I am somewhat more pessimistic about the near-term than Dr. Rodrik --

I certainly hope that inflows do materialize quickly, but I fear that it will take time ... and Erdogan has levered the CBRT to the hilt to try to make it to the election.

Thread

1/

I certainly hope that inflows do materialize quickly, but I fear that it will take time ... and Erdogan has levered the CBRT to the hilt to try to make it to the election.

Thread

1/

Turkey's fx debt isn't primarily through the government --

It is not mostly on the central bank's balance sheet.

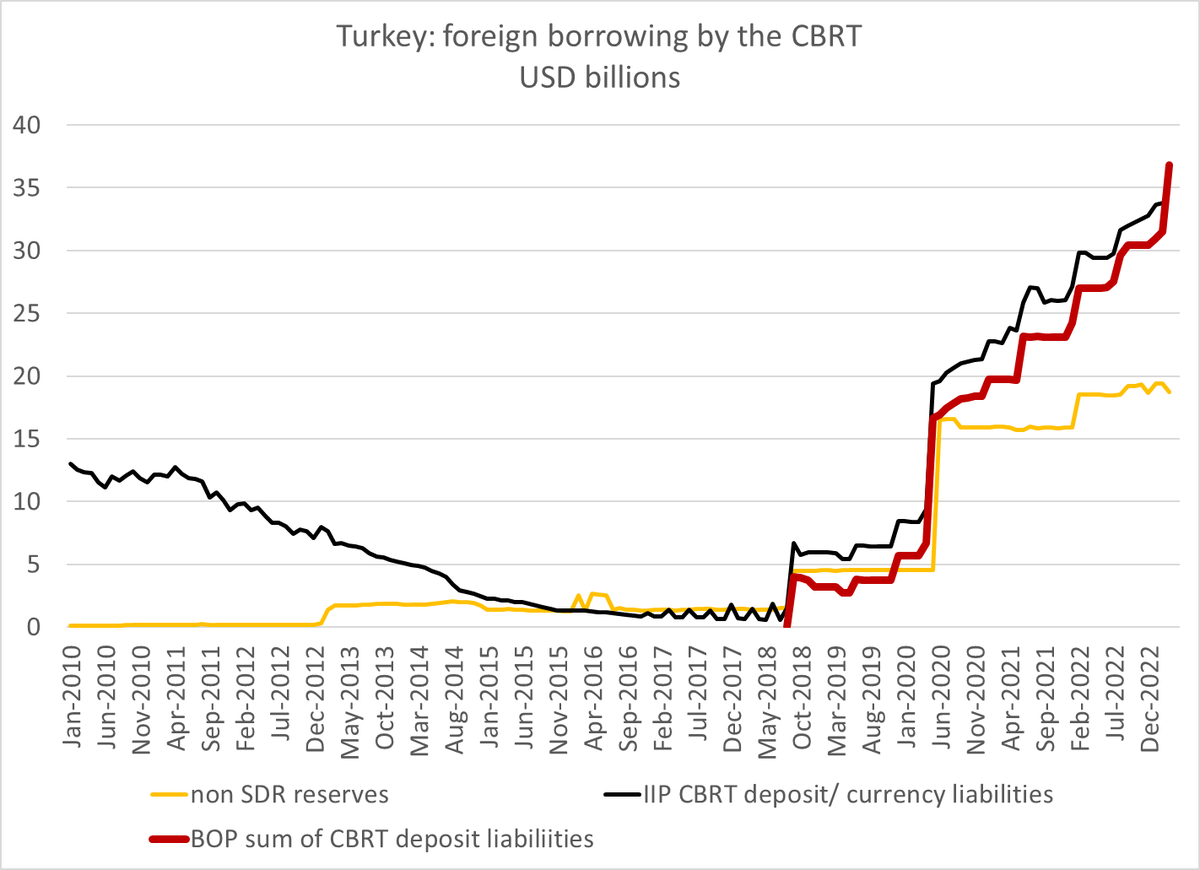

The CBRT has borrowed -- initially through swaps, now through deposits that provide it with usable dollars -- close to $40b externally.

