Is ICICI Bank the next HDFC Bank?

Is ICICI Bank the new market leader?

ICICI Bank just posted its results

How do the results compare with HDFC Bank?

A comprehensive thread🧵 analyzing the results of ICICI Bank and the comparison with HDFC Bank

Lets go👇

(1/16)

Is ICICI Bank the new market leader?

ICICI Bank just posted its results

How do the results compare with HDFC Bank?

A comprehensive thread🧵 analyzing the results of ICICI Bank and the comparison with HDFC Bank

Lets go👇

(1/16)

Loan growth:-

ICICI Bank grew loans at 23%

HDFC Bank grew loans at 23.5%

Retail loan growth was 21% for ICICI Bank while

it was 21.5% for HDFC Bank

Corporate loan growth 23% for ICICI Bank

whereas it grew at 27% for HDFC Bank

(2/16)

ICICI Bank grew loans at 23%

HDFC Bank grew loans at 23.5%

Retail loan growth was 21% for ICICI Bank while

it was 21.5% for HDFC Bank

Corporate loan growth 23% for ICICI Bank

whereas it grew at 27% for HDFC Bank

(2/16)

Verdict:-

Both Banks are leading the way in Loan growth

HDFC is covering up the retail growth slowdown over the past two quarters

ICICI is covering up the corporate growth slowdown!

But together both are gaining market share in loans

(3/16)

Both Banks are leading the way in Loan growth

HDFC is covering up the retail growth slowdown over the past two quarters

ICICI is covering up the corporate growth slowdown!

But together both are gaining market share in loans

(3/16)

Deposits:-

ICICI Grew deposits by 12%

HDFC Bank grew deposits by 19%

While both banks continue to gain market share in deposits

HDFC Bank's super impressive deposit grow is an eyecatcher.

(4/16)

ICICI Grew deposits by 12%

HDFC Bank grew deposits by 19%

While both banks continue to gain market share in deposits

HDFC Bank's super impressive deposit grow is an eyecatcher.

(4/16)

Cost of funds:-

ICICI pays nearly 3.58% on incremental deposits

HDFC Bank pays nearly the same on incremental deposits

Cost of funds is not a problem for both banks given the super quality franchise.

(5/16)

ICICI pays nearly 3.58% on incremental deposits

HDFC Bank pays nearly the same on incremental deposits

Cost of funds is not a problem for both banks given the super quality franchise.

(5/16)

Strong capital Adequacy:-

ICICI Bank has TIER-1 capital adequacy of 17.51%

HDFC Bank Bank has TIER-1 capital adequacy of 17.1%

Both banks are well positioned to push loan growth in the coming two years.

(6/16)

ICICI Bank has TIER-1 capital adequacy of 17.51%

HDFC Bank Bank has TIER-1 capital adequacy of 17.1%

Both banks are well positioned to push loan growth in the coming two years.

(6/16)

Asset Quality

HDFC Bank:-

🏦The Gross NPAs fell to 1.23% from 1.35%

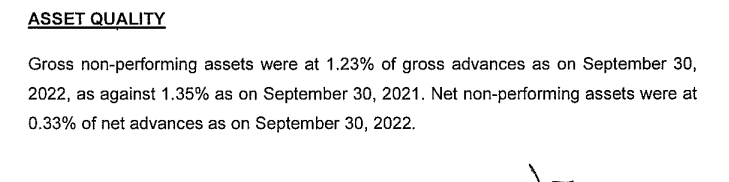

🏦The slippages at 3000cr were down significantly.

🏦The PCR remains extremely strong at 73.2%

🏦The credit cost ratio came in at 0.87%(best in many quarters)

(7/16)

HDFC Bank:-

🏦The Gross NPAs fell to 1.23% from 1.35%

🏦The slippages at 3000cr were down significantly.

🏦The PCR remains extremely strong at 73.2%

🏦The credit cost ratio came in at 0.87%(best in many quarters)

(7/16)

ICICI Bank:-

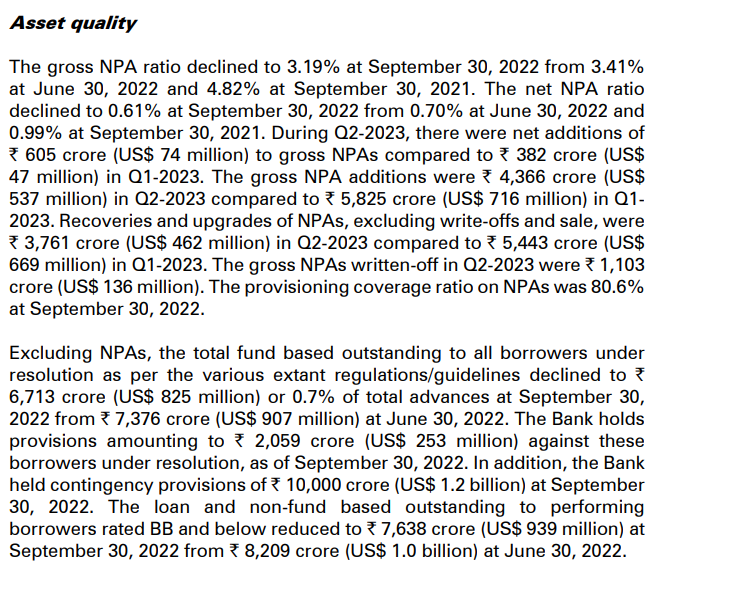

🏦Gross NPAs declined from 3.41% to 3.19%

🏦Slippages came down to 4366cr as compared to 5385cr last quarter

🏦PCR stood at 80.6%

Largely asset quality has remained very strong.

