Yet another thread on Shannon's Demon

moontowermeta.com

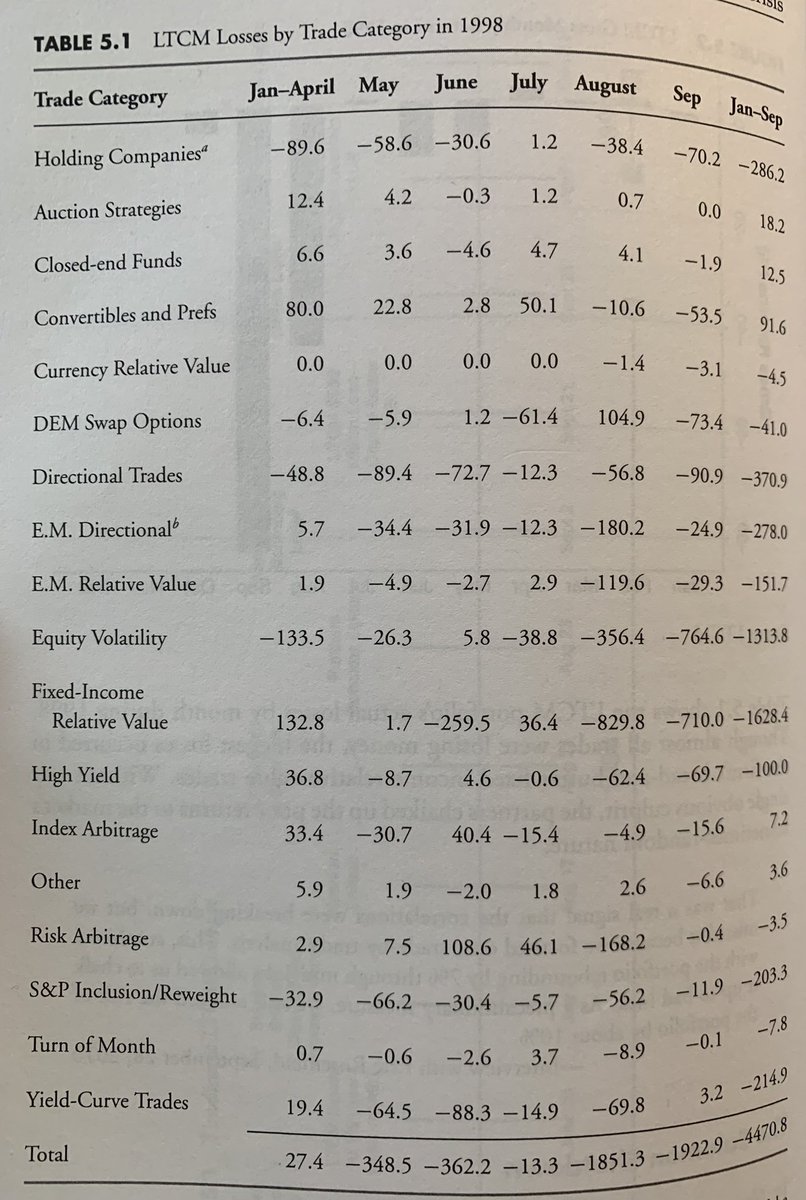

LTCM volatility, correlations, and losses. (From the book The Crisis of Crowding)

Recent Threads

wont tag because its a nothingburger. i think richy really hates himself more than anything else in the world and struggles with friendship because of...

🇧🇦 Bosnia have released an official World Cup song and it's an absolute BANGER. 💙💛 🎵 "I AM FROM BOSNIA, TAKE ME TO AMERICA." https://t.co/yKZs5r7vBw

New in Claude Code (research preview): dynamic workflows. Claude writes an orchestration script on the fly, then spins up a large fleet of coordinate...

What if you could take three completely different model families… and distill them into one tiny model? 🤯 📜 Paper: https://t.co/K2iKD4xFvp MOPD (Mul...

🇺🇸💥🇮🇱 Congress Just Voted to Fuse the U.S. Military With Israel’s — and Buried It on Page 847 So You Wouldn’t Notice ☠️ Section 224 of the $1.15 Tril...

Police running down harassing this guy over a post on Facebook about protesting Data Centers. https://t.co/mfqEKnGwld

Popular Threads

Please retweet and share if you support my and others' vaccine injury recoveries. https://t.co/y8xNWwRUOO

A thread: Pakistani newspaper Dawn's front pages from 4th december 1971 to 20 December to see how they kept their own people in the dark. This was on...

Top 20 Players with the most goals + assists in football history, only players with assists available (following the Opta criteria for assists) Seaso...

Ware County, Ga has broken the Dominion algorithm: Using sequestered Dominion Equipment, Ware County ran a equal number of Trump votes and Biden vote...

ICT’s 2022 Mentorship Summarized: https://t.co/zFJCgIfDAR

The ICT Mentorship Core Content Month 1 Summarized: https://t.co/6tXJxPMDhm