As the stock price tanks,

A lot of speculation is evident on the HDFC Bank

Is HDFC losing its market leadership position?

Is the business strong or is there a problem in HDFC Bank?

A comprehensive thread🧵on the business of HDFC Bank and what lies ahead?

Lets go👇

A lot of speculation is evident on the HDFC Bank

Is HDFC losing its market leadership position?

Is the business strong or is there a problem in HDFC Bank?

A comprehensive thread🧵on the business of HDFC Bank and what lies ahead?

Lets go👇

How is the HDFC Bank business doing:-

Advances growth:-

Over the last 4 years

HDFC Bank has shown consistent growth of 15-20% in its advances.

Despite slowdown in the Retail loan growth,

Over the last 4 years the Bank has done exceptionally well.

Advances growth:-

Over the last 4 years

HDFC Bank has shown consistent growth of 15-20% in its advances.

Despite slowdown in the Retail loan growth,

Over the last 4 years the Bank has done exceptionally well.

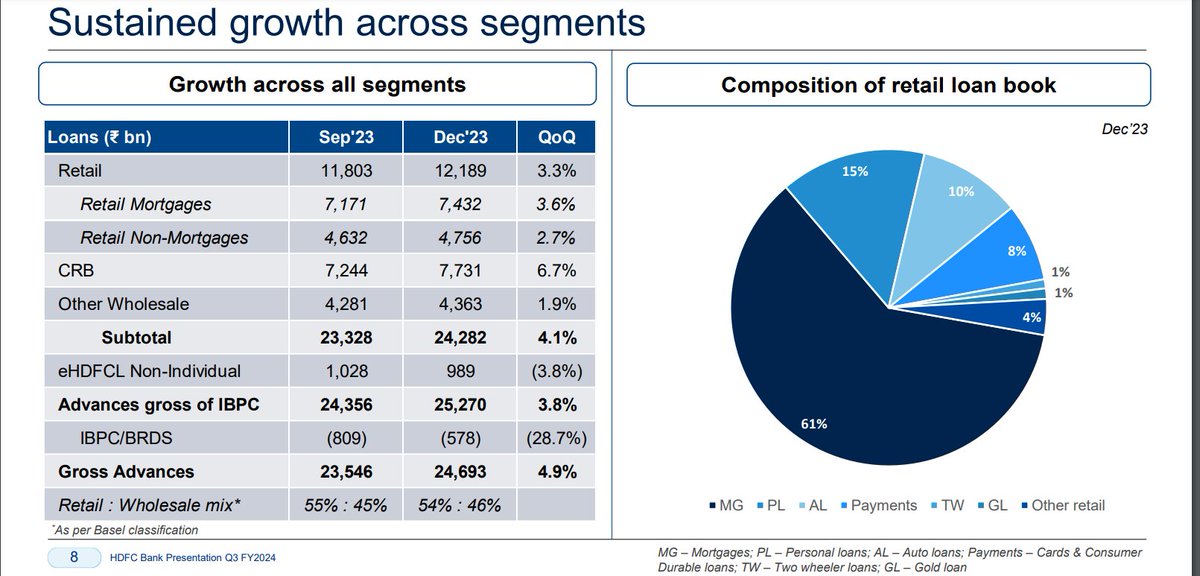

Ever since the merger with HDFC limited

HDFC Bank now has 54% retail loans and 46% wholesale loans

HDFC Bank now has 54% retail loans and 46% wholesale loans

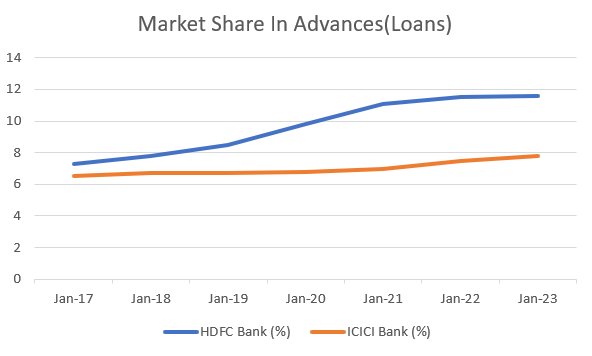

Market Share of HDFC Bank and ICICI Bank

Over the last 7-8 years

Both HDFC Bank and ICICI Bank have gained market share on Advances

Over the last 3 years,

HDFC Bank has gained much more market share

Market Share For HDFC Bank

FY17-7.3%

FY23-11.6%(Before merger)

