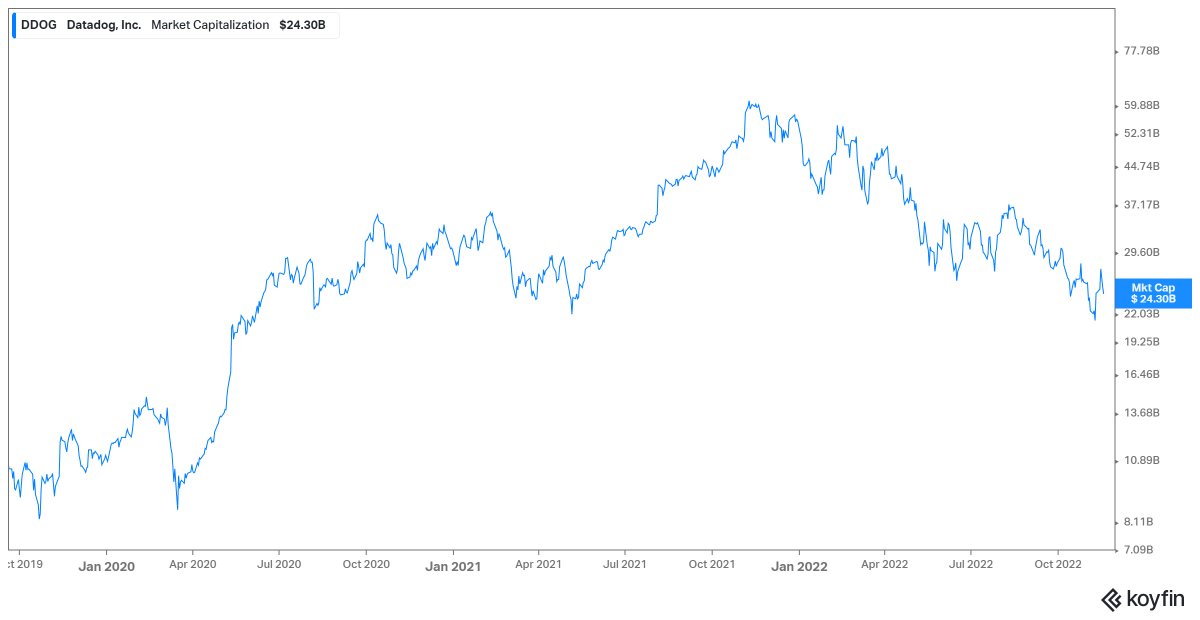

Take $DDOG for example which is widely loved.

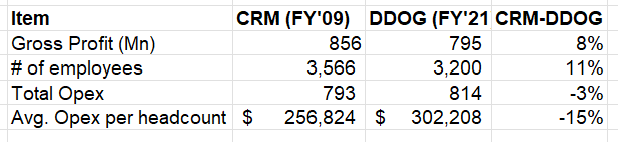

CRM numbers in '09 is more or less similar to DDOG in '21 except Opex per headcount which understandably crept up over time.

Let's start with good news.

