The P/E ratio sucks

It’s a metric that easily deceives investors

Here are 8 reasons why the P/E ratio can be INCREDIBLY misleading (and what metrics to use instead): ⤵️

It’s a metric that easily deceives investors

Here are 8 reasons why the P/E ratio can be INCREDIBLY misleading (and what metrics to use instead): ⤵️

What is the P/E ratio?

P/E stands for “price-to-earnings”

It’s a simple metric for determining a company’s current valuation

It divides the stock price by the last 12 months of earnings per share

P/E stands for “price-to-earnings”

It’s a simple metric for determining a company’s current valuation

It divides the stock price by the last 12 months of earnings per share

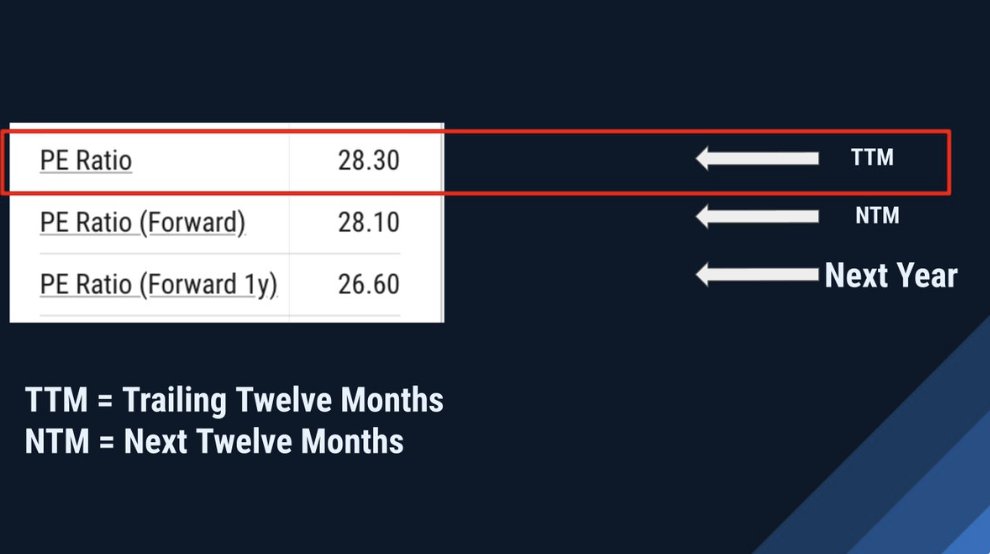

There are 3 main P/E ratios

They all use a different denominator

1: P/E TTM earnings (actual)

2: P/E Forward: NTM earnings (estimates)

3: P/E Forward 1 yr: Next Fiscal Year earnings (estimates)

#1 is the most popular & referenced by far

They all use a different denominator

1: P/E TTM earnings (actual)

2: P/E Forward: NTM earnings (estimates)

3: P/E Forward 1 yr: Next Fiscal Year earnings (estimates)

#1 is the most popular & referenced by far

What’s wrong with the P/E ratio?

It all boils down to the many ways that “Earnings” can be misleading

If “Earnings” aren’t sustainable or are artificially inflated/depressed, the P/E ratio doesn’t work

It all boils down to the many ways that “Earnings” can be misleading

If “Earnings” aren’t sustainable or are artificially inflated/depressed, the P/E ratio doesn’t work