FY25-15.40%(After merger)

Market Share for ICICI Bank

FY17-6.5%

FY23-7.8%

Some key trends:-

🏦Large private banks are cornering market share from PSU Banks and small private Banks

🏦The business of HDFC Bank is rock solid as it continues to gain market share.

🏦ICICI Bank will start to make large gains in the next 5 years as well

🏦Scale of HDFC is now nearly twice of ICICI Bank

Over the last 7-8 years

Both HDFC Bank and ICICI Bank have gained market share on Advances

Over the last 3 years,

HDFC Bank has gained much more market share

Market Share For HDFC Bank

FY17-7.3%

FY23-11.6%(Before merger)

FY25-15.40%(After merger)

Market Share for ICICI Bank

FY17-6.5%

FY23-7.8%

Some key trends:-

🏦Large private banks are cornering market share from PSU Banks and small private Banks

🏦The business of HDFC Bank is rock solid as it continues to gain market share.

🏦ICICI Bank will start to make large gains in the next 5 years as well

🏦Scale of HDFC is now nearly twice of ICICI Bank

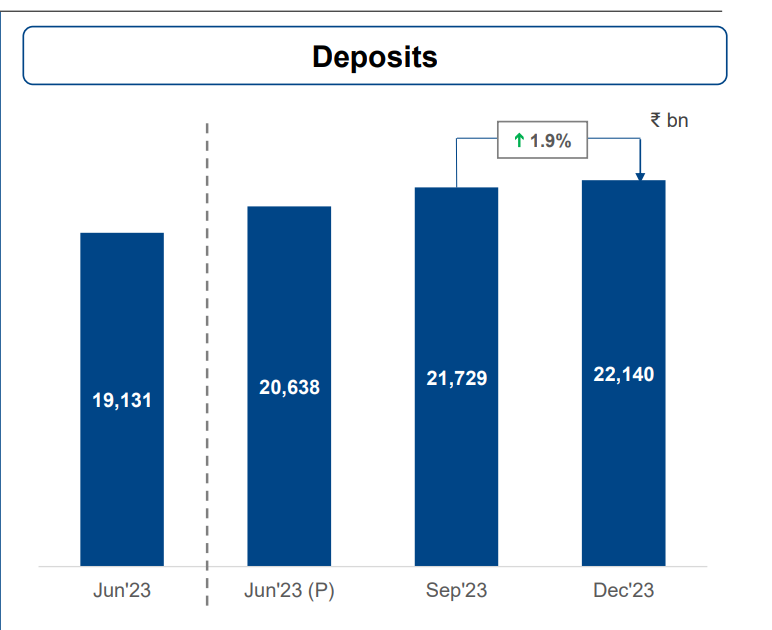

Deposit Growth:-

HDFC Bank continues to add strong deposits

The banks added nearly 1502 billion in deposits over the last 1 year.

The growth in deposits has been maintained at about 15%

This is higher than the system deposit growth.

HDFC Bank continues to add strong deposits

The banks added nearly 1502 billion in deposits over the last 1 year.

The growth in deposits has been maintained at about 15%

This is higher than the system deposit growth.

Market Share in Deposits:-

HDFC Bank has been gaining deposit market share over the last 4 years

Market Share in deposits has grown from:-

FY17-6.0%

FY23-10%(Before merger)

The deposit accretion is fairly steady

HDFC Bank has been gaining deposit market share over the last 4 years

Market Share in deposits has grown from:-

FY17-6.0%

FY23-10%(Before merger)

The deposit accretion is fairly steady

So where is the problem in deposits?

