Is Piramal Pharma a special situation play? Scenarios & Valuations.

A Thread 🧵👇

A Thread 🧵👇

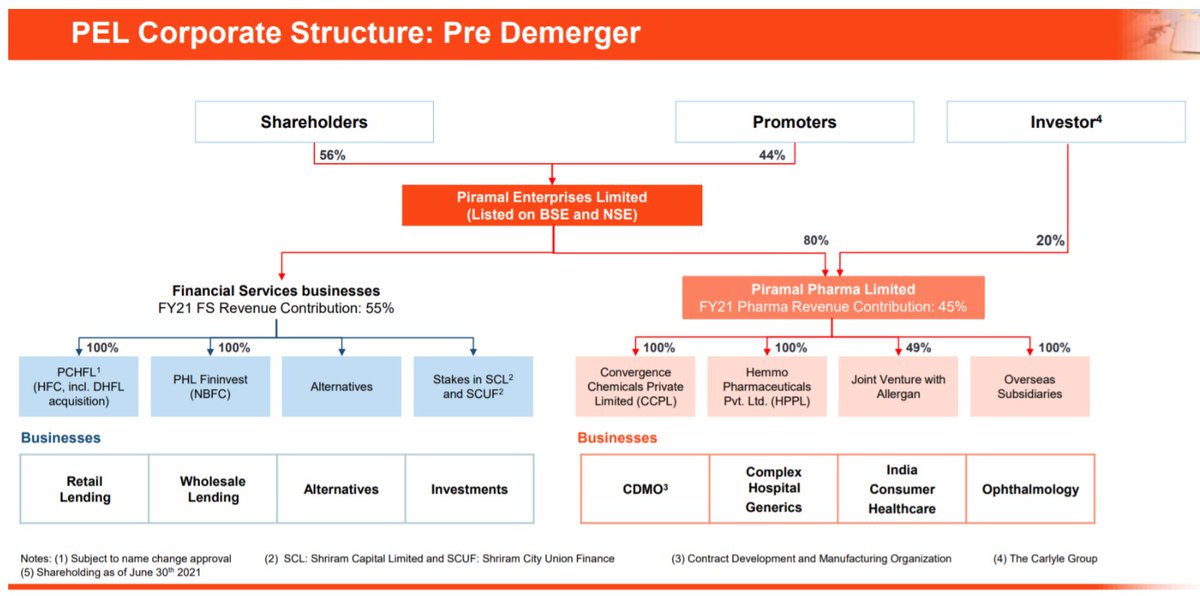

1/ Piramal Pharma is the soon-to-be demerged vertical of Piramal Enterprises: 4 shares of Piramal Pharma for 1 share of the listed entity

2/ Current Mcap of the group (listed Piramal Enterprises): 65Kcrs

which encompasses the financial services entity & 80% of the Pharma business (Sold 20% to Carlyle in Oct 2020)

So, One needs to value the pharmaceutical business accordingly.

which encompasses the financial services entity & 80% of the Pharma business (Sold 20% to Carlyle in Oct 2020)

So, One needs to value the pharmaceutical business accordingly.

