Technology

Finance

Cryptocurrency

Bitcoin

DeFi

Cryptoassets

Metaverse

Smart Contract Chains

Ethereum

SolLunAva

The 69 most interesting charts in crypto for 2021.

Let's do this 🎄🎅✨🧵

Let's do this 🎄🎅✨🧵

1/ Top performing cryptoassets with a current market value of over 200M.

2 clear themes in 2021; metaverse (ugh!) and smart contract chains.

Can't have one without the other.

2 clear themes in 2021; metaverse (ugh!) and smart contract chains.

Can't have one without the other.

2/ While smart contract chains raged on, Bitcoin and DeFi (1.0) on Ethereum lagged with a modest 2x YTD.

Meanwhile SolLunAva were a league of their own.

Meanwhile SolLunAva were a league of their own.

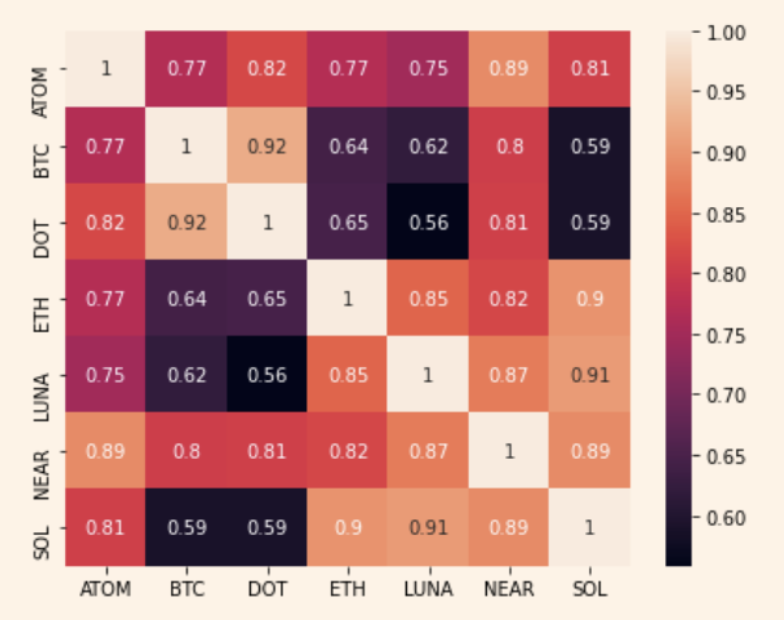

3/ Naturally the disparity in returns profiles has led correlations to weaken in 2021.

If this trend continues, 2022 is indeed going to be about long alpha-short beta.

If this trend continues, 2022 is indeed going to be about long alpha-short beta.

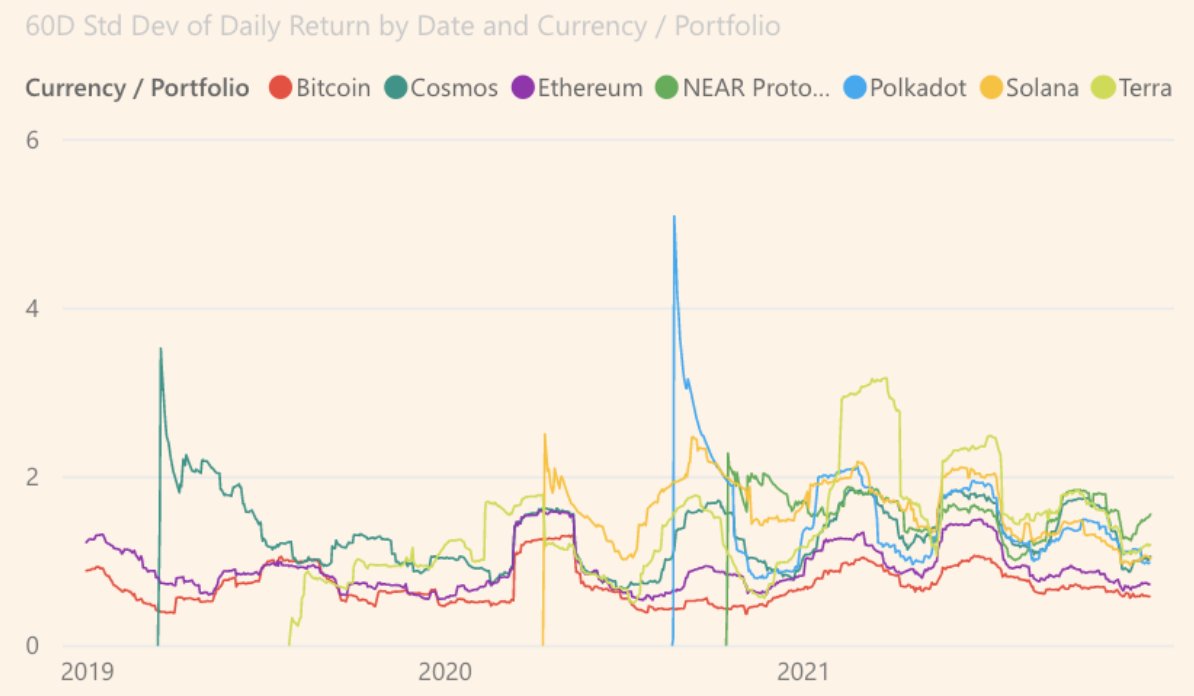

4/ Cryptoassets overall remained volatile, but towards the later half of the year volatility has been somewhat subdued.

Longer term trend remains flat-ish.

Longer term trend remains flat-ish.

5/ Amidst the volatility extreme negative funding rates on perpetual swaps continue to flash generational buying signals.

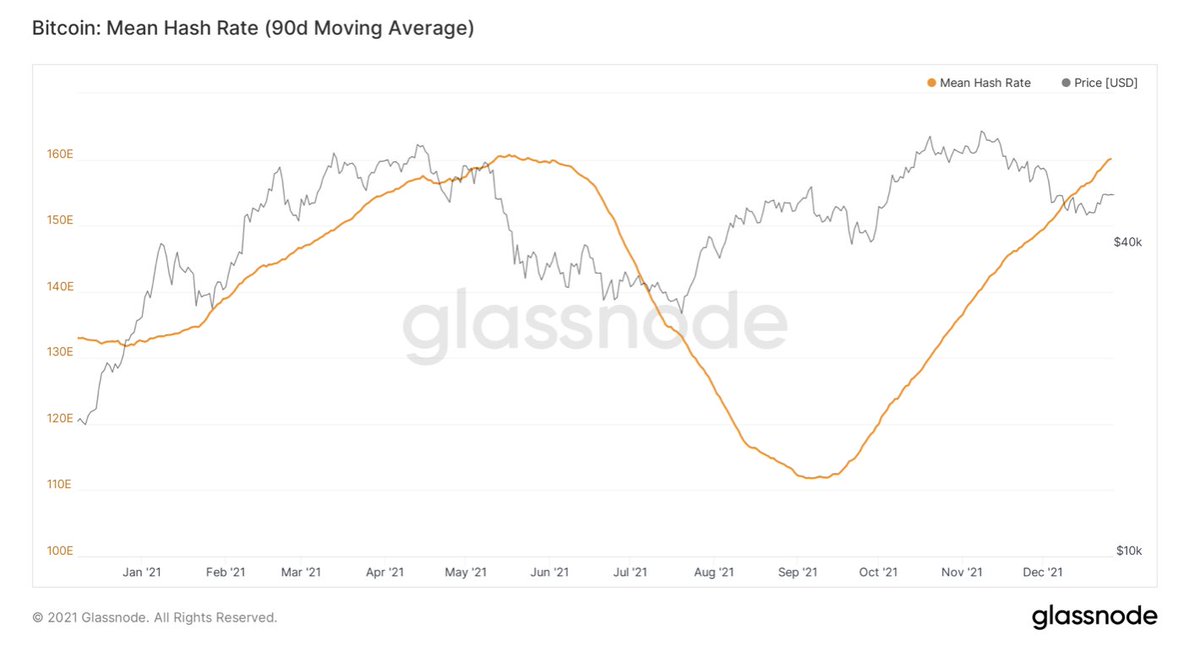

6/ The big bout of volatility this year was caused by China banning Bitcoin mining in May.

Bitcoin proceeded to lose 1/3 of its hashrate; it has since recovered it fully.

With that having come to pass, is there anything left to ban?

Bitcoin proceeded to lose 1/3 of its hashrate; it has since recovered it fully.

With that having come to pass, is there anything left to ban?

7/ As foretold earlier in this thread, this was a brutal year for Ethereum DeFi. The DPI is down 80% vs ETH.

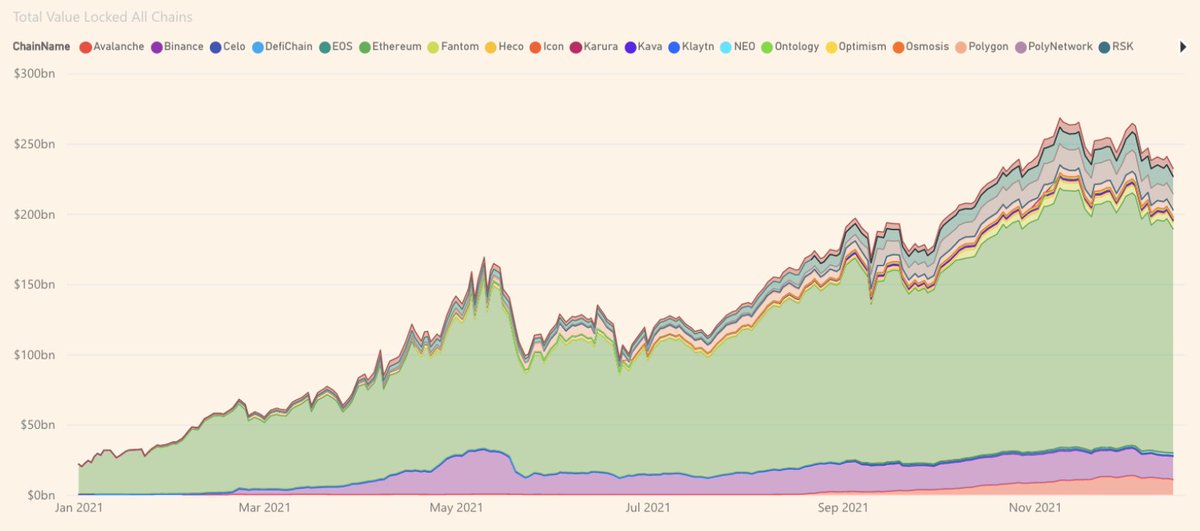

8/ The picture though is not at all indicative of this when looking at the degree of asset onboarding in DeFi applications.

Huge growth on all fronts in 2021–at least in USD terms.

Huge growth on all fronts in 2021–at least in USD terms.

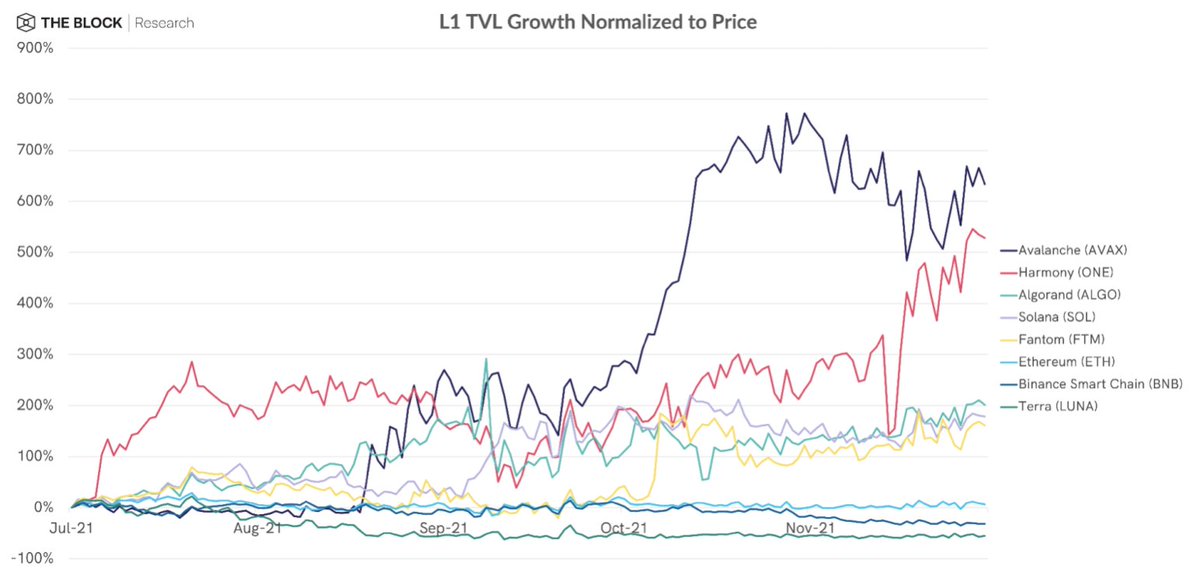

9/ Then again that very picture is not looking amazing for Ethereum DeFi when normalized for the L1’s token price appreciation.

Ethereum killers and sidechains take the W here.

Ethereum killers and sidechains take the W here.

