Since the current decade is already looking like the 70’s in many ways (ignominious defeat on the global stage, energy crisis, inflation, new ABBA album, etc.), let’s go back to something else that happened in 1974: the establishment of the PETRODOLLAR system.

Read about it here. investopedia.com

Basically, it was a “protection racket.” Nixon struck a deal with the Arab states to standardize the sale of oil based on USD in return for “protection.” Disproportionately beneficial for the US as it created an ecosystem with more network effects than ETH can ever dream of.

There are many pundits in FinTwit (usually those long positions in BTC) foretelling the imminent demise of the USD as GRC (Global Reserve Currency) for this reason or that reason. I am here to call bullshit on that thesis.

There are many reasons to hate the USD – esp. in light of the seemingly incessant “money printing” from both excessive monetary AND fiscal pumps. BUT, like a thick-skinned comedian dodging rotten tomatoes, the USD has shrugged off every insult and exhibited amazing resilience.

Why HAS the USD been ripping lately despite unprecedented expansion of our monetary supply?

First, the determinants of value for the USD are manifold, and to base a “dollar demise thesis” on a single-variable regression to “Debt/GDP” is as misleading as basing a “world demise thesis” on a single-variable regression to “atmospheric carbon concentration.”

The world of FX in particular is about RELATIVE VALUE and COMPARATIVE ADVANTAGE. One can’t legitimately say that one “hates the USD” without also saying “relative to what.” Sorry, BTC does NOT fix this, so don’t even go there. What’s left? EUR? JPY? CNY?

Before we even go back to the petrodollar system, there are many other reasons why the world has chosen the USD as GRC – despite the repeated insults we’ve thrown at it in terms of escalating Debt/GDP.

Again, we need to take a step back and think about what other COMPARATIVE ADVANTAGES we have over other countries.

I wrote a thread a while back about why our GEOPOLITICAL ADVANTAGES are unparalleled, which would explain reflexive “safe haven” bids for our USTs and the USD when the rest of the world shits the bed -- IN SPITE OF AN AGGRESSIVE WEAK DOLLAR POLICY.

The other reason I think the USD has been strengthening is ironically related to the structural bull-market emerging in OIL. “Ironic” because the traditional relationship between USD and oil has been an INVERSE correlation.

BUT that inverse correlation has been breaking down. This article gives some reasons: babypips.com

