Indian apparel exports have largely remained range

bound over FY14-20.

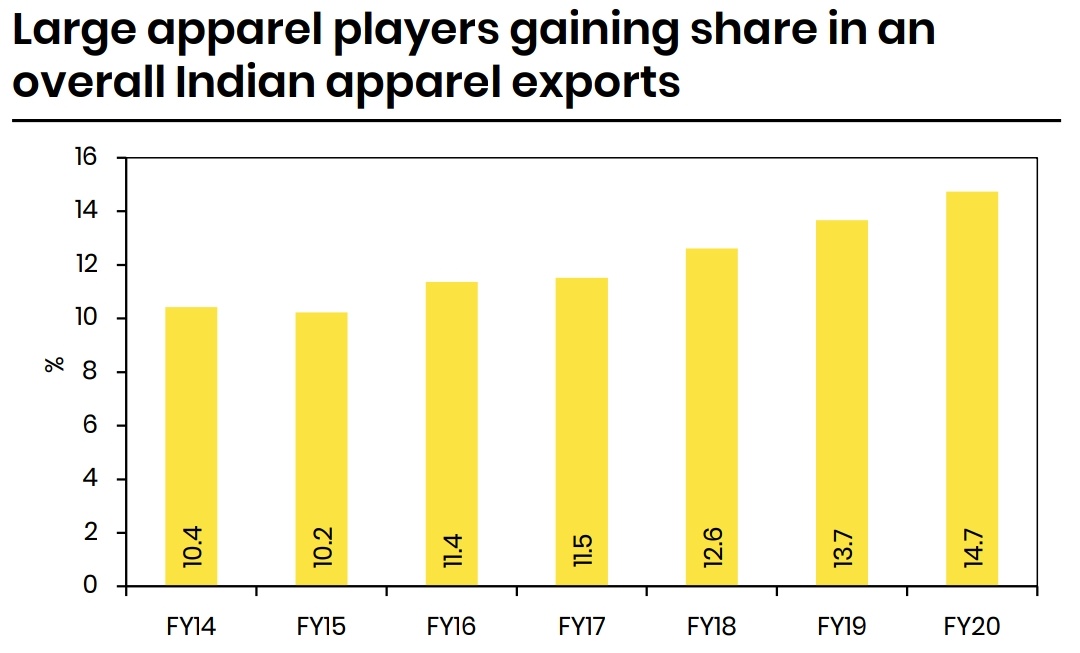

However, market share of large

apparel players in the overall Indian apparel exports

increased from 10.4% in FY14 to 14.7% in FY20.

bound over FY14-20.

However, market share of large

apparel players in the overall Indian apparel exports

increased from 10.4% in FY14 to 14.7% in FY20.

Indian apparel

players are in a sweet spot to seize the opportunities

prevailing in the global market (alternative sourcing &

ban on Xinjiang products) along with govt’s focus

on reviving exports.

Apparel players

investing in capacities are likely to gain going

forward.

players are in a sweet spot to seize the opportunities

prevailing in the global market (alternative sourcing &

ban on Xinjiang products) along with govt’s focus

on reviving exports.

Apparel players

investing in capacities are likely to gain going

forward.

KPRMILL is a fully vertically integrated player with focus on Yarn, Fabrics, Garments & Sugar/Ethanol.

Majority of yarn (1/3rd) & fabric (~50%) are captively consumed to

manufacture downstream products enabling better control on supply chain

& generate sustainable margins.

Majority of yarn (1/3rd) & fabric (~50%) are captively consumed to

manufacture downstream products enabling better control on supply chain

& generate sustainable margins.

Its sugar plant is also vertically

integrated to produce ethanol from captive crushed cane.

Vertically integrated textile players with stronger quality control mechanisms and

adherence to delivery timelines place KPRMILL in a favourable position.

integrated to produce ethanol from captive crushed cane.

Vertically integrated textile players with stronger quality control mechanisms and

adherence to delivery timelines place KPRMILL in a favourable position.

KPR’s garment

export order book has expanded by ~10-15% higher than pre-Covid level.

Further,

revenue from garmenting division is expected to increase going forward due to

the company’s capacity expansion plans and focus on value addition.

export order book has expanded by ~10-15% higher than pre-Covid level.

Further,

revenue from garmenting division is expected to increase going forward due to

the company’s capacity expansion plans and focus on value addition.

KPRMILL is self-sufficient in power through green energy with a

total wind power capacity of 62 MW and sugar co-gen capacity of 40 MW.

Due to these, in-house power generation

facilities, its power cost is lowest in the industry at ~3.8% (of sales) in FY20.

total wind power capacity of 62 MW and sugar co-gen capacity of 40 MW.

Due to these, in-house power generation

facilities, its power cost is lowest in the industry at ~3.8% (of sales) in FY20.

Despite completion of ethanol capex & expansion of spinning capacities in FY20, the company

has net debt-to-equity of 0.1x in FY21.

Even after completion of its largest capex

worth 750Cr in FY22, KPRMILL can have the strongest balance sheet and can generate massive FCF.

has net debt-to-equity of 0.1x in FY21.

Even after completion of its largest capex

worth 750Cr in FY22, KPRMILL can have the strongest balance sheet and can generate massive FCF.

Sugar business was set up to ensure availability of power for the

textiles business.

With improving demand-supply dynamics of ethanol business coupled with government thrust on

ethanol blending in fuel programme, the company started investing in this segment from FY20.

textiles business.

With improving demand-supply dynamics of ethanol business coupled with government thrust on

ethanol blending in fuel programme, the company started investing in this segment from FY20.

Revenue share of sugar-

cum-ethanol segment is likely to increase from 7.4% in FY19 to 22.8% in FY23E and ~50% of total segment revenue will be

contributed by high margin ethanol business. This will also reduce cyclicality in the sugar business.

cum-ethanol segment is likely to increase from 7.4% in FY19 to 22.8% in FY23E and ~50% of total segment revenue will be

contributed by high margin ethanol business. This will also reduce cyclicality in the sugar business.

Loading suggestions...