Japan will now allow 10-year yields to trade as high as 0.50%.

And while this seems like a minor policy change, it is likely to cause some serious market volatility.

Why?

A thread.

1/

And while this seems like a minor policy change, it is likely to cause some serious market volatility.

Why?

A thread.

1/

For years, Japan implemented an aggressively dovish monetary policy stance.

Bank of Japan rates were effectively pinned at 0% for decades.

Large-scale QE was standard practice, and a few years ago the BoJ switched to Yield Curve Control.

2/

Bank of Japan rates were effectively pinned at 0% for decades.

Large-scale QE was standard practice, and a few years ago the BoJ switched to Yield Curve Control.

2/

This was necessary as permanent QE had led the BoJ to own >50% of the Japanese government bond market, and buying more bonds would seriously alter the functioning of the market.

For days, there were basically no trades happening in the Japanese government bond (JGB) market.

3/

For days, there were basically no trades happening in the Japanese government bond (JGB) market.

3/

So to keep 10-year yields low, the Bank of Japan moved from targeting a quantity of bonds to buy (QE) to a qualitative measure (YCC).

It succeeded: between 2016 and today, 10-year JGBs traded between -25 and +25 bps like the BoJ wanted.

Why does this matter?

4/

It succeeded: between 2016 and today, 10-year JGBs traded between -25 and +25 bps like the BoJ wanted.

Why does this matter?

4/

Japan is a huge exporter of capital

Since the '90s, Japanese investors are used to look abroad for opportunities to deploy their domestic excess savings

When doing so, they consider both yield differentials and the cost of hedging for foreign currency risks

For instance...

5/

Since the '90s, Japanese investors are used to look abroad for opportunities to deploy their domestic excess savings

When doing so, they consider both yield differentials and the cost of hedging for foreign currency risks

For instance...

5/

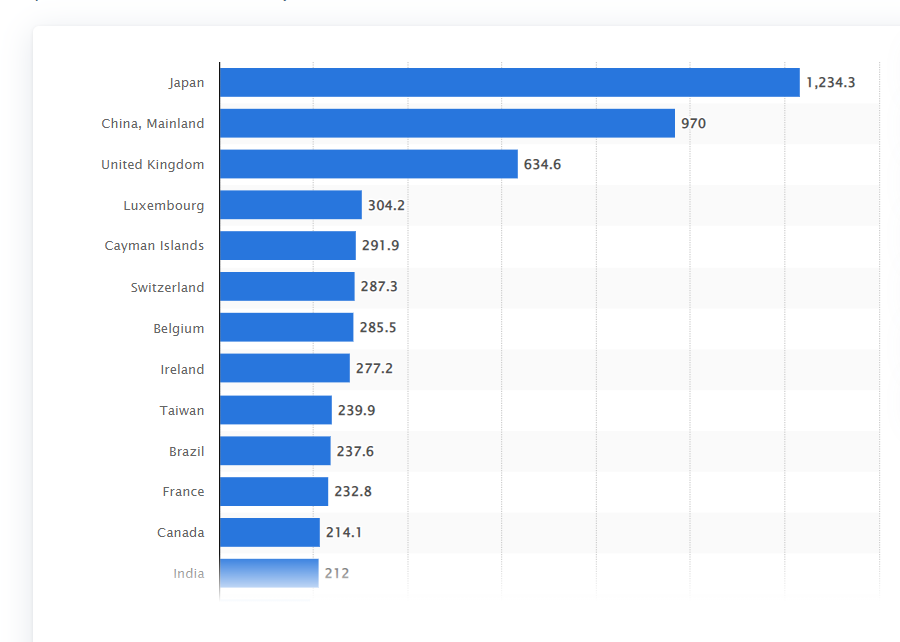

...as of July 2022 Japan is the largest holder of US Treasuries in the world

Japan has accumulated over $1 trillion in USTs as it's a convenient way to recycle excess savings: yield differentials were positive, and often more than offsetting the cost of hedging USD/JPY risks

6/

Japan has accumulated over $1 trillion in USTs as it's a convenient way to recycle excess savings: yield differentials were positive, and often more than offsetting the cost of hedging USD/JPY risks