As HDFC Limited merged with HDFC Bank

High cost deposit share went up from 7% to about 21%.

This means the cost of funds has shot up for HDFC Bank:-

June '22 ~3.1%

Sep '22 ~3.3%

Dec '22 ~3.5%

Mar '23 ~3.7%

Merger

June '23 ~4%

Sep '23 ~4.8%

Dec '23 ~4.9%

The sharp increase has been upto 1%.

This has meant a sharp dent in Net Interest Margins

As HDFC Limited merged with HDFC Bank

High cost deposit share went up from 7% to about 21%.

This means the cost of funds has shot up for HDFC Bank:-

June '22 ~3.1%

Sep '22 ~3.3%

Dec '22 ~3.5%

Mar '23 ~3.7%

Merger

June '23 ~4%

Sep '23 ~4.8%

Dec '23 ~4.9%

The sharp increase has been upto 1%.

This has meant a sharp dent in Net Interest Margins

How is HDFC Bank coping up with its increased demand for deposits?

HDFC's deposit growth is just fine at 15% growth

But the sharp need for it to replace HDFC Ltd's borrowing means the demand for deposits is higher at HDFC Bank.

HDFC Bank has opened 1000 branches over the last 1 year.

These branches will start to mobilize deposits over the next 2-3 years.

HDFC's deposit growth is just fine at 15% growth

But the sharp need for it to replace HDFC Ltd's borrowing means the demand for deposits is higher at HDFC Bank.

HDFC Bank has opened 1000 branches over the last 1 year.

These branches will start to mobilize deposits over the next 2-3 years.

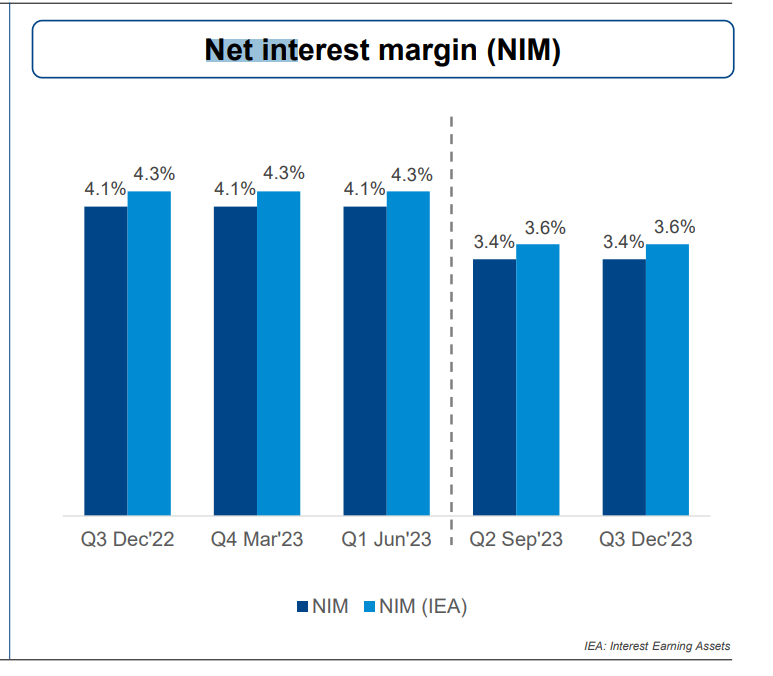

Net Interest Margin:-

HDFC Bank has seen a sharp erosion in margins as the merger took place

The main reasons

1. Higher cost of funds for HDFC Ltd

2.Lower Yield for HDFC ltd

3. Slowdown in unsecured retail loans by HDFC Bank.

As borrowings gets replaced and HDFC Bank starts to push unsecured retail loans.