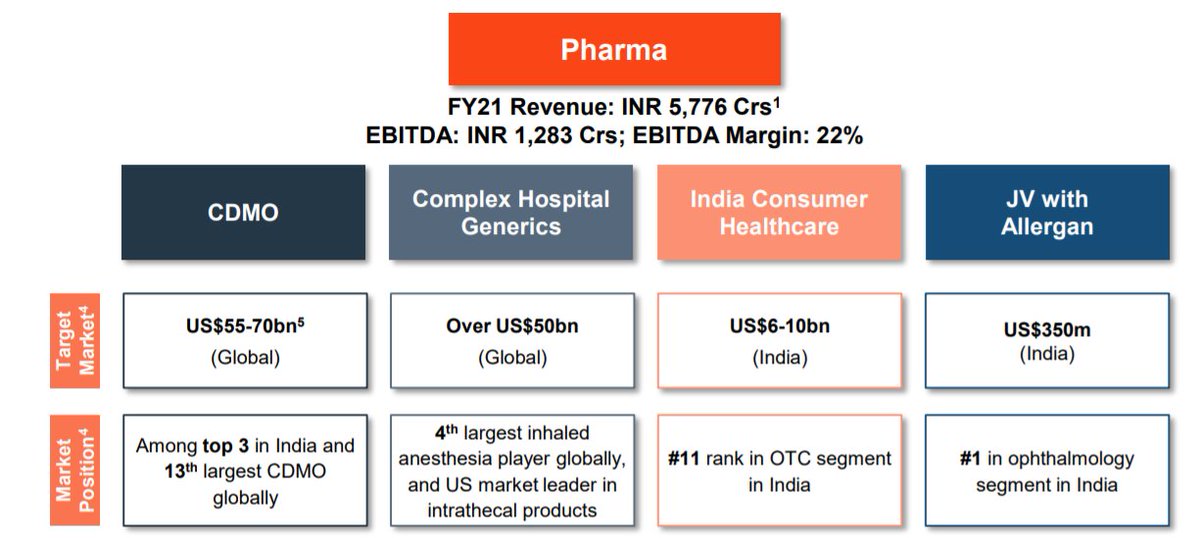

3/ Piramal Pharma's TTM Rev: 6K crs

CDMO: 3.7K crs

Complex Hospital Generics: 1.8K crs

Indian Consumer Healthcare: 0.6K crs

JV with Allergen: 0.4K crs (49% stake)

TTM EBITDA of Piramal Pharma: 1.3K crs

CDMO: 3.7K crs

Complex Hospital Generics: 1.8K crs

Indian Consumer Healthcare: 0.6K crs

JV with Allergen: 0.4K crs (49% stake)

TTM EBITDA of Piramal Pharma: 1.3K crs

4/ At the time of the demerger:

Pharma business is projected to have an equity of 6.8-7K crs at the time of the merger with 3-3.2Kcrs of debt.

That leaves the financial services business at 29-30K crores of equity (book value of the business)

Pharma business is projected to have an equity of 6.8-7K crs at the time of the merger with 3-3.2Kcrs of debt.

That leaves the financial services business at 29-30K crores of equity (book value of the business)

5/ Scenario 1:

If I take in a Price to book of 0.75x for Financial services (expecting more stress from DHFL book)

Value of 80% of Piramal Pharma at 42.5K crores - Total Mcap of 53K crores & EV of 56K crores

Valuations:

EV/EBITDA- 43x

EV/Sales- 9.3x

If I take in a Price to book of 0.75x for Financial services (expecting more stress from DHFL book)

Value of 80% of Piramal Pharma at 42.5K crores - Total Mcap of 53K crores & EV of 56K crores

Valuations:

EV/EBITDA- 43x

EV/Sales- 9.3x

6/ Scenario 2:

If I take in a Price to book of 1x for Financial services

Value of 80% of Piramal Pharma at 35K crores - Total Mcap of 44K crores & EV of 47K crores

Valuations:

EV/EBITDA- 36x

EV/Sales- 7.7x

If I take in a Price to book of 1x for Financial services

Value of 80% of Piramal Pharma at 35K crores - Total Mcap of 44K crores & EV of 47K crores

Valuations:

EV/EBITDA- 36x

EV/Sales- 7.7x

7/ Scenario 3:

If I take in a Price to book of 1.5x for Financial services

Value of 80% of Piramal Pharma at 20K crores - Total Mcap of 25K crores & EV of 28K crores

Valuations:

EV/EBITDA- 21.5x

EV/Sales- 4.7x

If I take in a Price to book of 1.5x for Financial services

Value of 80% of Piramal Pharma at 20K crores - Total Mcap of 25K crores & EV of 28K crores

Valuations:

EV/EBITDA- 21.5x

EV/Sales- 4.7x

8/ Scenario 4:

If I take in a Price to book of 2x for Financial services (Bull market & credit upcycle)

Value of 80% of Piramal Pharma at 5K crores - Total Mcap of 6.3K crores & EV of 9.5K crores

Valuations:

EV/EBITDA- 7.3x

EV/Sales- 1.6x

If I take in a Price to book of 2x for Financial services (Bull market & credit upcycle)

Value of 80% of Piramal Pharma at 5K crores - Total Mcap of 6.3K crores & EV of 9.5K crores

Valuations:

EV/EBITDA- 7.3x

EV/Sales- 1.6x

9/ What valuation is comfortable?