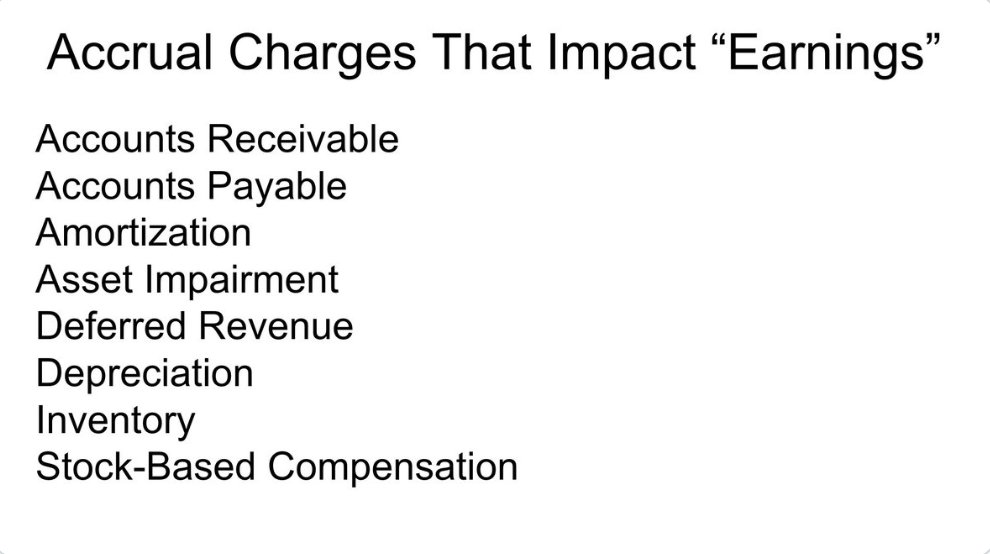

1: Accrual Accounting

The GAAP income statement uses accrual accounting

Accrual accounting is useful, but it’s basically an accountant’s opinion

There are lots of charges that can cause reported “Earning” to be higher or lower than the actual cash flow of a business

The GAAP income statement uses accrual accounting

Accrual accounting is useful, but it’s basically an accountant’s opinion

There are lots of charges that can cause reported “Earning” to be higher or lower than the actual cash flow of a business

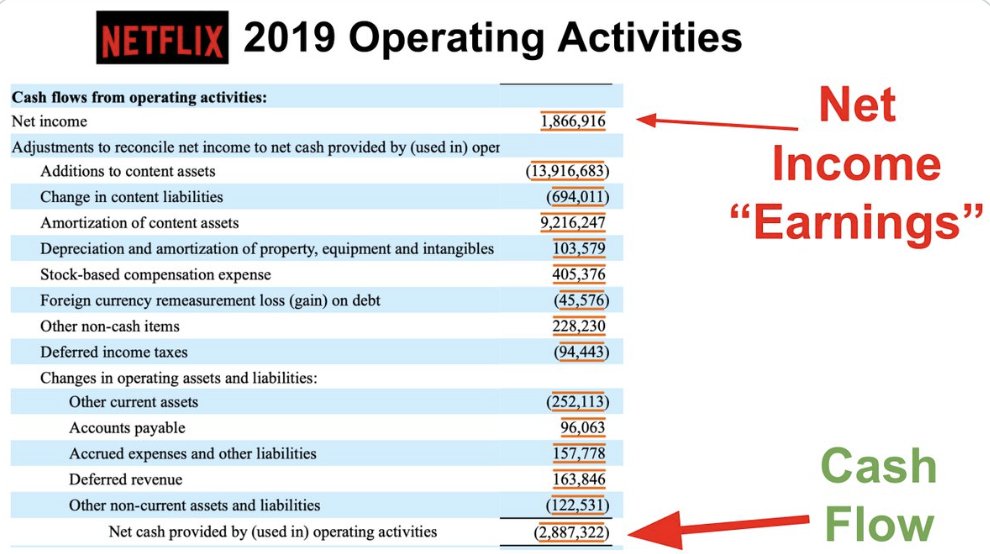

Ex: In 2019, $NFLX reported $1.9 billion in earnings, but its operating cash flow was NEGATIVE $2.9 billion

While it was “profitable” on a net income basis, its actual cash outflow was enormous

The P/E ratio doesn’t reflect this at all

While it was “profitable” on a net income basis, its actual cash outflow was enormous