The NIM will steadily recover,

But this will take at least 2-4 quarters to play out.

This is longer than anyone had expected.

But that is how the merger is playing out

HDFC Bank has seen a sharp erosion in margins as the merger took place

The main reasons

1. Higher cost of funds for HDFC Ltd

2.Lower Yield for HDFC ltd

3. Slowdown in unsecured retail loans by HDFC Bank.

As borrowings gets replaced and HDFC Bank starts to push unsecured retail loans.

The NIM will steadily recover,

But this will take at least 2-4 quarters to play out.

This is longer than anyone had expected.

But that is how the merger is playing out

Asset Quality:-

One would be really very worried if there was an asset quality problem with HDFC Bank

On the contrary,

Asset quality for HDFC Bank continues to be stable with nothing to complain about.

Credit costs are coming down

The company is adequately provided for with the provisions.

One would be really very worried if there was an asset quality problem with HDFC Bank

On the contrary,

Asset quality for HDFC Bank continues to be stable with nothing to complain about.

Credit costs are coming down

The company is adequately provided for with the provisions.

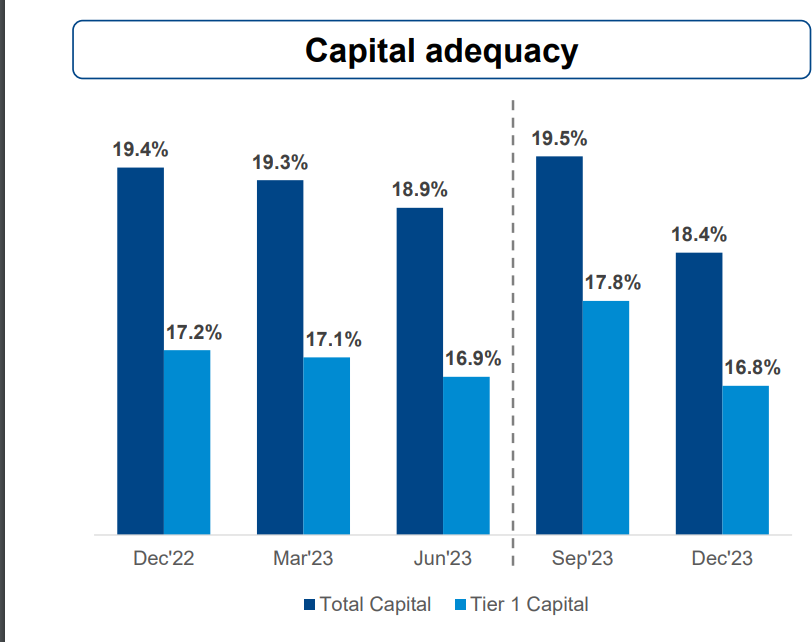

HDFC Bank sits on Strong capital adequacy ratios

18.4% capital adequacy and

TIER-1 capital adequacy at 16.8%

The bank is sufficiently capitalized for now

18.4% capital adequacy and

TIER-1 capital adequacy at 16.8%

The bank is sufficiently capitalized for now

Technology problems:-

HDFC historically has been very very slow at adapting technology.

Some of the interfaces just lacked smooth functioning.

The bank has taken the first step by launching the all new Payzapp which is really very smooth.

Over the next 1 year we will see complete overhaul of the digital platforms from HDFC Bank

HDFC historically has been very very slow at adapting technology.

Some of the interfaces just lacked smooth functioning.

The bank has taken the first step by launching the all new Payzapp which is really very smooth.

Over the next 1 year we will see complete overhaul of the digital platforms from HDFC Bank

Is there a problem with the leadership?

Mt Shashidhar jagdishan has been at HDFC Bank for many years now.

He understands the bank inside out.

The merger b/w HDFC And HDFC Bank is big

It will require time to stabilize.