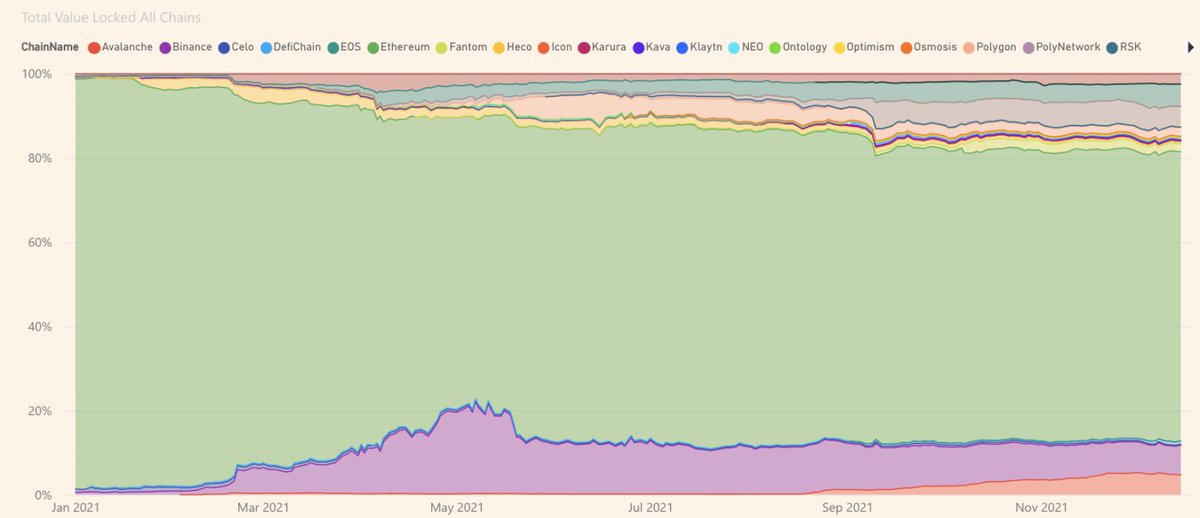

10/ As they do in terms of growing their share of the market.

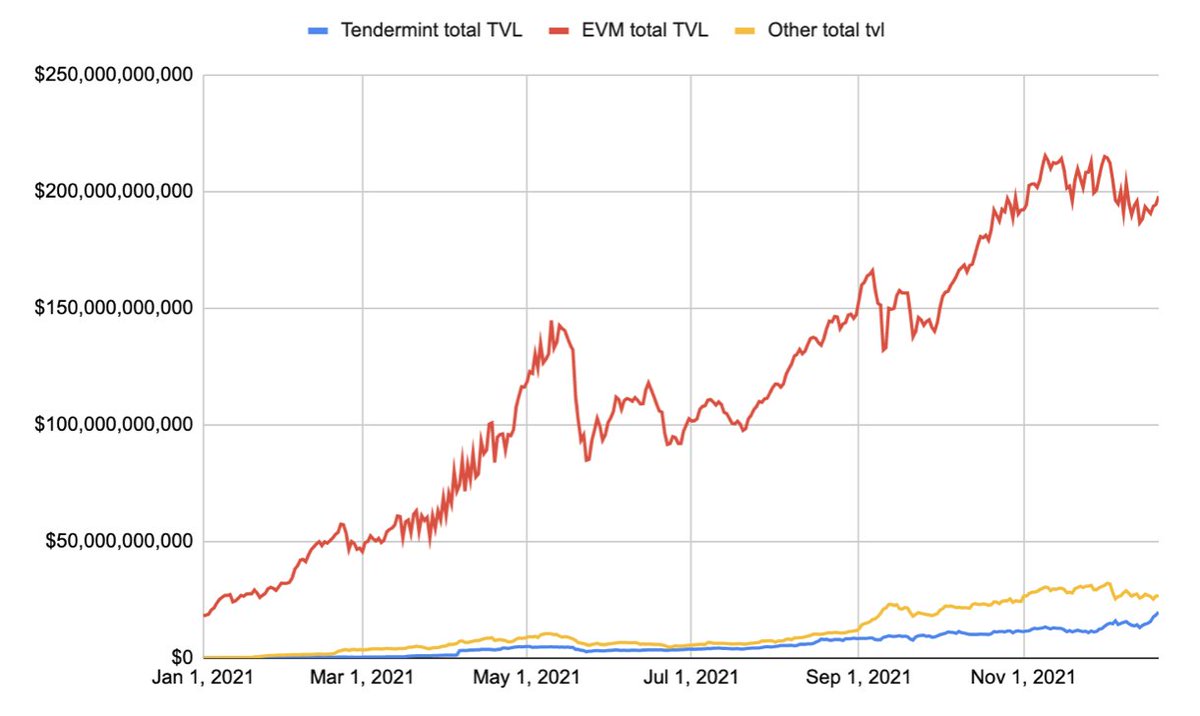

11/ There’s a flipside to all of this though. Most of the asset value today lives on EVM compatible environments. These dwarf all else by many orders of magnitude.

EVM; the standard.

Also, notice the pick-up in Tendermint based TVL more recently?

EVM; the standard.

Also, notice the pick-up in Tendermint based TVL more recently?

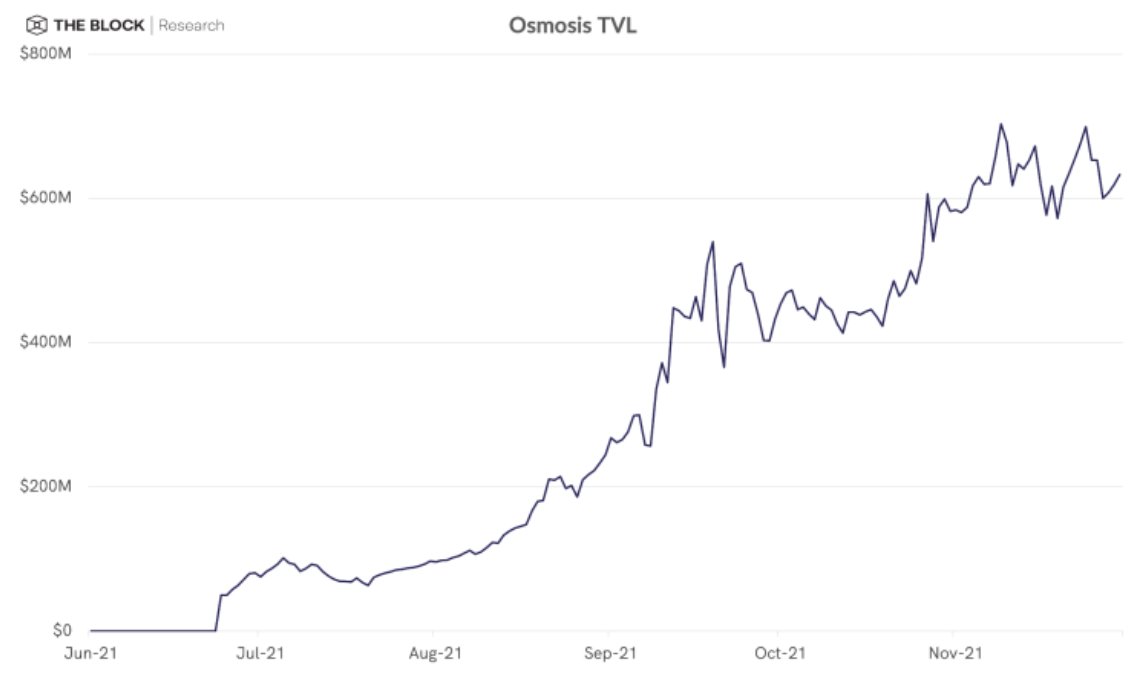

12/ There are many advantages to building application based chains.

With IBC enabled and facilities like Osmosis, Umee, Stargaze and the broader Terra ecosystem coming live and hitting their stride, there's also a lot less of the opportunity cost.

Expect more of those in 2022.

With IBC enabled and facilities like Osmosis, Umee, Stargaze and the broader Terra ecosystem coming live and hitting their stride, there's also a lot less of the opportunity cost.

Expect more of those in 2022.

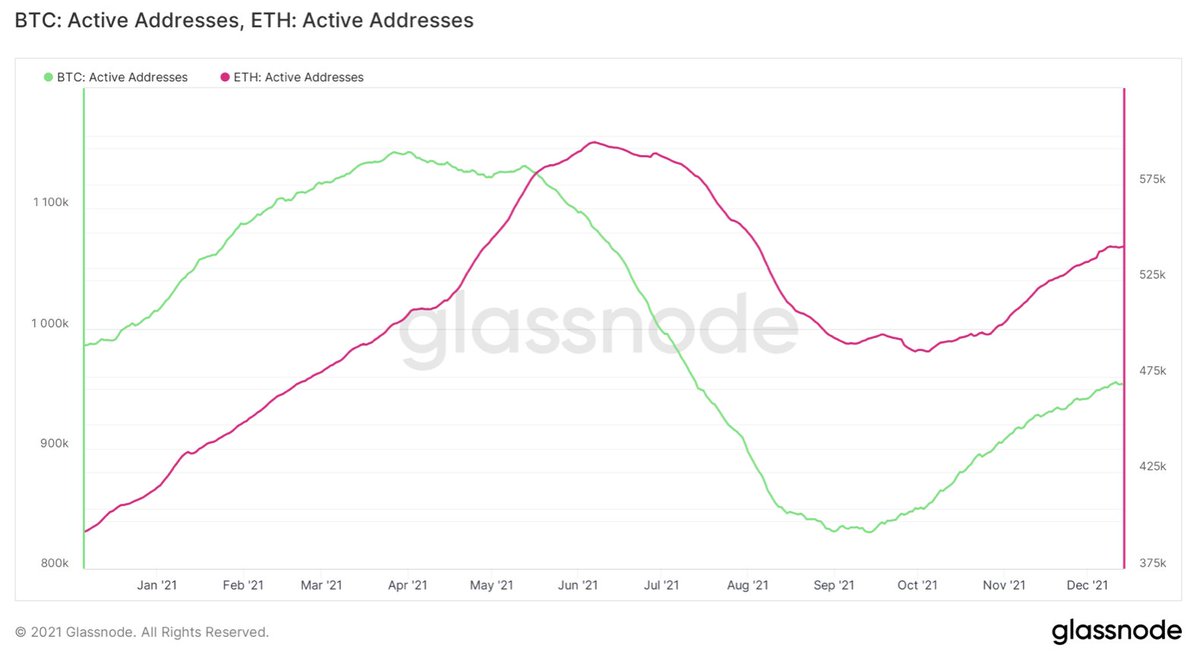

13/ Now, looking at active addresses, BTC appears to range at nearly twice as many as Ethereum.

On Bitcoin aa’s are in a clear downtrend in 2021, while on Ethereum the opposite–even in the face of all-time-highs in USD denominated gas costs.

On Bitcoin aa’s are in a clear downtrend in 2021, while on Ethereum the opposite–even in the face of all-time-highs in USD denominated gas costs.

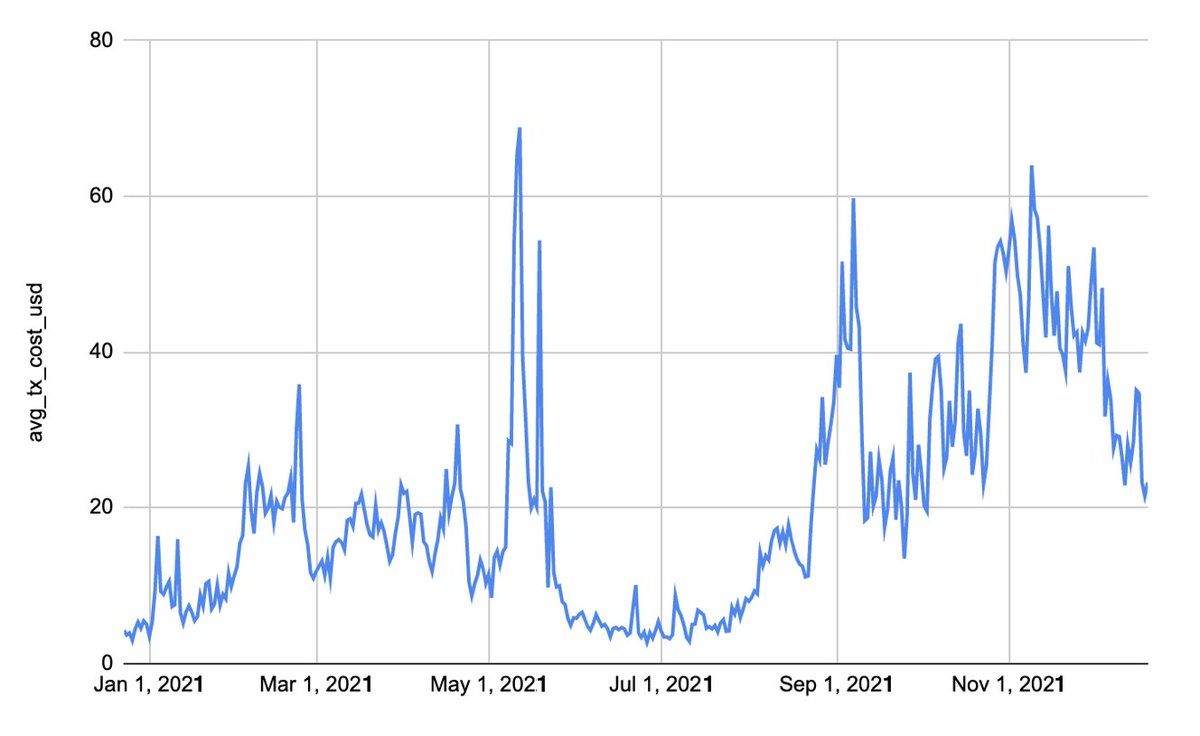

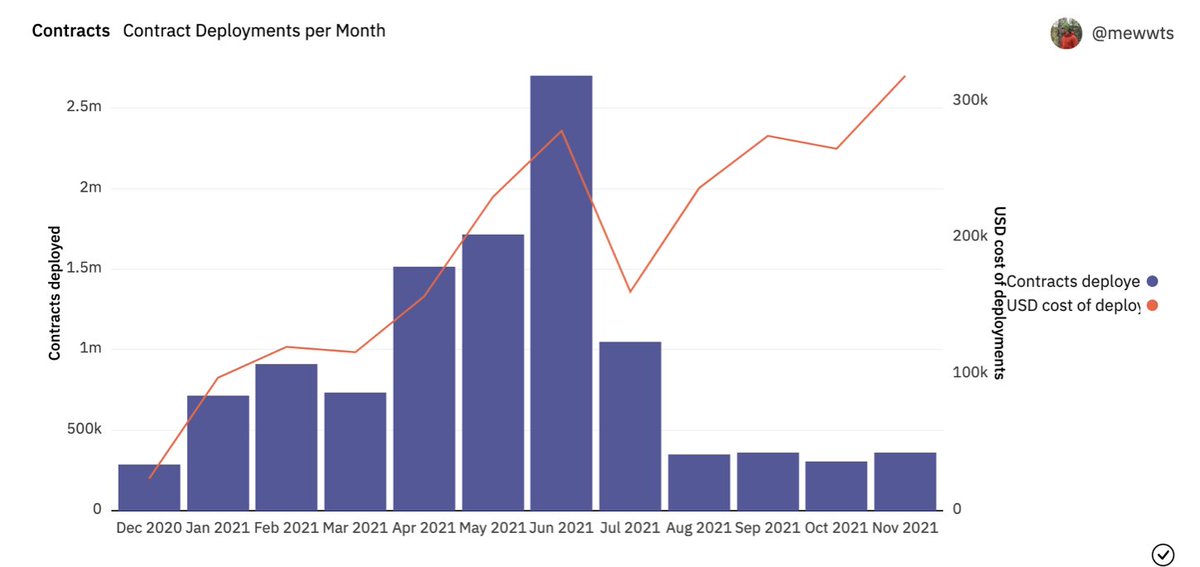

14/ Speaking of gas on Ethereum…it has been as brutal for users,

15/ as it has for developers.

