Sudarshan Chemical- The focus pigment player has their conducted their concall today at 11:00 am.

Here are the key highlights 😃

Here are the key highlights 😃

About Company:

• Surdarshan is in color goldflask.

• Co. has 2 goldflask site. One in Roha which is scalable and dedicated R&D site on outskirt of Pune.

• Co. has 50-60+ Channel partner, 50-60 sales people with 2000 workforce.

• Focus on colors and pigment.

• Surdarshan is in color goldflask.

• Co. has 2 goldflask site. One in Roha which is scalable and dedicated R&D site on outskirt of Pune.

• Co. has 50-60+ Channel partner, 50-60 sales people with 2000 workforce.

• Focus on colors and pigment.

Business Updates:

• Global reach in 85+ countries.

• Latest addition of sub subsidiary- Sudarshan Japan.

• Domestic Market Share is 35%.

• Renewable Energy now stands at 20% which was 0% past 10 years.

• Global reach in 85+ countries.

• Latest addition of sub subsidiary- Sudarshan Japan.

• Domestic Market Share is 35%.

• Renewable Energy now stands at 20% which was 0% past 10 years.

Industry & Covid Impact:

• Co. has global market opportunity of 8.6Bill $.

• Plastic has seen low impact on covid.

• Packing has also seen low impact with good recovery.

• Paint / Coatings was impacted due to covid.

• Supply Chain was hampered and RM prices increased.

• Co. has global market opportunity of 8.6Bill $.

• Plastic has seen low impact on covid.

• Packing has also seen low impact with good recovery.

• Paint / Coatings was impacted due to covid.

• Supply Chain was hampered and RM prices increased.

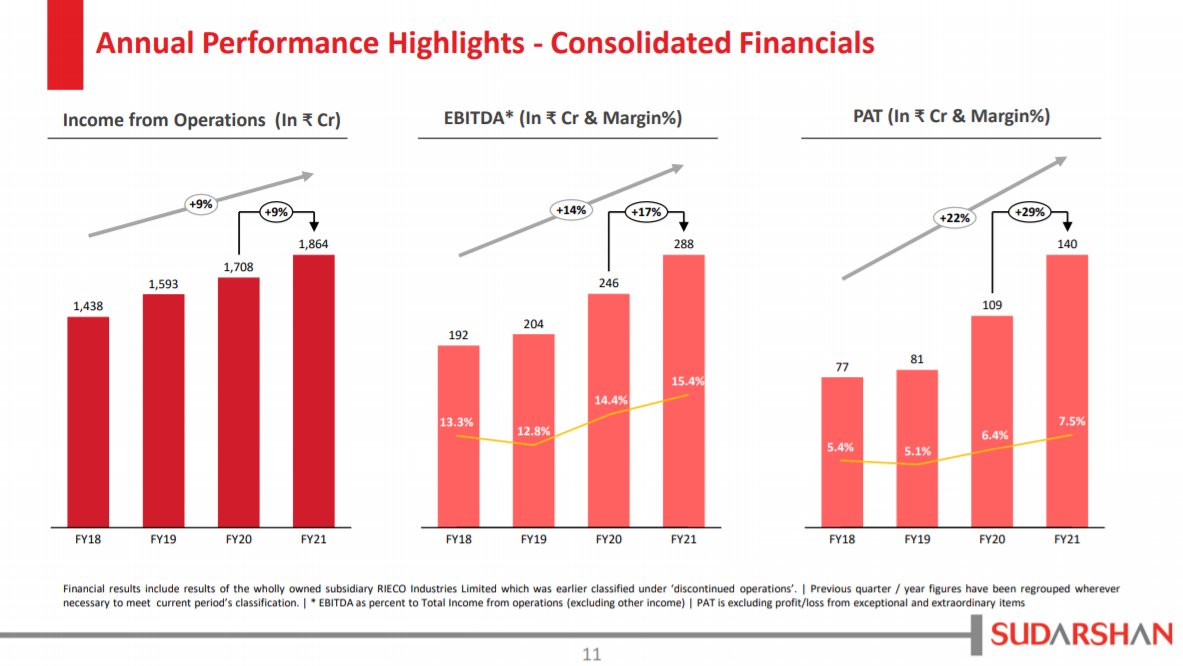

Pigment: Performance mentioned in image.

• Business improved 10% YoY.

• Export sales improved 14% and is expected to increase in the coming year as well.

• Business improved 10% YoY.

• Export sales improved 14% and is expected to increase in the coming year as well.

