Many employers that offer a 401(k) actually have two types of plans.

- A traditional 401(k)

- A Roth 401(k)

Let’s discuss each and which is the best option for you:

- A traditional 401(k)

- A Roth 401(k)

Let’s discuss each and which is the best option for you:

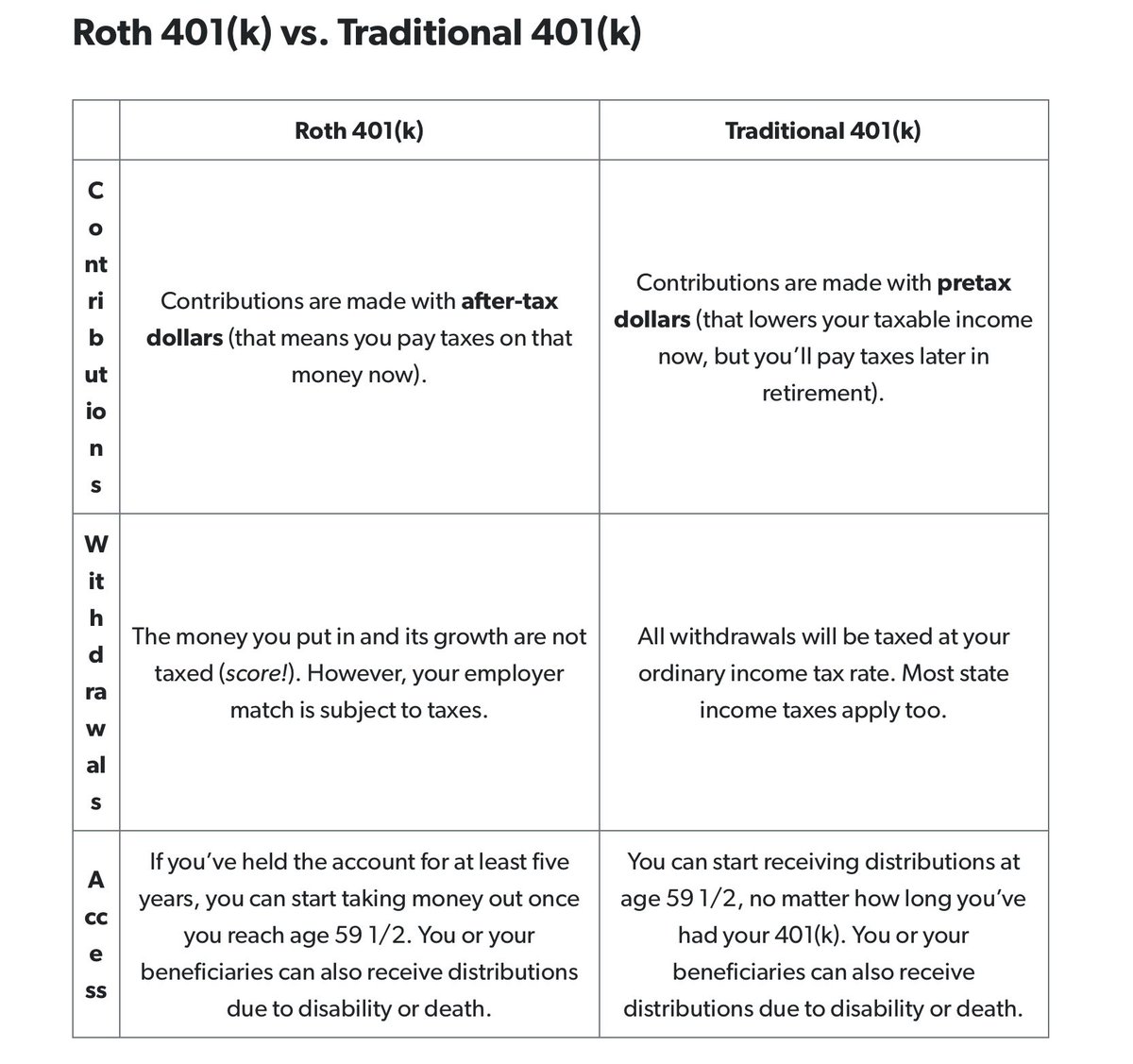

With a traditional 401(k) your contributions are deducted up front from your taxable income.

But then all future withdrawals are taxed at your ordinary income tax rate.

So you’ll pay taxes on the money invested plus any gains from appreciation or dividends.

But then all future withdrawals are taxed at your ordinary income tax rate.

So you’ll pay taxes on the money invested plus any gains from appreciation or dividends.

With a Roth 401(k) your contributions are taxed today with the rest of your income.

But then any money gained through investment appreciation or dividends isn’t taxed upon withdrawal.

However, if your employer was matching contributions those matches are subject to tax.

But then any money gained through investment appreciation or dividends isn’t taxed upon withdrawal.

However, if your employer was matching contributions those matches are subject to tax.

Check out this helpful graph for reference:

So which option is right for you?

I personally choose to utilize the Roth 401(k) option myself.

I like the idea of paying taxes on only my invested income now vs paying much more in taxes on these contributions AND capital gains later.

I personally choose to utilize the Roth 401(k) option myself.

I like the idea of paying taxes on only my invested income now vs paying much more in taxes on these contributions AND capital gains later.

I also love my Roth 401(k) because it’s the only way to invest more money with great Roth tax incentives.

The contribution limit for a Roth IRA is only $6500 a year, but utilizing a Roth 401(k) gives you an additional $22.5k to invest per year with the same beneficial tax laws.

The contribution limit for a Roth IRA is only $6500 a year, but utilizing a Roth 401(k) gives you an additional $22.5k to invest per year with the same beneficial tax laws.

Both 401(k) plans are decent options for the average person.

They both offer the ability to passively invest for your future without needing to do much with your portfolio.

But in my opinion the Roth option is far superior and can save you a lot of money in taxes over time.

They both offer the ability to passively invest for your future without needing to do much with your portfolio.

But in my opinion the Roth option is far superior and can save you a lot of money in taxes over time.

That being said, I still recommend maxing out a Roth IRA as well as utilizing a Roth 401(k).

In Roth IRAs, you have more control over your portfolio and often times less fees are involved.

I personally prioritize my Roth IRA and only invest up to the match in my Roth 401(k).

In Roth IRAs, you have more control over your portfolio and often times less fees are involved.

I personally prioritize my Roth IRA and only invest up to the match in my Roth 401(k).

I’m passionate about spreading financial knowledge to as many as possible.

School didn’t teach you this stuff, but I will! If you found this thread helpful then:

- Follow me @LTI_finance

- Retweet to share with others

- Subscribe to my FREE newsletter

markwlosinski.substack.com

School didn’t teach you this stuff, but I will! If you found this thread helpful then:

- Follow me @LTI_finance

- Retweet to share with others

- Subscribe to my FREE newsletter

markwlosinski.substack.com

Loading suggestions...