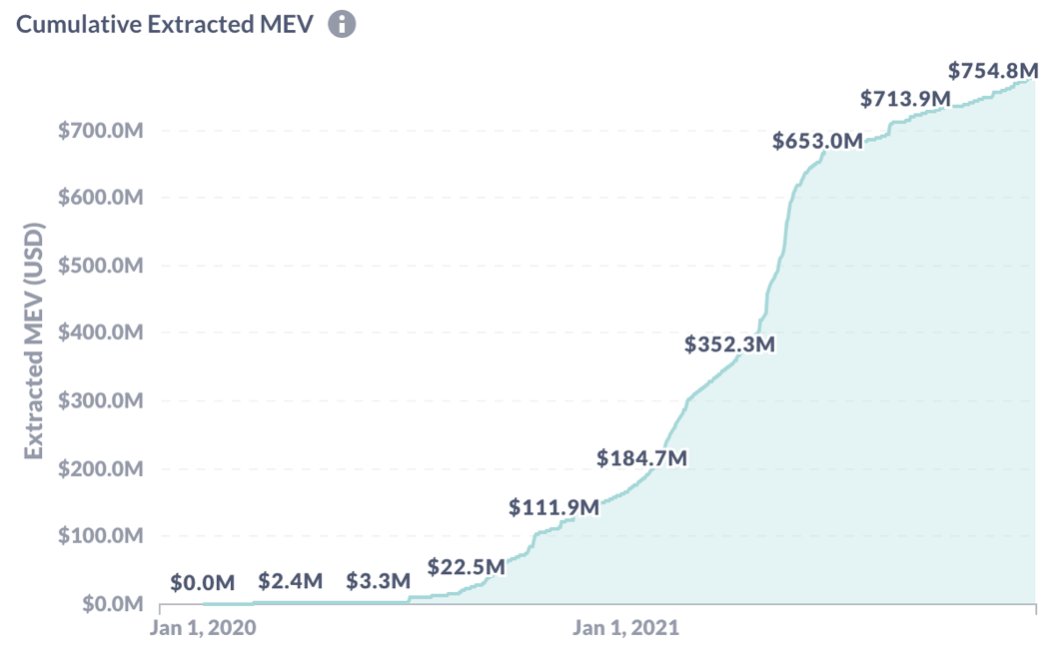

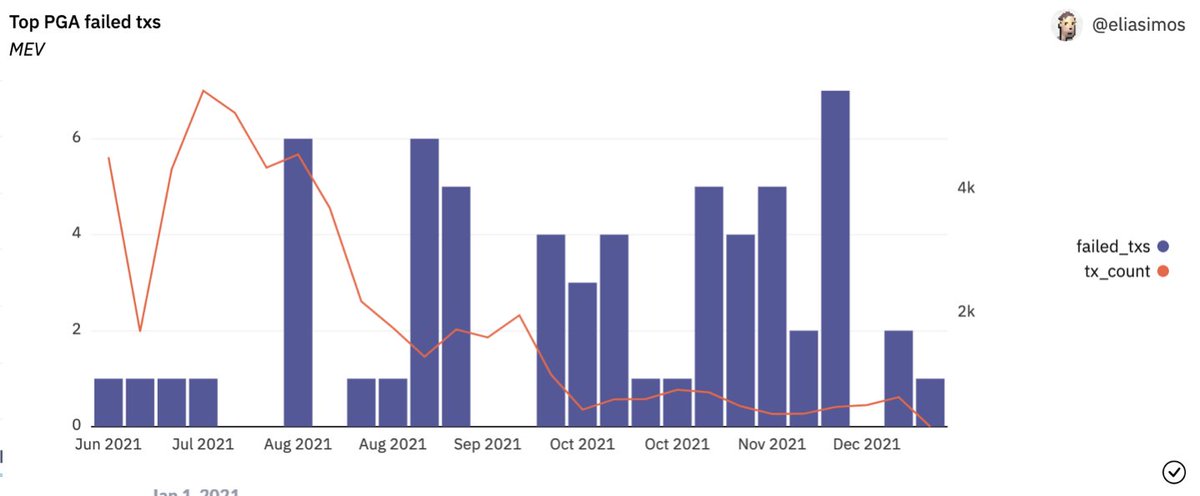

16/ MEV was undoubtedly one of the big themes of 2021.

As gas exploded upwards, MEV extraction on Ethereum slowed down in unison, most likely chasing after opportunities in cheaper EVM compatible environments as activity in those picked up.

As gas exploded upwards, MEV extraction on Ethereum slowed down in unison, most likely chasing after opportunities in cheaper EVM compatible environments as activity in those picked up.

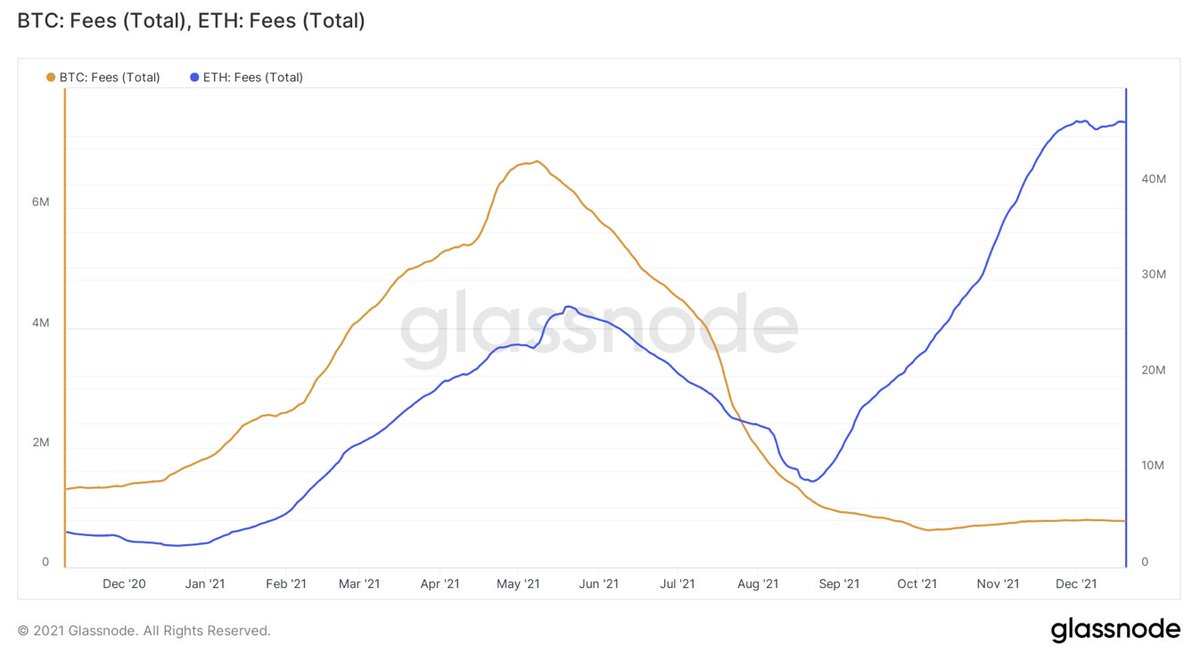

17/ On the other hand, as high gas persisted Ethereum miners had a field day; they have been earnings more in total fees than Bitcoin miners for most of 2021.

With the merge coming in 2022, both MEV and fees + inflationary rewards will be reaped by validators.

With the merge coming in 2022, both MEV and fees + inflationary rewards will be reaped by validators.

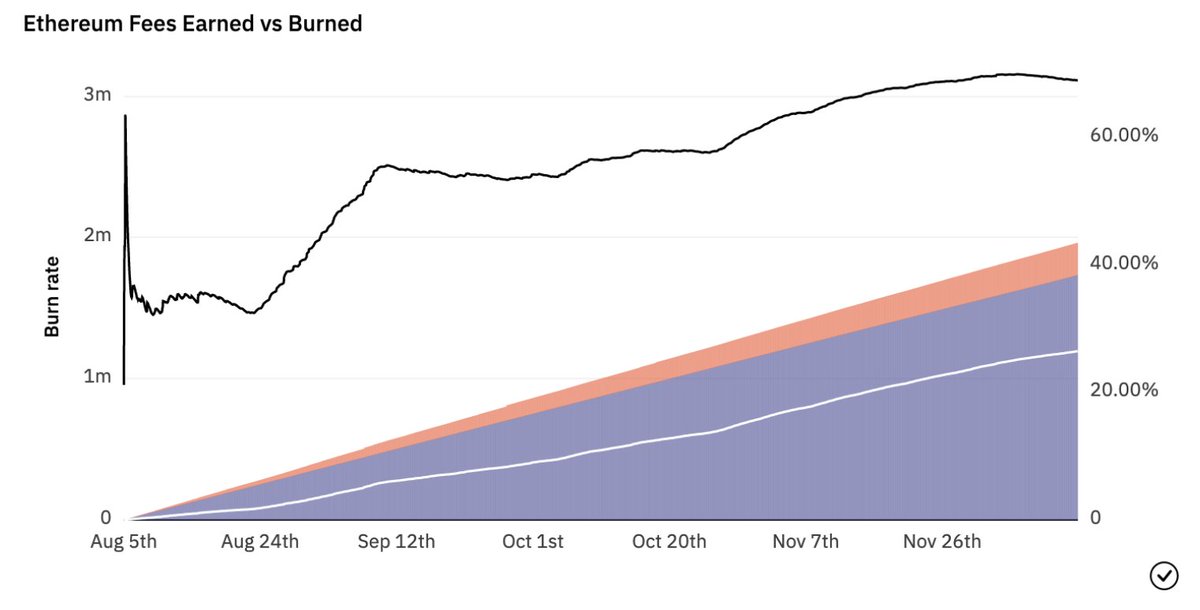

18/ Post EIP-1559, there's an aspect of ETH holders somewhat benefitting from high gas too.

Thus far 1.2M ETH has been burned, which at current prices corresponds to a whopping 5B USD.

That's the equivalent of a 2% annualized buyback on ETH’s mcap.

Thus far 1.2M ETH has been burned, which at current prices corresponds to a whopping 5B USD.

That's the equivalent of a 2% annualized buyback on ETH’s mcap.