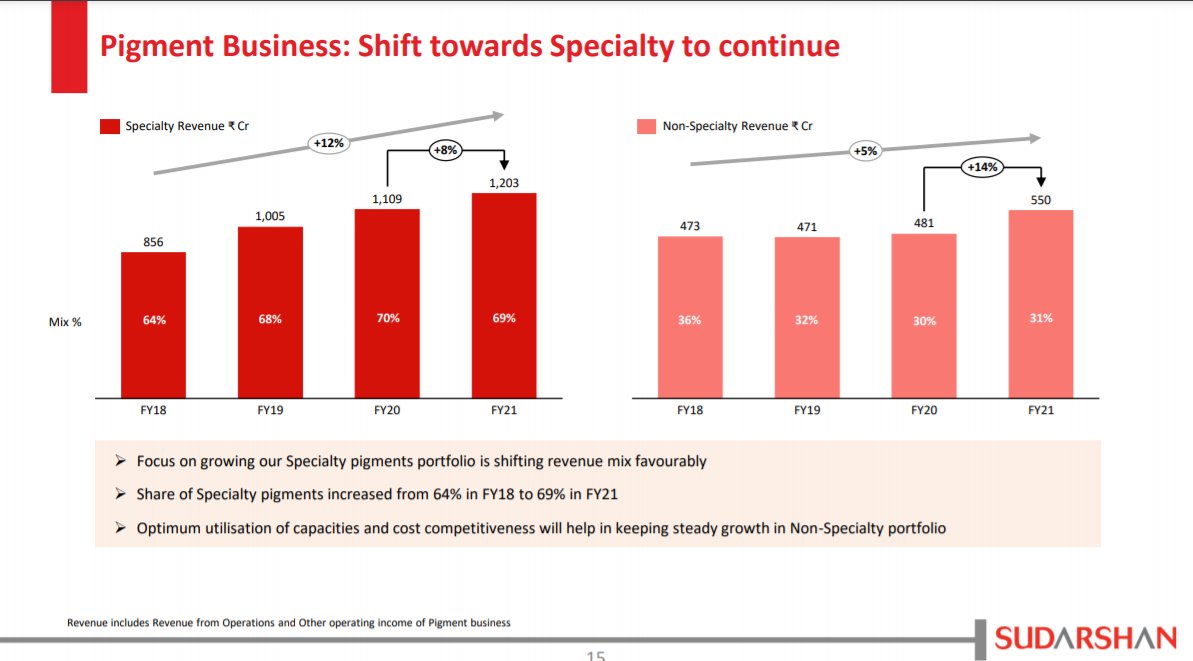

Specialty: Performance in image

• Specialty segment contributes 69% of sales. Rest by non-specialty.

• Major CAPEX is on Specialty, hence post capex this segment is expected to grow more; leading to increase in margin.

• Specialty segment contributes 69% of sales. Rest by non-specialty.

• Major CAPEX is on Specialty, hence post capex this segment is expected to grow more; leading to increase in margin.

Raw Material:

• There was increase in price of RM in all the product basket.

• While certain Acetic Acid, Urea based RM has steep rise in market.

• Sourcing from China has not decrease for Sudarshan.

• There was increase in price of RM in all the product basket.

• While certain Acetic Acid, Urea based RM has steep rise in market.

• Sourcing from China has not decrease for Sudarshan.

Margins Profile

• Some of the increased RM prices are passed to certain customer in March. Rest will be passed this quarter.

• Coal rate has grown up, while shipment cost also has gone up this quarter.

• Some of the increased RM prices are passed to certain customer in March. Rest will be passed this quarter.

• Coal rate has grown up, while shipment cost also has gone up this quarter.

Competitive:

• Company has international sales team o board, while Sudarshan has R&D facility which differentiates co. from other Asian players, which lead to decrease in margin but has long term benefit.

• Company has international sales team o board, while Sudarshan has R&D facility which differentiates co. from other Asian players, which lead to decrease in margin but has long term benefit.

CAPEX:

• None of the capex were canceled.

• 293 cr is put in use and 269 is in CWIP. Timeline of CAPEX mentioned in image.

• With specialty product coming up, margins are expected to be increased.

• New expansion now would be there on backward integration.- via Brown field.

• None of the capex were canceled.

• 293 cr is put in use and 269 is in CWIP. Timeline of CAPEX mentioned in image.

• With specialty product coming up, margins are expected to be increased.

• New expansion now would be there on backward integration.- via Brown field.

• FY 22: Out of 600 cr CAPEX 307cr will be there this year, out of which 269 cr is done till now and rest will done in coming quarter.

• There is separate CAPEX of 135 cr announced previously which is for the infrastructure purpose.

• Maintenance CAPEX till now was: 30-35cr

• There is separate CAPEX of 135 cr announced previously which is for the infrastructure purpose.

• Maintenance CAPEX till now was: 30-35cr

New Product:

• New product has good launch till now. However major launch will be in Q2 this year.

• Investment in new product is done. Co. now focus on introducing cost leadership- which is for backward integration.

• New product has good launch till now. However major launch will be in Q2 this year.

• Investment in new product is done. Co. now focus on introducing cost leadership- which is for backward integration.

Capacity Utlization:

• Currently is around 86%. This can go till 90% as well but major growth from capex side of revenue.

Net Debt:

• Net debt as of March 2021 was 641 cr. Co is looking for reducing its debt as well.

• Currently is around 86%. This can go till 90% as well but major growth from capex side of revenue.

Net Debt:

• Net debt as of March 2021 was 641 cr. Co is looking for reducing its debt as well.

Loading suggestions...