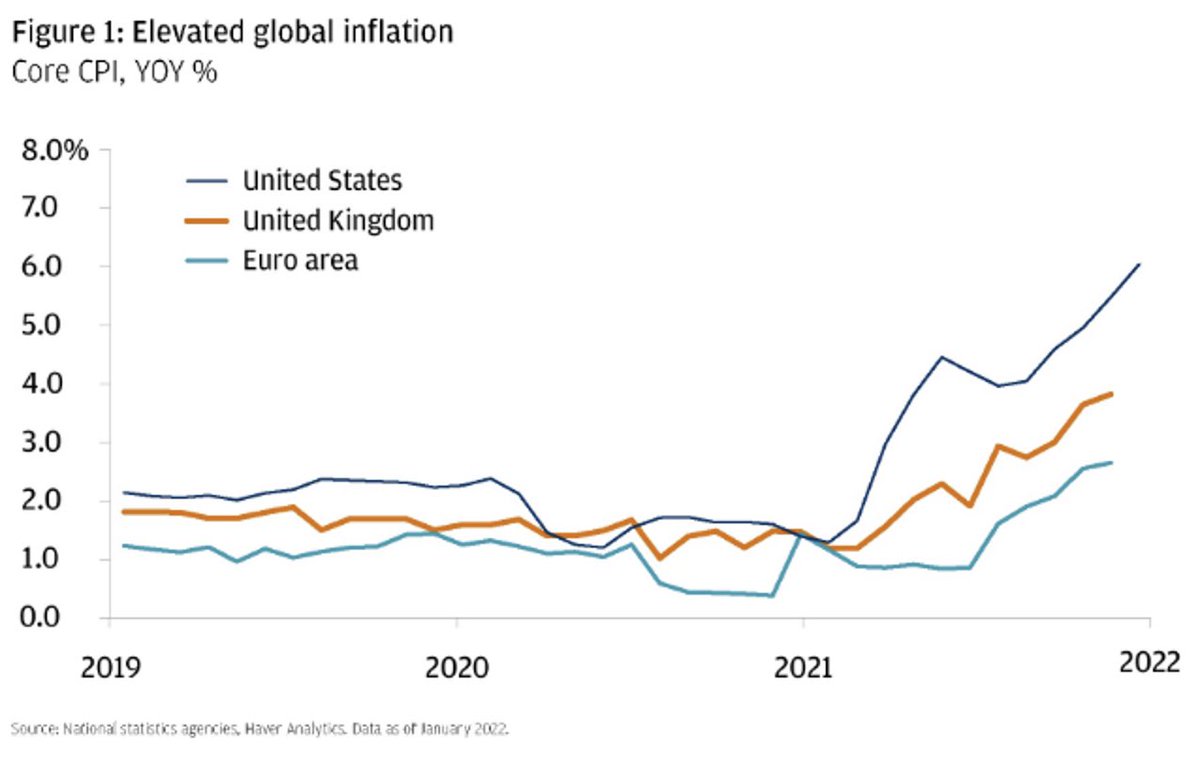

If anything, I think oil’s secular STRENGTH is driving USD STRENGTH this time around, because 1) oil is by far the largest cap-weighted commodity...

2) its strength is derived from structural issues years in the making but hugely exacerbated by current policies, 3) oil inflation is NOT likely to be transitory.

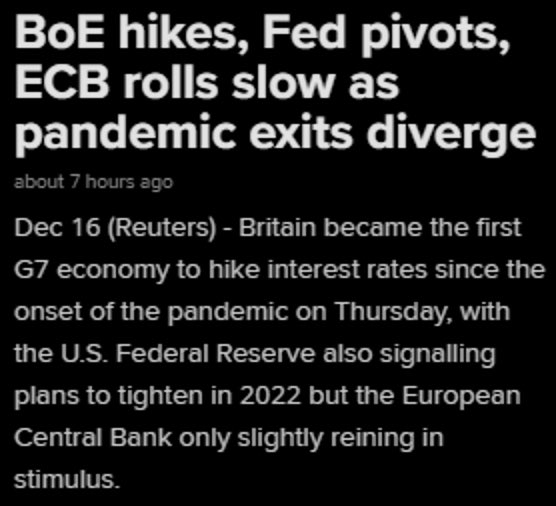

As such, OIL INFLATION has ALREADY opened the Overton Window to an early taper (weren’t the USD doomsayers preaching “QE forever” just a month ago?) and will likely do the same for HIKING, despite Powell’s best attempts to be “stock market whisperer” yesterday.

When Powell abruptly drops both “transitory” and the “2% inflation target” in his rhetoric, do you trust him when he says that “rates will remain near zero until we reach full employment”? All it takes is triple-digit oil to change that tune!

So how does this create a stronger USD? Aside from qualitative “comparative advantage” factors I mentioned, FX exchange rates are driven quantitatively by CHANGES IN INTEREST RATE DIFFERENTIAL EXPECTATIONS between countries.

In the US, we have a strong economy, a tight labor market (to quote Roman Roy, “as tight as a scrotum over a timpani drum”), and strongly rising inflation expectations – all of these portend a regime shift from EASING conditions to TIGHTENING conditions here.

As an aside, I wrote another thread about ramifications of this regime shift on risk assets:

The problem is that the RoW’s economies are NOT nearly as hot as ours – generally speaking, our COVID vax rates have been better, we have not (YET) experienced the extreme energy shortages in Europe/China, we have stimulated our economies MUCH more.

Welcome to the USD Wrecking Ball.

These economic disparities imply UNSYNCRONIZED MONETARY POLICIES with the US leading the regime shift to tighter policies.

And because FX rates are determined by changes in interest differential expectations, the USD has and will continue to STRENGTHEN until global economies synchronize again.

In recent days, I have opined that CNY may very well defy the consensus of being UNDERvalued to USD and actually be OVERvalued to USD.

But the BoC is in a bind. A CB can only control 2 of the following 3 levers: 1) monetary policy, 2) FX rate, 3) capital flows.

I’m guessing that Xi won’t/can’t restrict capital flows so that leaves only one of the remaining two levers it can control: interest rates and FX. Problem: China can only ease so much because 1) it’s not far from zero-bound either, 2) US is TIGHTENING.

Seems to me that the CNY is very vulnerable to DEVALUATION. But wait, there might be another lever that China has that I might have missed:

This where I go back to the power of the PETRODOLLAR ecosystem and why that lever that Luke mentioned is not even remotely close to a safety valve for China -- MORE THAN 99% OF WORLD OIL IS DENOMINATED IN USD.

