🧵What if I tell you that you can get a Free Term Insurance along with your Mutual Fund SIPs? It’s called SIP Insure. This thread is a primer on how it works.

Hit the ‘re-tweet’ & help me educate more investors

#Investing (1/n)

Hit the ‘re-tweet’ & help me educate more investors

#Investing (1/n)

(Q1) Use Case

1) You are not getting a term insurance due to medical conditions

2) Taking additional life cover for free

‘SIP Insure’ is the perfect arrangement for you! In this thread we will take example of PGIM Smart SIP plan to explain the concept (2/n)

1) You are not getting a term insurance due to medical conditions

2) Taking additional life cover for free

‘SIP Insure’ is the perfect arrangement for you! In this thread we will take example of PGIM Smart SIP plan to explain the concept (2/n)

(Q2) What is the product?

When you start an SIP, opt for the optional “SIP Insure” plan. The accumulation through SIP belongs to you (like it normally works) + you get a free term insurance upto 50 lakhs where the cost (premium) is borne by the Mutual Fund company (AMC) (3/n)

When you start an SIP, opt for the optional “SIP Insure” plan. The accumulation through SIP belongs to you (like it normally works) + you get a free term insurance upto 50 lakhs where the cost (premium) is borne by the Mutual Fund company (AMC) (3/n)

- No medical tests required

- No declaration of good health required

- No waiting period for insurance, cover starts from the first SIP (4/n)

- No declaration of good health required

- No waiting period for insurance, cover starts from the first SIP (4/n)

(Q3) How does it work?

SIP works the way it normally does. In case of insurance, the cover is different for different AMCs. Lets discuss PGIM; cover is 20 times of the ‘monthly’ SIP in the first year, 75 times in the second year and 120 times from the 3rd year onward (5/n)

SIP works the way it normally does. In case of insurance, the cover is different for different AMCs. Lets discuss PGIM; cover is 20 times of the ‘monthly’ SIP in the first year, 75 times in the second year and 120 times from the 3rd year onward (5/n)

For a 10,000/monthly SIP

Cover in the first year = 10,000 * 20 = 2,00,000

Cover in the second year = 10,000 * 75 = 7,50,000

Cover in the third year = 10,000 * 120 = 12,00,000

Maximum of 50 lakh per person can be availed per AMC (6/n)

Cover in the first year = 10,000 * 20 = 2,00,000

Cover in the second year = 10,000 * 75 = 7,50,000

Cover in the third year = 10,000 * 120 = 12,00,000

Maximum of 50 lakh per person can be availed per AMC (6/n)

(Q4) Is the term insurance given by the AMC?

No. AMCs buy Group Term plans from an insurance company to provide for the insurance. The premium is borne by the AMC (7/n)

No. AMCs buy Group Term plans from an insurance company to provide for the insurance. The premium is borne by the AMC (7/n)

(Q5) Eligibility criteria?

- Minimum entry age-18

- Maximum entry age-51

- Minimum SIP period-3 years but the insurance cover continues till the time no withdrawals are made or you reach 55 years of age, what ever comes first

- SIP should continue uninterrupted for 3 years (8/n)

- Minimum entry age-18

- Maximum entry age-51

- Minimum SIP period-3 years but the insurance cover continues till the time no withdrawals are made or you reach 55 years of age, what ever comes first

- SIP should continue uninterrupted for 3 years (8/n)

(Q6) Lets look at some examples to clarify the same

(Case 1) Monthly SIP – 50,000, started at age 35 & no death till 55 years

Fund value at 55 assuming 12% return – 4.6 cr

Insurance Cover = Zero

Total receivable = 4.6 cr (9/n)

(Case 1) Monthly SIP – 50,000, started at age 35 & no death till 55 years

Fund value at 55 assuming 12% return – 4.6 cr

Insurance Cover = Zero

Total receivable = 4.6 cr (9/n)

(Case 2)

Monthly SIP – 50,000, started at age 35 & 'death' at 50 years

Fund value at 50 assuming 12% return – 2.38 cr

Insurance Cover = 50,000 * 120 (times third year SIP) = 60 lakhs but maximum is 50 lakhs

Total receivable = 2.38 + 0.50 = 2.88 cr (10/n)

Monthly SIP – 50,000, started at age 35 & 'death' at 50 years

Fund value at 50 assuming 12% return – 2.38 cr

Insurance Cover = 50,000 * 120 (times third year SIP) = 60 lakhs but maximum is 50 lakhs

Total receivable = 2.38 + 0.50 = 2.88 cr (10/n)

(Case 3)

Monthly SIP – 50,000, started at age 35 & 'death' at 50 years & SIP discontinued ‘after’ 3 years

Fund value at 50 assuming 12% return – 2.38 cr

Insurance Cover = 50 lakhs (same like case 2)

Total receivable = 2.38 + 0.50 = 2.88 cr (11/n)

Monthly SIP – 50,000, started at age 35 & 'death' at 50 years & SIP discontinued ‘after’ 3 years

Fund value at 50 assuming 12% return – 2.38 cr

Insurance Cover = 50 lakhs (same like case 2)

Total receivable = 2.38 + 0.50 = 2.88 cr (11/n)

(Case 4)

Monthly SIP – 50,000, started at age 35 & death at 50 years but SIP discontinued ‘before’ 3 years

Fund value at 50 assuming 12% return – 2.38 cr

Insurance Cover=0

Total receivable=2.38 cr

The Insurance amount is paid by the insurance company directly to the nominee

Monthly SIP – 50,000, started at age 35 & death at 50 years but SIP discontinued ‘before’ 3 years

Fund value at 50 assuming 12% return – 2.38 cr

Insurance Cover=0

Total receivable=2.38 cr

The Insurance amount is paid by the insurance company directly to the nominee

(Q7) Which AMCs offer this service?