2/

It is not mostly on the central bank's balance sheet.

The CBRT has borrowed -- initially through swaps, now through deposits that provide it with usable dollars -- close to $40b externally.

2/

So a substantial share of the CBRT's non gold reserves and borrowed from the rest of the world (and $20b are in illiquid GCC currencies). The FX liquidity situation the new government will face is dire.

3/

3/

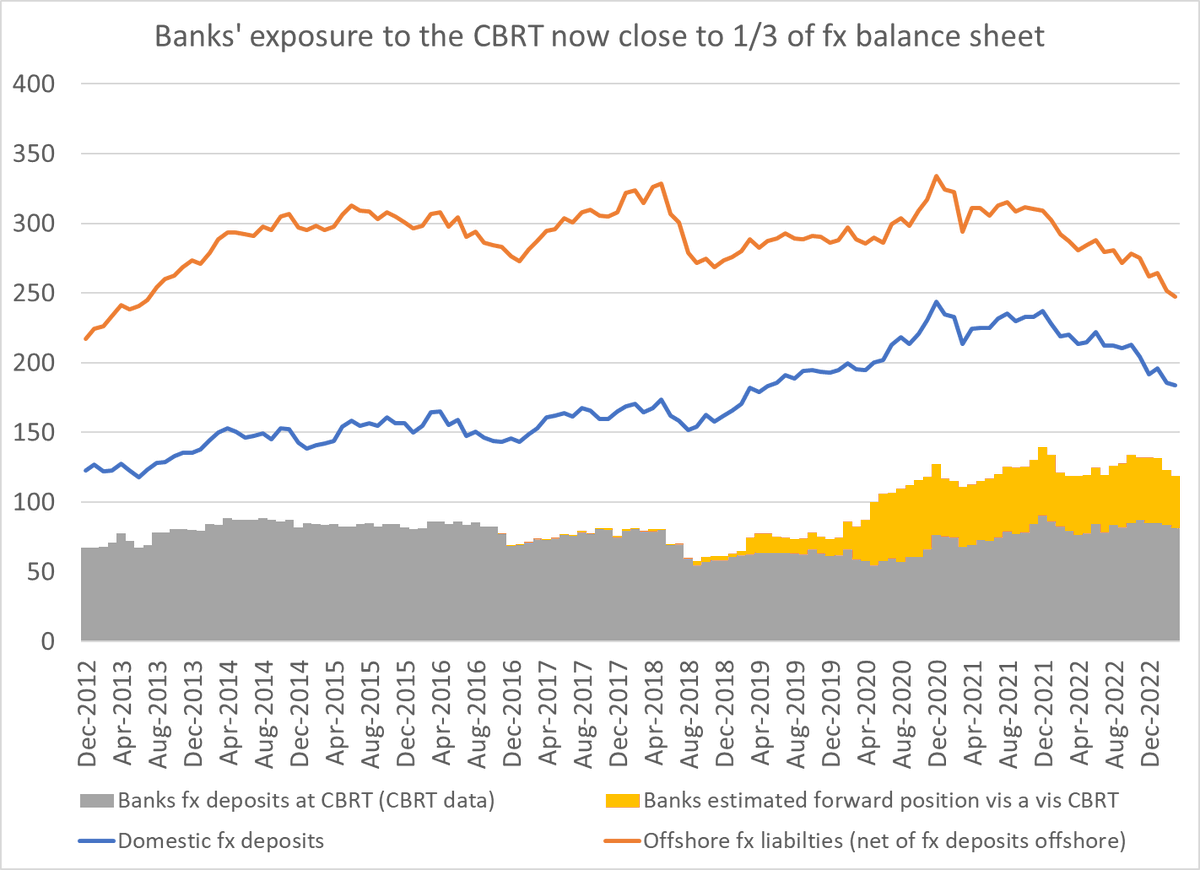

The domestic banks have also lent the CBRT about $120b -- $40b through swaps (Banks send fx to the CBRT for TL), and $80b plus in deposits (including required reserves).