The P/E ratio doesn’t reflect this at all

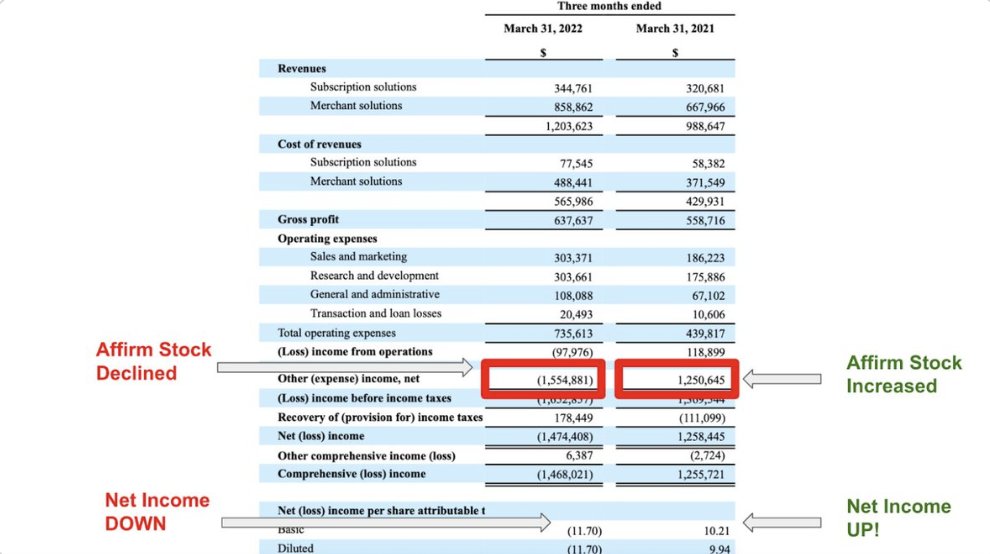

2: Equity investments

Some companies buy stock in other businesses

Ex: $SHOP owns a bunch of $AFRM stock

GAAP accounting requires that companies mark UP their “other income” when their investments increase in value and DOWN when they decline

Some companies buy stock in other businesses

Ex: $SHOP owns a bunch of $AFRM stock

GAAP accounting requires that companies mark UP their “other income” when their investments increase in value and DOWN when they decline

This is doing WILD things to $SHOP EPS, which makes its P/E ratio all but useless

The same is true for $AMZN, $BRK, $GOOG, $ABMD, and more

The same is true for $AMZN, $BRK, $GOOG, $ABMD, and more

3: One-time events

Ever receive a windfall?

Lottery? Bonus? Inheritance?

Companies receive windfalls from taxes, asset sales, and one-off deals

When this happens, “earnings” can SKYROCKET

Ever receive a windfall?

Lottery? Bonus? Inheritance?

Companies receive windfalls from taxes, asset sales, and one-off deals

When this happens, “earnings” can SKYROCKET

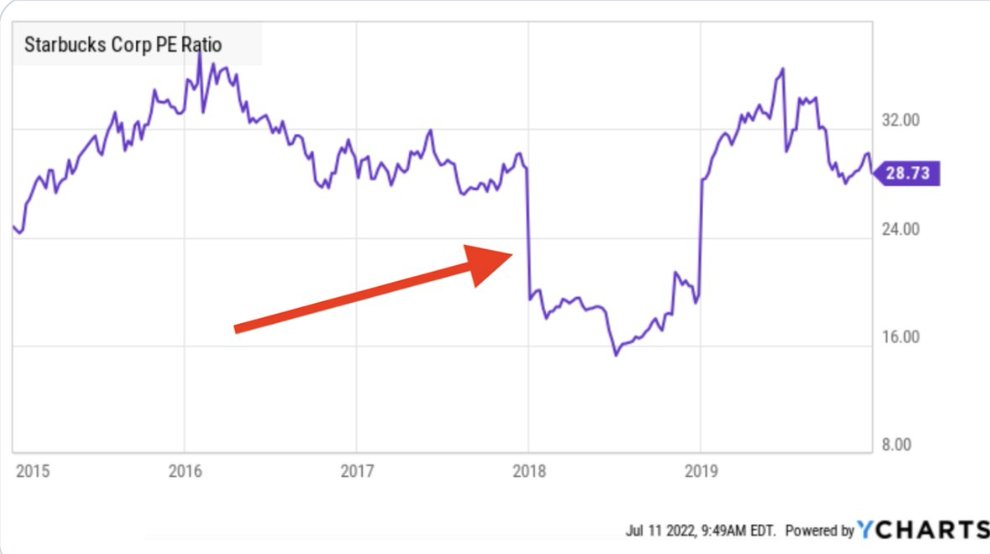

This happened to $SBUX in 2018

They received a $1.4 billion payment from a joint venture with Nestle

These HUGELY boosted earnings, which artificially DEPRESSED the P/E that whole year

During the year, the P/E ratio was artificially LOW, and it was a deceiving metric

They received a $1.4 billion payment from a joint venture with Nestle

These HUGELY boosted earnings, which artificially DEPRESSED the P/E that whole year

During the year, the P/E ratio was artificially LOW, and it was a deceiving metric

