1/ Thread on @GMX_IO (originally a @Delphi_Digital report)

GMX is a perps and spot exchange on Arbitrum with plans to launch on AVAX in the future.

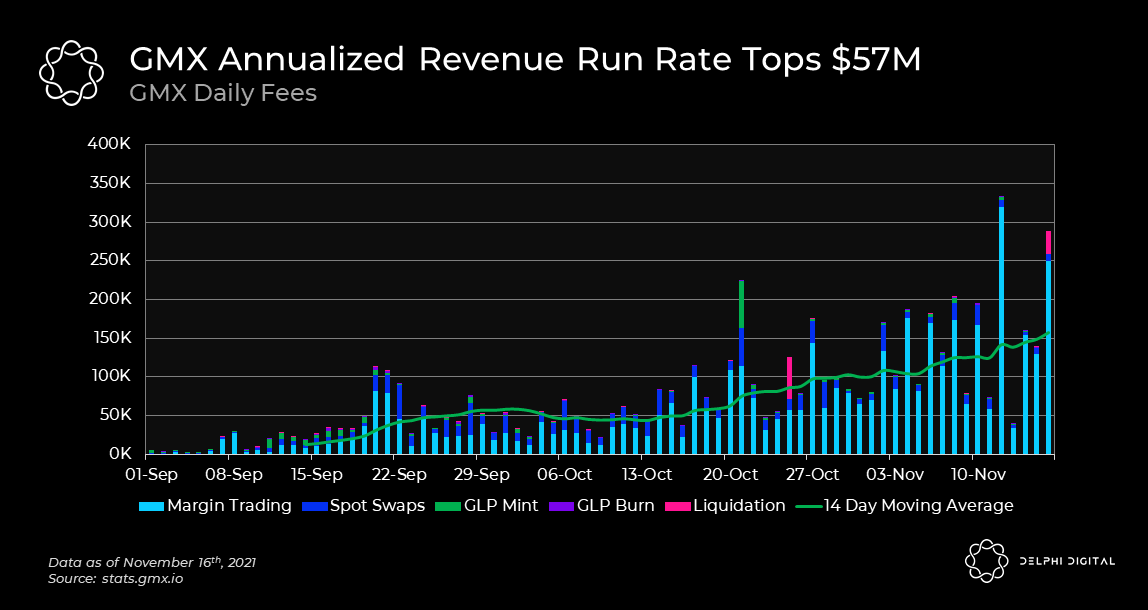

GMX has a revenue run rate of $57.3M per year, 30% of which goes directly to GMX stakers.

Meaning GMX trades at a ~16x P/E ($38)

GMX is a perps and spot exchange on Arbitrum with plans to launch on AVAX in the future.

GMX has a revenue run rate of $57.3M per year, 30% of which goes directly to GMX stakers.

Meaning GMX trades at a ~16x P/E ($38)

2/ GMX uses GLP, a basket of ETH, BTC, LINK, UNI, USDC, USDT, and MIM to facilitate margin trading and swaps on the platform.

Swaps are executed based on pricing from @Chainlink @FTX_Official & @Binance allowing GLP to offer zero slippage swaps and low fees.

Swaps are executed based on pricing from @Chainlink @FTX_Official & @Binance allowing GLP to offer zero slippage swaps and low fees.

3/ Using CEX pricing GLP achieves a “true price” with far less liquidity than AMMs.

This also protects LPs against “impermanent loss” associated with AMMs.

Tradeoffs: Oracle based pricing does not work well with illiquid assets; since traders can avoid market impact.

This also protects LPs against “impermanent loss” associated with AMMs.

Tradeoffs: Oracle based pricing does not work well with illiquid assets; since traders can avoid market impact.