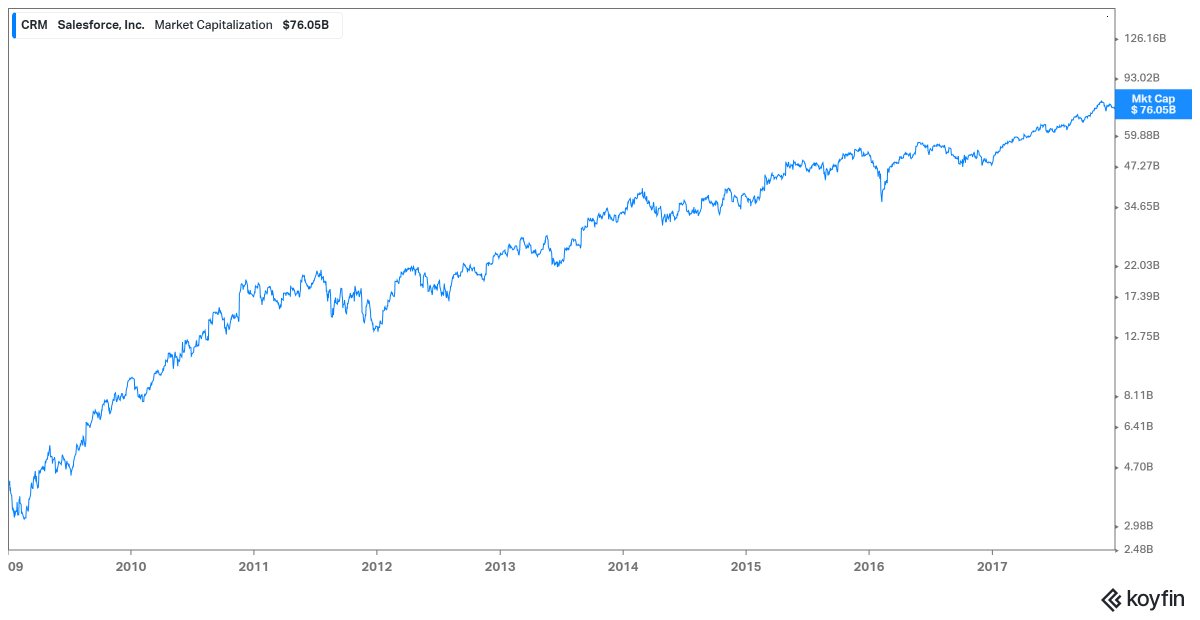

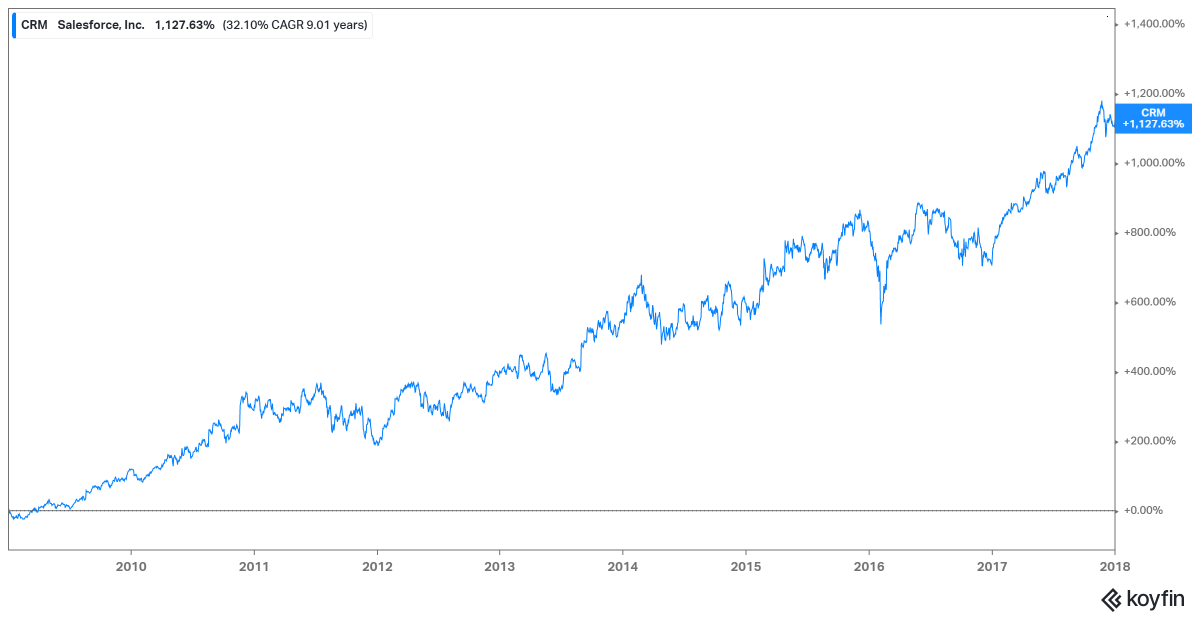

CRM market cap was almost 19x from Jan'09 to Dec'17.