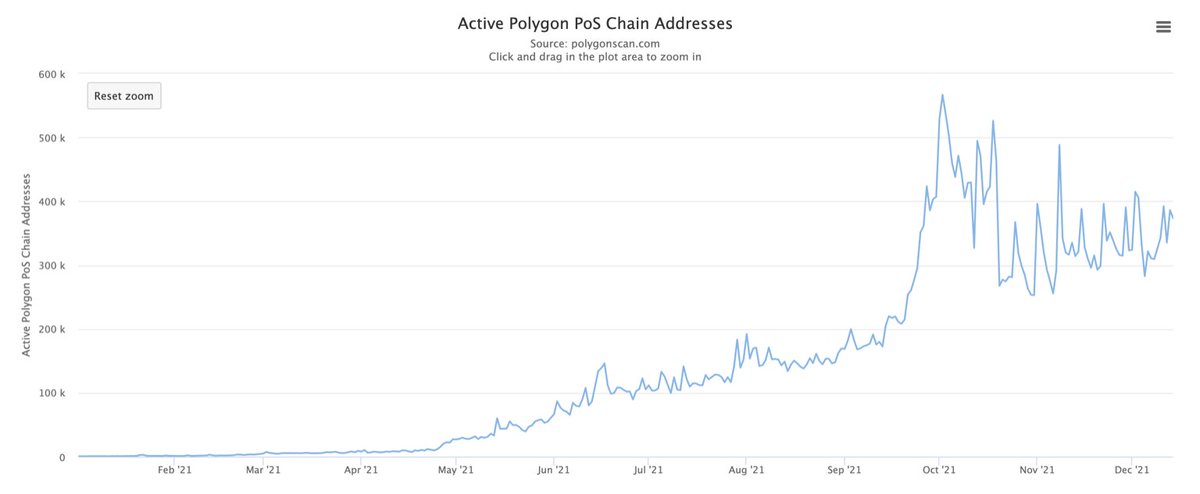

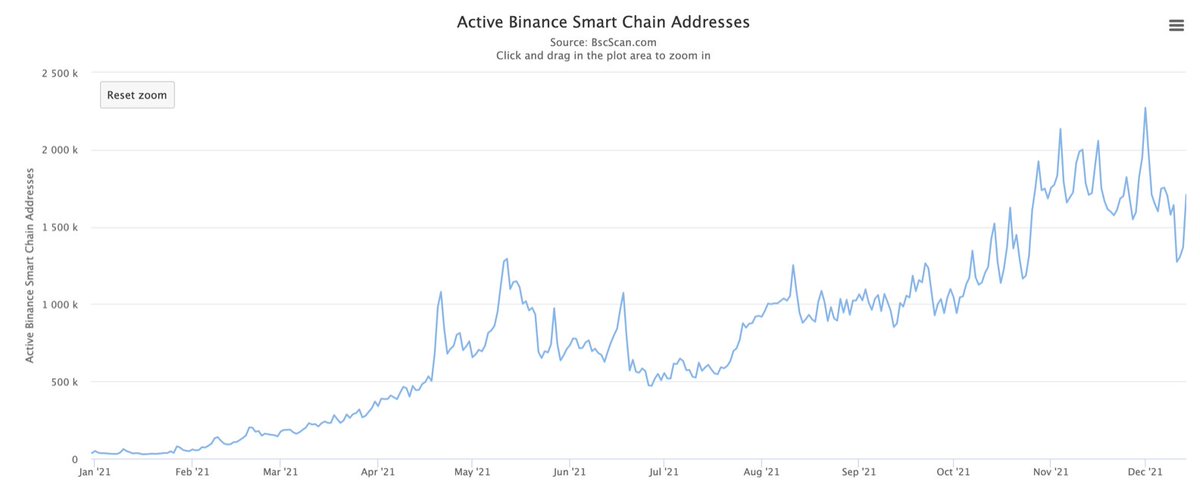

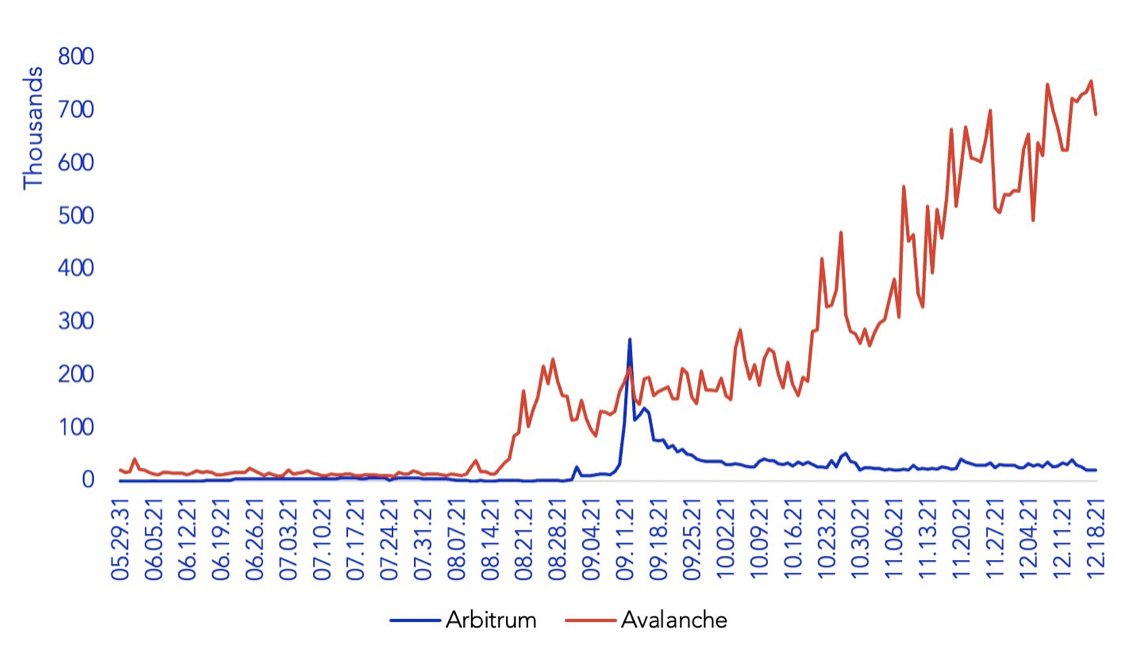

19/ As all this was unfolding on Ethereum, EVM compatible environments stepped in to serve user demand.

In most cases active addresses have been up and to the right with no real sign of stopping.

In most cases active addresses have been up and to the right with no real sign of stopping.

20/ And for all their promise, L2 rollups (at least the generalised developer platform kind) are still lagging in activity.

Let’s see what happens when they drop tokens to users.

Let’s see what happens when they drop tokens to users.

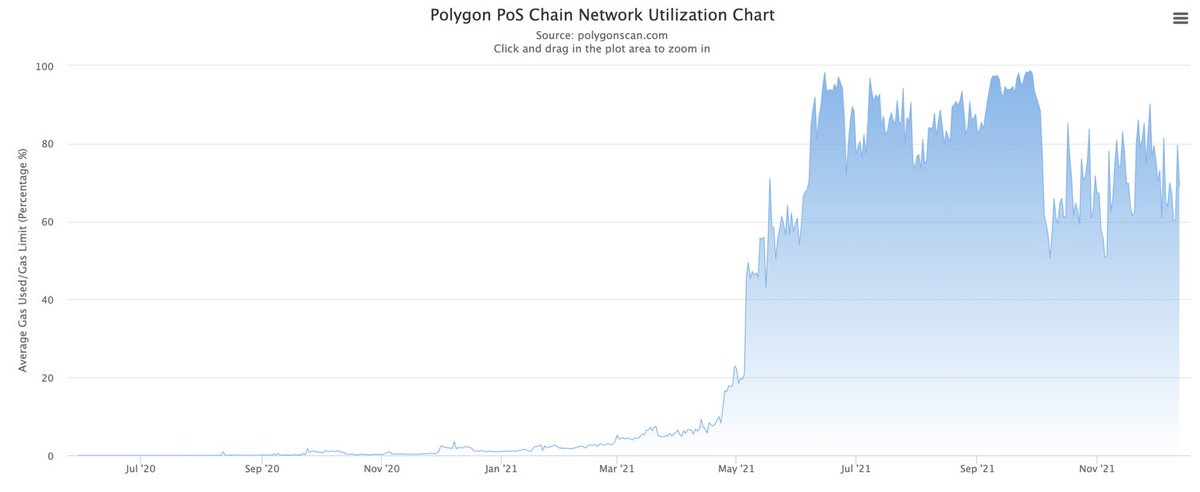

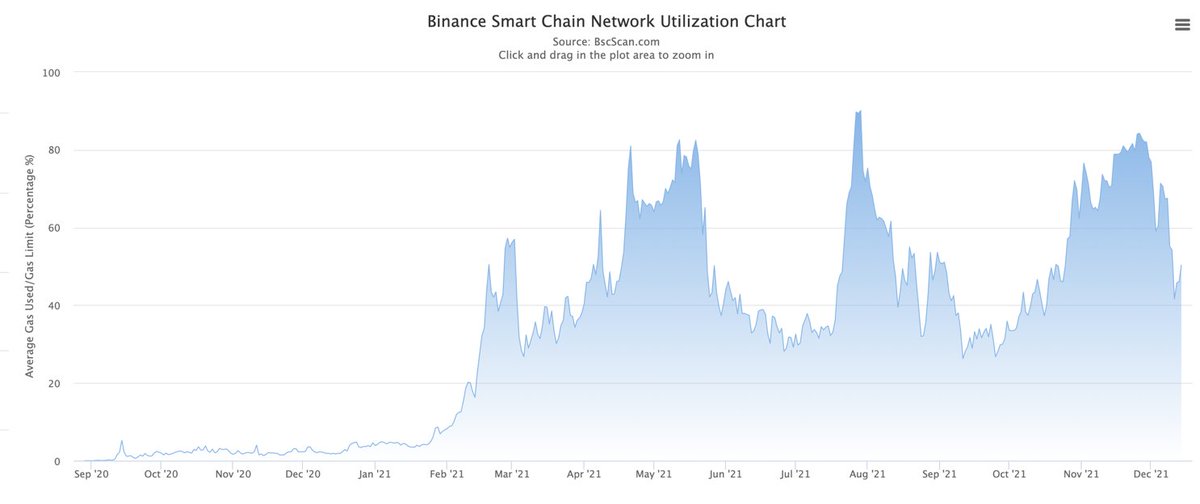

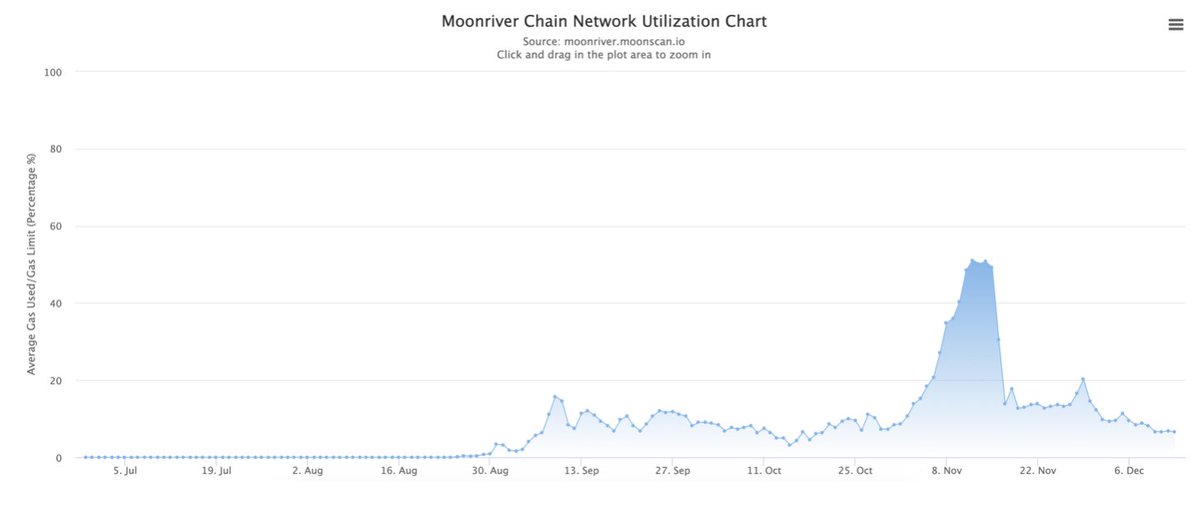

21/ There is a small kink in the whole EVM compatible chain narrative though.

In 2021 we learned that the most popular ones can too reach their limits.

In 2021 we learned that the most popular ones can too reach their limits.

22/ But with more EVM compatible environments like @MoonbeamNetwork and @EvmosOrg coming online, the global EVM blockspace will continue to increase and perhaps become increasingly commoditised.

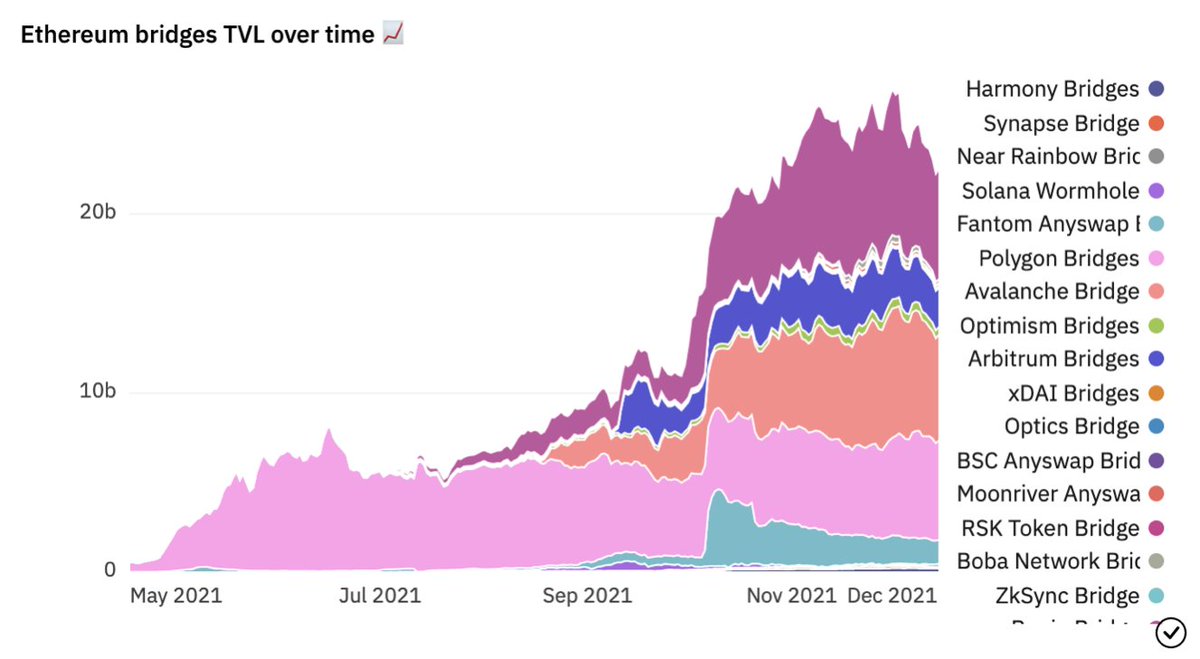

23/ The great migration to other EVM compatible environments is evident in the explosion in the activity bridging away from Ethereum.

From $200M in assets before May to over $20B locked in bridge multi-sigs to other ecosystems.

From $200M in assets before May to over $20B locked in bridge multi-sigs to other ecosystems.