4: Unsustainable trend

Sometimes businesses ride a short-term trend that causes profits to boom

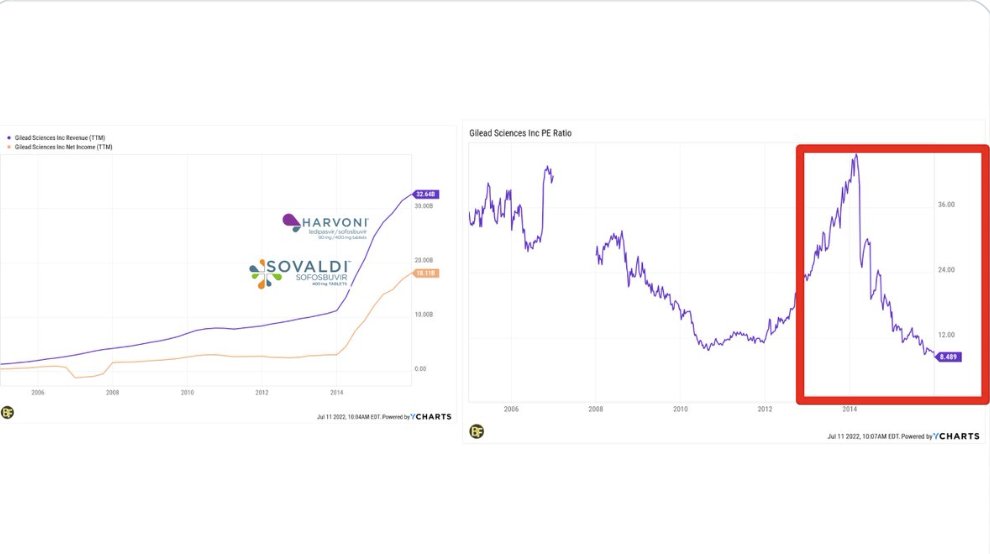

Ex: $GILD in 2014

It launched two blockbuster drugs that cured patients of Hepatitis-C

Revenue & profits EXPLODED, which caused the P/E ratio to sink to just 8!

Sometimes businesses ride a short-term trend that causes profits to boom

Ex: $GILD in 2014

It launched two blockbuster drugs that cured patients of Hepatitis-C

Revenue & profits EXPLODED, which caused the P/E ratio to sink to just 8!