Diluted shares outstanding FY'09: 501 Mn

Diluted shares outstanding FY'18: 700 Mn

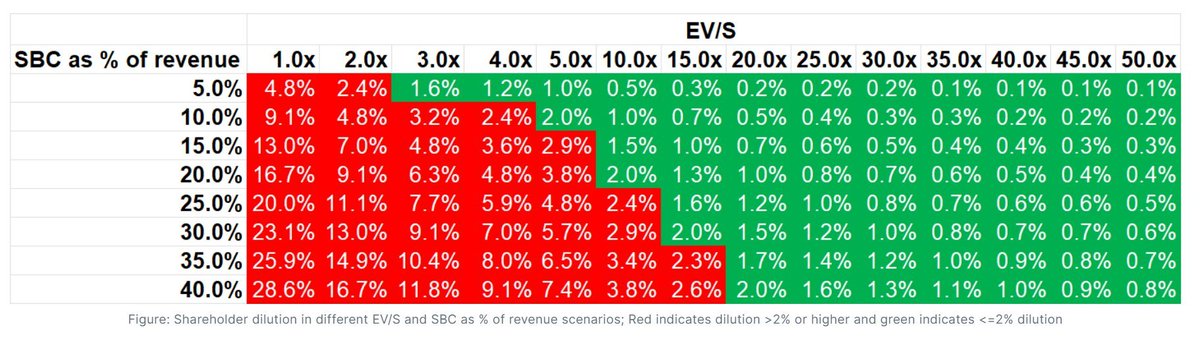

SBC matters (see image).

~11x is still pretty good, so hard to complain too much.

In FY'18, CRM posted ~$7.8 Bn Gross Profit (GP).

To generate this GP, CRM spent $7.3 Bn in opex with ~29k employees. Avg. opex per headcount was ~$270k.

In *2030*, I modeled DDOG

GP $8.6 Bn

Opex $7.2 Bn

# of employees ~26k

Avg. Opex per headcount ~$300k (same as it was in 2021)

As you can see, entry prices of CRM (~$4 Bn in Jan'09; was $8-10 Bn in much of '08-'10) vs DDOG are VERY different even though operating # are similar

But that's EV (or market cap to keep things simple).

For the stock to double, market cap probably needs to be even higher as DDOG mentioned they're targeting ~3-5% dilution each year.

And 10-year treasury yield in 2017 was ~2.0-2.5%. If it were ~4% as it is today, CRM's market cap would obviously be lower then.

~35x *2030* GAAP EBIT for not even a double? Well, you can pay ~35x *NTM* AWS GAAP EBIT to buy the whole $AMZN today

mbi-deepdives.com

Recent Threads

I’ve recently seen a lot of people criticizing smaller indie projects for releasing merchandise or doing kickstarter funding to fund their projects. T...

I compiled all the specific references I noticed in May's moveset! #イニブ #g_bd #g_bdr #GBDR https://t.co/PvNHzH6yj6

taekook taguan ng anak au wherein jk received a surprising gift from their xmas party… [ christmas special 🎄] https://t.co/WY3C450KpV

@HitWithAHeart I hear him before I see him. The weight of his steps on the stairs. Slower than usual. Measured. Like he’s already bracing for whatev...

(1/7) I'm not going to do a full trailer breakdown for Zach Cregger's Resident Evil film, since we have an early form of the script you can place a lo...

Nikola Jokic is 0-6 against 50+ win teams in the playoffs. https://t.co/l5hCeVCoUj

Popular Threads

ICT’s 2022 Mentorship Summarized: https://t.co/zFJCgIfDAR

Winning the Chevening Scholarship + 12 Strong Samples of the Chevening Essay There are four important Essays on the Chevening Scholarship application...

A thread: Pakistani newspaper Dawn's front pages from 4th december 1971 to 20 December to see how they kept their own people in the dark. This was on...

1. There are more people added on the list of arrests and executions of famous people but no further intel is available at this time. ARRESTS and EXE...

Ware County, Ga has broken the Dominion algorithm: Using sequestered Dominion Equipment, Ware County ran a equal number of Trump votes and Biden vote...

The ICT Mentorship Core Content Month 1 Summarized: https://t.co/6tXJxPMDhm