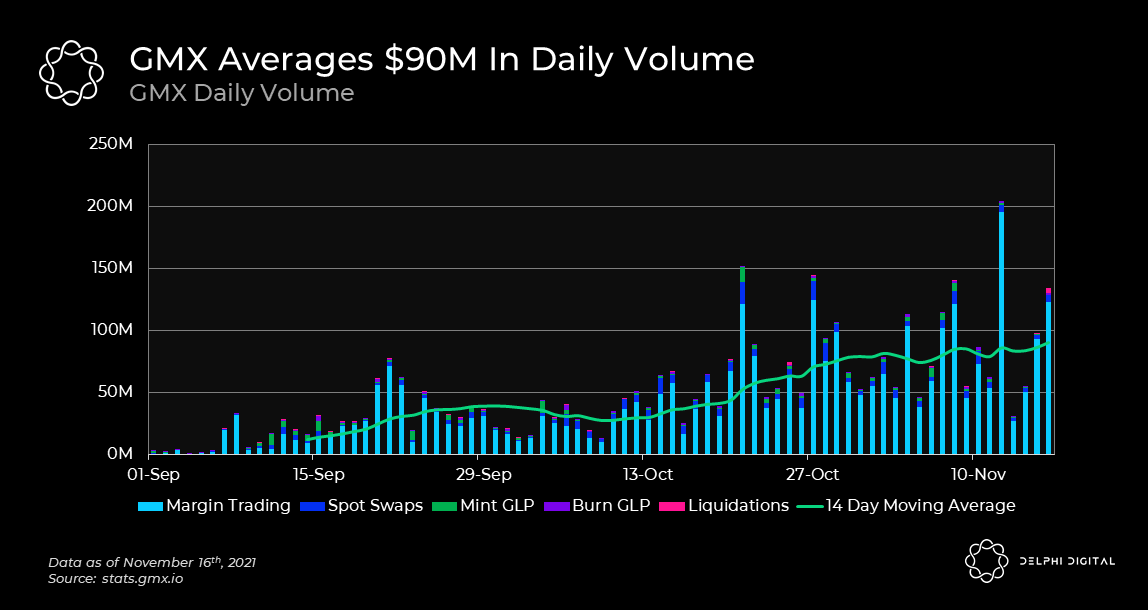

4/ The GLP pool sits at $100M AUM and has historically had utilization rates of ~100% per day!

This is extremely high and is made possible by the oracle based pricing and dual utility of capital. Spot swaps & perps.

This is extremely high and is made possible by the oracle based pricing and dual utility of capital. Spot swaps & perps.

5/ GMX's GLP equivalent called USDG, launched on BSC boasts a 200-300% utilization per day on spot swaps alone!

One would expect spot swap volume for GLP to further increase with more activity on Arbitrum, addition of GLP to aggregators and CEX deposits / withdrawals.

One would expect spot swap volume for GLP to further increase with more activity on Arbitrum, addition of GLP to aggregators and CEX deposits / withdrawals.

6/ Based on daily GLP fees, ~$157K over the past two weeks, GMX is projected to bring in over ~$57.3M in annualized revenues.

This represents a GLP natural fee APR of ~64%!

Fees are distributed 70% to GLP LPs and 30% to GMX stakers.

This represents a GLP natural fee APR of ~64%!

Fees are distributed 70% to GLP LPs and 30% to GMX stakers.

7/ These are some pretty crazy returns especially considering GLP is made up out of blue-chip assets like BTC, ETH and stables.

Lets break down how GMX works and discuss GLPs potential risks.

Lets break down how GMX works and discuss GLPs potential risks.

8/ When traders open leverage positions on GMX they are utilizing assets within the GLP.

Entering a long on ETH can be described as “renting out” the upside of ETH in GLP.

Ex: 2 ETH of leverage = 2 ETH from GLP is “rented out” to give the trader their desired exposure.

Entering a long on ETH can be described as “renting out” the upside of ETH in GLP.

Ex: 2 ETH of leverage = 2 ETH from GLP is “rented out” to give the trader their desired exposure.

