1/5

🧵on changes in thinking in just 2 weeks

Today's forward curve (cyan) is now equal to the year-end Fed's (blue), This is a HUGE move from Feb 2 (green).

A pivot is no longer priced in.

Also, for the first time this cycle, the market is pricing MORE hikes than the Fed.

🧵on changes in thinking in just 2 weeks

Today's forward curve (cyan) is now equal to the year-end Fed's (blue), This is a HUGE move from Feb 2 (green).

A pivot is no longer priced in.

Also, for the first time this cycle, the market is pricing MORE hikes than the Fed.

2/5

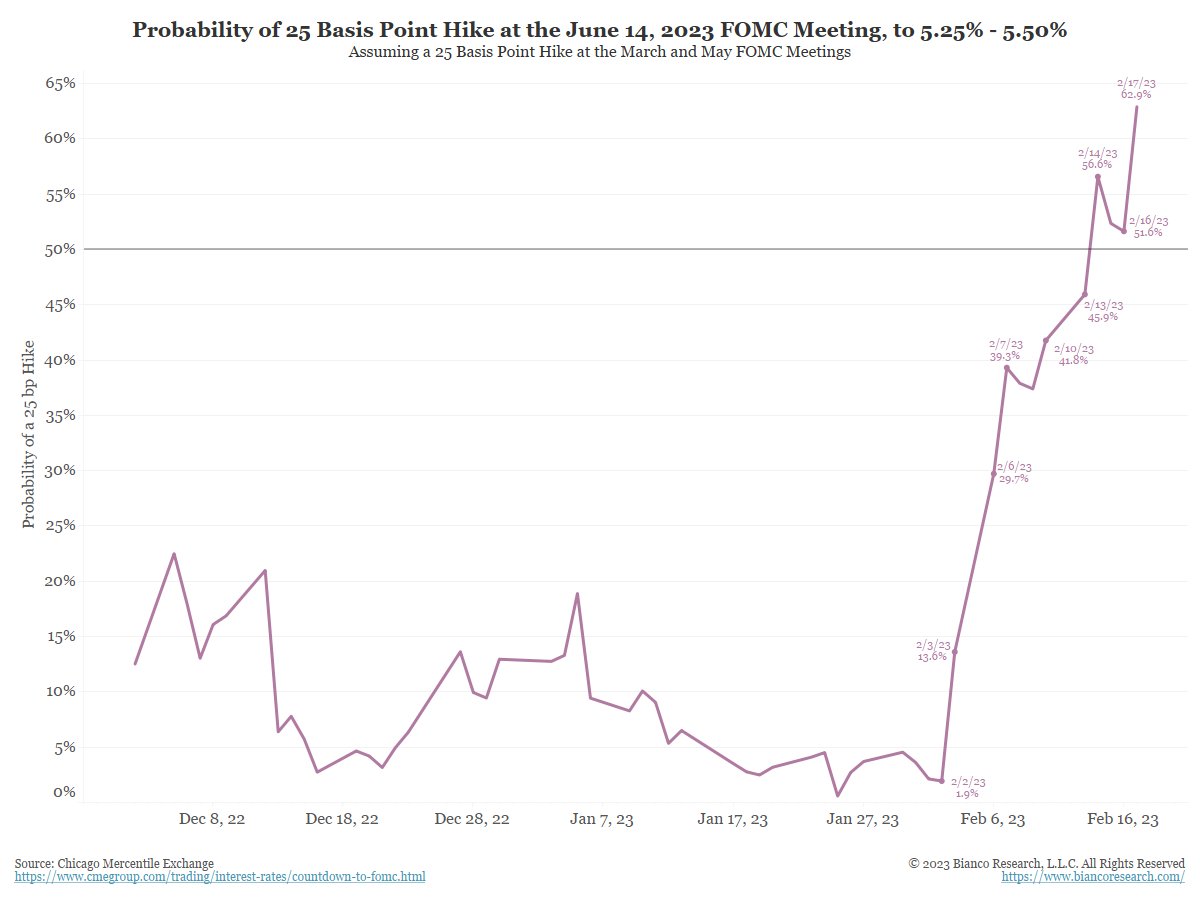

The focal point is the June 14 FOMC mtg. Will the Fed hike to 5.50%, above the Fed's 5.25% terminal target?

Feb 2, the day before the 517k payroll report, a June 5.50% funds rate was just a 2% probability. Yesterday it surged again to 63%.

A big change in thinking!

The focal point is the June 14 FOMC mtg. Will the Fed hike to 5.50%, above the Fed's 5.25% terminal target?

Feb 2, the day before the 517k payroll report, a June 5.50% funds rate was just a 2% probability. Yesterday it surged again to 63%.