That is about 2/3rds of domestic fx deposits and 1/2 their fx balance sheet ...

4/

That is about 2/3rds of domestic fx deposits and 1/2 their fx balance sheet ...

4/

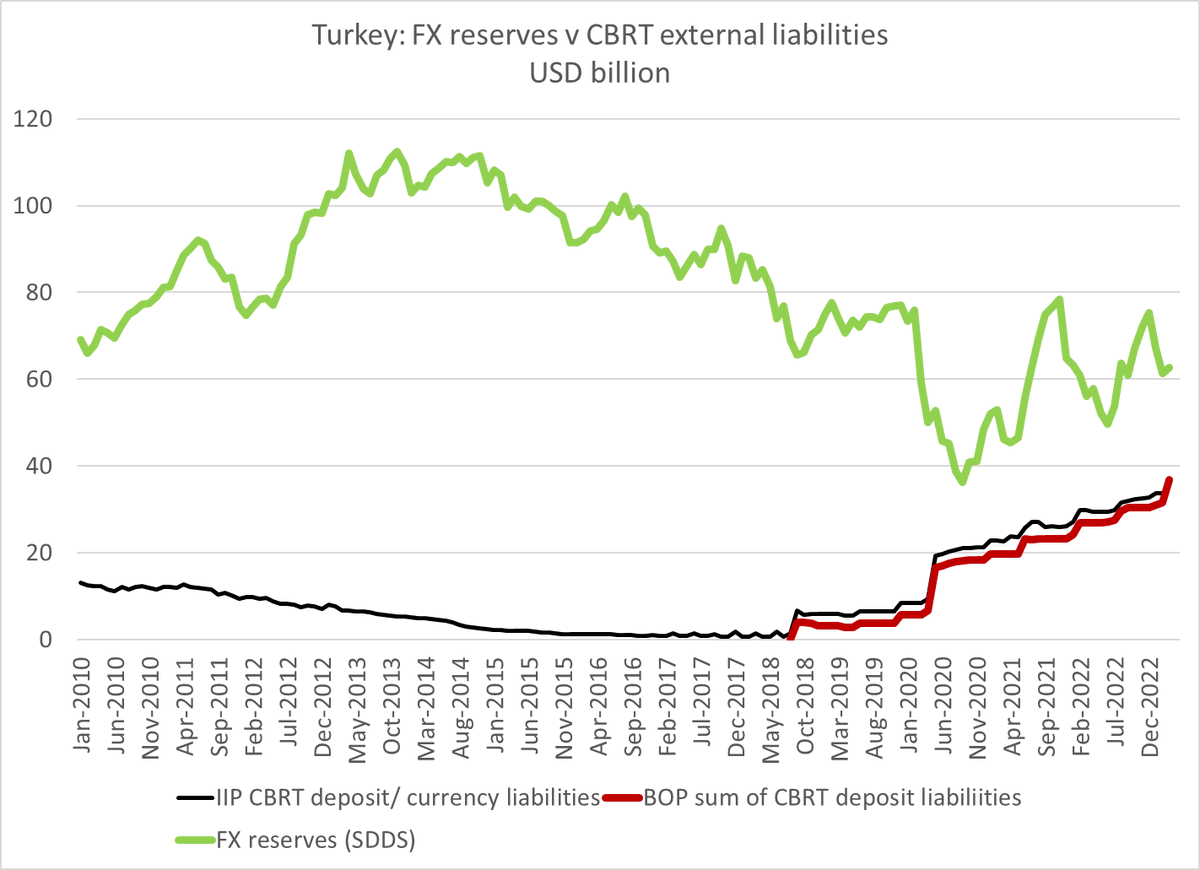

So the FX liquidity picture is dire

-- the CBRT has $50b in real fx reserves (probably a bit less now), and $20b in GCC currencies.

