Everyone tells you to "Buy Cash Flowing Rental Properties" but no one shows you how...

Here is EXACTLY how to run the numbers on any rental property in LESS THAN 60 seconds:

Here is EXACTLY how to run the numbers on any rental property in LESS THAN 60 seconds:

Pro Tip:

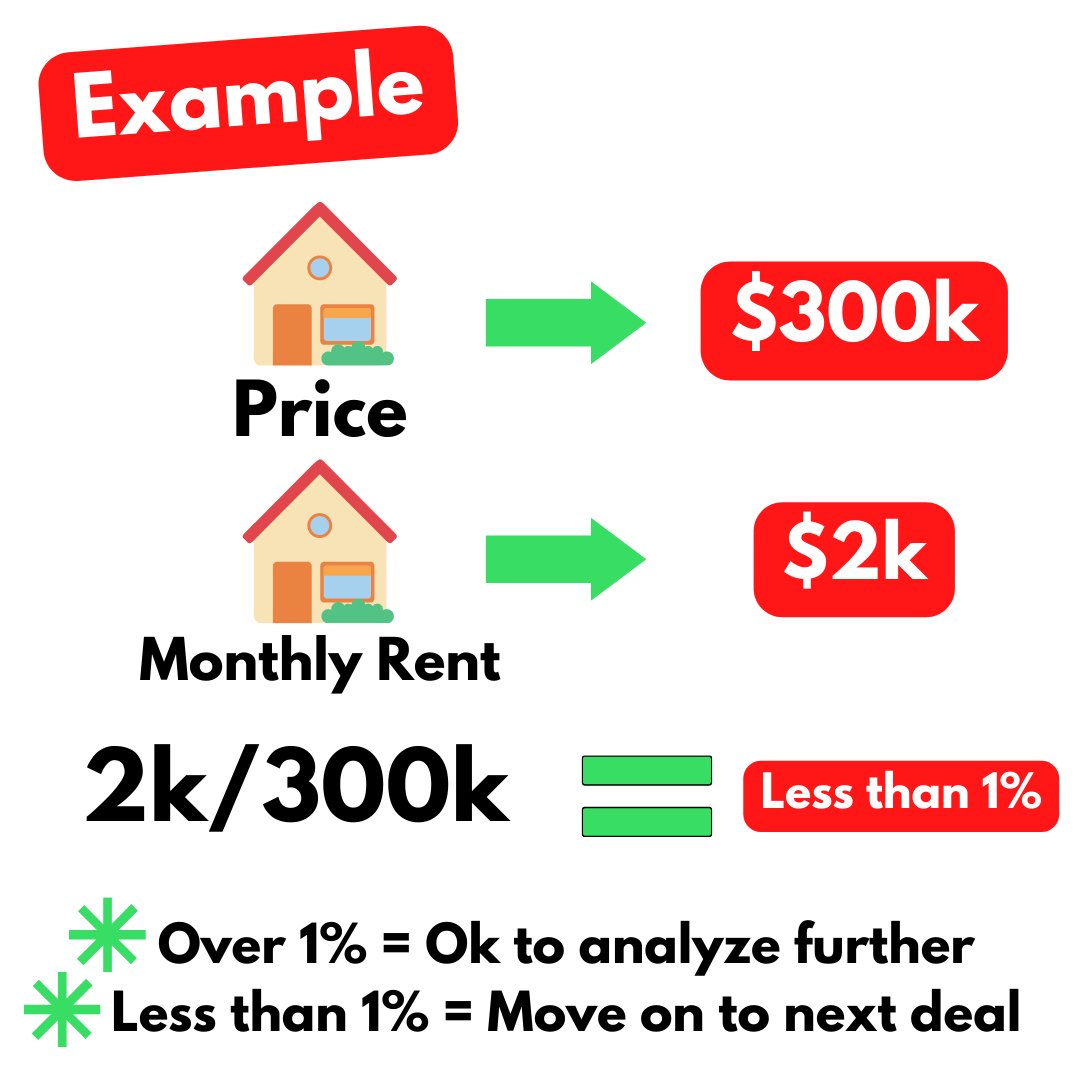

Before you start, use the 1% rule to quickly disqualify properties so you don't waste your time.