6/

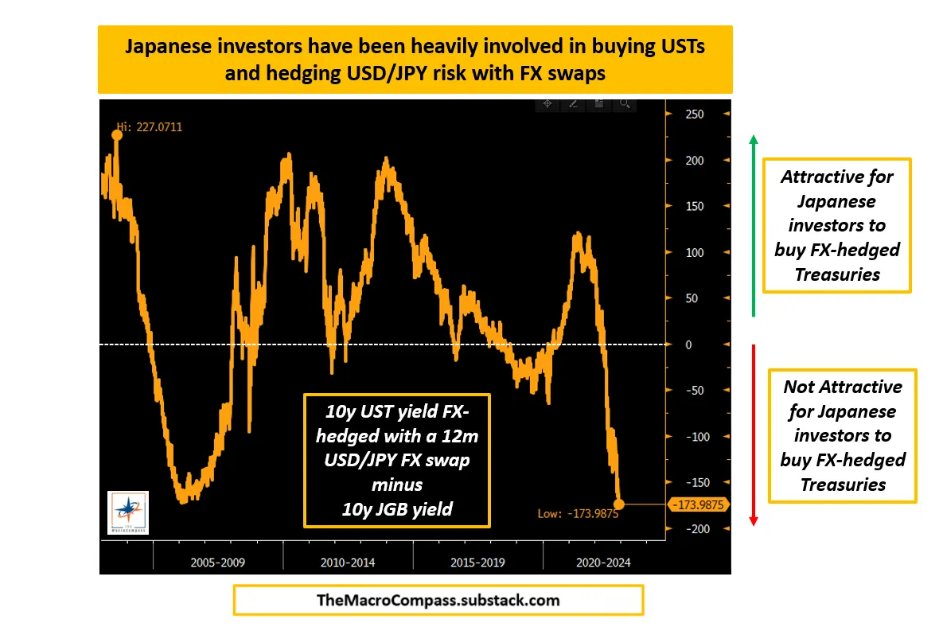

The chart below shows how convenient it was for Japanese investors to buy Treasuries and cover the FX risks.

They would on average get a 100-150 bps additional return than simply buying domestic government bonds.

The BoJ decision today impacts this flow of capital.

7/

They would on average get a 100-150 bps additional return than simply buying domestic government bonds.

The BoJ decision today impacts this flow of capital.

7/

Kuroda announced that 10-year JGB can now trade between -0.50% and +0.50%, hence widening the band for YCC.

This is what bond futures thought about it.

It was a true surprise: but why did he choose to do it now?

8/

This is what bond futures thought about it.

It was a true surprise: but why did he choose to do it now?

8/

Core inflation is rising in Japan, and many analysts expect it to be stable around 2% in 2023.

After years of relentless easing, Kuroda can likely claim ''job done'' and set the stage for his successor to set a new monetary policy in 2023.

A ''victory lap'', if you wish...

9/

After years of relentless easing, Kuroda can likely claim ''job done'' and set the stage for his successor to set a new monetary policy in 2023.

A ''victory lap'', if you wish...

9/

Now, let me show what the bond market really thinks about this BoJ decision.

First: while economists and policymakers are more convinced inflation will sit at 2% in Japan next year, inflation swap traders disagree.

1% CPI priced in late 2023 / beginning 2024.

10/

First: while economists and policymakers are more convinced inflation will sit at 2% in Japan next year, inflation swap traders disagree.

1% CPI priced in late 2023 / beginning 2024.

10/

Nevertheless, as the BoJ controls half the domestic bond market and it says a new monetary policy regime is applicable - bond markets have to adjust to that.

In Japan, it's very useful to look at swaps rather than bonds - the BoJ doesn't influence that market directly...

11/

In Japan, it's very useful to look at swaps rather than bonds - the BoJ doesn't influence that market directly...