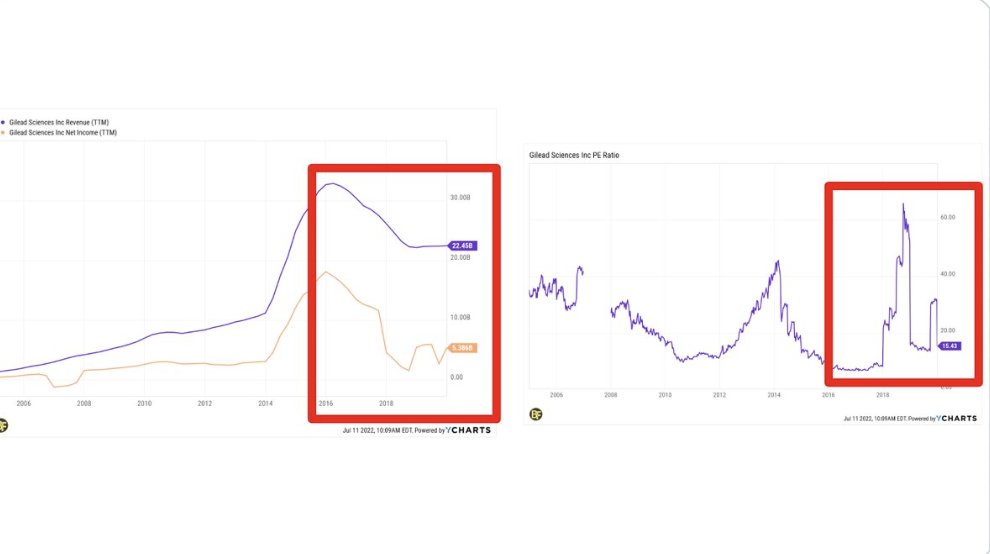

But, Gilead was riding an unsustainable trend

Competition soon entered, which drove prices down, down, down

Revenue & profits fell sharply, which cause the P/E ratio to expand

If you bought because of the “cheap” P/E ratio (like me), you did poorly

Competition soon entered, which drove prices down, down, down

Revenue & profits fell sharply, which cause the P/E ratio to expand

If you bought because of the “cheap” P/E ratio (like me), you did poorly

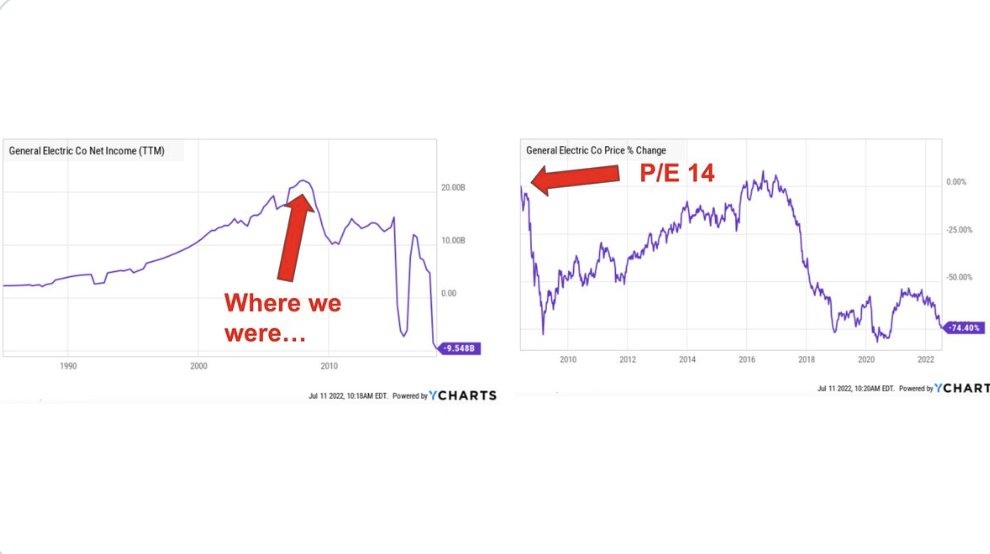

5: Disruption

Sometimes a company’s earnings are in a permanent state of decline due to disruption

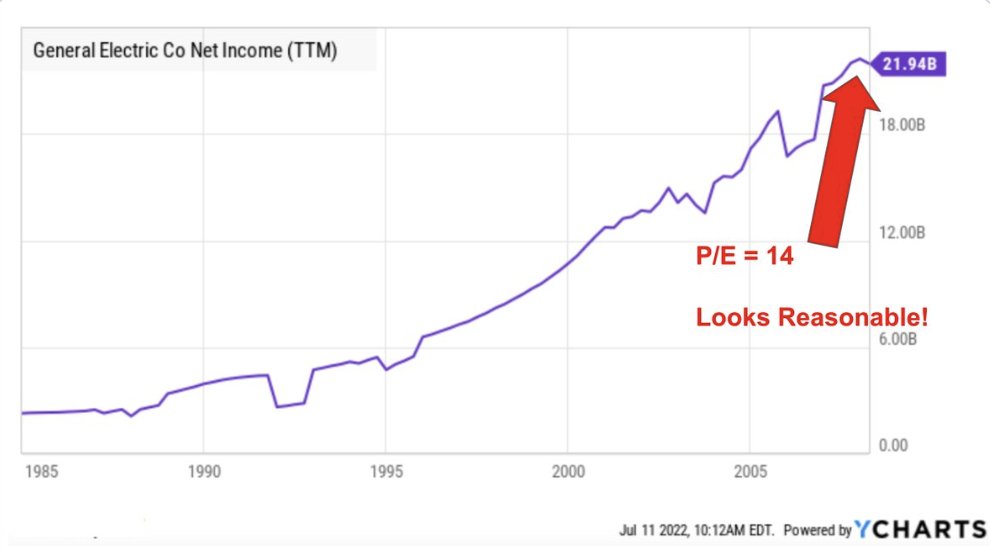

Consider what has happened to $GE

Net income had grown for a century+, and in 2008 its P/E ratio was just 14. Reasonable!

Sometimes a company’s earnings are in a permanent state of decline due to disruption

Consider what has happened to $GE

Net income had grown for a century+, and in 2008 its P/E ratio was just 14. Reasonable!