Rule: Monthly Rent must be > 1% of Purchase Price of Home

Ex: Price: $300,000

That means the rent MUST BE AT LEAST $3,000/month or we don't need to calculate the rest.

Before you start, use the 1% rule to quickly disqualify properties so you don't waste your time.

Rule: Monthly Rent must be > 1% of Purchase Price of Home

Ex: Price: $300,000

That means the rent MUST BE AT LEAST $3,000/month or we don't need to calculate the rest.

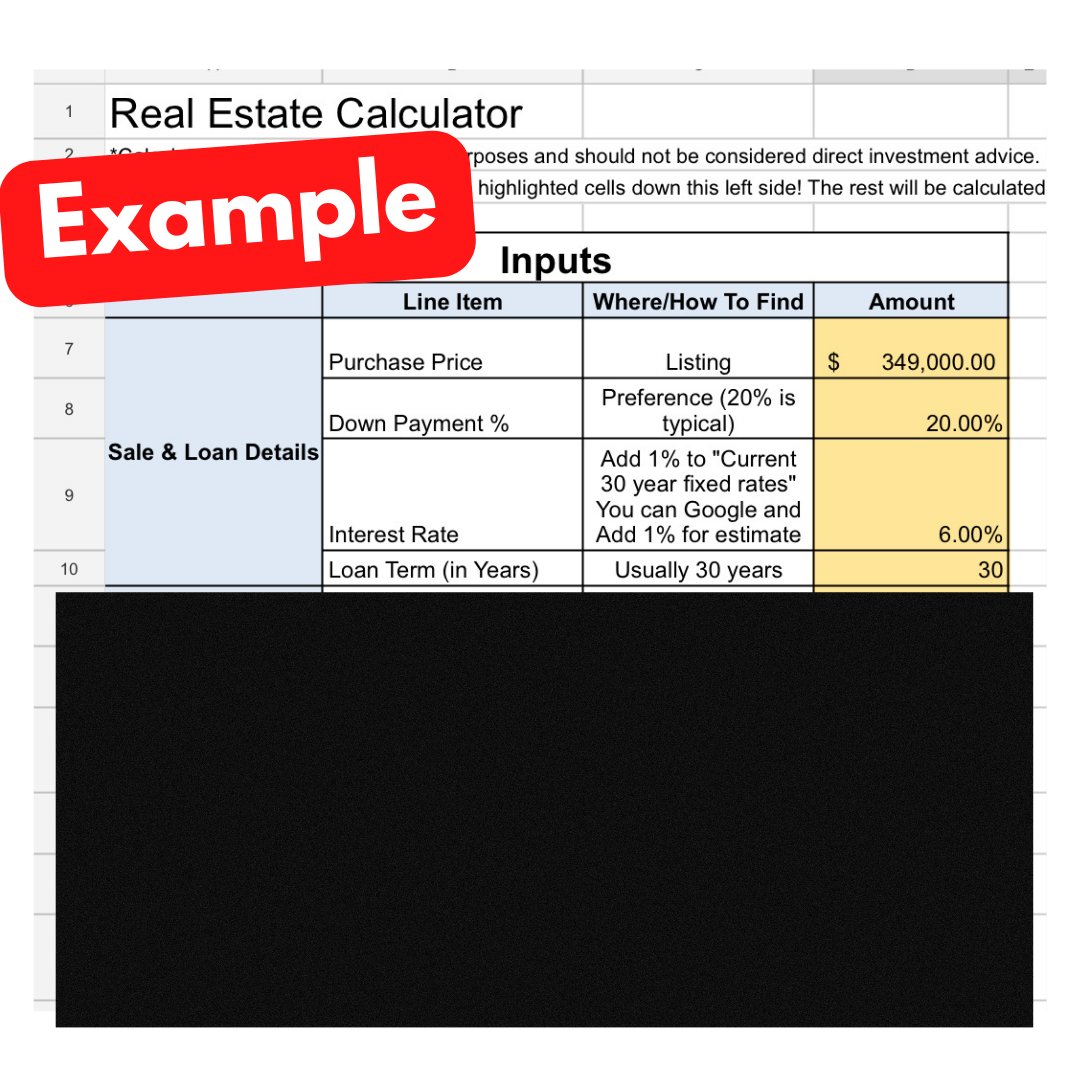

First, you will need the Sale and Loan Details and the Income.

