KRBL conducted their concall today at 4:00 Pm

Here are the key highlights 😀

Here are the key highlights 😀

Business Updates:

• Net debt of the company has reduced with improvement in interest coverage ratio.

• MSP in Paddy has increased by 4% to Rs 1940 per quintal. This will drive a reduction in total Basmati crop size by 5-10%

• Business is coming back to normalcy.

• Net debt of the company has reduced with improvement in interest coverage ratio.

• MSP in Paddy has increased by 4% to Rs 1940 per quintal. This will drive a reduction in total Basmati crop size by 5-10%

• Business is coming back to normalcy.

India Gate:

• India Gate brand improved 20%.

• There was transportation issued in the Q4, where export was hampering a lot. However things have improved and co. was back on track at the end of quarter.

• India Gate brand improved 20%.

• There was transportation issued in the Q4, where export was hampering a lot. However things have improved and co. was back on track at the end of quarter.

Basmati:

• 40% of product is now sold through package marketing, while 60% of Basmati is still sold on loose based.

• 40% of product is now sold through package marketing, while 60% of Basmati is still sold on loose based.

New Production launch:

• Flax and Chia Seeds are launched- expanding health portfolio.

• Domestically Idli Rava and Rice Flour package.

• Flax and Chia Seeds are launched- expanding health portfolio.

• Domestically Idli Rava and Rice Flour package.

Strategy:

• Company has shifted to integrated supply channel.

• Launched Project Disha.

• 30% of revenue now comes from wholesale distributors. KRBL also intending to increase sales team.

• E-Commerce has been focused. E-commerce share has been increase from 0.3% to 4% YoY.

• Company has shifted to integrated supply channel.

• Launched Project Disha.

• 30% of revenue now comes from wholesale distributors. KRBL also intending to increase sales team.

• E-Commerce has been focused. E-commerce share has been increase from 0.3% to 4% YoY.

Company will increasing the distributors count and focus remains on improving the supply chain front.

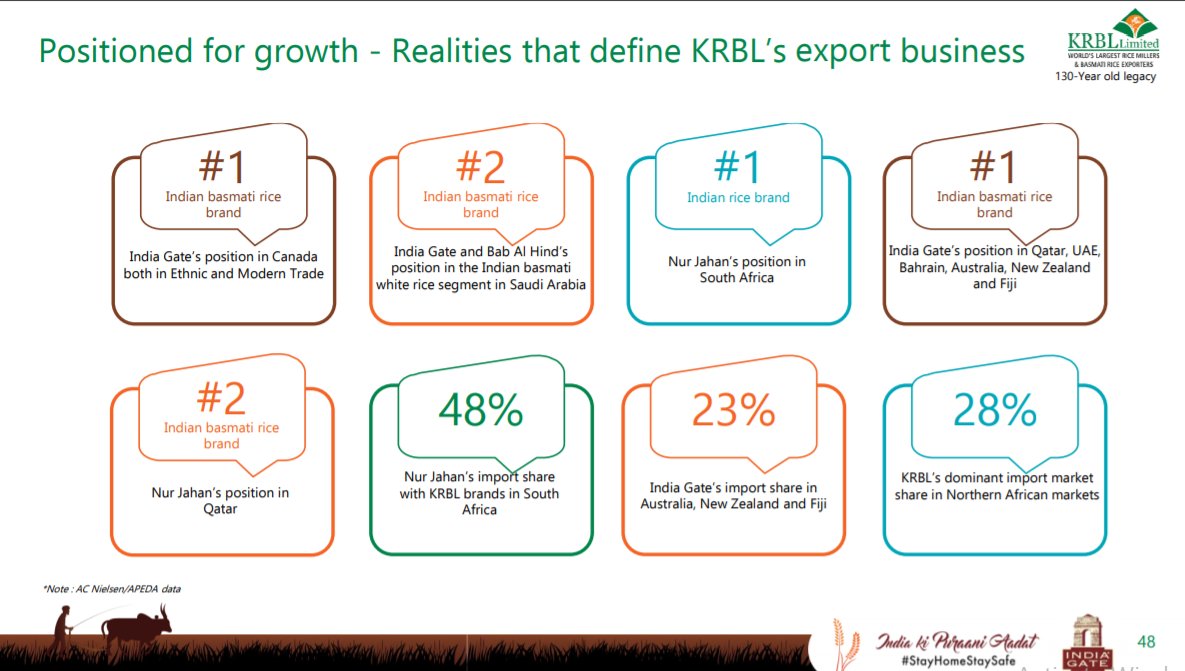

Export:

• Dominant Player in Basmati Side in Middle East.