It turns out that $GE made a series of big bets that didn’t pay off, partially due to disruption

Net income was at a peak

Shareholders are down ~70+% since they, even though they thought they were buying a “blue chip” at a reasonable P/E ratio

Net income was at a peak

Shareholders are down ~70+% since they, even though they thought they were buying a “blue chip” at a reasonable P/E ratio

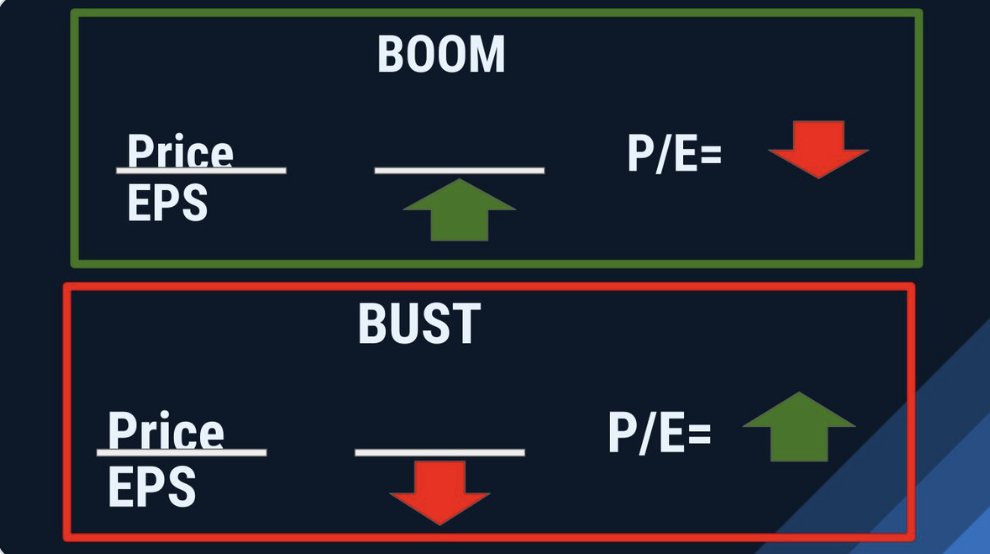

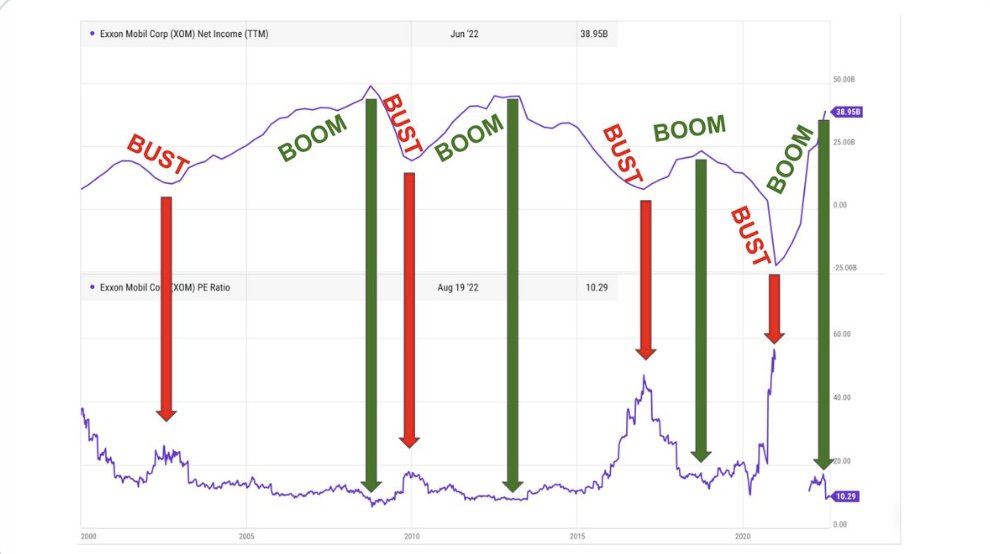

6: Cyclical demand

Some industries are prone to frequent booms and busts

Earnings explode during boom times and crash during bust times

For these companies, the P/E ratio literally works backward

Some industries are prone to frequent booms and busts

Earnings explode during boom times and crash during bust times

For these companies, the P/E ratio literally works backward

Consider $XOM

Profits surges when energy prices are high and sink when they fall

The worst time to invest is at a cyclical peak, which is when the P/E ratio looks cheapest (the inverse is also true)

Profits surges when energy prices are high and sink when they fall

The worst time to invest is at a cyclical peak, which is when the P/E ratio looks cheapest (the inverse is also true)

