Renting a home is often financially superior to owning.

A common perception is that buying is a better decision if you can purchase a home with a mortgage payment equal to or less than what you would otherwise pay in rent.

This perception is flawed.

A common perception is that buying is a better decision if you can purchase a home with a mortgage payment equal to or less than what you would otherwise pay in rent.

This perception is flawed.

A mortgage payment does not tell you the cost of owning a home.

To properly assess the rent versus buy decision, we need to compare the total unrecoverable costs of renting to the total unrecoverable costs of owning.

To properly assess the rent versus buy decision, we need to compare the total unrecoverable costs of renting to the total unrecoverable costs of owning.

Crunching those numbers results in a simple metric to evaluate the rent vs. buy decision.

To start, I need to lay out some background information and assumptions.

An unrecoverable cost is a cost that you pay with no residual value. Rent is an obvious unrecoverable cost.

To start, I need to lay out some background information and assumptions.

An unrecoverable cost is a cost that you pay with no residual value. Rent is an obvious unrecoverable cost.

The unrecoverable costs for a homeowner are property taxes, maintenance costs, and the cost of capital. These costs are comparable to rent.

Property taxes are pretty easy for most people to grasp. You pay the tax to own the home and there is no residual value.

Property taxes are pretty easy for most people to grasp. You pay the tax to own the home and there is no residual value.

Maintenance costs can be high, like replacing a roof or updating a kitchen, but they can also be small things like re-doing the caulking in the bathroom.

These costs either show up as explicit costs or as depreciation in the building value over time.

These costs either show up as explicit costs or as depreciation in the building value over time.

Pinning down the right number to estimate maintenance costs is not easy.

Statistics Canada uses 1.5% of the building's value as a depreciation expense in the CPI basket; this figure aligns with multiple academic studies and the statistical agencies of

other countries.

Statistics Canada uses 1.5% of the building's value as a depreciation expense in the CPI basket; this figure aligns with multiple academic studies and the statistical agencies of

other countries.

The cost of capital is the opportunity cost of equity in the home, and the cost of mortgage debt.

Globally, real estate has historically appreciated at about 1% real per year, or 3.5% nominal assuming 2.5% inflation. Stocks have appreciated at a higher rate.

Globally, real estate has historically appreciated at about 1% real per year, or 3.5% nominal assuming 2.5% inflation. Stocks have appreciated at a higher rate.

PWL Capital's estimate for expected stock returns is 6.97% nominal. This suggests a greater than 3% opportunity cost for home equity vs. stocks.

Mortgage rates in Canada are currently around 4.5%. Borrowing at 4.5% to finance a home appreciating at 3.5% costs 1%.

Mortgage rates in Canada are currently around 4.5%. Borrowing at 4.5% to finance a home appreciating at 3.5% costs 1%.

The blended cost of capital will depend on how the home is financed.

Taking all of these unrecoverable costs together - property tax, maintenance / depreciation, and the cost of capital - we get a single figure that can be used for a simple comparison to rent.

Taking all of these unrecoverable costs together - property tax, maintenance / depreciation, and the cost of capital - we get a single figure that can be used for a simple comparison to rent.