A big change in thinking!

3/5

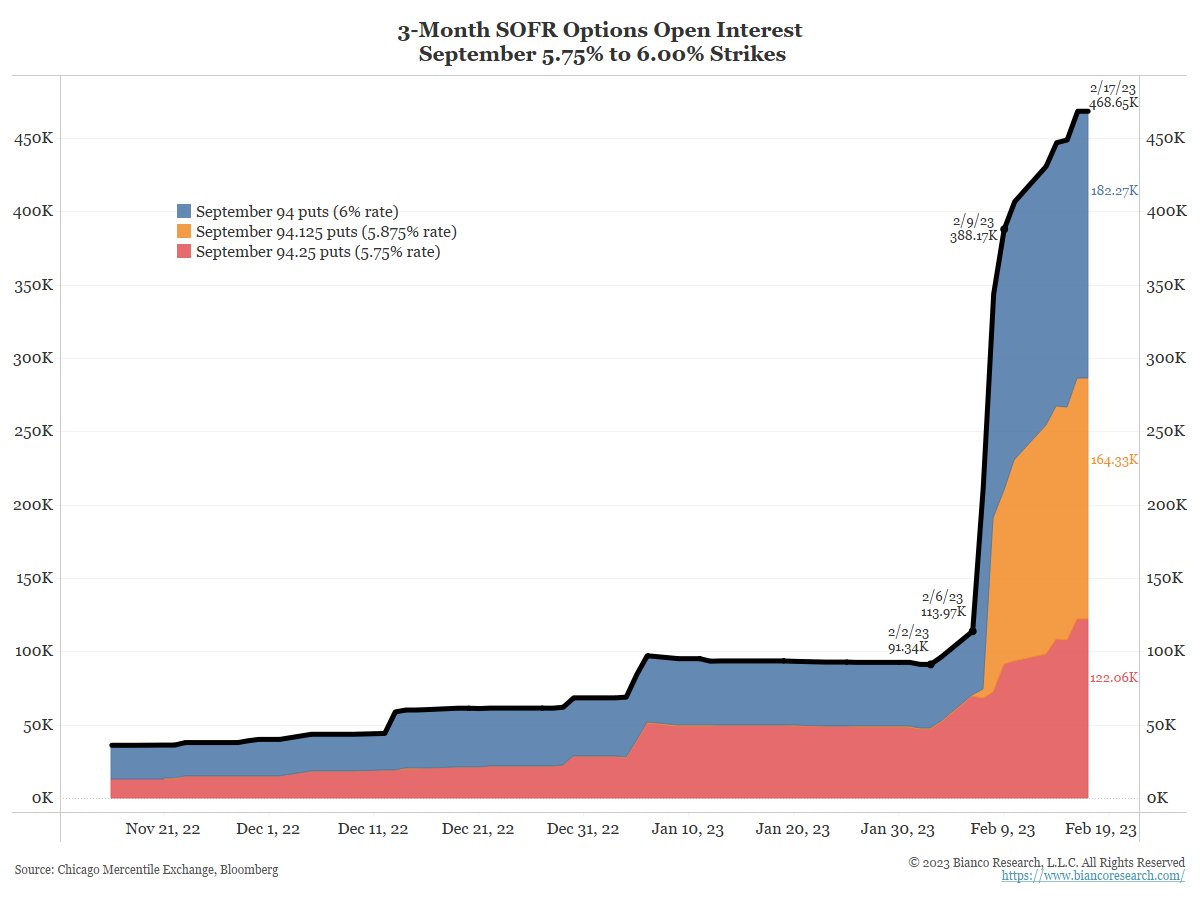

Where does the Fed go if the 5.25% "ceiling" is broken?

Since Feb 2, options betting that the Fed goes to a target of 5.75% - 6.00% by SEPTEMBER is exploding higher.

Again, all of this has been new in the last two weeks.

Where does the Fed go if the 5.25% "ceiling" is broken?

Since Feb 2, options betting that the Fed goes to a target of 5.75% - 6.00% by SEPTEMBER is exploding higher.

Again, all of this has been new in the last two weeks.