11/

...hence it's a cleaner signal of what fixed income investors are pricing in

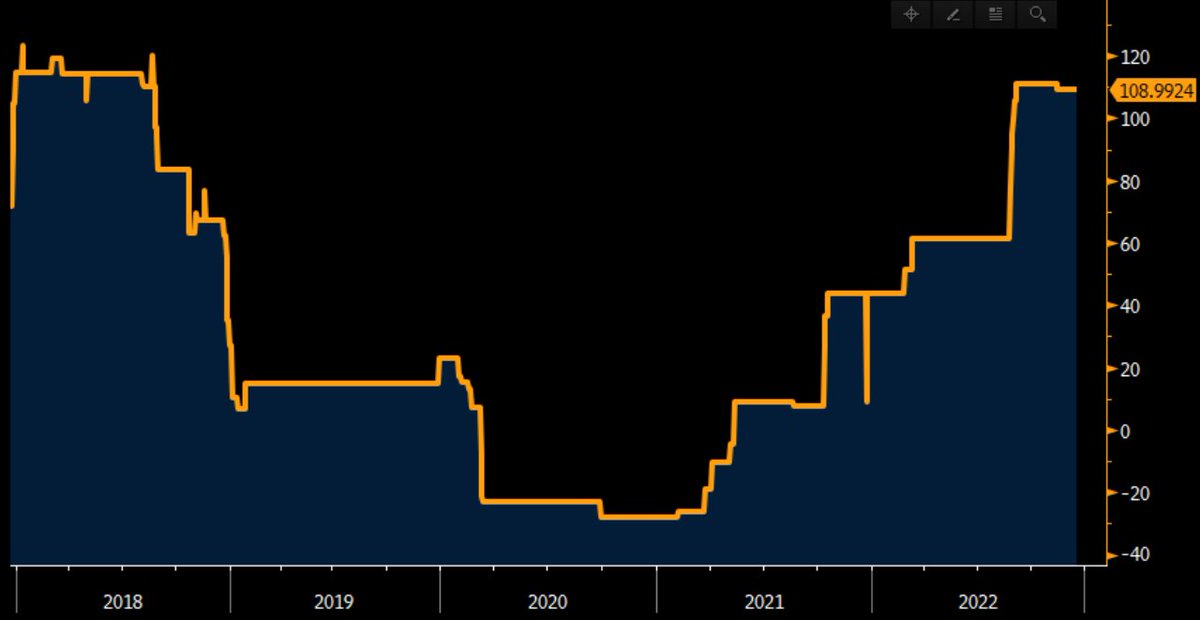

First: what about the front-end?

One thing is for the BoJ to change the 10y trading band, the other is to hike rates: will they?

Bond market says yes: 35 bps of hikes are priced in the next year

12/

First: what about the front-end?

One thing is for the BoJ to change the 10y trading band, the other is to hike rates: will they?

Bond market says yes: 35 bps of hikes are priced in the next year

12/

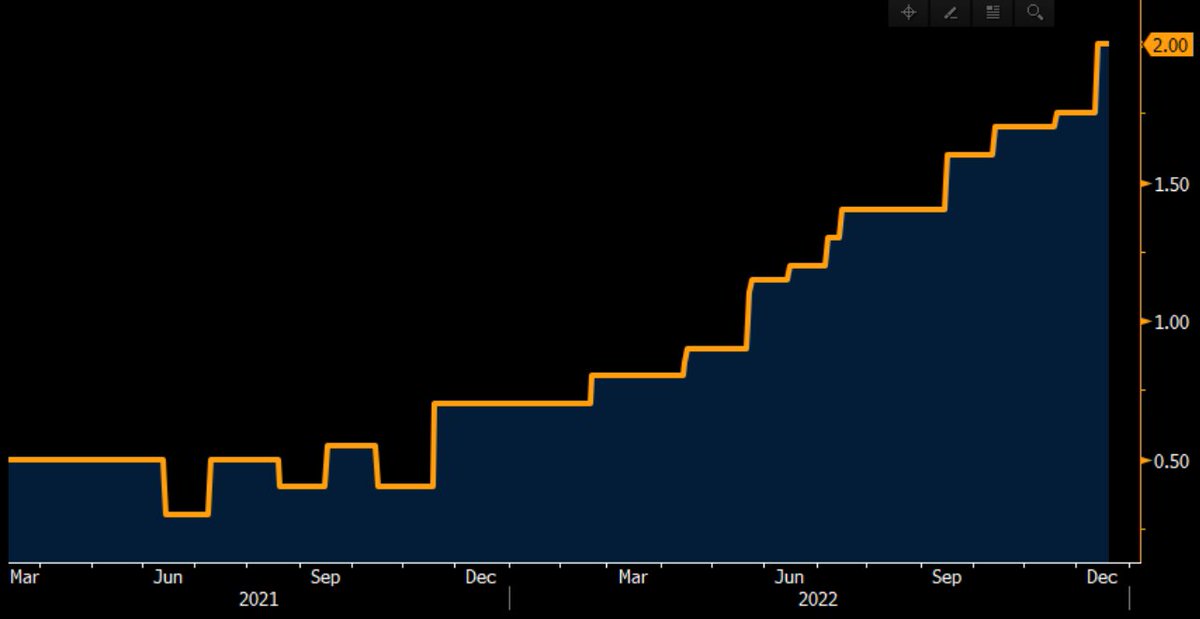

What about the long-end?