So let’s tie this all together:

Commodity (specifically OIL) Inflation ->

Driving US To Tighten Faster Than RoW ->

USD Strength Becomes Wrecking Ball For Weaker Economies ->

Eventually Feeds Back To US

Commodity (specifically OIL) Inflation ->

Driving US To Tighten Faster Than RoW ->

USD Strength Becomes Wrecking Ball For Weaker Economies ->

Eventually Feeds Back To US

I wrote this a while back, which is essentially the same thesis, but without the tie-in to the USD as a transmission mechanism for risk-off:

Oil will eventually spell the seeds of its own demise, but because this is a structural situation AND because the US shot its SPR bullets too early, there is a LONG runway for the "Crucible of Pain."

Lmk what you all think. I am worried, but that’s what I do.

Literally just saw this pop up.

The UNEVENNESS of global regime shifts from easing to tightening is going to really fuck things up for some countries — China especially.

The Overton Window to tightening policy in response to inflation is definitely opening wider and wider. nytimes.com

The first victim of the USD Wrecking Ball. This is going to pressure the economies of the surrounding countries and create pressure for “EUR fracture” risk again. zerohedge.com

Chalk productivity as another key reason for why USD is GRC for foreseeable future. H/r to my friend Todd for this. marketwatch.com

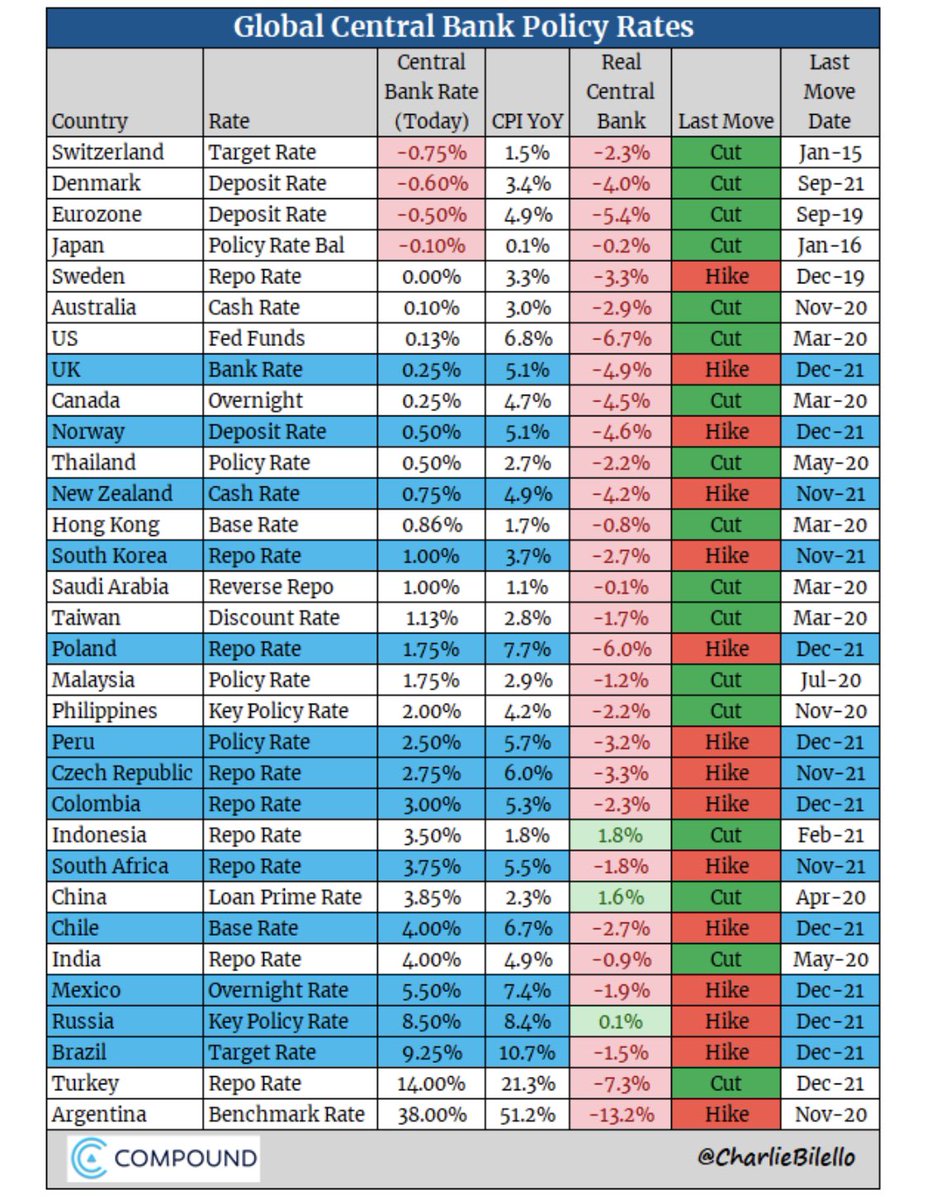

So much to digest in this chart from @charliebilello. What stands out is the stark dichotomy in real rates in the US and China and what mean reversion will mean.