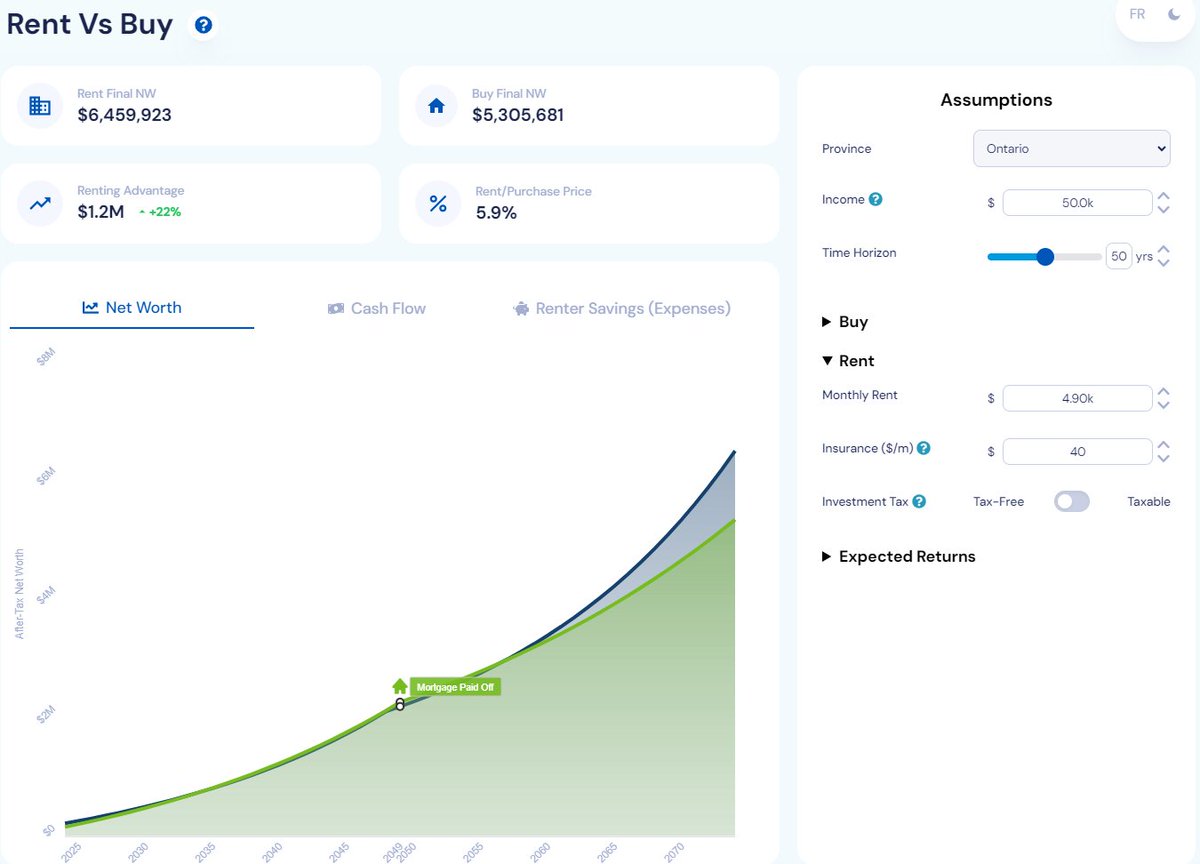

The results will vary based on the inputs, but I typically find a number between 5 and 6% of the home value.

If you can rent for less than that, renting is a sensible financial decision.

The estimated unrecoverable cost for a $1m home is $50,000 per year, or $4,166 per month.

If you can rent for less than that, renting is a sensible financial decision.

The estimated unrecoverable cost for a $1m home is $50,000 per year, or $4,166 per month.

The math changes if your investments are taxable. In Canada, increases in the value of the primary residence are not taxed, while investments held in a taxable account are.

This lowers the relative expected investment return on stocks, lowering your opportunity cost.

This lowers the relative expected investment return on stocks, lowering your opportunity cost.

Similarly, a very conservative investor would not use stocks as the counterfactual investment to estimate their opportunity cost.

Importantly, there are also many non-financial reasons that someone might decide to either rent or own.

Importantly, there are also many non-financial reasons that someone might decide to either rent or own.

Owning hedges your future housing consumption costs, but can be risky if you need to move to a new location unexpectedly.

Renting is more flexible and lower risk if you need to move, but rents can increase rapidly.

Renting is more flexible and lower risk if you need to move, but rents can increase rapidly.

Personally, I find home ownership to be mentally expensive. Managing and maintaining a home is a job in itself, and it's a job I don't like doing.

I don't have a model for that, but I do have a model for the financial component of the rent vs. buy decision. Enjoy!

I don't have a model for that, but I do have a model for the financial component of the rent vs. buy decision. Enjoy!

Want to see how PWL helps Canadians make better financial decisions?

Meet with PWL: calendly.com

Meet with PWL: calendly.com

Loading suggestions...