7: Industries Dynamics

There are several industries where the P/E ratio just doesn’t work because of the nature of the industry

Ex:

Banks: Credit cycles

Biotech: Losses, then a big payout

REITs: High depreciation charges

For these industries, the P/E ratio doesn't work

There are several industries where the P/E ratio just doesn’t work because of the nature of the industry

Ex:

Banks: Credit cycles

Biotech: Losses, then a big payout

REITs: High depreciation charges

For these industries, the P/E ratio doesn't work

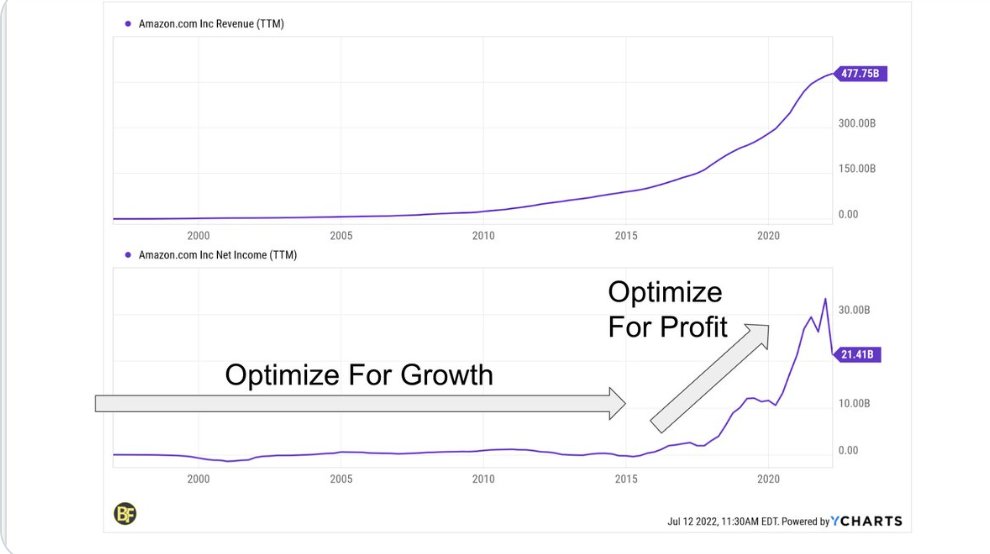

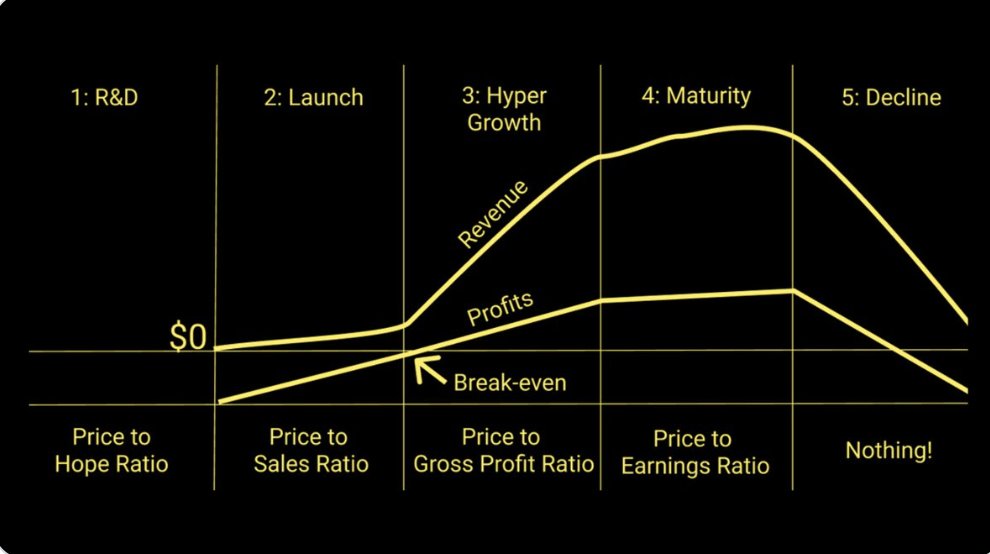

8: Business Growth Cycle

When a new company is created, it is optimized for GROWTH, not profits

Management plows all available resources into hiring & expansion

This artificially UNDERSTATES the true earnings power of the business, which artificially OVERSTATES the P/E ratio

