The Main Types of #Depreciation Methods ⬇️

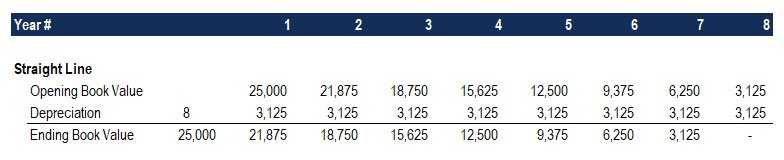

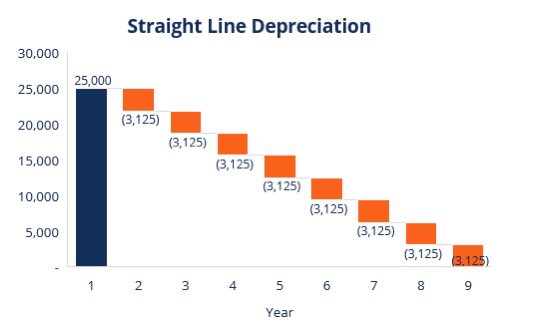

1- Straight-line depreciation : is a very common, and the simplest, method of calculating depreciation expense. In straight-line depreciation, the expense amount is the same every year over the useful life of the asset.

Depreciation Formula for the Straight Line Method:

Depreciation Expense = (Cost – Salvage value) / Useful life

Example

Consider a piece of equipment that costs $25,000 with an estimated useful life of 8 years and a $0 salvage value.

Depreciation Expense = (Cost – Salvage value) / Useful life

Example

Consider a piece of equipment that costs $25,000 with an estimated useful life of 8 years and a $0 salvage value.

The depreciation expense per year for this equipment would be ($25,000 – $0) / 8 = $3,125 per year.

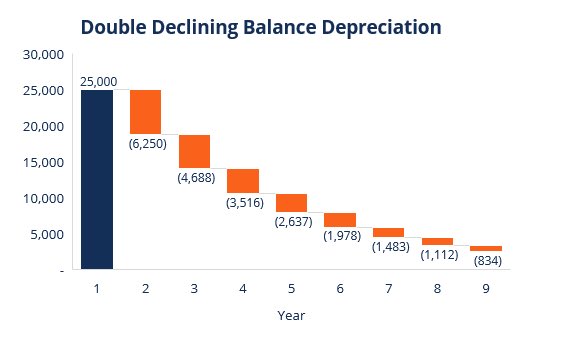

2- Compared to other depreciation methods,double-declining-balance depreciation results in a larger amount expensed in the earlier years as opposed to the later years of an asset’s useful life. In this method, the depreciation factor is 2x that of the straight-line expense method

Depreciation formula for the double-declining balance method:

Periodic Depreciation Expense = Beginning book value x Rate of depreciation

Periodic Depreciation Expense = Beginning book value x Rate of depreciation

Example

Consider a piece of property, plant, and equipment (PP&E) that costs $25,000, with an estimated useful life of 8 years and a $2,500 salvage value. To calculate the double-declining balance depreciation, set up a schedule:

Consider a piece of property, plant, and equipment (PP&E) that costs $25,000, with an estimated useful life of 8 years and a $2,500 salvage value. To calculate the double-declining balance depreciation, set up a schedule:

1.The rate of depreciation (Rate) is calculated as follows:

Expense = (100% / Useful life of asset) x 2

Expense = (100% / 8) x 2 = 25% .

Note: Since this is a double-declining method, we multiply the rate of depreciation by 2.

Expense = (100% / Useful life of asset) x 2

Expense = (100% / 8) x 2 = 25% .

Note: Since this is a double-declining method, we multiply the rate of depreciation by 2.

2- Multiply the rate of depreciation by the beginning book value to determine the expense for that year. For example, $25,000 x 25% = $6,250 depreciation expense.

The ending book value for that year is the beginning book value for the following year

The ending book value for that year is the beginning book value for the following year

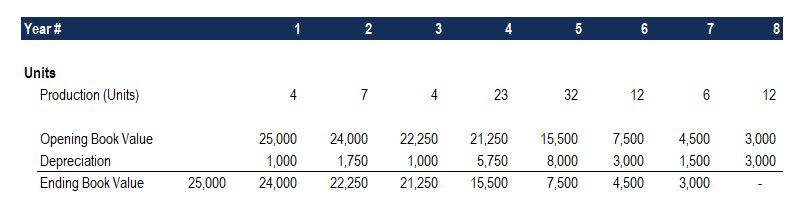

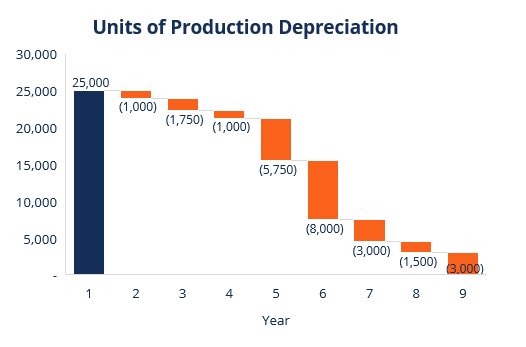

3- The units-of-production depreciation method depreciates assets based on the total number of hours used or the total number of units to be produced by using the asset, over its useful life.

The formula for the units-of-production method:

Depreciation Expense = (Number of units produced / Life in number of units) x (Cost – Salvage value).

Depreciation Expense = (Number of units produced / Life in number of units) x (Cost – Salvage value).

Example

Consider a machine that costs $25,000, with an estimated total unit production of 100 million and a $0 salvage value. During the first quarter of activity, the machine produced 4 million units

Consider a machine that costs $25,000, with an estimated total unit production of 100 million and a $0 salvage value. During the first quarter of activity, the machine produced 4 million units

To calculate the depreciation expense using the formula above:

Depreciation Expense = (4 million / 100 million) x ($25,000 – $0) = $1,000.

Depreciation Expense = (4 million / 100 million) x ($25,000 – $0) = $1,000.

@rattibha

رتب💙

رتب💙

Loading suggestions...