• Export sales increase 11% QoQ.

• America market is growing well.

• In Australia, KRBL is still the dominant player.

• KRBL continuous to remain dominant brand in the export market.

• Widen the distribution market

• Dominant Player in Basmati Side in Middle East.

• Export sales increase 11% QoQ.

• America market is growing well.

• In Australia, KRBL is still the dominant player.

• KRBL continuous to remain dominant brand in the export market.

• Widen the distribution market

• In export market certain region are seeing 100% pipeline growth due to lower base.

• Certain product also gets closed down due to lower acceptance, however the pipeline is currently healthy and growing well.

• Certain product also gets closed down due to lower acceptance, however the pipeline is currently healthy and growing well.

Europe Market:

• KRBL has lost 50% of the export market share in Europe due to pesticide issue (mainly in brown rice)

• Co. is working on this problem and expect 1 year to solve this problem.

• KRBL has lost 50% of the export market share in Europe due to pesticide issue (mainly in brown rice)

• Co. is working on this problem and expect 1 year to solve this problem.

• Past 2 quarters, there was muted growth, however consumption is changing now.

• People are shifting to branding product, where there is presence of KRBL has. Premium product is seeing good traction, and mgmt expects exports business to improve well.

• People are shifting to branding product, where there is presence of KRBL has. Premium product is seeing good traction, and mgmt expects exports business to improve well.

Capital Allocation:

• Company is almost debt free with enough cash in hand.

• Company has sourced the rice at very lower level, and has inventory in hand as well.

• Company is almost debt free with enough cash in hand.

• Company has sourced the rice at very lower level, and has inventory in hand as well.

Corporate Announcement:

• Market has already discounted the share price of KRBL because of the corporate governance.

• The share price has been decreased more than 50% from high because of the issue and there is no much worse left, what mgmt thinks.

• Market has already discounted the share price of KRBL because of the corporate governance.

• The share price has been decreased more than 50% from high because of the issue and there is no much worse left, what mgmt thinks.

Cash Reserve:

• Company has much cash reserve, while dividend is still low.

• Mgmt wants to keep the BS strengthen, and working capital of the KRBL has higher requirement of liquidity.

• Co. has to hedge price for 2 year and sales required additional 1 year of hedging.

• Company has much cash reserve, while dividend is still low.

• Mgmt wants to keep the BS strengthen, and working capital of the KRBL has higher requirement of liquidity.

• Co. has to hedge price for 2 year and sales required additional 1 year of hedging.

• KRBL is having 1.5-2% advantage of bank borrowing with respect to other players in the market.

• There is no decrease in limit amount from bank, & co. can source loan at any time they want.

• With current cash balance, working capital can be manage without bank borrowing.

• There is no decrease in limit amount from bank, & co. can source loan at any time they want.

• With current cash balance, working capital can be manage without bank borrowing.

Realization:

• COGS has reduced 17% and revenue realization is reduced by 12%.

• Decrease in realization was due to lower value inventory stock available in hands of KRBL. This inventory has to be passed on the customer, hence there is lower utilization on inventory levels.

• COGS has reduced 17% and revenue realization is reduced by 12%.

• Decrease in realization was due to lower value inventory stock available in hands of KRBL. This inventory has to be passed on the customer, hence there is lower utilization on inventory levels.

Growth Trajectory:

• MSP of rice is increasing 10% every year, for incentivize farmer for growing Basmati.

• Non Basmati consumption is 88-90%, hence there is scope is available in Basmati segment as well.

• MSP of rice is increasing 10% every year, for incentivize farmer for growing Basmati.

• Non Basmati consumption is 88-90%, hence there is scope is available in Basmati segment as well.

Ethanol Blending:

• Ethanol product can only be made from waste, while Rice prices (MSP) are consistently growing up.

• Hence in north-east, Basmati Rice in ethanol blending will now be viable for the farmers.

• Ethanol product can only be made from waste, while Rice prices (MSP) are consistently growing up.

• Hence in north-east, Basmati Rice in ethanol blending will now be viable for the farmers.

Pricing:

• For premium products, KRBL never change the price in domestic and export.

• For premium products, KRBL never change the price in domestic and export.

For more discussion on Equity research and OI analysis

Subscribe to our YouTube channel 😃

Link 🖇: youtube.com

Subscribe to our YouTube channel 😃

Link 🖇: youtube.com

Loading suggestions...