However, the bank is doing the right things under the new leadership

1. Garnering deposits faster

2. Working on tech issues

3. Expanding branch network

4. Prioritising margins over growth

and a lot more

Mt Shashidhar jagdishan has been at HDFC Bank for many years now.

He understands the bank inside out.

The merger b/w HDFC And HDFC Bank is big

It will require time to stabilize.

However, the bank is doing the right things under the new leadership

1. Garnering deposits faster

2. Working on tech issues

3. Expanding branch network

4. Prioritising margins over growth

and a lot more

So the business is fairly resilient for HDFC Bank.

Advance growth of 15-20% can be achieved for the bank in the next 4 years

Deposit mobilisation is just fine but needs to pick up given the need to replace deposits

Asset quality is fairly stable.

Capital is not a problem

NIMs need to recover.

Advance growth of 15-20% can be achieved for the bank in the next 4 years

Deposit mobilisation is just fine but needs to pick up given the need to replace deposits

Asset quality is fairly stable.

Capital is not a problem

NIMs need to recover.

So why did the HDFC Bank stock tank?

Frankly,the stabilisation of the internal performance of HDFC Bank is taking much more time than expected.

The increase in cost of funds is higher than expected.

This has hit profitability and NIMs.

And this is the thing the market is not happy about.

But this is not a problem that cannot be solved.

It is not as big a problem as poor asset quality.

Frankly,the stabilisation of the internal performance of HDFC Bank is taking much more time than expected.

The increase in cost of funds is higher than expected.

This has hit profitability and NIMs.

And this is the thing the market is not happy about.

But this is not a problem that cannot be solved.

It is not as big a problem as poor asset quality.

Valuation:-

HDFC Bank once used to trade ar 4xP/B.

Now trades at 2xP/B.

Given the subsidiaries of HDFC Bank

The stock now trades at 1.5x-1.8x P/Bx

The problems are fairly known to the amrker

HDFC Bank once used to trade ar 4xP/B.

Now trades at 2xP/B.

Given the subsidiaries of HDFC Bank

The stock now trades at 1.5x-1.8x P/Bx

The problems are fairly known to the amrker

Is ICICI bank the next HDFC Bank?

Is ICICI bank the new market leader?

Both ICICI Bank and HDFC Bank have

1. Strong Balance Sheet

2. Strong Management

3. Strong capital to deploy

4. Huge physical as well as digital presence to tap growth

5. Low cost of funds

Is ICICI bank the new market leader?

Both ICICI Bank and HDFC Bank have

1. Strong Balance Sheet

2. Strong Management

3. Strong capital to deploy

4. Huge physical as well as digital presence to tap growth

5. Low cost of funds

Both these banks are very strong,the scope of opportunity means that all can do extremely well. ICICI+HDFC combo will lead India in the next decade to come!

So what now for HDFC Bank?

The Bank will take time to stabilize.

The internal metrics are a key thing to watch over the coming quarters.

As the bank focusses on getting NIMs upto 4%.

The machine that is HDFC Bank will start to fire.

As a business HDFC Bank is just doing fairly okay.

Stabilisation of merger will be the key theme over the next 1 year

The Bank will take time to stabilize.

The internal metrics are a key thing to watch over the coming quarters.

As the bank focusses on getting NIMs upto 4%.

The machine that is HDFC Bank will start to fire.

As a business HDFC Bank is just doing fairly okay.

Stabilisation of merger will be the key theme over the next 1 year

Keep following me -@AdityaD_Shah as I write daily to make you aware around:

📈Personal Finance

📈Investing

📈Stock Analysis

Go to my profile and hit the bell icon🔔to always stay updated

📈Personal Finance

📈Investing

📈Stock Analysis

Go to my profile and hit the bell icon🔔to always stay updated

Disclaimer:-

This is my own study

Not an investment recommendation

Please consult your own financial advisor before making any investment decisions

This is my own study

Not an investment recommendation

Please consult your own financial advisor before making any investment decisions

Loading suggestions...