4/5

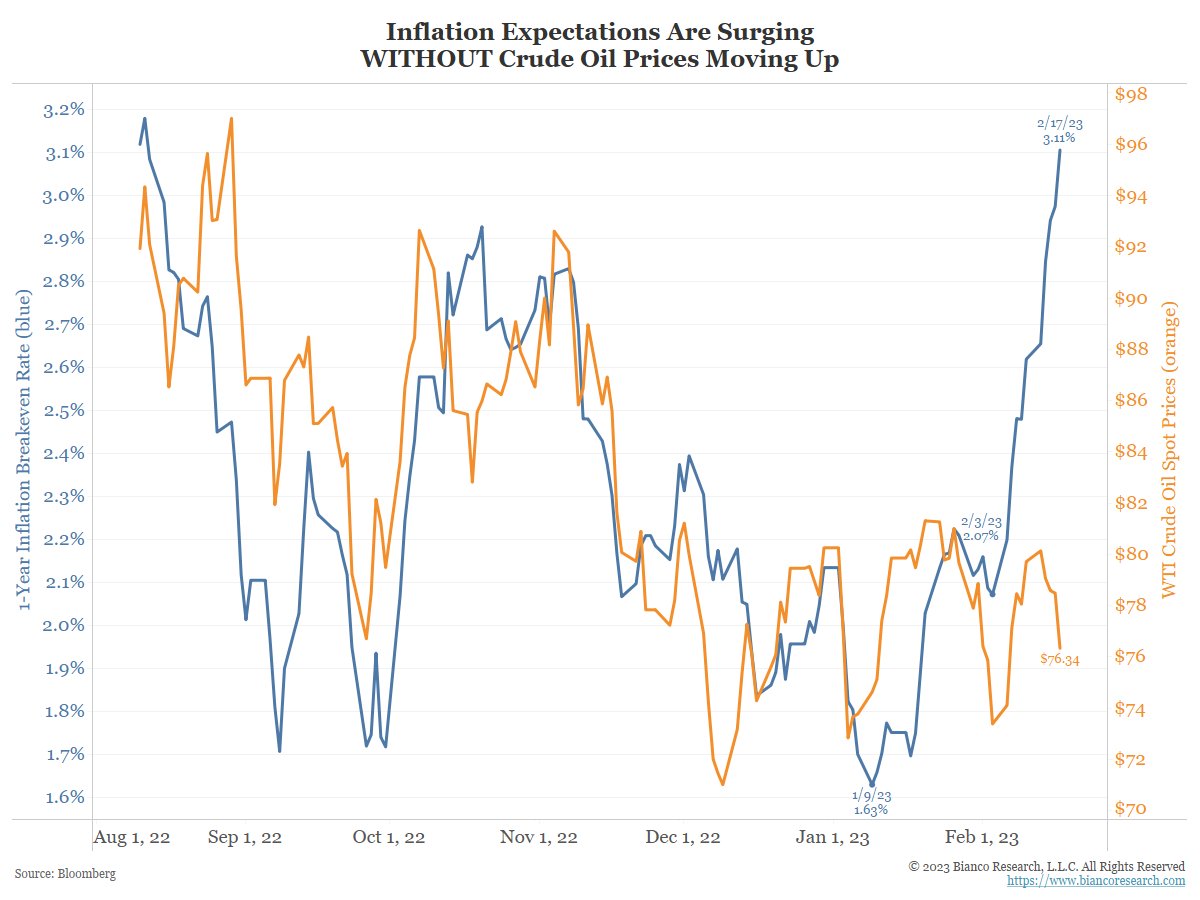

And why does the market think the Fed can hike well above 5.25%?

Since Feb 2, 1-year Inflation breakevens (blue) are surging, diverging with crude, so it is more than just higher gas prices.

"Persistent" inflation means the Fed is not "sufficiently restrictive" at 5.25%.

And why does the market think the Fed can hike well above 5.25%?

Since Feb 2, 1-year Inflation breakevens (blue) are surging, diverging with crude, so it is more than just higher gas prices.

"Persistent" inflation means the Fed is not "sufficiently restrictive" at 5.25%.

5/5

Will the stock market notice?

BofA's Michael Hartnett is trying to tell it. Will it listen?

Or are we too busy with 0DTE options and $BTC/ $TSLA big YTD gains to look more than a week into the future?

zerohedge.com

Will the stock market notice?

BofA's Michael Hartnett is trying to tell it. Will it listen?

Or are we too busy with 0DTE options and $BTC/ $TSLA big YTD gains to look more than a week into the future?

zerohedge.com

Recap

Since Feb 2, the day b4 payrolls:

Forward curves, massively changed

June probability of 5.50%, 2% to 63%

Options betting 6% by fall, exploded

1-year inflation breakevens, surged.

Not everyone has caught up.

I detailed this in my last podcast.

youtube.com

Since Feb 2, the day b4 payrolls:

Forward curves, massively changed

June probability of 5.50%, 2% to 63%

Options betting 6% by fall, exploded

1-year inflation breakevens, surged.

Not everyone has caught up.

I detailed this in my last podcast.

youtube.com

Loading suggestions...