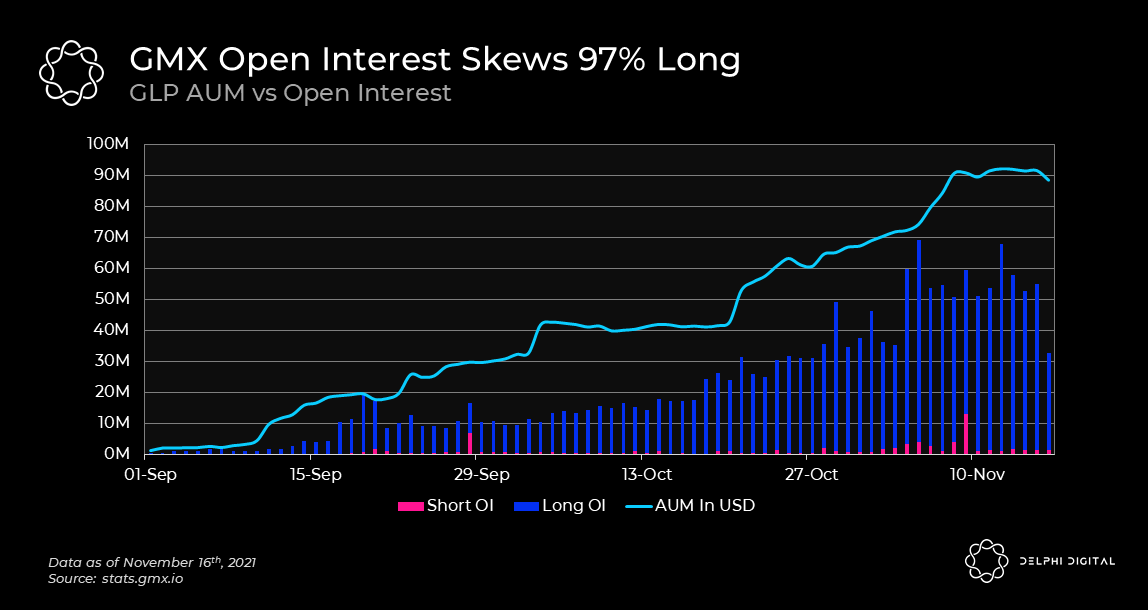

9/ Meaning that open interest for perp positions is capped at the total assets within GLP.

Since we are in a bull market and borrowing rates are calculated based on utilization of an asset versus the demand for longs vs shorts, we get a very skewed distribution of OI on GMX.

Since we are in a bull market and borrowing rates are calculated based on utilization of an asset versus the demand for longs vs shorts, we get a very skewed distribution of OI on GMX.

10/ With 97% of the platform long, GLP is forgoing some of its upside to perp traders.

If these perp traders make money, GLP needs to pay them the upside that they've borrowed.

If traders are super profitable on GMX this makes GLP a potentially unattractive place to LP.

If these perp traders make money, GLP needs to pay them the upside that they've borrowed.

If traders are super profitable on GMX this makes GLP a potentially unattractive place to LP.

11/ In a bull market this design is fairly safe, its difficult for GLP to actually lose money due to the long skew (just lose upside).

In a bear market with the platform skewed short, GLP would be paying out stables while the value of ETH, BTC, LINK & UNI in the pool fall.

In a bear market with the platform skewed short, GLP would be paying out stables while the value of ETH, BTC, LINK & UNI in the pool fall.

12/ So how can we make GLP more resilient for LPs in all market conditions?

A potential solution is redistributing a portion of GLP fees to the underutilized side mimicking a funding rate used with traditional perp models.

A potential solution is redistributing a portion of GLP fees to the underutilized side mimicking a funding rate used with traditional perp models.

13/ An example of this could be tweaking the fee distribution slightly ex:

15% of fees to the underutilized side, 25% to GMX stakers, and 60% to GLP holders.

Resulting in ~$8.6M per year to incentivize shorts on GMX.

15% of fees to the underutilized side, 25% to GMX stakers, and 60% to GLP holders.

Resulting in ~$8.6M per year to incentivize shorts on GMX.

14/ Over the past 3 months traditional ETH perps have been paying ~15-20% APR to shorters.

With $8.6M you could incentivize a constant demand of ~$25M worth of shorts on GMX with a 34% APR.

(although this would require increasing stable coin weights in GLP slightly).

With $8.6M you could incentivize a constant demand of ~$25M worth of shorts on GMX with a 34% APR.

(although this would require increasing stable coin weights in GLP slightly).

15/ This would change the long short skew from $50M/$1M to $50M/$25M. Making GLP less directionally biased in return for a slightly lower fee APR, dropping from 45% to 39%.

This example shows that GLP can be made less directionally biased while maintaining an attractive APR.