(8/16)

🏦Gross NPAs declined from 3.41% to 3.19%

🏦Slippages came down to 4366cr as compared to 5385cr last quarter

🏦PCR stood at 80.6%

Largely asset quality has remained very strong.

(8/16)

Verdict:-

Asset quality has eased up for both banks

Covid-19 problems are now behind both banks

Slippages are at a multi-quarter low.

Both banks are ready to push loan growth into the system.

(9/16)

Asset quality has eased up for both banks

Covid-19 problems are now behind both banks

Slippages are at a multi-quarter low.

Both banks are ready to push loan growth into the system.

(9/16)

Valuation:-

ICICI Bank is now available at 3x P/B

HDFC Bank is now available at 3x P/B

Given the larger number of subsidiaries of ICICI Bank,it is relatively cheaper than HDFC Bank.

Both Banks are certainly not cheap.

(10/16)

ICICI Bank is now available at 3x P/B

HDFC Bank is now available at 3x P/B

Given the larger number of subsidiaries of ICICI Bank,it is relatively cheaper than HDFC Bank.

Both Banks are certainly not cheap.

(10/16)

Merger Hangover on HDFC Bank:-

1. HDFC book will need CRR+SLR provisions.

The book coming from HDFC ltd doesn't have adequate SLR and CRR provisions.

To make those provisions the bank could need to shore up 80-90000cr of capital.

(11/16)

1. HDFC book will need CRR+SLR provisions.

The book coming from HDFC ltd doesn't have adequate SLR and CRR provisions.

To make those provisions the bank could need to shore up 80-90000cr of capital.

(11/16)

While getting the capital is not a problem.

This is will be a drag on the RoE of the bank in the near term.

The bank has asked for dispensation from the regulator.

However, the regulator is yet to respond.

(12/16)

This is will be a drag on the RoE of the bank in the near term.

The bank has asked for dispensation from the regulator.

However, the regulator is yet to respond.

(12/16)

So which result is better?

HDFC Bank performed better on some parameters than ICICI Bank.

ICICI Bank performed better on come parameters than HDFC Bank.

(13/16)

HDFC Bank performed better on some parameters than ICICI Bank.

ICICI Bank performed better on come parameters than HDFC Bank.

(13/16)

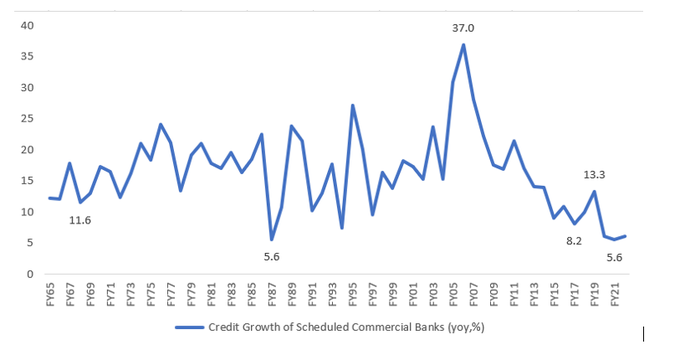

We are at the bottom of a credit cycle.

Credit growth is at a 50-year low.

We need strongly capitalized banks with clean balance sheets to achieve the vision of $5 trillion economy.

(14/16)

Credit growth is at a 50-year low.

We need strongly capitalized banks with clean balance sheets to achieve the vision of $5 trillion economy.

(14/16)

Both ICICI Bank and HDFC have:-

1. Strong Balance Sheet

2. Strong Management

3. Strong capital to deploy

4. Huge physical as well as digital presence to tap growth

(15/16)

1. Strong Balance Sheet

2. Strong Management

3. Strong capital to deploy

4. Huge physical as well as digital presence to tap growth

(15/16)

Analysts will be analysts and try to create narratives.

Why should only one of ICICI or HDFC do well?

Both Banks are extremely strong and the scope of opportunity means that both can do extremely well.

Both ICICI+HDFC COMBO will lead India in the next decade to come!

(16/16)

Why should only one of ICICI or HDFC do well?

Both Banks are extremely strong and the scope of opportunity means that both can do extremely well.

Both ICICI+HDFC COMBO will lead India in the next decade to come!

(16/16)

Loading suggestions...