-- v $35-40b in external fx liabilities, $40b in domestic swap liabilities and $80b plus in other domestic dx liabilities ...

-- the CBRT has $50b in real fx reserves (probably a bit less now), and $20b in GCC currencies.

-- v $35-40b in external fx liabilities, $40b in domestic swap liabilities and $80b plus in other domestic dx liabilities ...

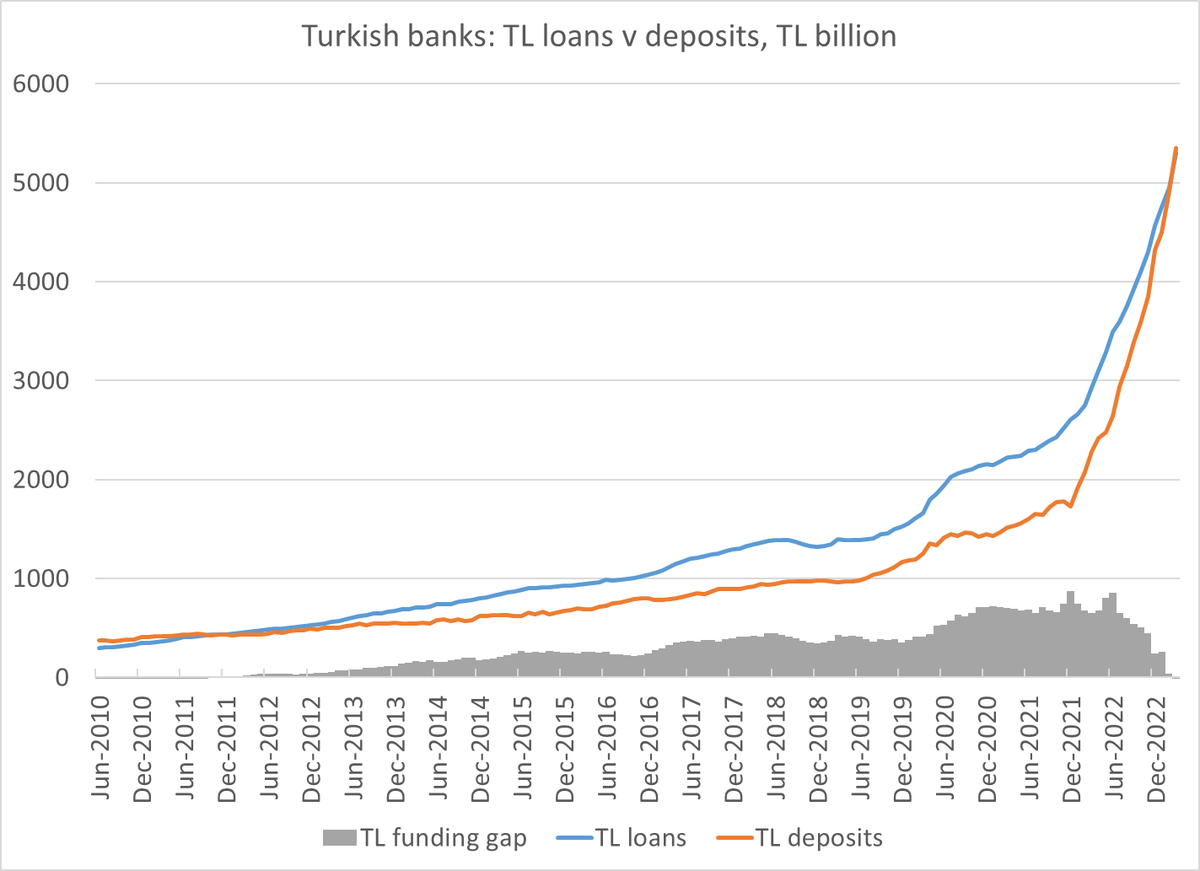

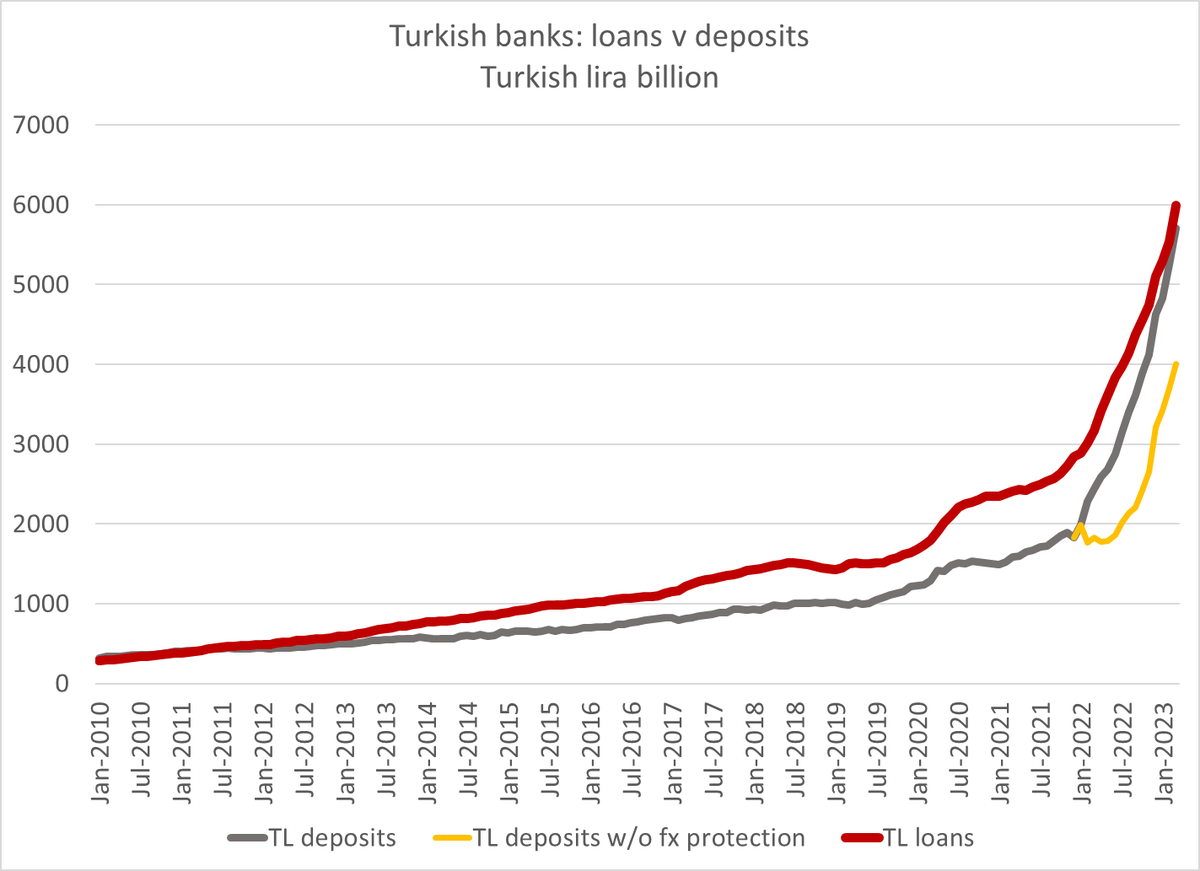

Domestic bank lending has gone crazy (no doubt to try to juice the economy ahead of an election ... )

Easy to see why there has been a bit of inflation

6/

Easy to see why there has been a bit of inflation

6/

A lot of that lira lending has been financed out of the fx protected deposits -- which are now such a bit part of the banks lira funding base that they will be hard to eliminate anytime soon (creating an additional set of problems)

