1/

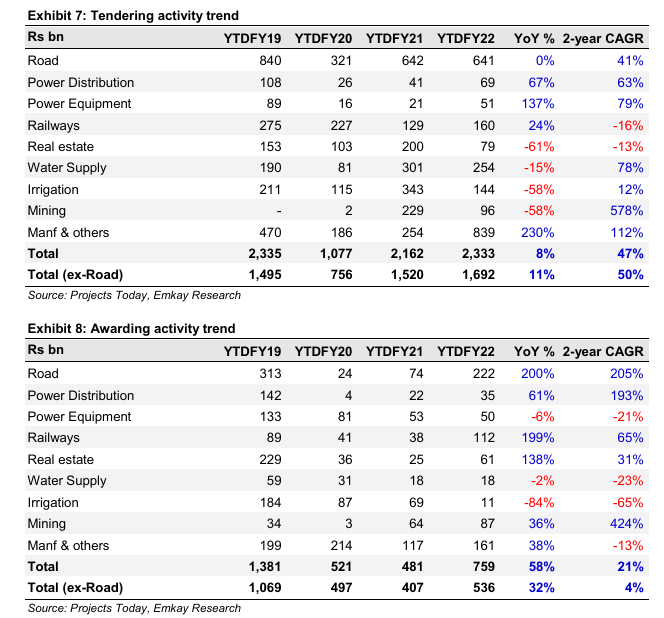

🏗️ Infrastructure new order tendering (opening for bid) and awarding (selection of EPC) has been very strong in the last few months.

🛣️ Driven by Roads (up 3x), Power Distribution (up 3x), Railways (up 65%) and RE (up 31%). Water and Irrigation orderbook yet to pickup.

🏗️ Infrastructure new order tendering (opening for bid) and awarding (selection of EPC) has been very strong in the last few months.

🛣️ Driven by Roads (up 3x), Power Distribution (up 3x), Railways (up 65%) and RE (up 31%). Water and Irrigation orderbook yet to pickup.

2/

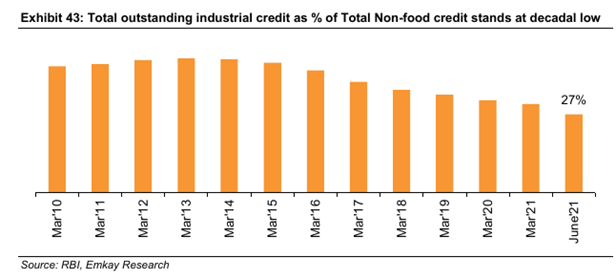

Total outstanding Industrial Credit as % of non-food credit is at decadal lows...

Total outstanding Industrial Credit as % of non-food credit is at decadal lows...

3/

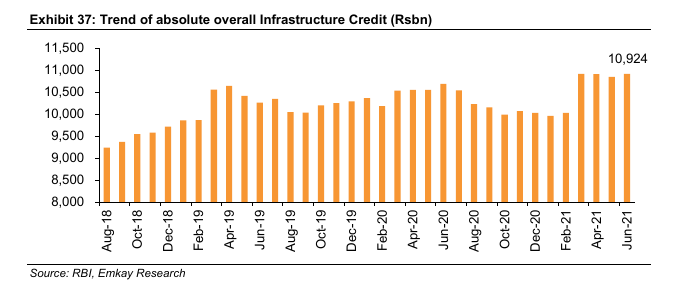

However, Infrastructure financing by lenders is seen picking up in recent months.

However, Infrastructure financing by lenders is seen picking up in recent months.

4/

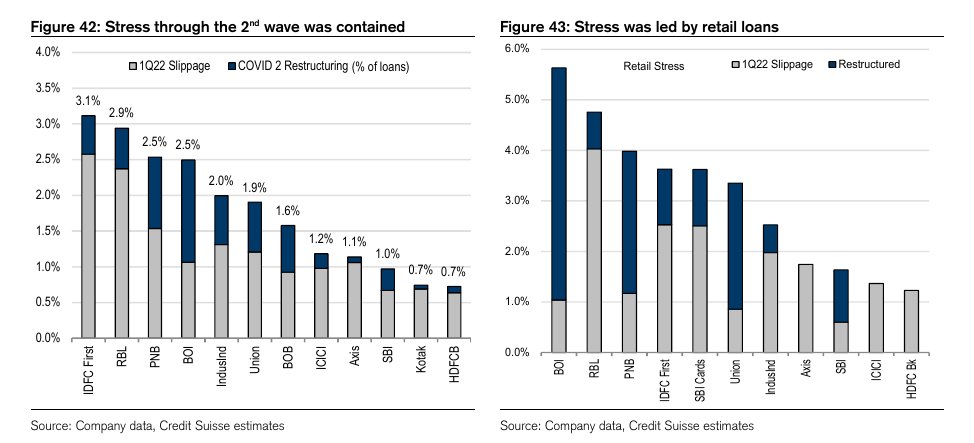

While overall Banking stress is under control, Retail loan book is under pressure. Given absence of moratorium unlike in 2020, there is continued pressure from restructured assets & is expected to continue over the next few quarters.

While overall Banking stress is under control, Retail loan book is under pressure. Given absence of moratorium unlike in 2020, there is continued pressure from restructured assets & is expected to continue over the next few quarters.

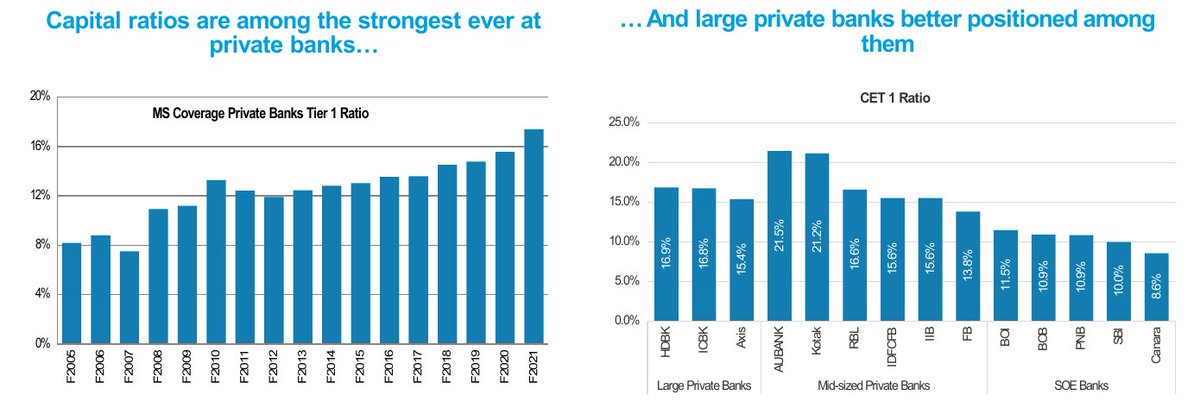

5/

But Capital adequacy ratios of Tier 1 Banks is the strongest ever after recent fund raises. With Credit growth being subdued in the recent few years, one can expect a fresh cycle of Industrial and Infrastructure Credit.

But Capital adequacy ratios of Tier 1 Banks is the strongest ever after recent fund raises. With Credit growth being subdued in the recent few years, one can expect a fresh cycle of Industrial and Infrastructure Credit.

6/

Strong order book, stable balance sheet, clearance of stuck orders and conducive financing ecosystem makes a good case for growth of Infra EPC companies.

Strong order book, stable balance sheet, clearance of stuck orders and conducive financing ecosystem makes a good case for growth of Infra EPC companies.

Loading suggestions...