When a new company is created, it is optimized for GROWTH, not profits

Management plows all available resources into hiring & expansion

This artificially UNDERSTATES the true earnings power of the business, which artificially OVERSTATES the P/E ratio

Look at $AMZN

For decades, the company was optimized for growth, not earnings, so the P/E ratio looked crazy

In 2017, it finally started to optimize for earnings

For decades, the company was optimized for growth, not earnings, so the P/E ratio looked crazy

In 2017, it finally started to optimize for earnings

Even today, $AMZN is dealing with overspending from the COVID boom. It’s still NOT optimized for earnings

The P/E ratio will only be useful once the true earnings power of the business shines through

The P/E ratio will only be useful once the true earnings power of the business shines through

What can investors do about this?

Learn when the P/E ratio is USEFUL and when it’s USELESS

Use other metrics when earnings are overstated/understated

Learn when the P/E ratio is USEFUL and when it’s USELESS

Use other metrics when earnings are overstated/understated

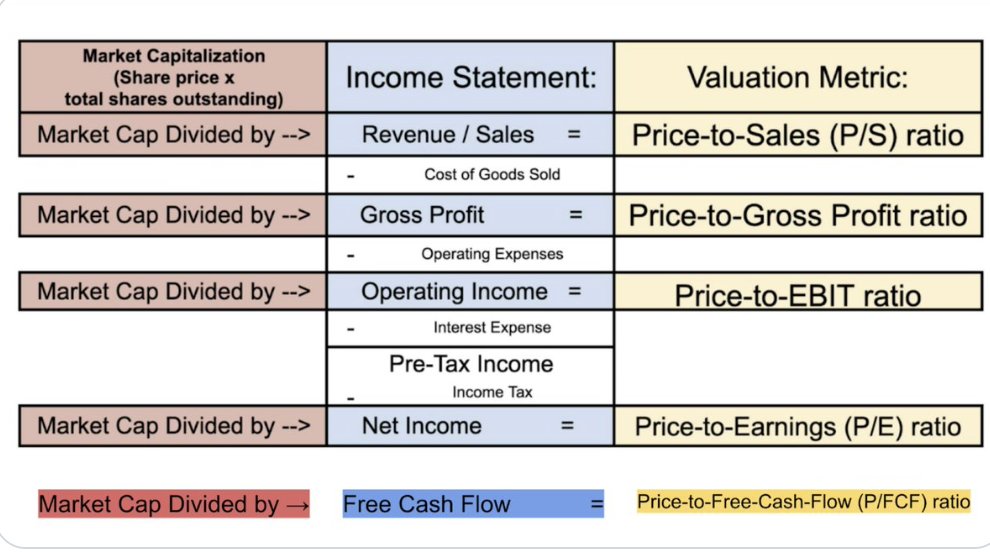

*Key Question*

What part of the income statement is the company currently optimized for?

Sales ➡️ P/S ratio

Gross Profit ➡️ P/Gross Profit ratio

Operating Income➡️ P/EBIT ratio

Earnings➡️ P/E Ratio

Free Cash Flow➡️P/FCF Ratio

What part of the income statement is the company currently optimized for?

Sales ➡️ P/S ratio

Gross Profit ➡️ P/Gross Profit ratio

Operating Income➡️ P/EBIT ratio

Earnings➡️ P/E Ratio

Free Cash Flow➡️P/FCF Ratio

Use this picture as a general guide

(and understand that it has flaws and is FAR from perfect)

(and understand that it has flaws and is FAR from perfect)

Find this helpful? You'll LOVE the course @BrianFeroldi and I teach:

*Financial Statements Explained Simply*

Our third cohort starts January 10th. DM me and I'll give you a code for HUNDREDS off the list price.

But hurry, enrollment closes January 9th

maven.com

*Financial Statements Explained Simply*

Our third cohort starts January 10th. DM me and I'll give you a code for HUNDREDS off the list price.

But hurry, enrollment closes January 9th

maven.com

@BrianFeroldi That's a wrap!

If you enjoyed this thread:

1. Follow me @Brian_Stoffel_ for more of these

2. RT the tweet below to share this thread with your audience

If you enjoyed this thread:

1. Follow me @Brian_Stoffel_ for more of these

2. RT the tweet below to share this thread with your audience

Loading suggestions...