1. Purchase Price: On the Listing

2. Interest Rate: Take the average mortgage rate on a primary home and add 50 to 75 basis points to it

- Ex: Average Rate: 7.5%

Estimated Rental Rate: 8.0-8.25% for Rental Property

1. Purchase Price: On the Listing

2. Interest Rate: Take the average mortgage rate on a primary home and add 50 to 75 basis points to it

- Ex: Average Rate: 7.5%

Estimated Rental Rate: 8.0-8.25% for Rental Property

3. Down Payment:

- Typically 20% for a property you are not living in but there can be exceptions

- House Hack: 3-5%

- Vacation Loan- 10%

- Seller Financing- Whatever you can work out with the seller

4. Loan Term: Typically 30 years

- Typically 20% for a property you are not living in but there can be exceptions

- House Hack: 3-5%

- Vacation Loan- 10%

- Seller Financing- Whatever you can work out with the seller

4. Loan Term: Typically 30 years

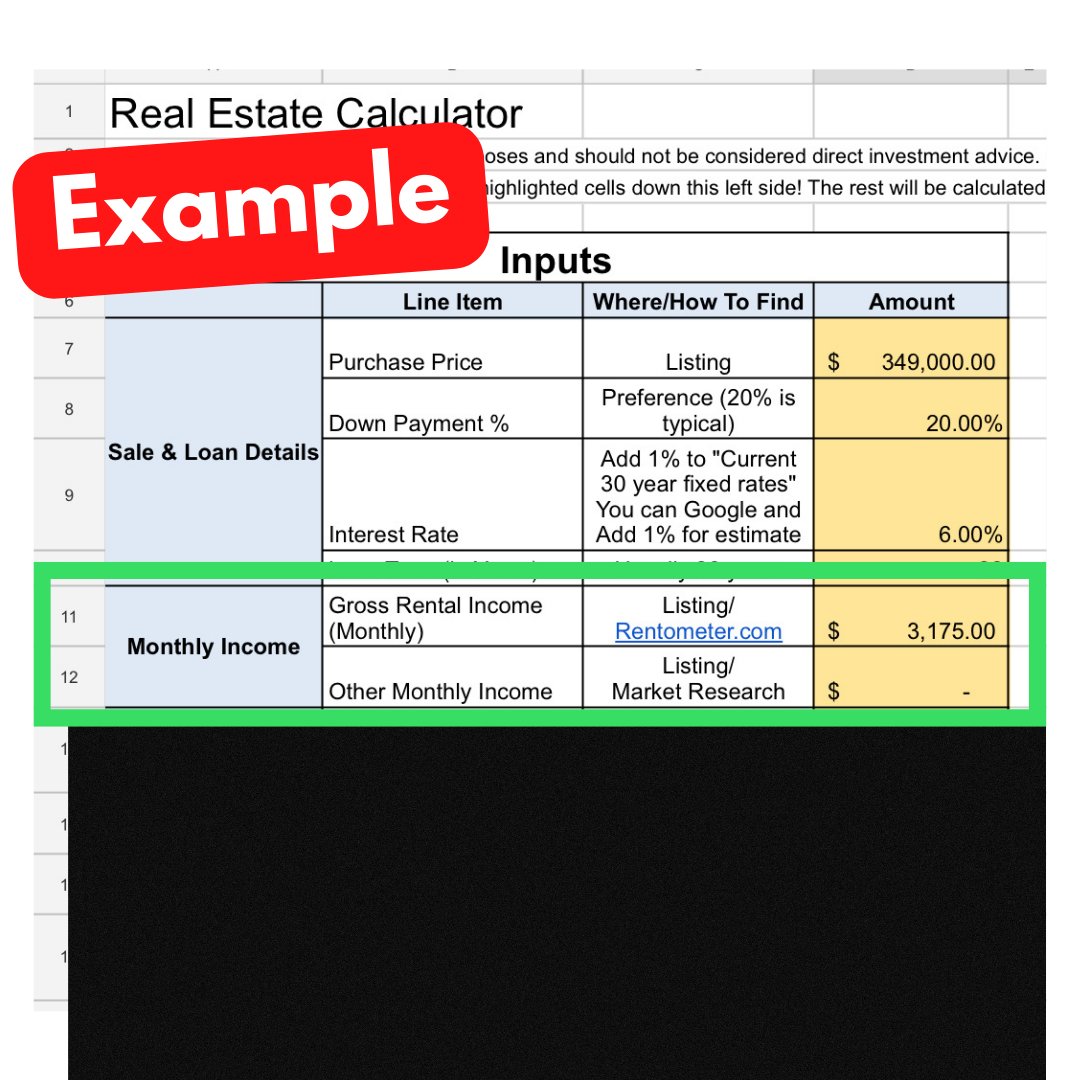

Income:

1. Rental Income: This should be on the listing but you can also use Rentometer.com to check what similar properties are renting for

2. Other Income: Washers/Dryers/Parking/Storage etc. You can find this info on the listing.

1. Rental Income: This should be on the listing but you can also use Rentometer.com to check what similar properties are renting for

