DeFi 30-for-30 #4:

Lending & Borrowing Protocols

Putting the "Finance" in DeFi

Thread 👇

Lending & Borrowing Protocols

Putting the "Finance" in DeFi

Thread 👇

1/ What are lending and borrowing protocols in DeFi?

These are Dapps that function like TradFi institutions (e.g. banks) but they use smart contracts.

User provide funds (also called "supplying liquidity") and earn interest on them.

Borrowers pay to borrow.

Simple concept.

These are Dapps that function like TradFi institutions (e.g. banks) but they use smart contracts.

User provide funds (also called "supplying liquidity") and earn interest on them.

Borrowers pay to borrow.

Simple concept.

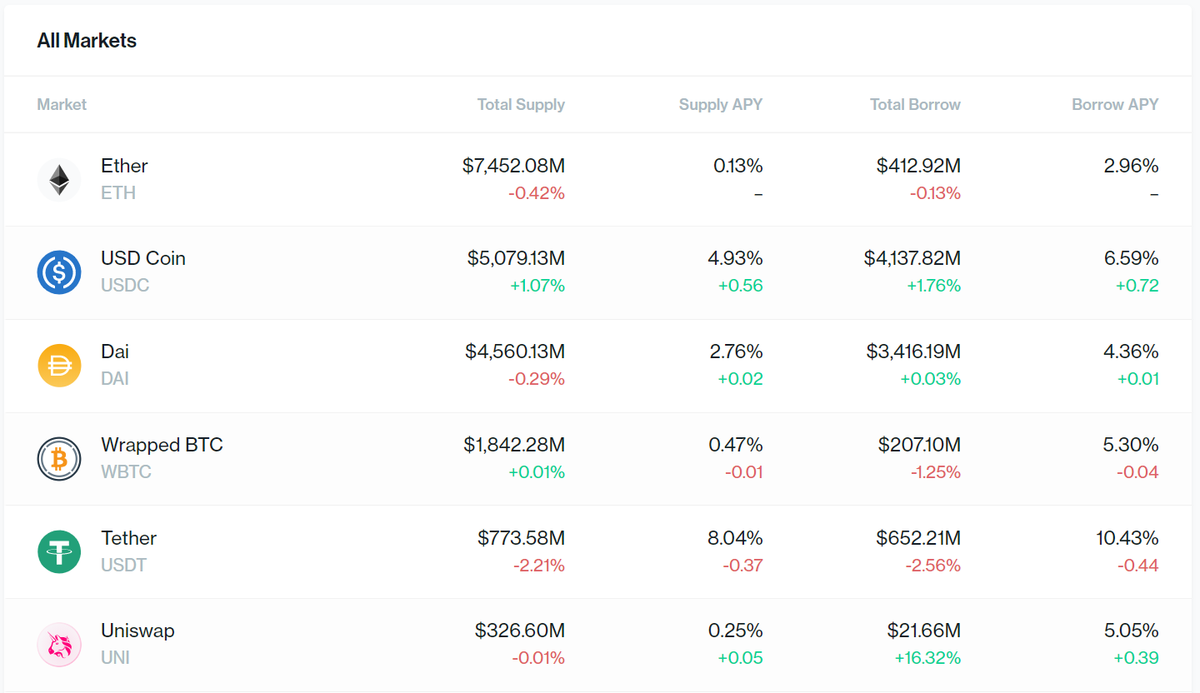

2/ For e.g, when you go to Compound Finance, you see a table as such.

If you supply liquidity, you earn the supply APY; vice versa for borrowing rates.

What's different in DeFi is the leverage.

If you supply liquidity, you earn the supply APY; vice versa for borrowing rates.

What's different in DeFi is the leverage.

3/ How are the interest rates decided?

They are algorithmically set by the protocol, depending on various factors including the supply and demand.

The higher the demand for borrowing an asset, the higher the APY to draw more depositors to supply that particular asset.

They are algorithmically set by the protocol, depending on various factors including the supply and demand.

The higher the demand for borrowing an asset, the higher the APY to draw more depositors to supply that particular asset.

4/ In traditional finance, you go to a bank and apply for loans.

The bank checks your eligibility including your credit history, DSR and a plethora of data they have on you to conclude if you're a credit-worthy person.

The bank checks your eligibility including your credit history, DSR and a plethora of data they have on you to conclude if you're a credit-worthy person.

5/ Say you wanna buy a house. If you pass the above criteria, the bank loans you the money. You pay back loan + interest over time.

During that time, your house is the collateral which the bank can seize and auction off should you fail to pay.

During that time, your house is the collateral which the bank can seize and auction off should you fail to pay.

6/ In DeFi, you need a collateral that you stake, against which you can borrow against.

Your borrowing limit depends on the protocol, but it's commonly accepted that you cannot borrow more than 50% (or any other <100% percentage) of the value that you stake.

Your borrowing limit depends on the protocol, but it's commonly accepted that you cannot borrow more than 50% (or any other <100% percentage) of the value that you stake.

7/ What's different is the flexibility. You can supply 1000 USDC, and borrow 500USDC worth of any token and the contract doesn't care.

All of it is coded into the protocol. Lending and borrowing becomes efficient, instantaneous and frictionless (if you ignore the gas fees)

All of it is coded into the protocol. Lending and borrowing becomes efficient, instantaneous and frictionless (if you ignore the gas fees)

8/ As your asset fluctuates in value, liquidation events might happen. If the asset that you deposit falls in value, your loan-to-value ratio rises above 50%, triggering a liquidation event.

Liquidation means you lose what you supplied as collateral, plus penalties.

Liquidation means you lose what you supplied as collateral, plus penalties.

9/ DeFi protocols then becomes a huge money lego playground as you can borrow low and stake high, or borrow against your asset for some short term trading or speculation.

The risks are high, so it's not for beginners as crypto prices are very volatile and you could lose it all.

The risks are high, so it's not for beginners as crypto prices are very volatile and you could lose it all.

10/ But there will never be a risk to the system as a whole as you cannot leverage beyond what you own. For every lending, there must always be an overcollateralised asset.

This represents a fundamental shift away from the fractional reserve banking system we have today.

This represents a fundamental shift away from the fractional reserve banking system we have today.

11/ How is it different?

If the reserve ratio is set at 2% (Malaysia's current rate) - for every 100mil a bank owns, only 2mil is required to be backed by real deposits from customers.

Yet the bank can loan out that full 100mil and earn interest from it. Free money yeehaw!

If the reserve ratio is set at 2% (Malaysia's current rate) - for every 100mil a bank owns, only 2mil is required to be backed by real deposits from customers.

Yet the bank can loan out that full 100mil and earn interest from it. Free money yeehaw!

12/ In DeFi, there is no such fractional reserve. Every asset you borrow are backed by assets deposited from other participants in the ecosystem.

So there is no possibility of a "bank run", collapsing the protocol if depositors panic and withdraw all their assets.

So there is no possibility of a "bank run", collapsing the protocol if depositors panic and withdraw all their assets.

TL;DR:

On DeFi, you can supply and borrow assets from protocols with fixed or variable interest rates.

On DeFi, you can supply and borrow assets from protocols with fixed or variable interest rates.

As crypto progresses rapidly, it's not possible to provide in-depth guide to any of the lending and borrowing protocols on all the different chains in one thread.

That's a project for another time.

That's a project for another time.

Loading suggestions...