7/

7/

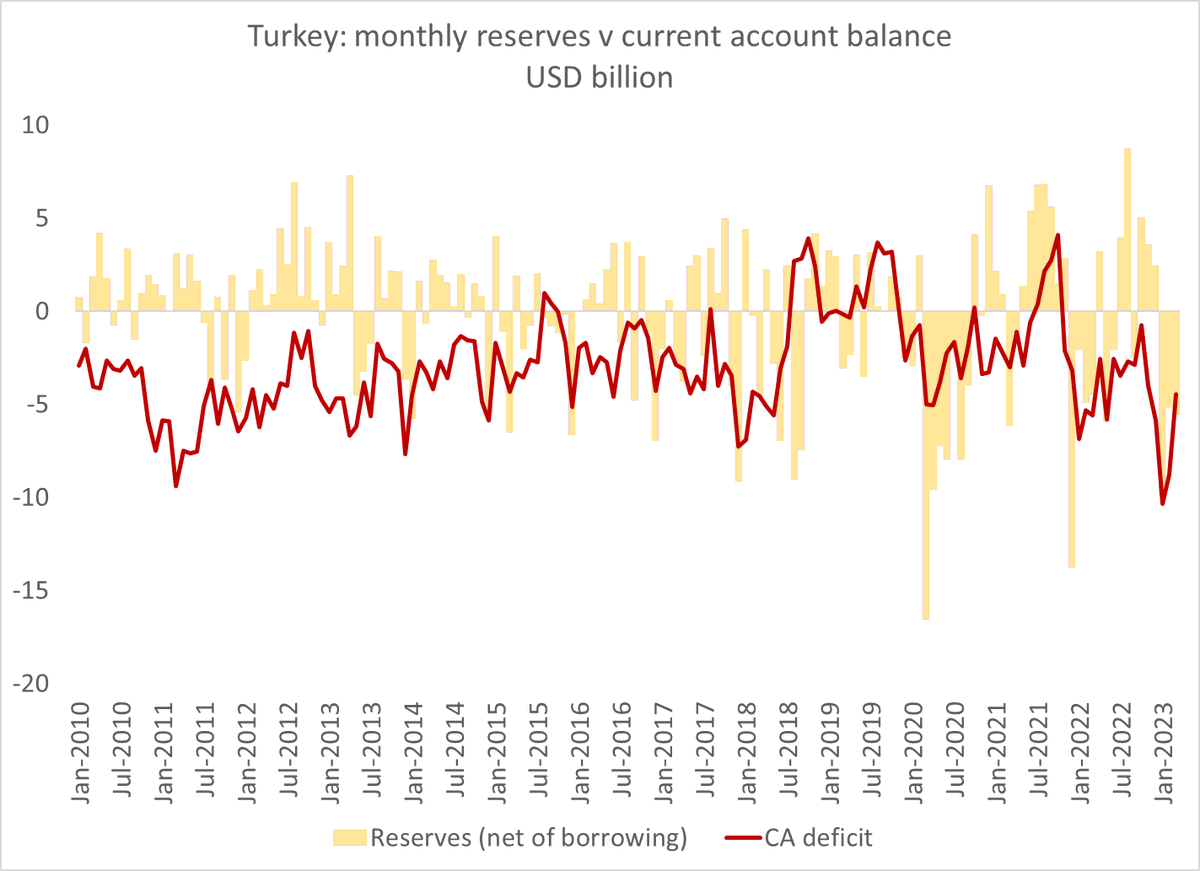

This year's current account deficit has effectively been financed by reserve sales -- but for the new Saudi deposit at the CBRT, reported reserves would be even lower.

