of 2022 but there is no doubt that output growth was unusually low and job growth was very high--so general conclusion is robust.

I'm less sure where we are relative to pre-pandemic trend productivity. The official series says below while the GDI-based series says above.

Going forward productivity will be among the most important (if most poorly measured) aspects of the economy. It is the major factor in GDP growth and also real wage growth. Plus inflation for any given nominal wage.

But there is some reason to believe that the pandemic period distracted businesses from innovation as they focused on COVID, reduced business investment, continues to weigh on workers with long COVID and disruptive absences, with a big question mark on work from home.

P.S. These data were almost completely predictable from other data the government already released. So it's not a surprise and not market moving. The quarterly numbers are especially volatile. But Willie and I using it to take broader stock of where we are in the economy.

Loading suggestions...