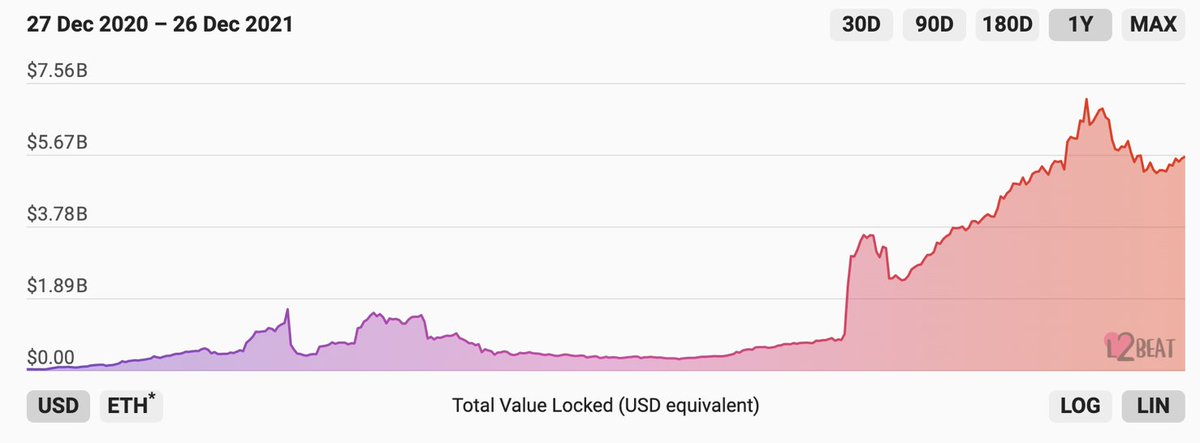

24/ On the other hand, L2's have only managed to collectively attract ~$5.5B in assets.

Again, let's see what happens when they drop tokens.

Again, let's see what happens when they drop tokens.

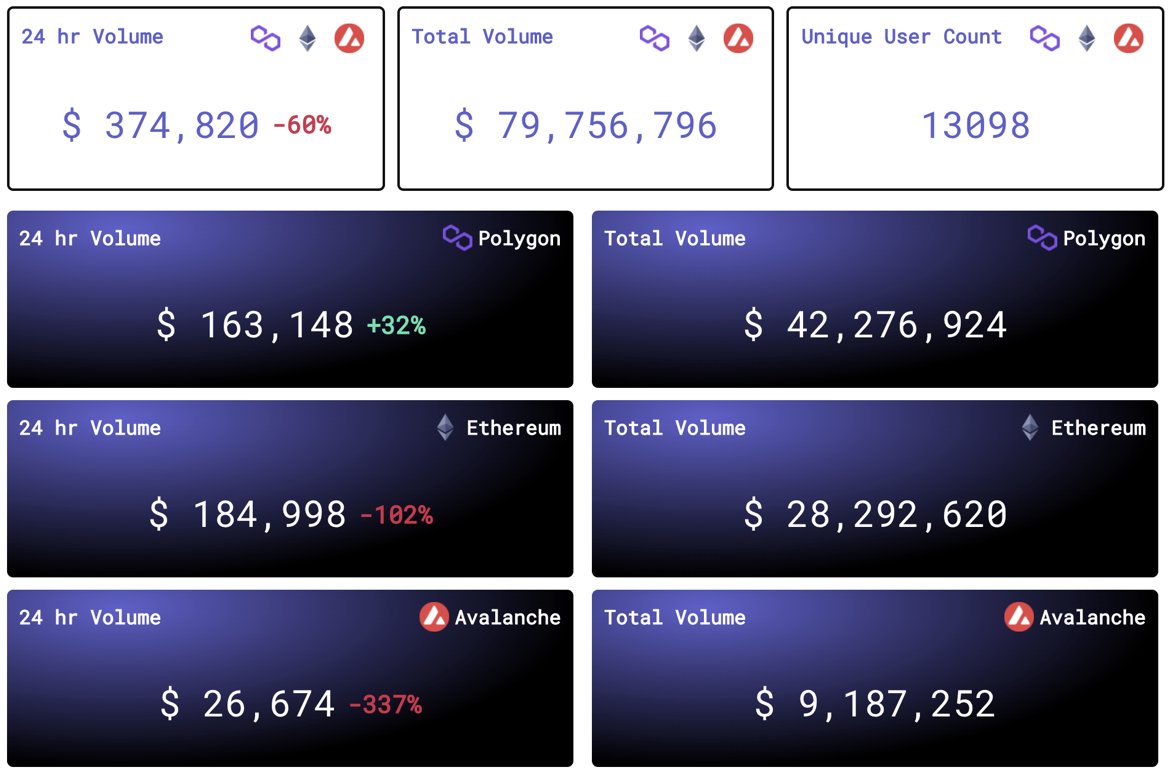

25/ At the same time, routing and liquidity protocols stepped in in a big way to fill the demand for transfers accross the disjointed EVM environments.

Arguably, these still are capacity constrained but we should expecting that to change in 2022.

Arguably, these still are capacity constrained but we should expecting that to change in 2022.

26/ As developers sought to deploy in environments other than Ethereum, Pocket Network activity picked up.

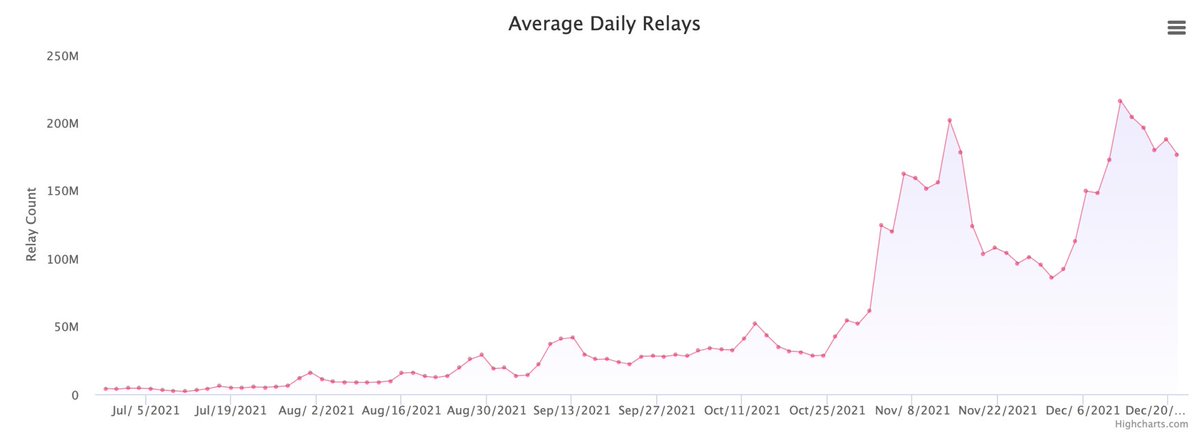

Developers need high quality read/write bandwidth. Pocket delivers that a very competitive price point.

$POKT might just be one of the best ways to go long multi-chain.

Developers need high quality read/write bandwidth. Pocket delivers that a very competitive price point.

$POKT might just be one of the best ways to go long multi-chain.

27/ Switching gears a bit, in 2021 ETH staked on the newly launched Beacon Chain grew 8-fold to over 8M ETH, in expectation of the transition to PoS.

28/ Though it looks like over time the rate of deposits has been gradually slowing down throughout 2021.

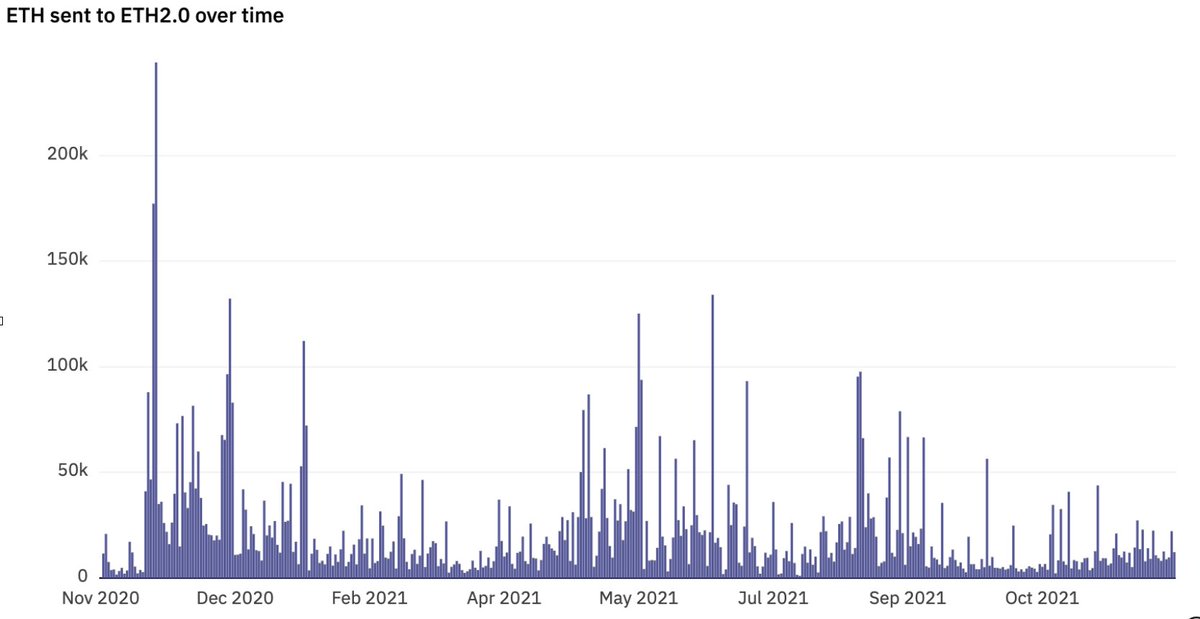

Contrary to a popular narrative that come merge time stakers will look for the exit door, I’m expecting a new surge in deposits.

Contrary to a popular narrative that come merge time stakers will look for the exit door, I’m expecting a new surge in deposits.

29/ On the network, validator effectiveness has been ranging between 90% and 95% with a couple sharp dips during network upgrades.

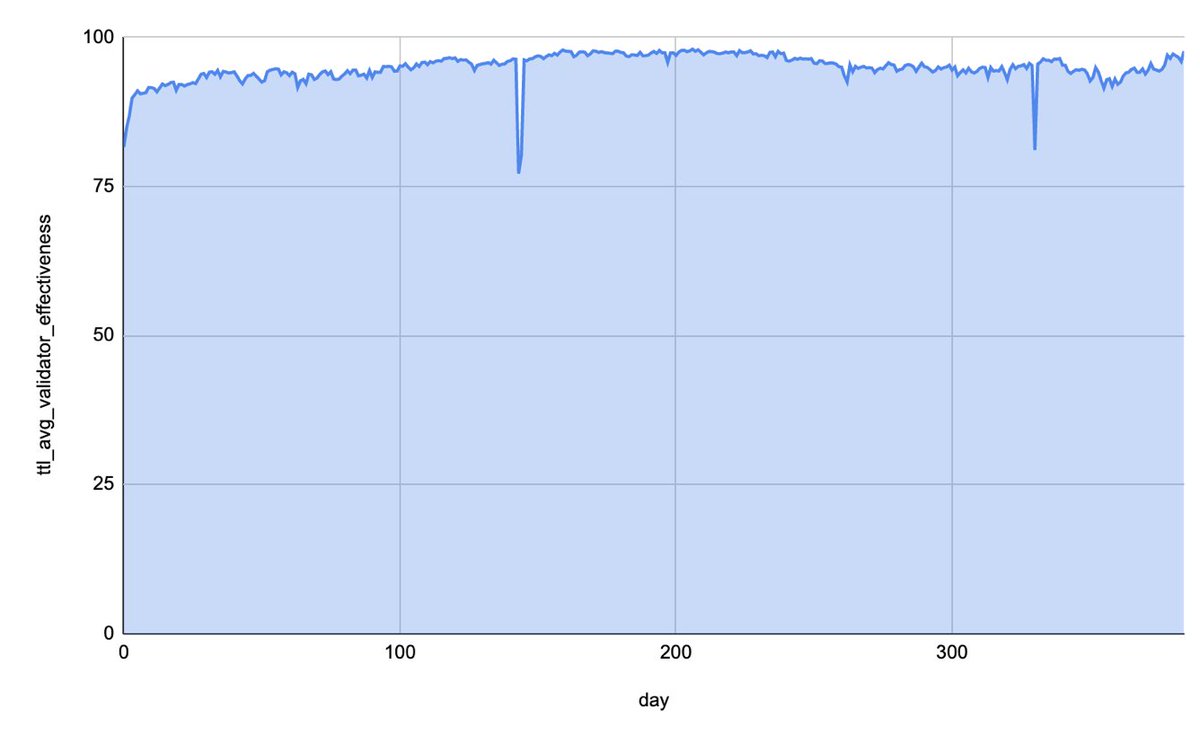

Will be very interesting to see how this behaves once validators are faced with reconciling more complex activity than just attestations.

Will be very interesting to see how this behaves once validators are faced with reconciling more complex activity than just attestations.

