Banks have been beaten down over the last 3 years

The valuation of many Banks now trades at a multi-year low

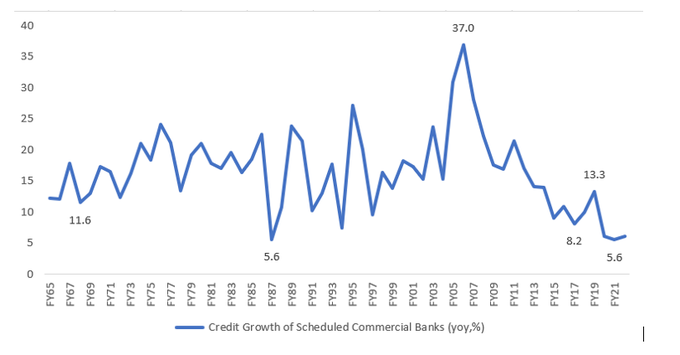

Credit growth has now picked up to 20%.

Banks are the place to be now

We have a banking & financial services small case

A thread on the rationale-

Source-ICICI Direct

The valuation of many Banks now trades at a multi-year low

Credit growth has now picked up to 20%.

Banks are the place to be now

We have a banking & financial services small case

A thread on the rationale-

Source-ICICI Direct

Credit growth at a Multi-year low has now picked up:-

Credit growth was at a 50-year low!

Several shocks like:-

1. IL&FS

2. DHFL+Yes Bank

3. COVID-19 crisis

Banks flush with capital are pushing credit back into the system

Credit growth was at a 50-year low!

Several shocks like:-

1. IL&FS

2. DHFL+Yes Bank

3. COVID-19 crisis

Banks flush with capital are pushing credit back into the system

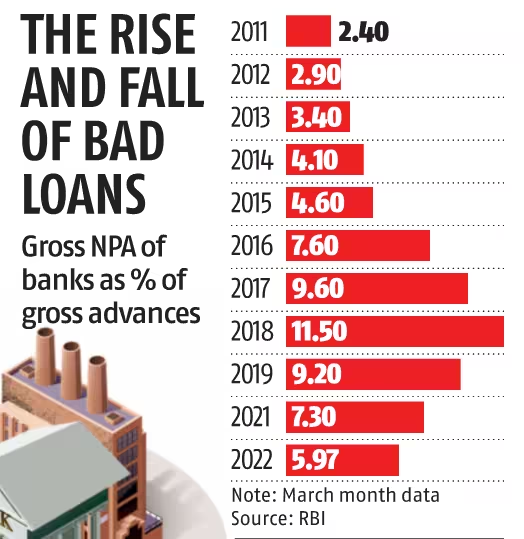

Improvement in Asset quality:-

Systemic NPAs at 10-year low:-

Rbi forced all banks to undergo an asset quality cleanup with Covid.

🏦The systemic NPAs are now at a 10-year low.

🏦Low NPAs=Low Provisions=Less drag on Bank Capital.

Systemic NPAs at 10-year low:-

Rbi forced all banks to undergo an asset quality cleanup with Covid.

🏦The systemic NPAs are now at a 10-year low.

🏦Low NPAs=Low Provisions=Less drag on Bank Capital.

COVID-19 made sure all Banks:-

Big or small

PSU or private

Had to clean up their books!

A lot of poison(NPAs) in the system was cleaned out

Big or small

PSU or private

Had to clean up their books!

A lot of poison(NPAs) in the system was cleaned out

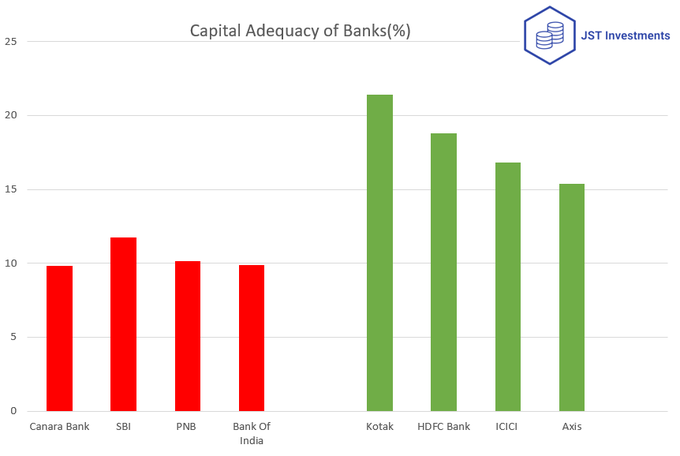

Banks are flushed with capital

While PSU banks are struggling for capital

All private sector banks are raring to go with a huge amount of capital waiting to be deployed

While PSU banks are struggling for capital

All private sector banks are raring to go with a huge amount of capital waiting to be deployed

Recovery in the economy and start of the CAPEX cycle:-

Ever since 2018,a fall in credit meant that economic growth took a hit.

COVID-19 lockdowns further accentuated the fall in economic growth.

Vaccination has resulted in large-scale opening up of the economy

Ever since 2018,a fall in credit meant that economic growth took a hit.

COVID-19 lockdowns further accentuated the fall in economic growth.

Vaccination has resulted in large-scale opening up of the economy

As the economy continues to open up....we have seen a huge consumption spree.

Hotels and vacation spots have a long waiting period.

The backbone of any economic growth is credit!

Slowly and steadily as the economy opens up economic growth will b

Hotels and vacation spots have a long waiting period.

The backbone of any economic growth is credit!

Slowly and steadily as the economy opens up economic growth will b

Start of the capex cycle:-

The government expects the Capex cycle to revive in the second half of 2022.

Many corporates are already talking about capacity expansion.

All of this expansion will be undertaken by the flow of credit.

The government expects the Capex cycle to revive in the second half of 2022.

Many corporates are already talking about capacity expansion.

All of this expansion will be undertaken by the flow of credit.

Downside risks:-

1. The global banking stress could lead to a correction

2. If the economy takes longer to recover there will be problems

3. Corporate deleveraging-However this should reverse as we embark on a capex cycle

1. The global banking stress could lead to a correction

2. If the economy takes longer to recover there will be problems

3. Corporate deleveraging-However this should reverse as we embark on a capex cycle

So what do we offer in this portfolio?

In the portfolio we have:-

1. Large Private sector Banks

2. Small Private sector Banks

3. PSU Banks

4. NBFCs

5. AMCs

6. Insurance companies

In the portfolio we have:-

1. Large Private sector Banks

2. Small Private sector Banks

3. PSU Banks

4. NBFCs

5. AMCs

6. Insurance companies

For whom is this portfolio useful?

JST Banking and Financial Services portfolio is a HIGHLY RISKY sectoral portfolio.

Sectoral funds carry a high sector risk and only those who have a high risk tolerance should invest in this fund.

JST Banking and Financial Services portfolio is a HIGHLY RISKY sectoral portfolio.

Sectoral funds carry a high sector risk and only those who have a high risk tolerance should invest in this fund.

Entry and exit from a sectoral fund must always be times.

We believe the time is right to enter the financial services space.

We believe the time is right to enter the financial services space.

How to subscribe to the portfolio?

Subscribe here:-

jstinvestments.smallcase.com

If u have any questions,email us at adityashah291@gmail.com

Subscribe here:-

jstinvestments.smallcase.com

If u have any questions,email us at adityashah291@gmail.com

Loading suggestions...