India ---> 5th largest paper consumer

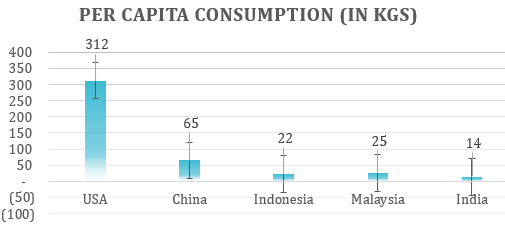

Still, per capita paper consumption much lower than global average

Still, per capita paper consumption much lower than global average

What is the interesting part?

10 yr growth rate (India) = 7.5% CAGR

10 yr growth rate (World) ~ 0%

Indian market is growing, world market has stagnated!

10 yr growth rate (India) = 7.5% CAGR

10 yr growth rate (World) ~ 0%

Indian market is growing, world market has stagnated!

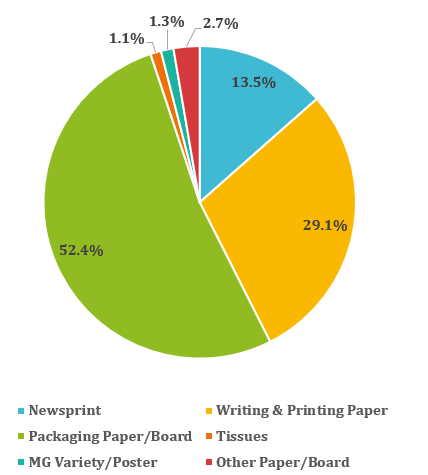

Industry Segmentation

Packaging & Tissue paper --> fastest growing segments (though in a small base)

Packaging & Tissue paper --> fastest growing segments (though in a small base)

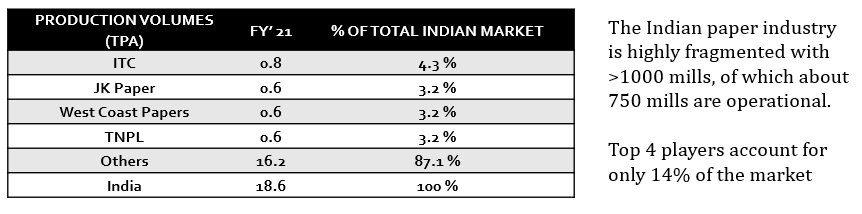

Paper Industry in India is highly fragmented

Top 4 players --> 14% capacity

Balance capacity --> 700+ paper mills

Top 4 players --> 14% capacity

Balance capacity --> 700+ paper mills

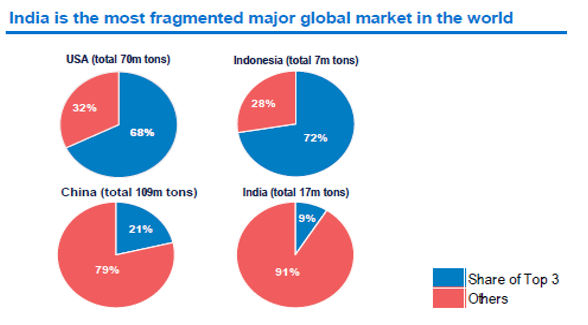

Globally, the paper industry is much more consolidated.

In India, as well consolidation over a period of time is expected.

In India, as well consolidation over a period of time is expected.

Key variables impacting Paper Industry

- Availability of raw material (Wood Pulp)

- Highly CAPEX intensive

- Environmental Compliances

- Volatility in Global Pulp Prices

- Availability of raw material (Wood Pulp)

- Highly CAPEX intensive

- Environmental Compliances

- Volatility in Global Pulp Prices

As in any commodity, China is the biggest factor

Biggest producer --> China

Biggest consumer --> China

China recently (Jan 2021) banned import of waste paper --> Significant rally in Global Pulp Prices

Biggest producer --> China

Biggest consumer --> China

China recently (Jan 2021) banned import of waste paper --> Significant rally in Global Pulp Prices

In India

Anti-dumping duty (25%) on uncoated paper helps improve margins for the integrated players.

Anti-dumping duty (25%) on uncoated paper helps improve margins for the integrated players.

Growth Triggers for Indian Paper Industry

- Single use plastic ban

- Increase in education spend

- Packaging (more so after pandemic)

FMCG, Pharma, e-com are big drivers

- GDP Growth (co-relation)

- Single use plastic ban

- Increase in education spend

- Packaging (more so after pandemic)

FMCG, Pharma, e-com are big drivers

- GDP Growth (co-relation)

So, which company does @amitndoshi of @carepms is betting on?

J K Paper

Market Cap: Rs. 3800 Cr

Revenue: 2800 Cr

EBIDTA: 560 Cr

Trailing PE: 16

Forward PE: 7.5

J K Paper

Market Cap: Rs. 3800 Cr

Revenue: 2800 Cr

EBIDTA: 560 Cr

Trailing PE: 16

Forward PE: 7.5

J K Paper

- One of the oldest in the business

- Distribution Network: 4000+ dealers pan-India

- present in all 3 segments: coated, uncoated, packaging paper

- Post recent expansion, will be the largest paper manufacturer in India: bigger than ITC

- One of the oldest in the business

- Distribution Network: 4000+ dealers pan-India

- present in all 3 segments: coated, uncoated, packaging paper

- Post recent expansion, will be the largest paper manufacturer in India: bigger than ITC

Operating margins structurally improved

- 100% wood procurement within 200 Km of plant Vs just 25% a few yrs back

- 25% reduction in water consumption per tonne

- 25% increase in wood productivity

- ADD and higher global pulp prices helpsd

- 100% wood procurement within 200 Km of plant Vs just 25% a few yrs back

- 25% reduction in water consumption per tonne

- 25% increase in wood productivity

- ADD and higher global pulp prices helpsd

Financial Strength of J K Paper (last 5 yr analysis)

- Return ratios in double digits

- Avg cash from Ops ~500 Cr

- Op Margins ~25%

- Debtor days < 10 days

- Consistent dividend payout of 15%+

(maintained in covid year as well)

- Buyback of 100 Cr complete

- Return ratios in double digits

- Avg cash from Ops ~500 Cr

- Op Margins ~25%

- Debtor days < 10 days

- Consistent dividend payout of 15%+

(maintained in covid year as well)

- Buyback of 100 Cr complete

Loading suggestions...