Looks like Powell is starting to take away the monetary punchbowl while Manchin is guarding the fiscal punchbowl at the same time.

Interesting chart. With respect to China and CNY specifically, I think it ignores the key issue of China’s pressure to ease in the face of its RE fallout while the US tightens.

Hmmm 🤔 zerohedge.com

Musing of the Day: When O&G is OG again, it might not be pretty for a whole lotta other things.

Ouch.

It’s really hard to envisage CNY continuing to strengthen given the opposing trajectories of monetary policies in China and the US.

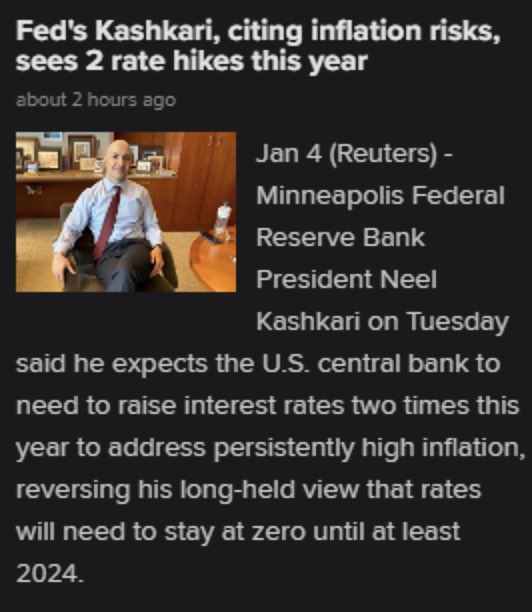

Talk about a shift in the Overton Window for tapering/tightening. This is from the biggest dove there is.

Just watch. Powell will be eating his words soon too. 👇

The USD is an equal-opportunity wrecking ball. Apparently, it’s not just EM FX that should be worried.

Oops!! Lol. That sure didn’t take long.

You know what else I didn’t hear today? Talk about YCC. What happened to all the YCC’ers?

Exactly.👆

From the second biggest dove…

nytimes.com

nytimes.com

More shades of ‘97…

And that’s how the Overton Window to accelerated tightening shifted…

If this isn’t a tell that the CNY is at risk of devaluation, idk what is.

Here we go…

There are obviously geopolitical concerns with this one (RUB), but the USD Wrecking Ball continues to swing nonetheless.

“Rumors of my death have been greatly exaggerated.” 💪USD -> 💥

MSM catching on to this theme. h/r @JohnCarey17 for pointing out.

The pressure builds.

Strong USD + Strong Oil = EM Rekt

Watch CNY 😬

Watch CNY 😬

100% agree with this. That the USD is exhibiting STRENGTH despite an overtly Weak USD Policy should give the world (especially commodity importing EM) cause for concern.

Reminder that lots of talking heads just 6 mos ago said the Fed could never tighten. Crazy how the Overton Window shifted by this much.