We have already seen the sharp reaction in JGB futures, and swap markets are pricing the BoJ to further move the trading band allowing 10-year JGBs to trade around 1% in '23

Bond markets are preparing for higher volatility: look at this chart...

13/

We have already seen the sharp reaction in JGB futures, and swap markets are pricing the BoJ to further move the trading band allowing 10-year JGBs to trade around 1% in '23

Bond markets are preparing for higher volatility: look at this chart...

13/

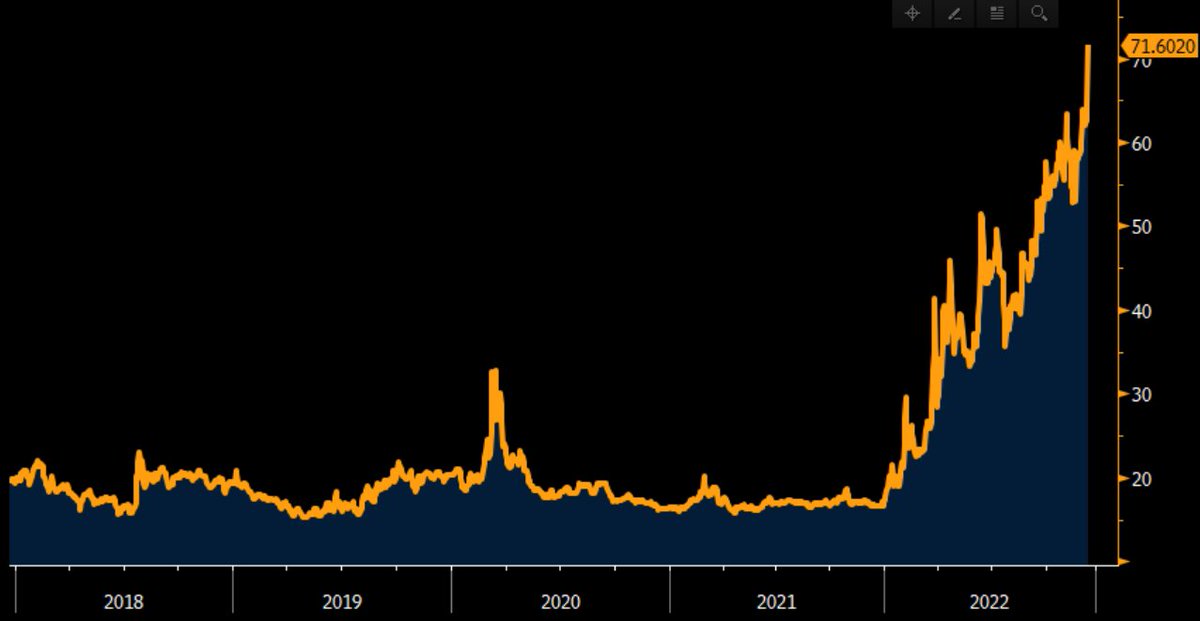

...which shows the implied volatility for the next 12 months priced in for 10-year Japanese government bonds.

It's literally 3x (!) what was priced at the beginning of 2022.

In other words...

14/

It's literally 3x (!) what was priced at the beginning of 2022.

In other words...

14/

...despite being hesitant in pricing sustainably higher inflation in Japan, markets are listening to the BoJ and adjusting for a new monetary policy regime in Japan.

The impact for global markets is very big.

Why?

15/

The impact for global markets is very big.

Why?

15/

Now that Japanese investors are getting positively rewarded to keep their cash at home during a global economic slowdown and periods of high macro uncertainty...

...they probably will choose to do that more.

That strengthens the Yen, and negatively affects foreign assets.

16/

...they probably will choose to do that more.

That strengthens the Yen, and negatively affects foreign assets.

16/

When one of the largest capital exporters in the world decides to domestically reward savings with a higher risk-free rate, there are big macro consequences.

Sign up to TheMacroCompass.substack.com as I will soon be releasing a deep dive on the BoJ decision there - it's free!

17/17

Sign up to TheMacroCompass.substack.com as I will soon be releasing a deep dive on the BoJ decision there - it's free!

17/17

Loading suggestions...