ABSL, ICICI, Nippon were initially offering it but today only Nippon & PGIM offer it. Please add if I have missed any other AMC offering it :) (13/n)

ABSL, ICICI, Nippon were initially offering it but today only Nippon & PGIM offer it. Please add if I have missed any other AMC offering it :) (13/n)

(Q8) What is the difference between the PGIM smart SIP explained in the thread above & Nippon’s SIP Insure?

(a) Nippon offers cover of 10 times of the monthly SIP in the first year (PGIM 20X), 50 times in the second year (PGIM 75X) and 120 times in the 3rd year (14/n)

(a) Nippon offers cover of 10 times of the monthly SIP in the first year (PGIM 20X), 50 times in the second year (PGIM 75X) and 120 times in the 3rd year (14/n)

(b) Declaration of good health is required in Nippon (Not required in PGIM)

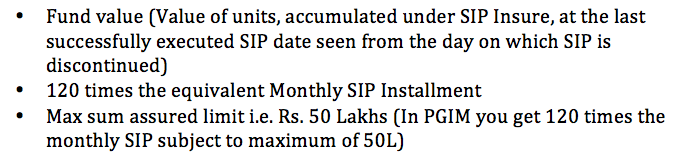

(c) In Nippon, if you have registered SIP for more than 3 years and you discontinued the SIP after 3 years, the sum insured will be lower of below 3 👇 (15/n)

(c) In Nippon, if you have registered SIP for more than 3 years and you discontinued the SIP after 3 years, the sum insured will be lower of below 3 👇 (15/n)

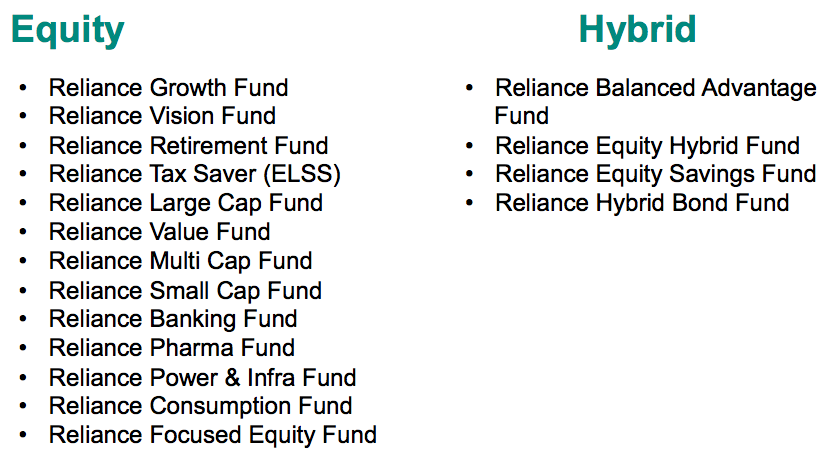

(Q9) On which schemes can I avail this service?

(a) PGIM – All schemes except small cap, arbitrage & debt schemes

(b) Nippon – attached (16/n)

(a) PGIM – All schemes except small cap, arbitrage & debt schemes

(b) Nippon – attached (16/n)

(Q10) What if I have an existing SIP running in the eligible schemes?

There is an option to add this feature in your existing SIPs as well provided your residual tenure was 3 years or more as on Dec 17th 2018, reach the fund house (17/n)

There is an option to add this feature in your existing SIPs as well provided your residual tenure was 3 years or more as on Dec 17th 2018, reach the fund house (17/n)

(Q 11) Can I do SIPs with both, Nippon & PGIM and increase my cover?

Yes, you can, but at each AMC level sum insured cannot be more than 50 lakhs ☺

(Q 12) Risk if any?

Discontinuation due to regulatory requirement. (18/n)

Yes, you can, but at each AMC level sum insured cannot be more than 50 lakhs ☺

(Q 12) Risk if any?

Discontinuation due to regulatory requirement. (18/n)

(Q13) Disadvantage, if any?

The only disadvantage I see is having to invest in a limited set of schemes offered by Nippon & PGIM to avail this benefit. Don’t compromise on scheme selection to avail the insurance unless you get denied term insurance for medical reasons (19/n)

The only disadvantage I see is having to invest in a limited set of schemes offered by Nippon & PGIM to avail this benefit. Don’t compromise on scheme selection to avail the insurance unless you get denied term insurance for medical reasons (19/n)

Other things 2 know

- Only for Indian citizens

- In case of Joint holding, the first holder in the folio is insured

- This life cover should not be your primary life cover

- Please do read the detailed addendum on the AMCs website before investing (20/n)

- Only for Indian citizens

- In case of Joint holding, the first holder in the folio is insured

- This life cover should not be your primary life cover

- Please do read the detailed addendum on the AMCs website before investing (20/n)

This is my 39th thread, 'do re-tweet'

Have earlier written on,

-Sector Analysis - Banking, Paints, Logistic, REIT, InvIT, Sugar, Steel

- Macro

- Debt Markets

- Equity

- Gold

- Personal Finance etc.

You can find them all in the link below (END)

Have earlier written on,

-Sector Analysis - Banking, Paints, Logistic, REIT, InvIT, Sugar, Steel

- Macro

- Debt Markets

- Equity

- Gold

- Personal Finance etc.

You can find them all in the link below (END)

Fund value will not be 2.38 cr. as the SIP is discontinued. The objective was to show that you will get what ever the fund value is + insurance.

Fund value will not be 2.38 cr. as the SIP is discontinued. The objective was to show that you will get what ever is the fund value.

Loading suggestions...