This example shows that GLP can be made less directionally biased while maintaining an attractive APR.

16/ With reduced directional risk, GLP becomes more resilient in all market conditions and expresses a bet against leveraged traders.

Now we have gone over the risks, lets see how GLP has actually performed. 🫐🫐

Now we have gone over the risks, lets see how GLP has actually performed. 🫐🫐

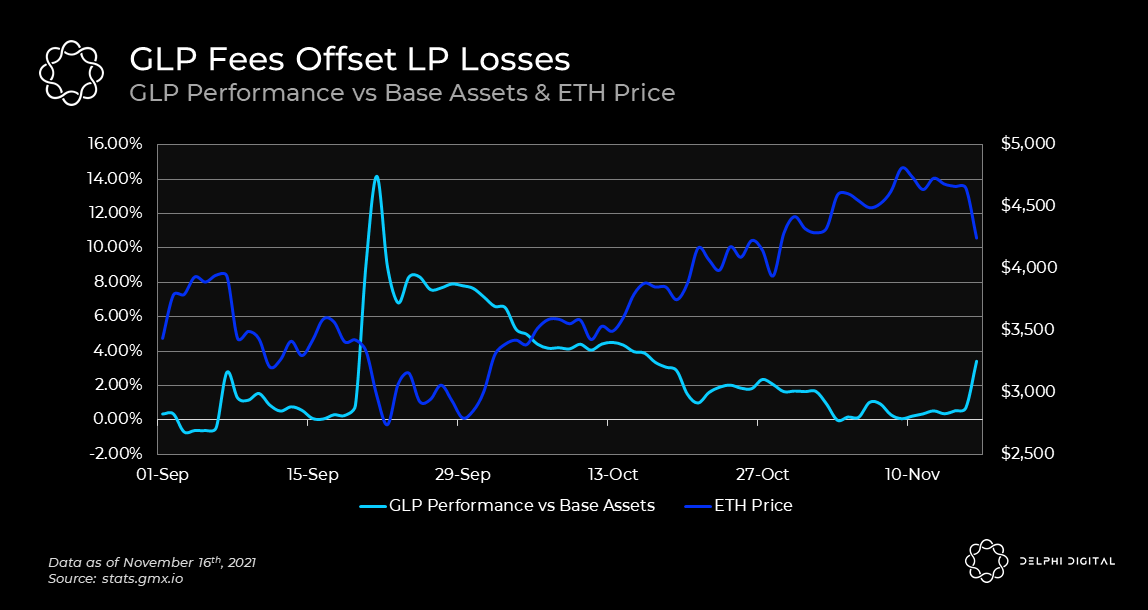

17/ Traders have made ~$1M in Net PNL on GMX since Sept 1st. Comparing this to the 70% take rate of fees, GLP has made ~$4M thus far resulting.

This results in a $3M (3.4%) outperformance versus hodling the underlying assets within GLP.

This results in a $3M (3.4%) outperformance versus hodling the underlying assets within GLP.