8/

8/

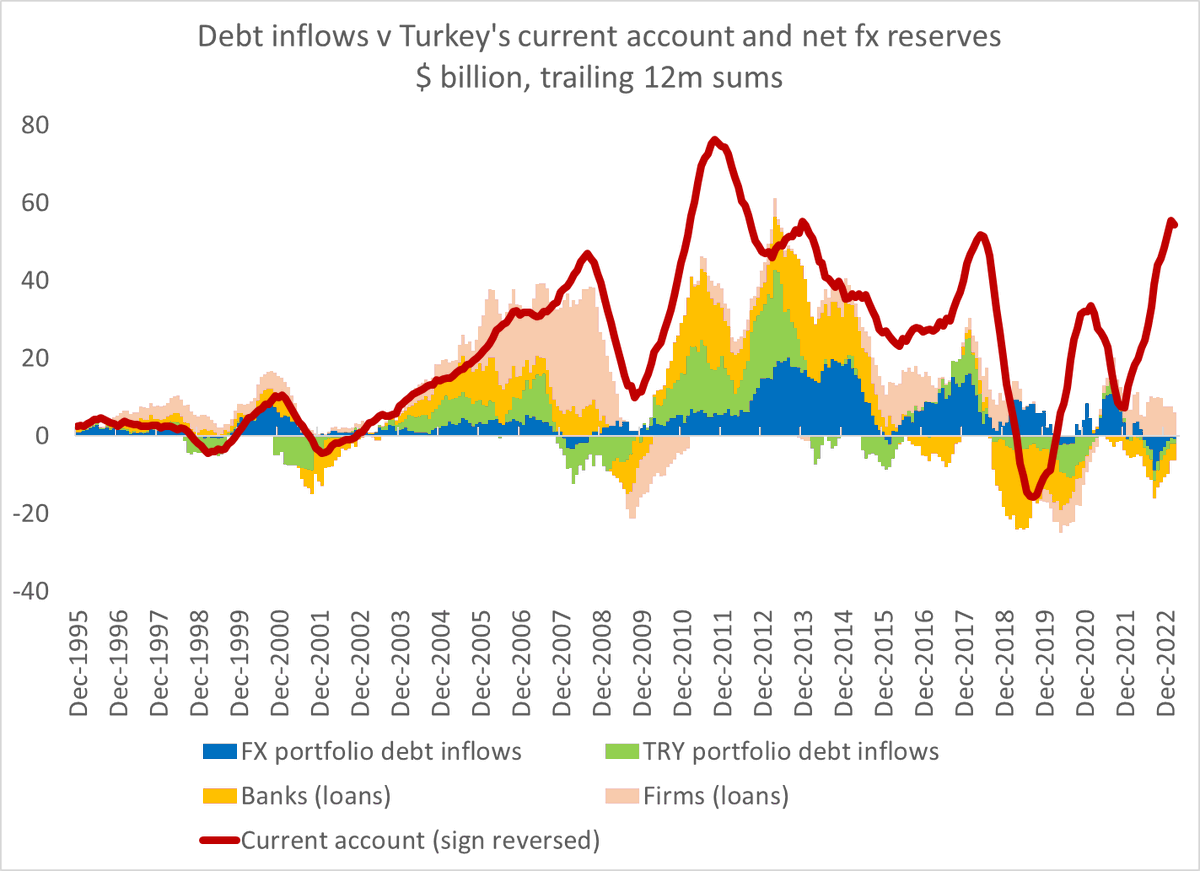

Erdogan's policies -- holding the TL pretty stable, low TL rates, a big increase in bank lending, no doubt some fiscal spending too -- have pushed up the current account deficit when the funding for it simply hasn't been there.

9/

9/

The hope is that better policies -- allowing the inevitable adjustment in the lira, raising domestic interest rates -- will need to renewed foreign demand for lira assets.

10/

10/

But I fear that the needed shifts in the lira and domestic interest rates won't be easy -- and will be disruptive. I wonder how quickly rates will be allowed to increase (pushing rates up above inflation would be painful to the banks etc)