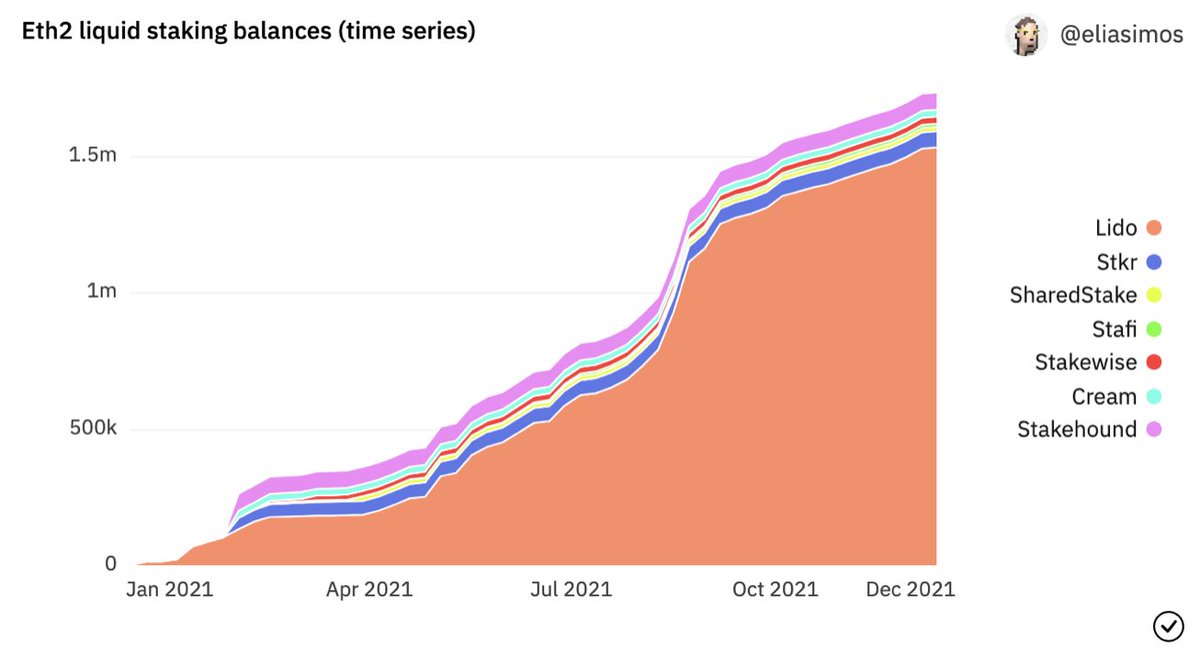

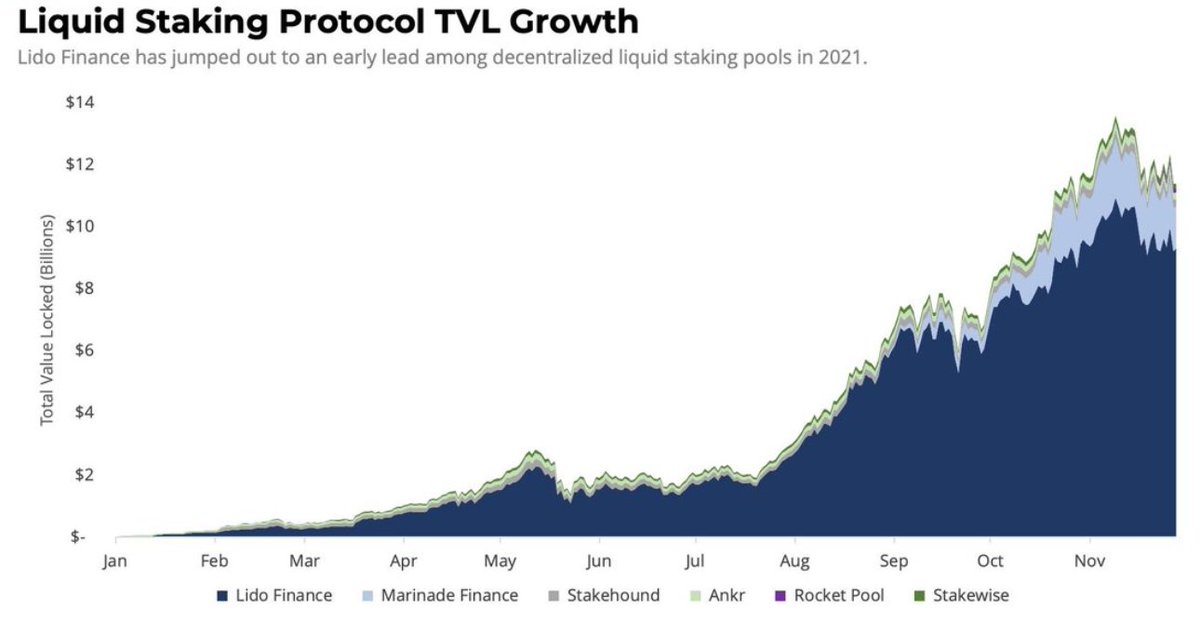

30/ Granted the Beacon Chain works with pure PoS and no delegations, liquid staking has taken off, solving a real pain point for users with smaller balances and offering insta-entry and exit for larger users.

Lido has been dominating the category.

Lido has been dominating the category.

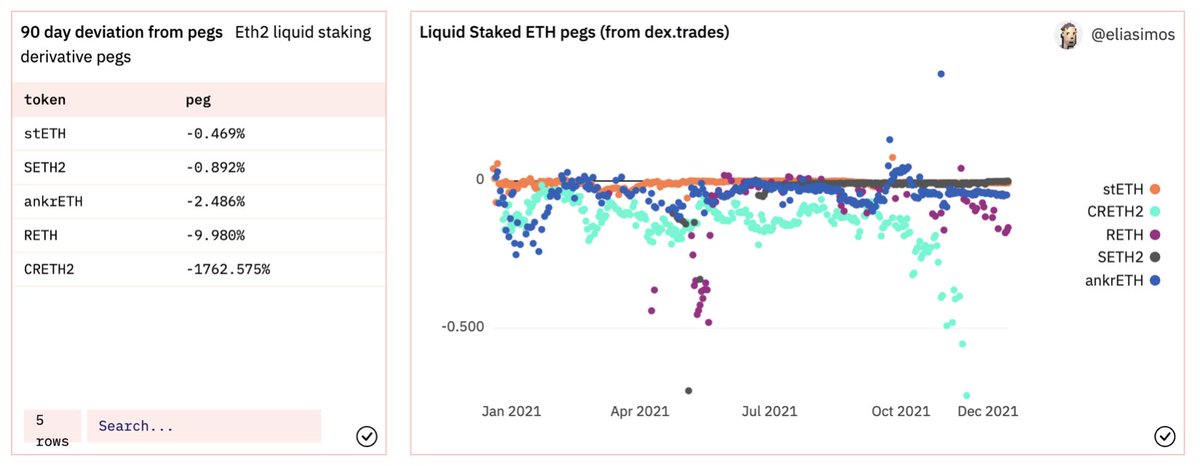

31/ This reflects not only in TVLs, but also in the way the derivative asset is behaving in relation to its peg.

Among the various competitors, stETH (Lido’s liquid staking derivative) has been holding the closest to ETH for the longest time.

Among the various competitors, stETH (Lido’s liquid staking derivative) has been holding the closest to ETH for the longest time.

32/ Liquid Staking is not exclusively an eth2 phenom. Lido has a large footprint on Terra, while liquid staking pools are appearing in a bunch of other proof of stake chains.

@meta_pool , @MarinadeFinance and @KaruraNetwork are only some examples.

Expect a lot more in 2022

@meta_pool , @MarinadeFinance and @KaruraNetwork are only some examples.

Expect a lot more in 2022

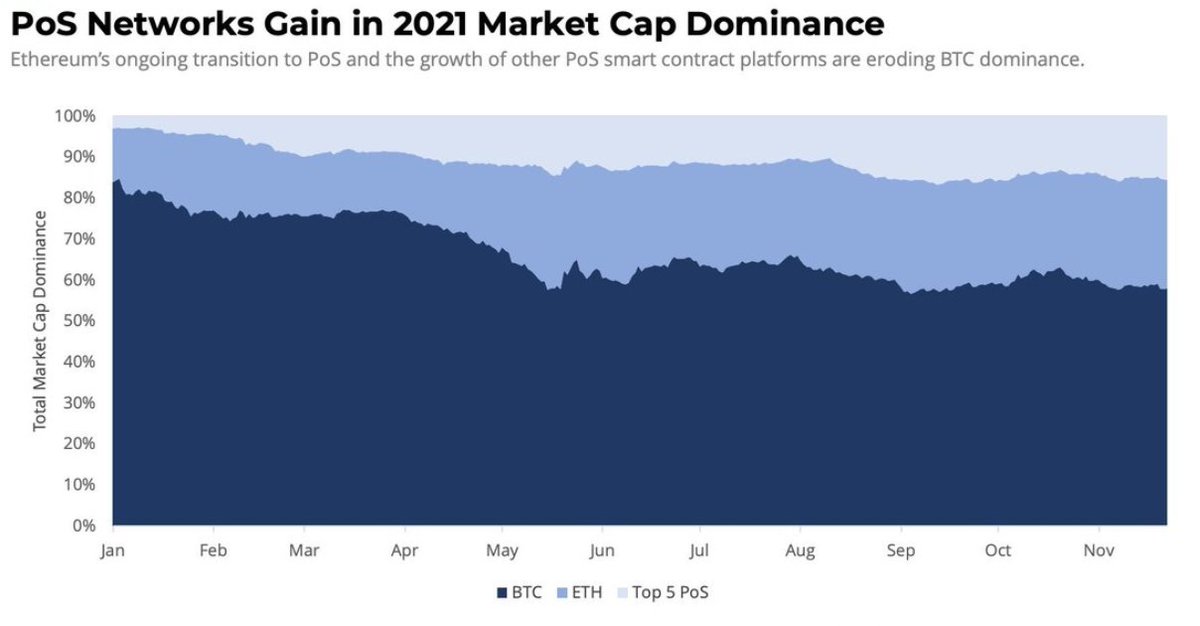

33/ Zooming out a bit, 2021 has been all about PoS protocols taking center stage.

From where I stand, the genie is out of the bottle. Most new networks are launching in PoS and some PoW (ETH, ZEC) are planning to transition to PoS.

PoS will be soon the defacto standard.

From where I stand, the genie is out of the bottle. Most new networks are launching in PoS and some PoW (ETH, ZEC) are planning to transition to PoS.

PoS will be soon the defacto standard.

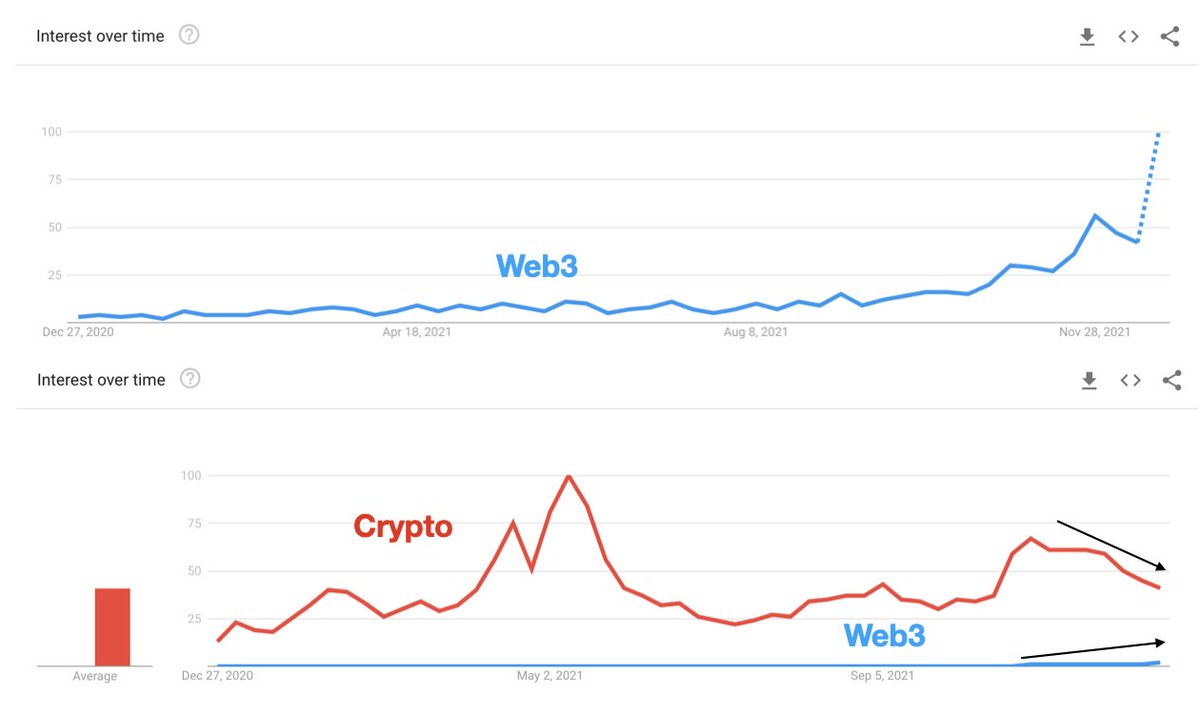

34/ Throughout all of 2021 the web3 narrative has been picking up steam, with interest in the term accelerating over Q4.

However, it looks like the world still knows web3 as…crypto.

The slope flip in the tail end of the year is something to pay attention to.

However, it looks like the world still knows web3 as…crypto.

The slope flip in the tail end of the year is something to pay attention to.