As per its high entry barrier business segments, we have observed that similar global assets trade anywhere b/w 15-20x EBITDA

Note that they sold 20% of the business to Carlyle at less than 4x EV/Sales & 20x EV/EBITDA.

As per its high entry barrier business segments, we have observed that similar global assets trade anywhere b/w 15-20x EBITDA

Note that they sold 20% of the business to Carlyle at less than 4x EV/Sales & 20x EV/EBITDA.

10/ Their Financial services biz has gone through a major downturn since IL&FS, so we stand to see how swiftly are they able to convert the wholesale business to retail in the upcoming years.

The Scenario (1-4) that will play out is dependent on management's execution.

The Scenario (1-4) that will play out is dependent on management's execution.

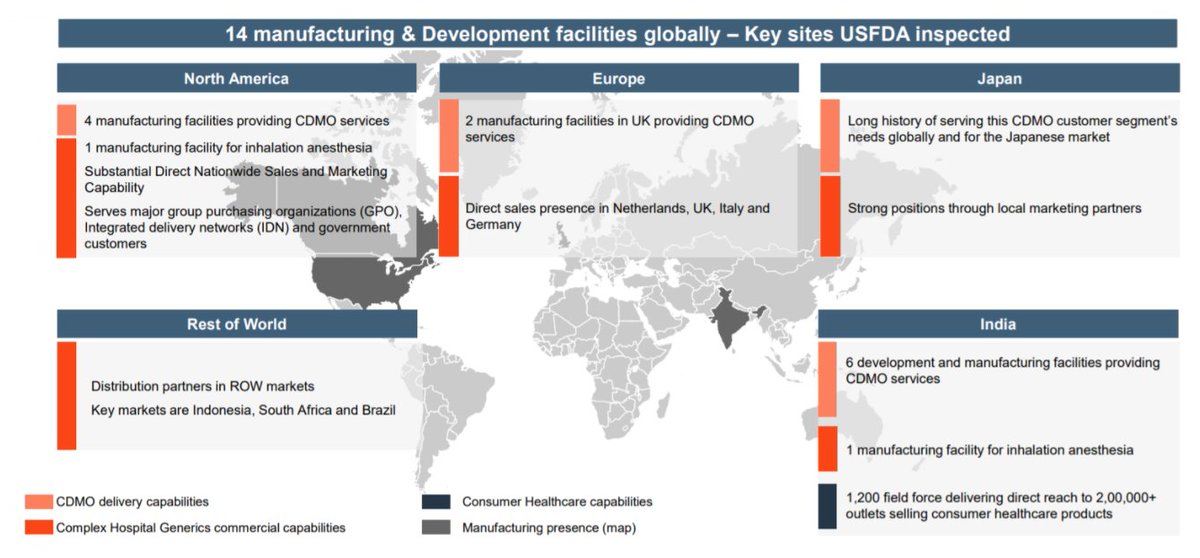

11/ Positive business optionalities for Piramal Pharma

CDMO: 3x increase in phase III molecules from 10 in FY17 to 30 in FY21 & Significant growth in commercial products under patent from 11 in FY19 to 19 in FY21 with 500+ customers

The potential scale-up 💥👇

CDMO: 3x increase in phase III molecules from 10 in FY17 to 30 in FY21 & Significant growth in commercial products under patent from 11 in FY19 to 19 in FY21 with 500+ customers