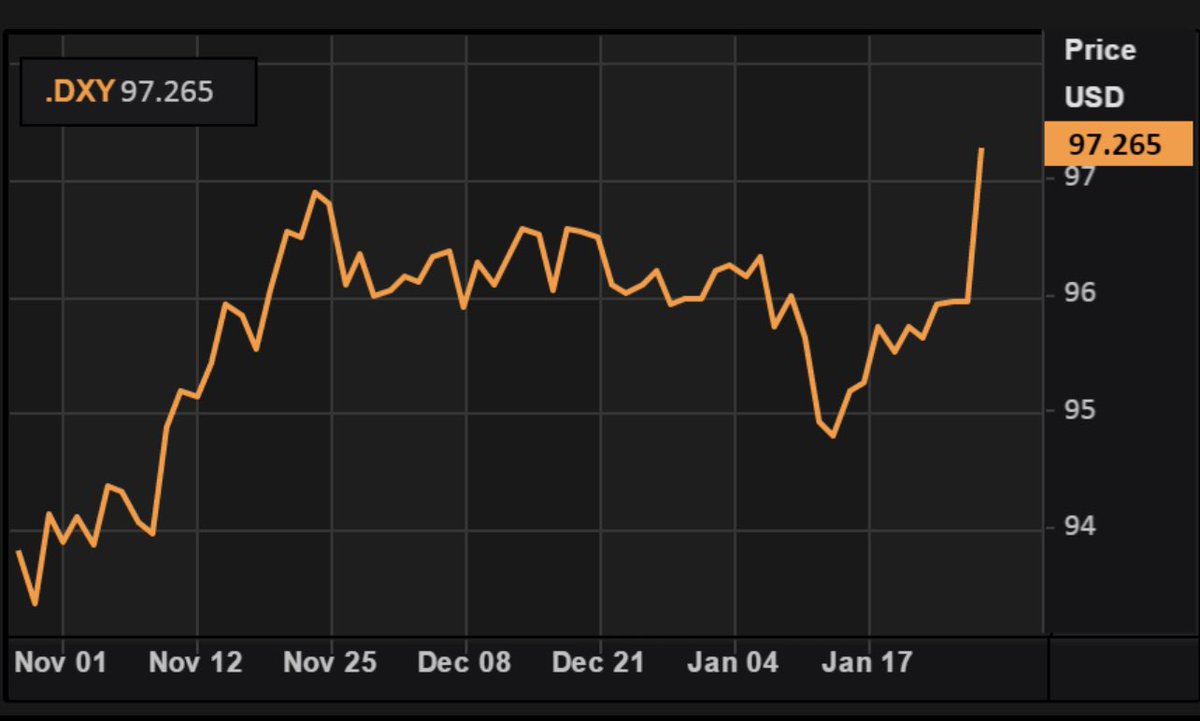

USD notably keeping gains despite today’s de-escalation flight out of safe havens. Fed water cooler arguments about that PPI print likely heating up.🔥

USD Wrecking Ball is just beginning to swing given how behind the curve the Fed is. (Chart h/t to JPM)

My “Oil->USD Wrecking Ball” thesis is coming true, and it is NOT a good thing for risk assets.

Appending @SantiagoAuFund’s fantastic thread to my own “USD Wrecking Ball” thread. We are reaching similar conclusions, albeit slightly different paths.

USD Wrecking Ball to Putin:

“Here’s the RUB.”🖕

“Here’s the RUB.”🖕

Appending to USD Wrecking Ball thread. Lots of speculation that the wrecking of the RUB pushes the de-dollarization push especially for China. I disagree. Not only does CNY have issues of its own, the immolation of the RUB highlights the danger of being out of the USD system.

Many say that this is bearish for the USD’s prospects as GRC. I say it has just convinced anyone “on the fence” to tread ever so carefully and stay within the orbit of the USD.

USD Wrecking Ball not just a threat to EM FX.

This bolsters the USD Wrecking Ball thesis.

👆

@LukeGromen pointed out CNY strength in recent days. Rather than interpret this as some harbinger of CNY supplanting USD, I interpret this as China's desperate attempt to paint a picture. I think CNY is under serious pressure to DEVALUE, and if it does, China takes RoW down.

As it is, I'm not sure how China is going to feed its people in the wake of Ukraine. If CNY goes...

CNY “strength” is a manipulated façade, imho. China easing while US tightens does NOT bode well for CNY, and Xi is terrified what a weaker CNY portends while food/energy prices (mostly USD denominated) spike.

zerohedge.com

zerohedge.com

👆

Yes. 👆

What about reduced foreign investment in China due to fear of future reprisals a la Russia? I expect that will further challenge China growth->more pressure for PBOC to ease->more pressure on CNY to weaken. wsj.com

Here’s the problem with the thesis that QE will once again fix things:

This is will continue to drive USD relative strength. From GS this am:

“The house baseline of seven hikes this year (of 25bp increments) feels like the minimum for me…The Fed [is] just far too behind…”

“The house baseline of seven hikes this year (of 25bp increments) feels like the minimum for me…The Fed [is] just far too behind…”

“…Whilst 25bp seems like the likely outcome for March, given the volatile market environment we find ourselves in, I think they could switch to 50bp at some point this year (at least for 2-3 meetings).”

About that new Russia/China trading bloc designed to supplant the USD…good luck with that. This article sums up the serious challenges facing China and the CNY. bloombergquint.com

When does PBOC embark on QE and start printing CNY…while the Fed is just beginning QT? Guess what comes next.

An interesting perspective from within China. Cracks in the Dragonbear thesis?

Loading suggestions...