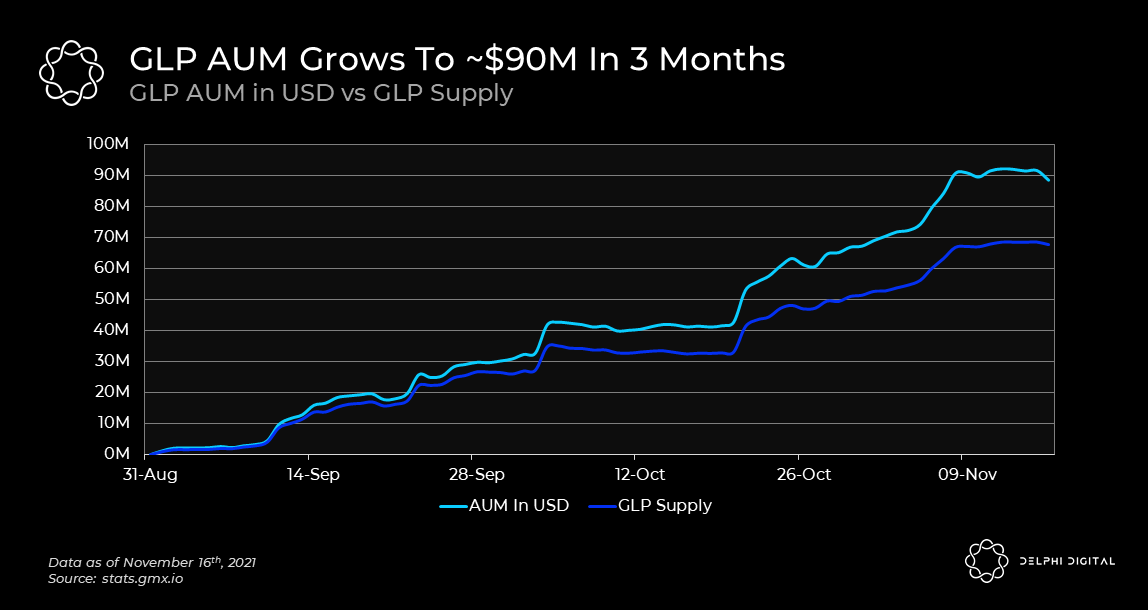

18/ In order for GMX to succeed it is key that GLP scales.

So far GLPs growth has been great, attracting over $90M worth of liquidity in less than 3 months. (Sits at $100M at the time of writing)

GLP currently pays out 45% in ETH (from fees) and ~48% in esGMX rewards.

So far GLPs growth has been great, attracting over $90M worth of liquidity in less than 3 months. (Sits at $100M at the time of writing)

GLP currently pays out 45% in ETH (from fees) and ~48% in esGMX rewards.

19/ At a first glance esGMX rewards seem high at 48% but these rewards deserve a liquidity discount.

esGMX fully unlocks over 1 year and only keep unlocking if you continue to hold the GLP (or GMX) rewards were earned with.

This creates a strong incentive to keep AUM in GLP.

esGMX fully unlocks over 1 year and only keep unlocking if you continue to hold the GLP (or GMX) rewards were earned with.

This creates a strong incentive to keep AUM in GLP.

20/ Single sided staking is also very attractive for GMX, with over 90% of circulating supply currently staked due to these 3 rewards:

1) 30% of platform fees

2) esGMX rewards

3) Multiplier points

MP's reward long term stakers with a larger share of platform revenues.

1) 30% of platform fees

2) esGMX rewards

3) Multiplier points

MP's reward long term stakers with a larger share of platform revenues.

21/ Close to 50% of the non-circulating supply is held by the GMX treasury and is ear marked for: esGMX rewards, protocol-owned liquidity, marketing, and development.

This war chest allows flexibility for GMX in it's development and cross chain expansion.

This war chest allows flexibility for GMX in it's development and cross chain expansion.

22/ Recently $GMX lead developer @xdev_10 announced plans to launch GMX on $AVAX.

This will make GMX one of the first platforms for perps on AVAX while also providing massive benefits through it's 0 slippage swaps on assets like AVAX, ETH & BTC.

This will make GMX one of the first platforms for perps on AVAX while also providing massive benefits through it's 0 slippage swaps on assets like AVAX, ETH & BTC.

23/ With GLP’s high ~64% APR fee yield, GMX has a sustainability advantage over protocols that are attracting mercenary capital with temporary token incentives.

GLP must prove its design can scale and attract enough capital to compete with other perp and spot DEXes long-term.

GLP must prove its design can scale and attract enough capital to compete with other perp and spot DEXes long-term.

24/ If you enjoyed this thread be sure to take a look at a @Delphi_Digital Pro subscription.

Our members got access to this GMX report in even more depth last week + a ton of other great crypto pieces, telegram access, discord access, and analyst calls!

members.delphidigital.io

Our members got access to this GMX report in even more depth last week + a ton of other great crypto pieces, telegram access, discord access, and analyst calls!

members.delphidigital.io

25/ Disclosure: I own GMX.

Also some of these numbers are from last week. Refer to: gmx.io & stats.gmx.io for the most up to date numbers.

Also some of these numbers are from last week. Refer to: gmx.io & stats.gmx.io for the most up to date numbers.

Again thanks to @ashwathbk for helping me with this piece, Delphi's derivatives expert.

Loading suggestions...