2. Other Income: Washers/Dryers/Parking/Storage etc. You can find this info on the listing.

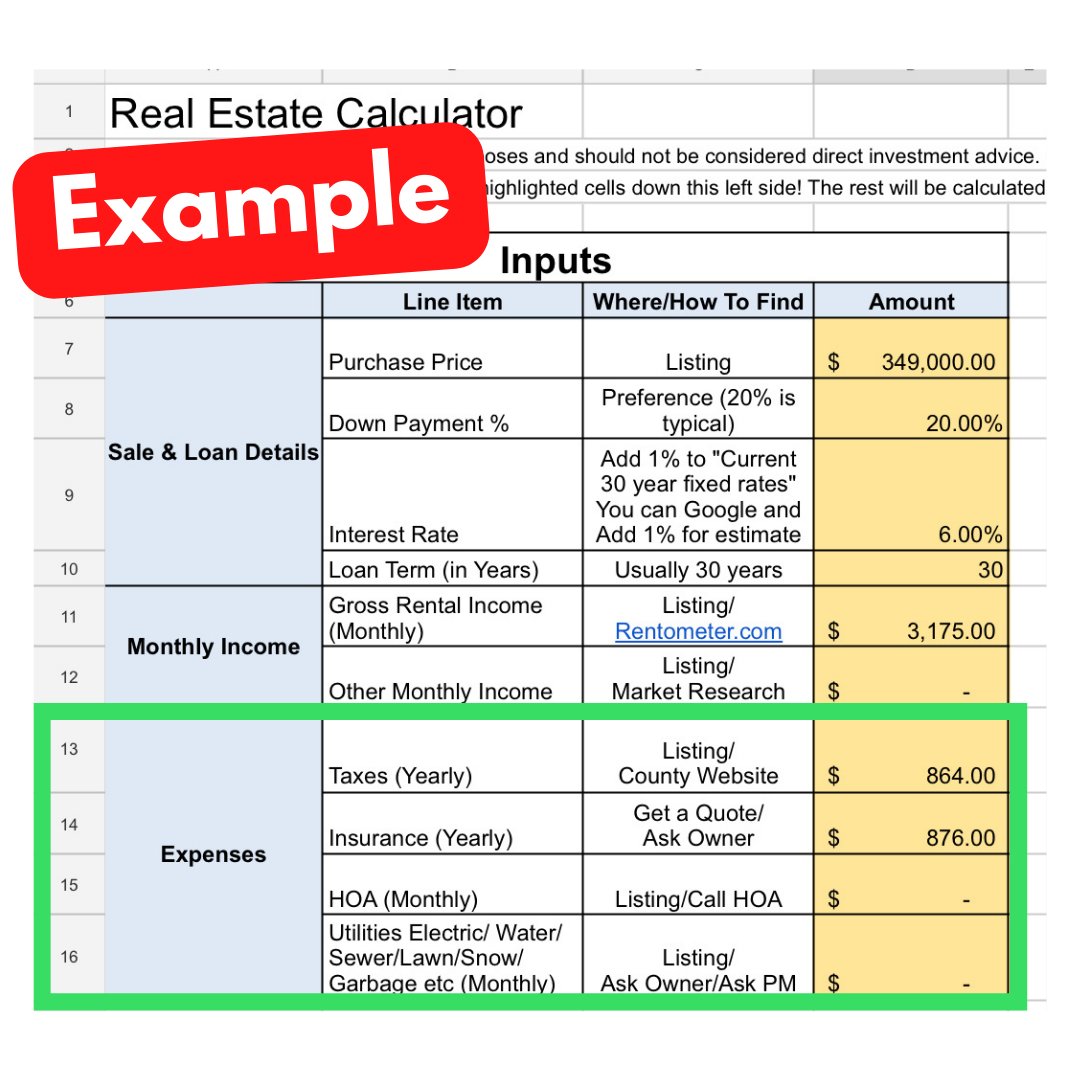

Expenses:

1. Mortgage Payment: You can put the sale and loan details from above into a mortgage calculator to see what your monthly mortgage payment will be

2. Property Taxes: Can be found on the listing or the county's property appraiser's website

1. Mortgage Payment: You can put the sale and loan details from above into a mortgage calculator to see what your monthly mortgage payment will be

2. Property Taxes: Can be found on the listing or the county's property appraiser's website

3. Insurance: You can call an Insurance Provider and get a quote for your area. Every area is drastically different.

Ex: Florida has hurricanes.

4. Vacancy Reserve: 10% of gross income set aside for potential vacancies

Ex: Florida has hurricanes.

4. Vacancy Reserve: 10% of gross income set aside for potential vacancies

5. Maintenance/CapEx: Typically plan to set aside 15% of Gross Rent for

6. Property Management: Typically 8-10% of Gross Rent

7. HOA: On the listing, if there is one.

8. Utilities: Sometimes the owner pays none, some or all of the utilities. Should be on the listing as well.

6. Property Management: Typically 8-10% of Gross Rent

7. HOA: On the listing, if there is one.

8. Utilities: Sometimes the owner pays none, some or all of the utilities. Should be on the listing as well.

Returns:

