Claim: Free cash flow compounding justifies owning companies trading at optically high valuations.

Let us analyse the compounding (past & future) by taking an example of 1 💎 in the dust.

Read on if you are curious about the valuations of cos like Asian Paints, Pidilite, Nestle

Let us analyse the compounding (past & future) by taking an example of 1 💎 in the dust.

Read on if you are curious about the valuations of cos like Asian Paints, Pidilite, Nestle

First of all, I must say I have deep respect for dominant franchises like asian paints, Nestle who have managed to capture > 40% market share in a large diverse country like India. The businesses are absolutely great.

Claim 1: Free cash flow (FCF) compounding has been 20-25% in the past.

Facts about claim 1: Free cash flow CAGR has reflected profit & Cash flow from operations (CFO) CAGR in any rolling 10 year period.

Facts about claim 1: Free cash flow CAGR has reflected profit & Cash flow from operations (CFO) CAGR in any rolling 10 year period.

Claim 2: 80 p/e or 100 p/e is only optically expensive because Free cash flow will compound at 20-25% for next 25 years.

Facts about claim 2: This has not happened in the past (data from 2004-2021). Free cash flow as % of profits has been largely stable ~50%, mildly grown to 66% in FY21 as capex has gone down.

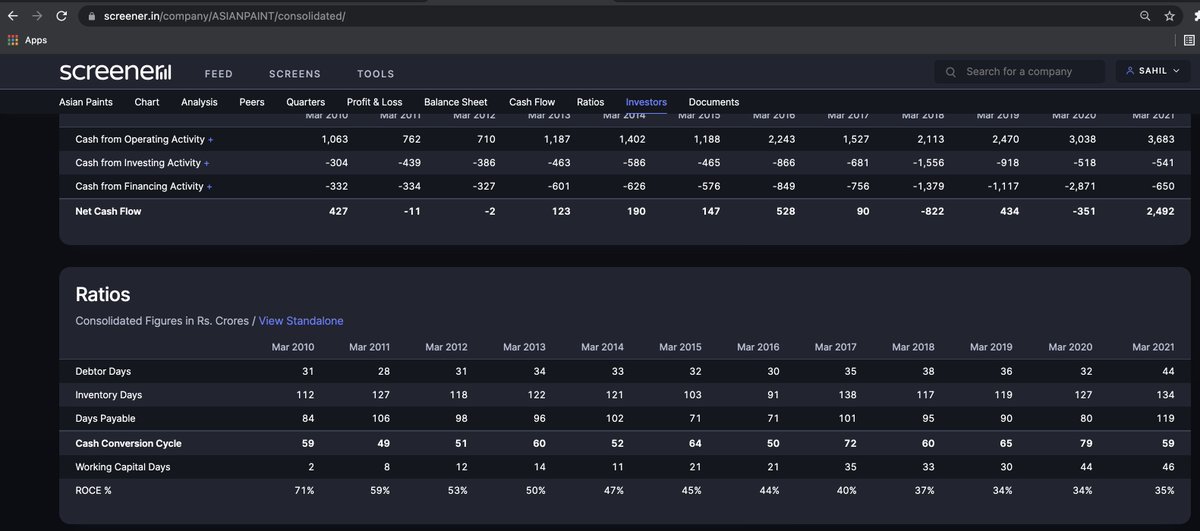

Claim 3: Dominant & improving working capital position which led to free cash flow growth.

Facts about claim 3: That is not the case. In fact, both working capital & ROCE have been deteriorating in last 10 years.

Facts about claim 3: That is not the case. In fact, both working capital & ROCE have been deteriorating in last 10 years.

My conclusion: They would find it difficult to grow profits, or free cash flows at > 15% CAGR. Even if FCF grows faster than profits, that would be by sacrificing capex which sacrifices future growth.

A quick reverse DCF will tell us that the embedded growth rate expectations (30% CAGR) are unsustainable. Courtesy @Tijori1

<end of thread>

<end of thread>

Ps: I forgot to add explicitly that all the data and the example I have taken is of Asian paints.

Loading suggestions...