The potential scale-up 💥👇

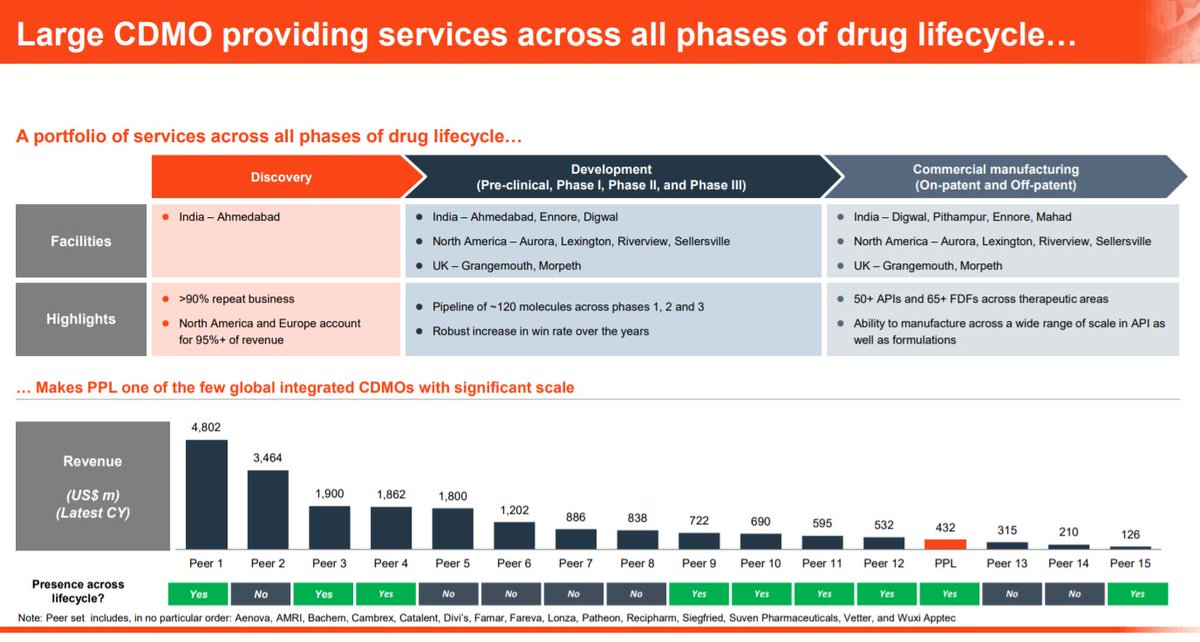

12/ Expertise in niche, complex, and high margin areas like HPAPI, ADCs, sterile injectables, hormones & peptide API

13th largest CDMO in the world & present across all phases of the drug lifecycle (for example, even Syngene isn't till now, it is trying to enter manufacturing)

13th largest CDMO in the world & present across all phases of the drug lifecycle (for example, even Syngene isn't till now, it is trying to enter manufacturing)

13/ Complex Hospital generics: Strong distribution to 100+ countries & 5,500+ hospitals in the US which will be capitalized with new launches (pipeline of 30+ products)

Similarly with the OTC portfolio where they are present in 250,000+ outlets in 🇮🇳

Similarly with the OTC portfolio where they are present in 250,000+ outlets in 🇮🇳

14/ Potential Re-entry into Domestic Formulations (Had sold their Indian formulations business for $3.7B to Abbott in 2010)

The clause that stopped them from entering has expired this year & they are actively looking for acquisitions in the space.

The clause that stopped them from entering has expired this year & they are actively looking for acquisitions in the space.

15/ Risks:

- Net debt to EBITDA of 2x: Lower the better

- Acquisitions focused strategy: can back-fire once in a while: Made 15 acquisitions over the last 10 years for which they have paid over 4000crs; 3 just in FY21.

- No Biologics capability investment till now.

- Net debt to EBITDA of 2x: Lower the better

- Acquisitions focused strategy: can back-fire once in a while: Made 15 acquisitions over the last 10 years for which they have paid over 4000crs; 3 just in FY21.

- No Biologics capability investment till now.

16/

- Adverse action from regulators (USFDA, MHRA, etc): At this point, 200+ Regulatory Inspections with no OAI

- High Capex: Major capacities are outside India, which have much lower asset turns (1x) vs Indian ones (2-3x); hurting steady-state ROCEs. | H/T @unseenvalue

- Adverse action from regulators (USFDA, MHRA, etc): At this point, 200+ Regulatory Inspections with no OAI

- High Capex: Major capacities are outside India, which have much lower asset turns (1x) vs Indian ones (2-3x); hurting steady-state ROCEs. | H/T @unseenvalue

17/ Conclusion:

Piramal Pharma as a standalone is a grade-A asset with sticky customers & has the potential to scale up multifold in many years to come, works if one gets in at a reasonable valuation.

The management furthermore has a victorious track record.

End of Thread.

Piramal Pharma as a standalone is a grade-A asset with sticky customers & has the potential to scale up multifold in many years to come, works if one gets in at a reasonable valuation.

The management furthermore has a victorious track record.

End of Thread.

If you found the thread to be of help, please do retweet the 1st tweet 👇 & help us educate more investors.

Loading suggestions...