1. NOI- Net Operating Income aka Net Income without factoring in the mortgage payment

2. Monthly Cash Flow: NOI after monthly mortgage payment

3. Cash on Cash Return: Cash flow divided by cash you put into the deal

1. NOI- Net Operating Income aka Net Income without factoring in the mortgage payment

2. Monthly Cash Flow: NOI after monthly mortgage payment

3. Cash on Cash Return: Cash flow divided by cash you put into the deal

Extra Returns:

1. Appreciation: Estimated 3% of the purchase price per year

2. Loan Paydown: The estimated amount the tenants' paid down the principal balance on the mortgage

3. Interest Write-Off and Depreciation: Estimated Tax Advantages

1. Appreciation: Estimated 3% of the purchase price per year

2. Loan Paydown: The estimated amount the tenants' paid down the principal balance on the mortgage

3. Interest Write-Off and Depreciation: Estimated Tax Advantages

All the pictures you saw are from my personal Deal Calculator, which allows me to run the numbers on any property in less than 60 seconds.

🔥 If you want it FOR FREE, you can download it here! 👇

In return, all I ask is that you RT the original tweet!

cheerful-motivator-7904.ck.page

🔥 If you want it FOR FREE, you can download it here! 👇

In return, all I ask is that you RT the original tweet!

cheerful-motivator-7904.ck.page

Here is the original tweet so you can click and RT it, hope you enjoy the calculator, cheers! 👇

Loading suggestions...