The two biggest source of broad money creation are 1) bank lending and 2) fiscal deficits.

In the 1970s inflation saga we had lending dominance, while in the 1910s, 1940s, and 2020s inflation sagas we had fiscal dominance

In the 1970s inflation saga we had lending dominance, while in the 1910s, 1940s, and 2020s inflation sagas we had fiscal dominance

This chart shows year-over-year loan creation and fiscal deficits for the 1960s/1970s in absolute dollar terms (billion USD) compared to the prior year. Loan creation was a bigger source of money creation than deficits, and drove inflation.

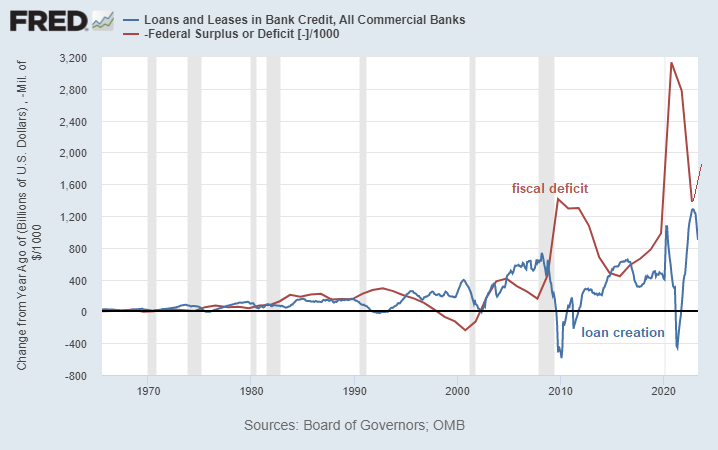

This chart shows year-over-year loan creation and fiscal deficits currently. Fiscal deficits are a bigger source of money creation than loans now.

The reason this matters is that interest rates as a policy tool are mainly useful for affecting lending growth, not fiscal deficits.

Higher rates have a reputation of slowing inflation because they can put downward pressure on lending. But, they make fiscal deficits worse.

Higher rates have a reputation of slowing inflation because they can put downward pressure on lending. But, they make fiscal deficits worse.

In the 1970s, since lending was a bigger source of money creation than fiscal deficits, higher rates were indeed a positive factor for suppressing inflation.

It worked in ways that many don't realize though, like suppressing oil demand from Latin America by causing a depression.

It worked in ways that many don't realize though, like suppressing oil demand from Latin America by causing a depression.

Right now, the bigger source of money creation is fiscal deficits. So, raising rates suppresses lending (which is disinflationary & recessionary) and increases deficits (which is inflationary & stimulative).

And deficits are bigger than loan creation now...

And deficits are bigger than loan creation now...

What this suggests is that 1) interest rates are less effective as an inflation-fighting tool in the 2020s than the 1970s and 2) beyond a certain point can actually become pro-inflationary.

Lending inflation wasn't the primary driver of inflation in this cycle, but that's the only driver that the Fed can directly target.

Suppressing lending can indirectly and cyclically reduce inflation, but doesn't target the actual core causes of inflation in this cycle.

Suppressing lending can indirectly and cyclically reduce inflation, but doesn't target the actual core causes of inflation in this cycle.

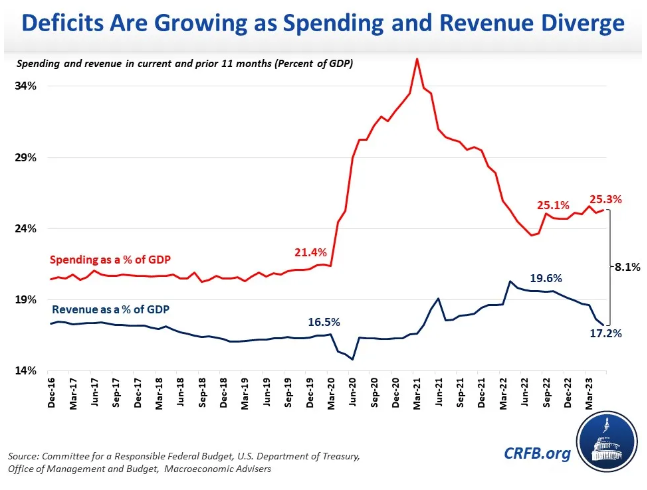

The core structural drivers of inflation currently are 1) fiscal deficits and 2) supply constraints.

Reducing the fiscal deficit, or increasing supply (i.e. energy abundance and AI/automation), are what directly tackle inflation.

Everything else just suppressed it for a time.

Reducing the fiscal deficit, or increasing supply (i.e. energy abundance and AI/automation), are what directly tackle inflation.

Everything else just suppressed it for a time.

Loading suggestions...