Getting inflation back to 2% will be tough.

Many expect the Fed will never be able to do that, with CPI settling in the 3% area.

But history tells us there is actually a way to get there: a recession.

Let's look at the data with a short thread.

1/

Many expect the Fed will never be able to do that, with CPI settling in the 3% area.

But history tells us there is actually a way to get there: a recession.

Let's look at the data with a short thread.

1/

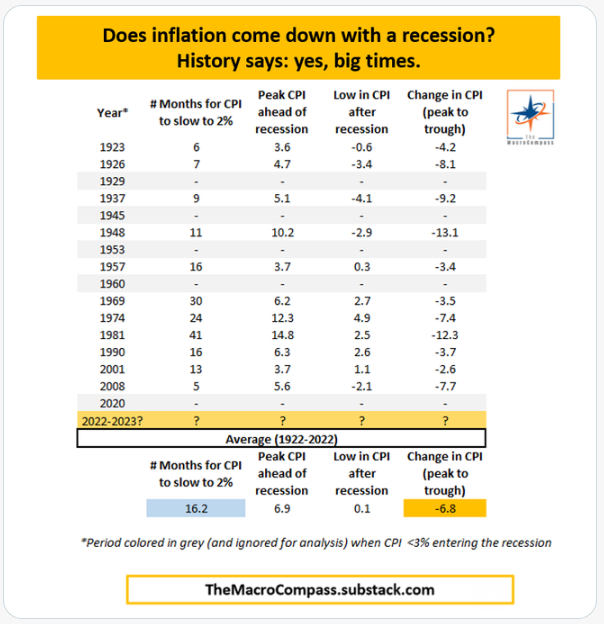

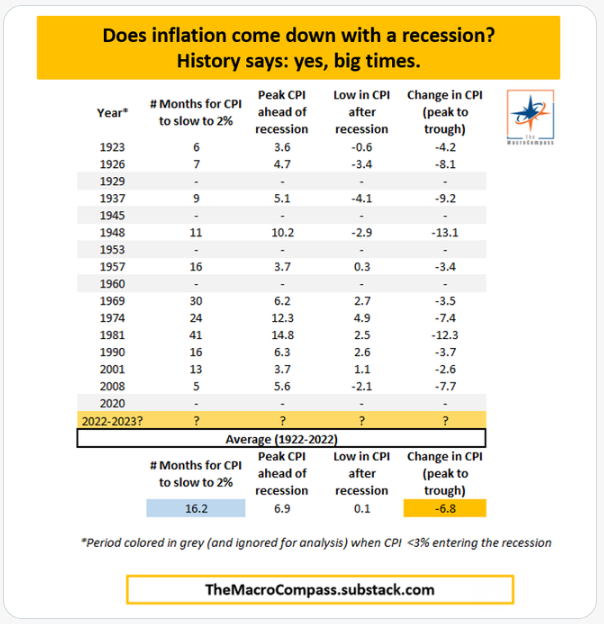

I went back 100 years and looked at all US recession (16) since then.

The idea was to test whether recessions are able to:

- Bring down inflation at all

- If so, to which extent

- How long would it take for CPI to stabilize back to 2%

2/

The idea was to test whether recessions are able to:

- Bring down inflation at all

- If so, to which extent

- How long would it take for CPI to stabilize back to 2%

2/

Here is what I found.

In all 11 episodes when we entered a recession with inflation above 3%, the resulting sharp economic slowdown DID bring inflation down.

On average:

- It took 16.2 months to slow CPI from peak to 2%

- The peak-to-trough reduction in CPI was -6.8%

3/

In all 11 episodes when we entered a recession with inflation above 3%, the resulting sharp economic slowdown DID bring inflation down.

On average:

- It took 16.2 months to slow CPI from peak to 2%

- The peak-to-trough reduction in CPI was -6.8%

3/

Not all recessions are the same.

The mid-70s recession materially slowed down CPI but only managed to bring it down to 4.9%.

In a highly industrialized & labor-intensive economy with strong credit growth and wage bargaining power it can be hard to push CPI down to 2%.

4/

The mid-70s recession materially slowed down CPI but only managed to bring it down to 4.9%.

In a highly industrialized & labor-intensive economy with strong credit growth and wage bargaining power it can be hard to push CPI down to 2%.

4/

The common trait seems to be that big recessions (5%+ drawdown in cumulative GDP) are very time-effective in lowering inflation.

In the 20s-30s and in 2008 it only took 7 months on average to push CPI down from the local peak to 2%.

5/

In the 20s-30s and in 2008 it only took 7 months on average to push CPI down from the local peak to 2%.

5/

What about today?

If we'd get the average recession today, history says we'd be able to lower CPI from roughly 9% to 2% in about 16 months

But given the dispersion in the dataset above, what's the likely path ahead?

A long but shallow recession, a short one or none at all?

6/

If we'd get the average recession today, history says we'd be able to lower CPI from roughly 9% to 2% in about 16 months

But given the dispersion in the dataset above, what's the likely path ahead?

A long but shallow recession, a short one or none at all?

6/

In the 1970s, an unleveraged and industrial-driven economy with strong demographics required long (2y+) recessions to reduce CPI.

Today's economy is vastly different.

If we get one, I'd expect it to be more similar to the 1940s or 2000s episodes.

7/

Today's economy is vastly different.

If we get one, I'd expect it to be more similar to the 1940s or 2000s episodes.

7/

The similarities with the 1940s:

- Exogenous shocks (war, C-19)

- Fiscal and monetary responses, and resulting cliffs

The similarities with the 2000s:

- Economic leverage

- Pre-recession financial market exuberance

8/

- Exogenous shocks (war, C-19)

- Fiscal and monetary responses, and resulting cliffs

The similarities with the 2000s:

- Economic leverage

- Pre-recession financial market exuberance

8/

While regulation is much more prudent now and banks' balance sheets look better than in 2007, the shadow banking system, the Eurodollar market and the total economy leverage have grown substantially.

Plus, the fiscal and monetary cliffs are huge.

9/

Plus, the fiscal and monetary cliffs are huge.

9/

If we'd get one, history suggests that a 12-16 months relatively severe recession should bring inflation down all the way to 2%.

Obviously, there is nothing to be happy about a recession.

10/

Obviously, there is nothing to be happy about a recession.

10/

Credit conditions tighten materially, firms lose access to financing and the labor market & consumers are hit hard too.

The Fed hopes for a soft landing, but a recession might be the price to pay to slow down CPI.

11/

The Fed hopes for a soft landing, but a recession might be the price to pay to slow down CPI.

11/

Next week, I will release a timely article covering the Fed decision and implication for markets on my free newsletter TheMacroCompass.substack.com.

Consider joining 94,000+ macro investors and subscribing, so you'll receive the piece directly in your inbox.

It's free.

12/12

Consider joining 94,000+ macro investors and subscribing, so you'll receive the piece directly in your inbox.

It's free.

12/12

Loading suggestions...