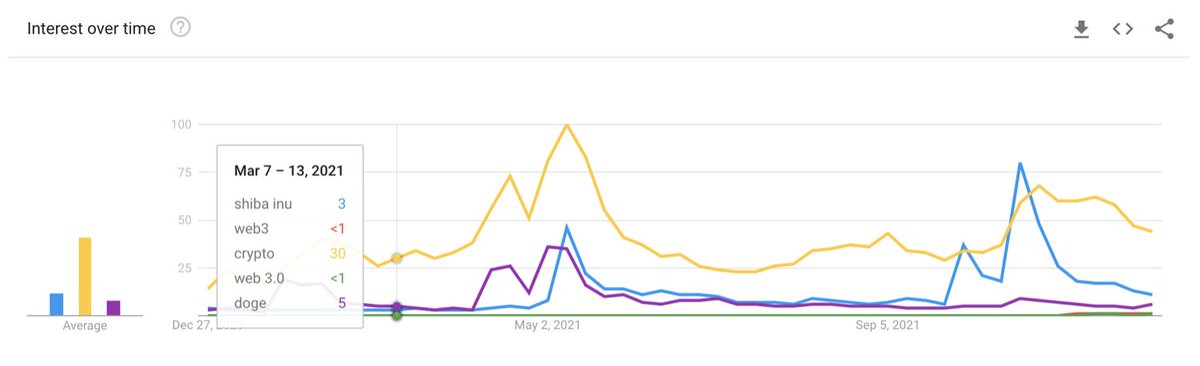

35/ On the subject of trending terms, it's worth noting that crypto’s dominance in mindshare as a term was briefly eclipsed by… $SHIB

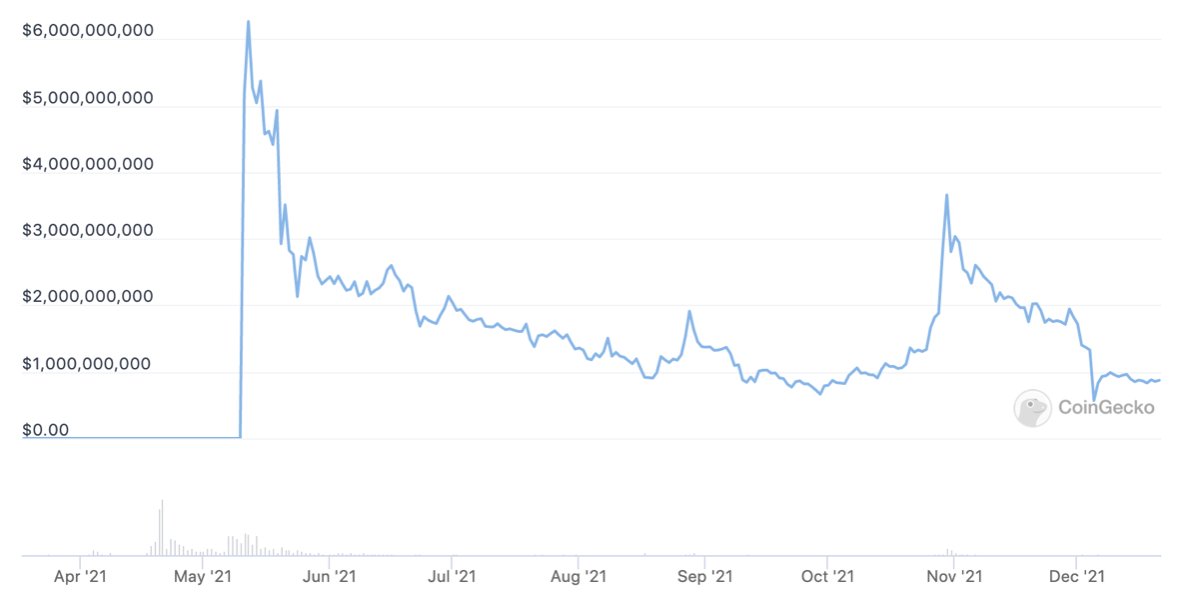

36/ Speaking of memecoins, SAFEMOON reached a $6B FDV, only to find its temporary resting place at $1B FDV.

2 things to glean from here; (i) people like the memecoins and (ii) nearly nobody looks at FDV.

That’s either your alpha or the bane of your existence dear reader.

2 things to glean from here; (i) people like the memecoins and (ii) nearly nobody looks at FDV.

That’s either your alpha or the bane of your existence dear reader.

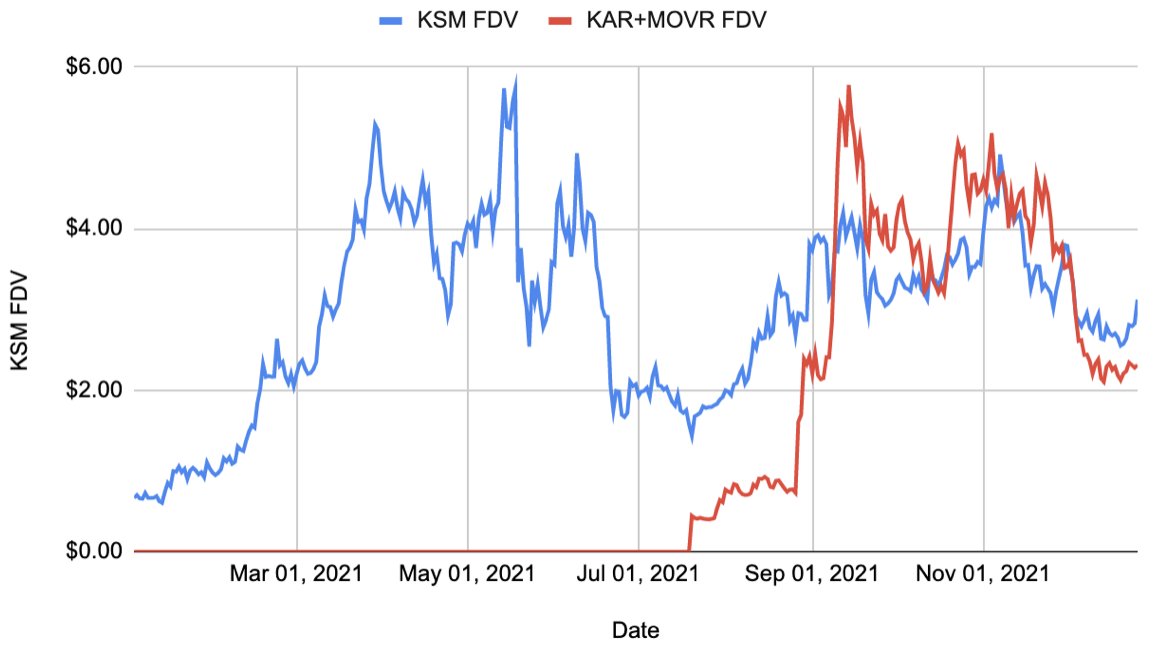

37/ Then again, I say this, but in the world of shared security it looks like the market is approaching FDVs with some modicum of sense.

The FDVs of Karura and Moonriver combined (the two largest Kusama parachains) have oscilated around the FDV of Kusama itself.

The FDVs of Karura and Moonriver combined (the two largest Kusama parachains) have oscilated around the FDV of Kusama itself.

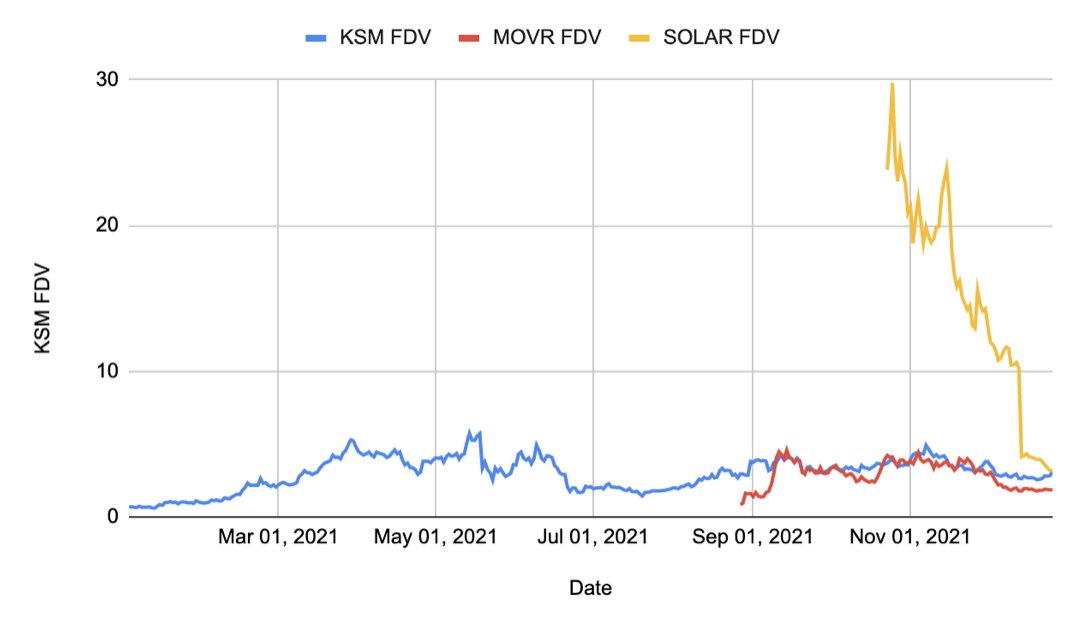

38/ Or…is it?! Solarbeam, the native DEX on Moonriver is valued almost equally to KSM’s FDV.

Obviously it's correcting sharply, but with more issuances coming online, should keep an eye on how much of a bellweather the L0 val becomes for vals of things built on top.

Obviously it's correcting sharply, but with more issuances coming online, should keep an eye on how much of a bellweather the L0 val becomes for vals of things built on top.

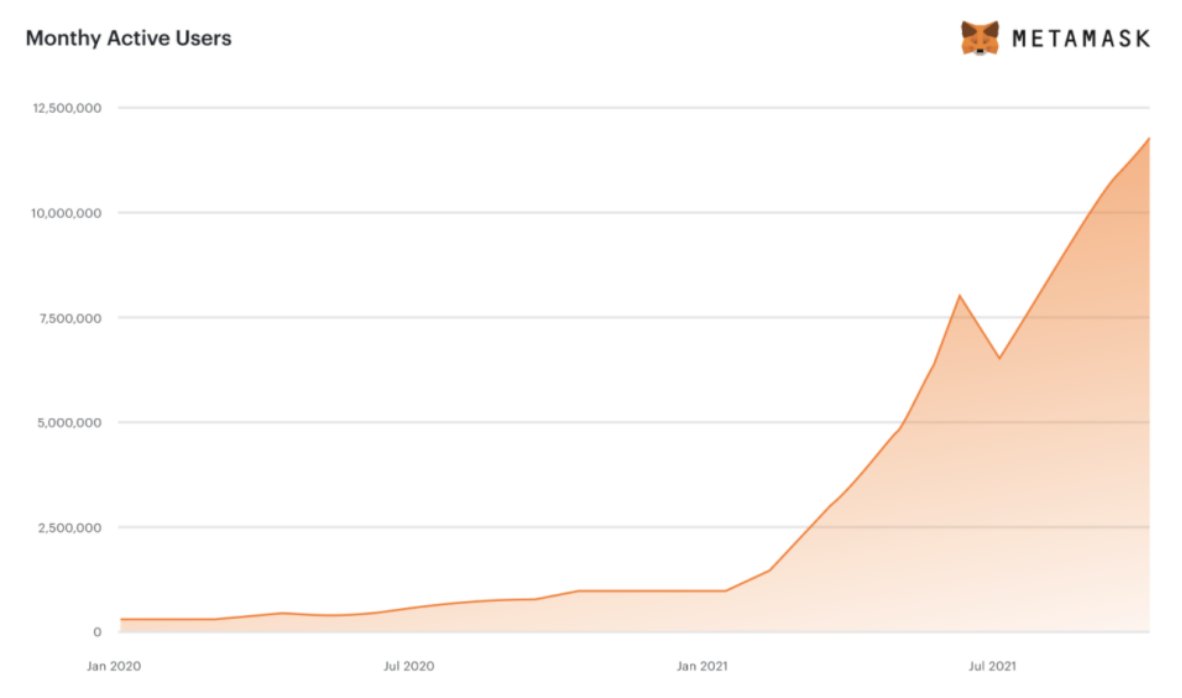

39/ Which ever way you cut it though, 2021 was a breakout year for web3/crypto.

The most interesting stat here is inarguably Metamask 10x’ing its user base by MAUs.

The most interesting stat here is inarguably Metamask 10x’ing its user base by MAUs.

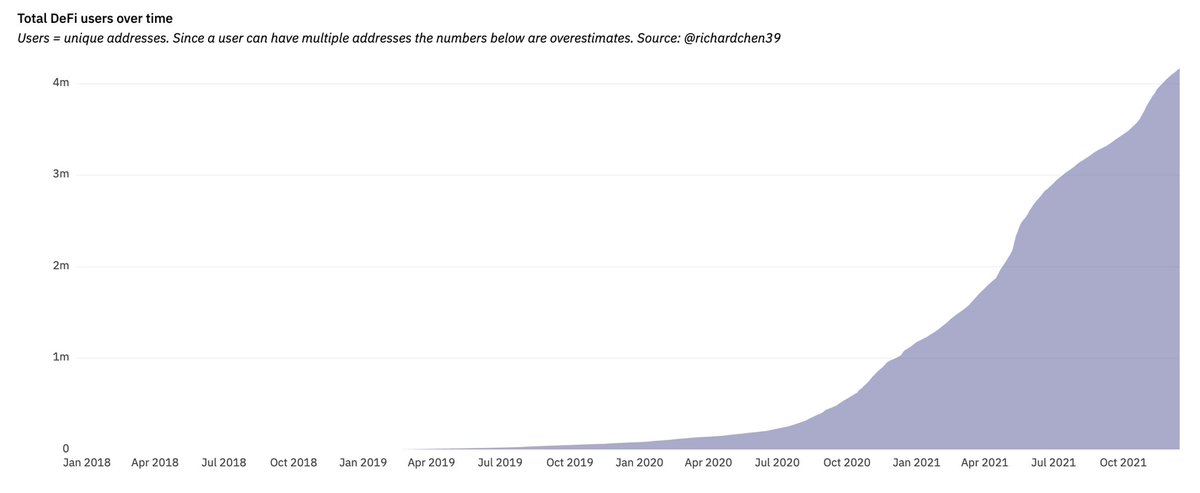

40/ And although DeFi fell out of favour in investors’ minds and portfolios, unique Ethereum addresses interacting with DeFi protocols 4x’ed.