11/

11/

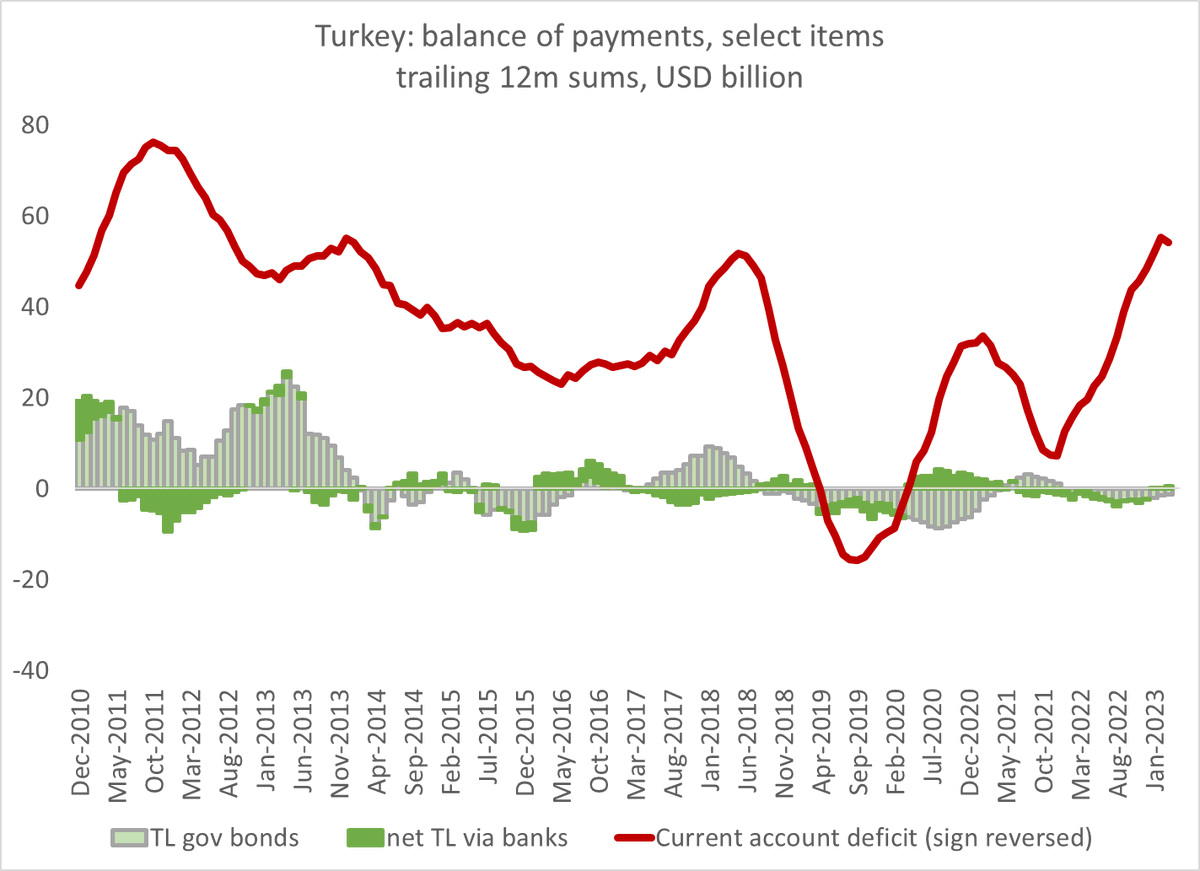

Foreign demand for TL bonds (or even deposits) may not materialize until after the adjustment is complete ...

and in the interim Turkey may need to draw on its fx reserves.

But, well, Erdogan has left the coffers pretty bare.

13/

and in the interim Turkey may need to draw on its fx reserves.

But, well, Erdogan has left the coffers pretty bare.

13/

Perhaps the GCC countries will come through with another slug of financing --

and no doubt the opposition hope Putin will continue to allow the purchase of gas on credit.

14/

and no doubt the opposition hope Putin will continue to allow the purchase of gas on credit.

14/

But it does seem at least to me like the US and the EU -- who have a lot at stake in Turkey -- should also be preparing some financial contingency plans.

Unwinding the policy mistakes of the last few years isn't going to be easy.

15/15

Unwinding the policy mistakes of the last few years isn't going to be easy.

15/15

Loading suggestions...