Sure, there’s probably a lot of airdrop hunting and duplication involved, but this must mean something right?

Sure, there’s probably a lot of airdrop hunting and duplication involved, but this must mean something right?

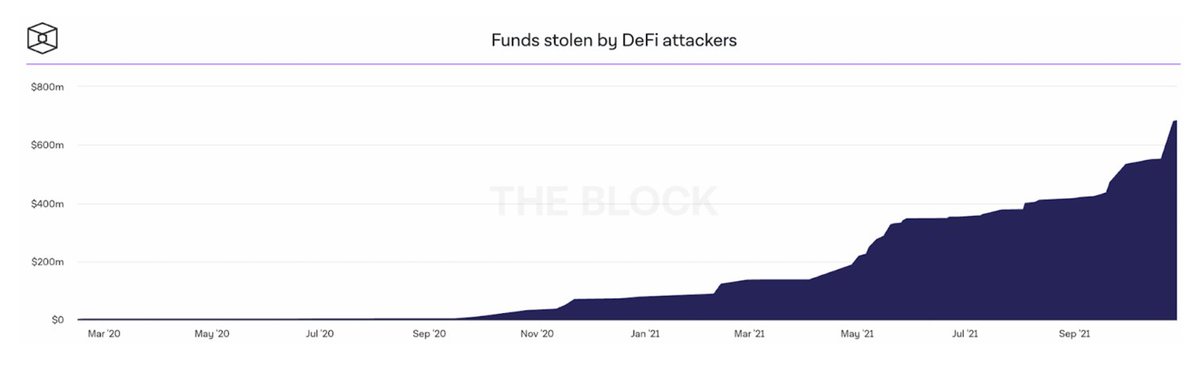

41/ But as those new users were enjoying the wonders of DeFi, they were also in for a fair bunch of unsavoury surprises.

Funds lost in DeFi hacks really reached escape velocity in 2021.

Remember new friends; farm safe @NexusMutual

Funds lost in DeFi hacks really reached escape velocity in 2021.

Remember new friends; farm safe @NexusMutual

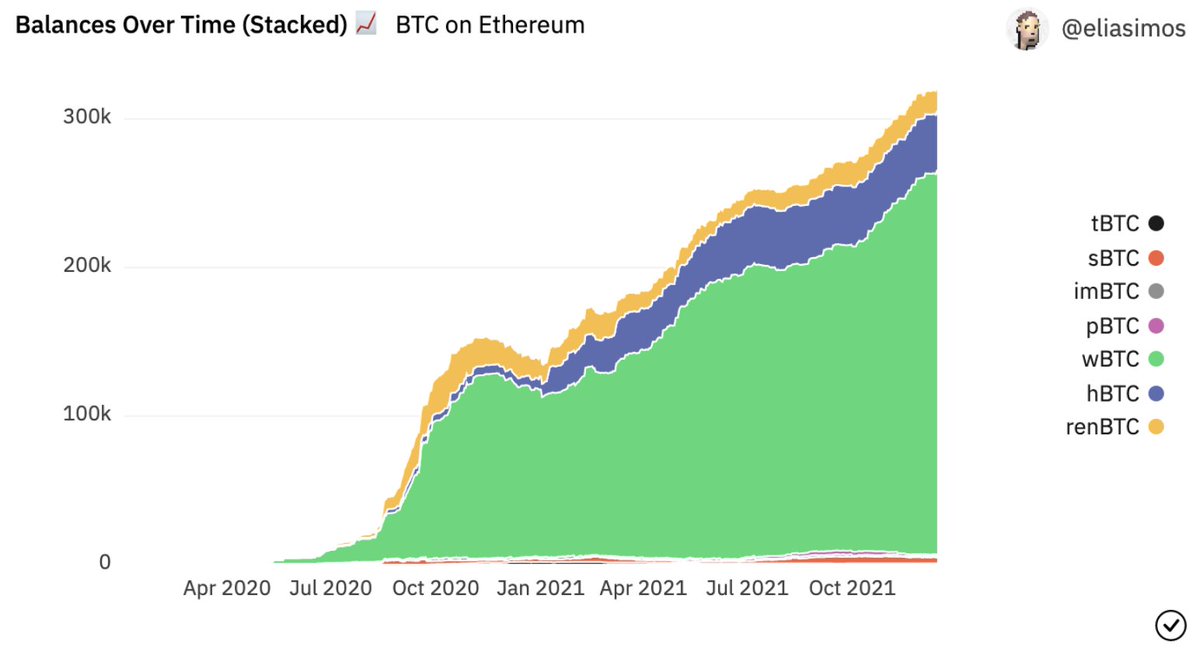

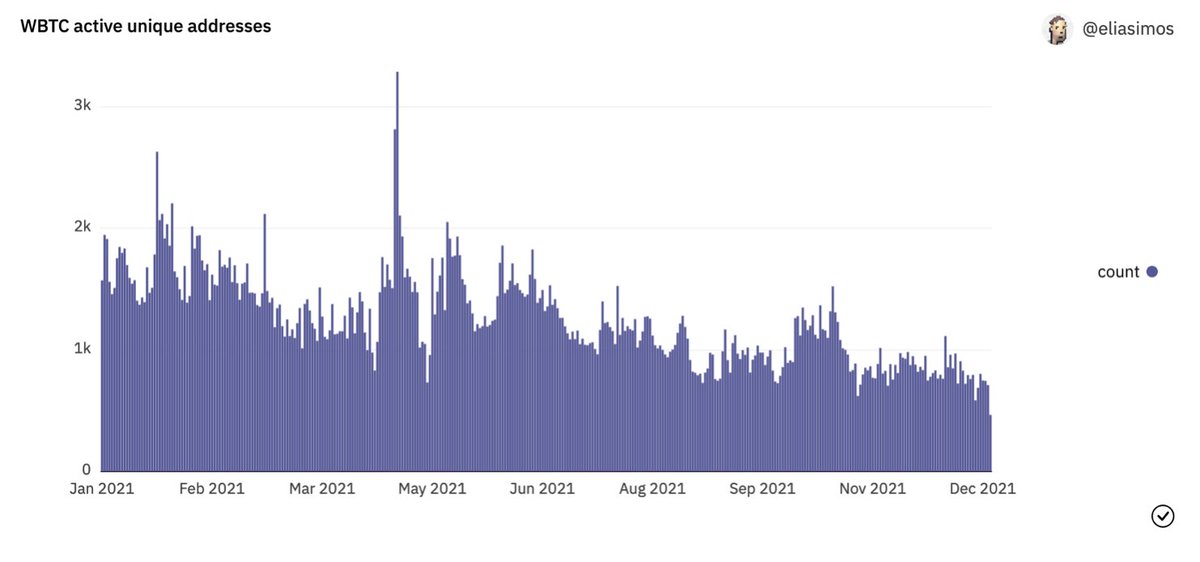

42/ WBTC on Ethereum continues to dominate the market for wrapped Bitcoin.

43/ And it’s pretty clear that the medium is used overwhelmingly for yield than it is for transactions.

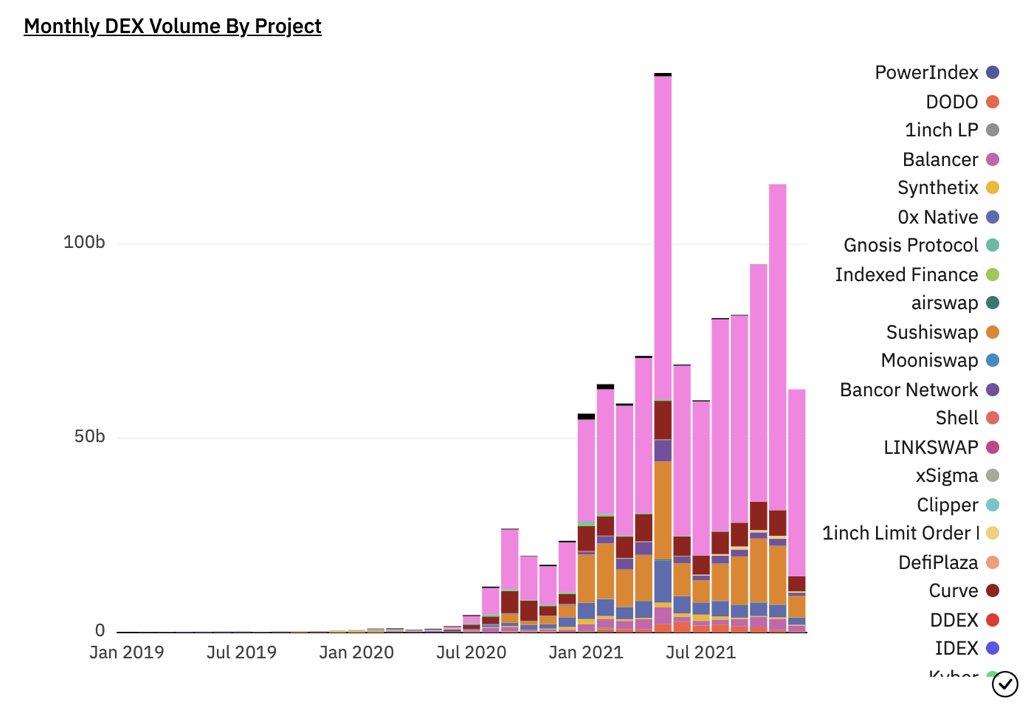

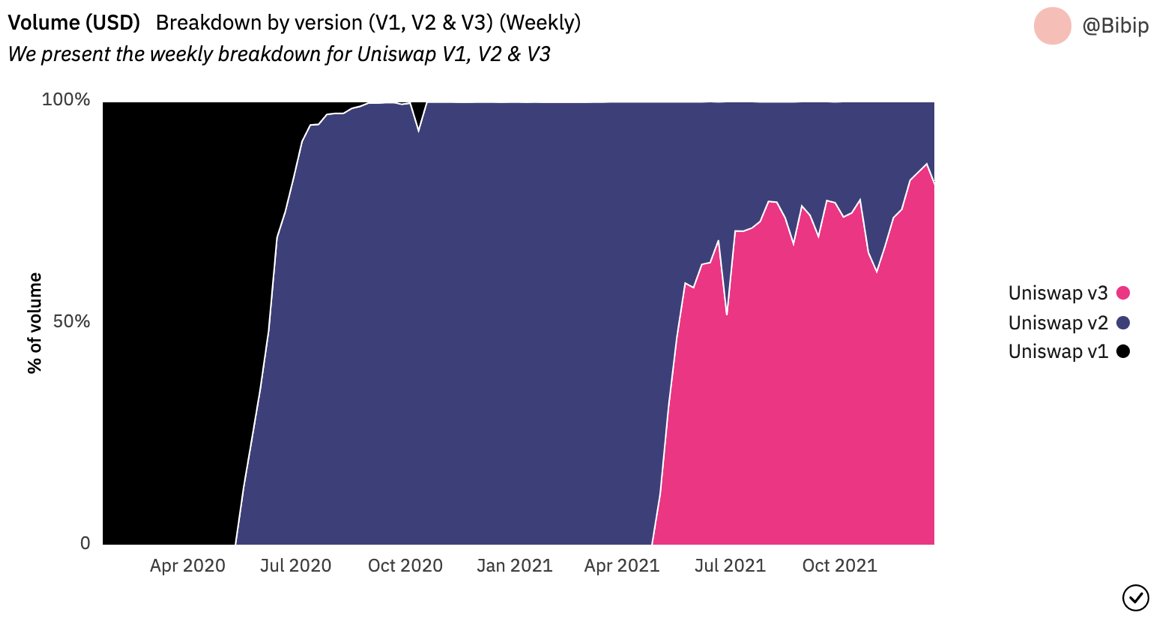

44/ DEX volumes continued their march up-and-to-the-right, with Uniswap and its many faces continuing to dominate.

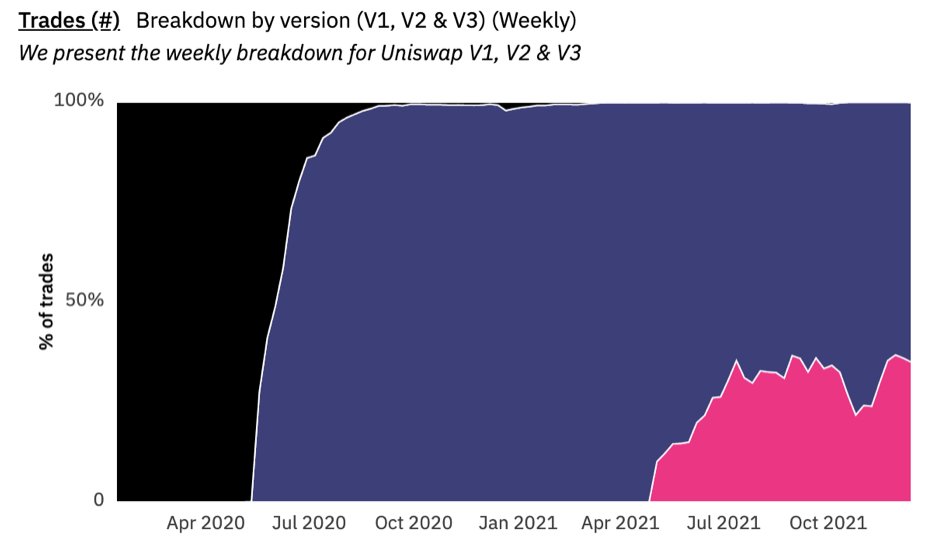

45/ Speaking of Uniswap, v3 was arguably one of the most innovative DeFi protocols to launch in 2021, introducing a whole lot of new functionality and capital efficiency into the system.

Yet its uptake hasn’t been as quick as v2’s, though it represents the majority of volume.

Yet its uptake hasn’t been as quick as v2’s, though it represents the majority of volume.

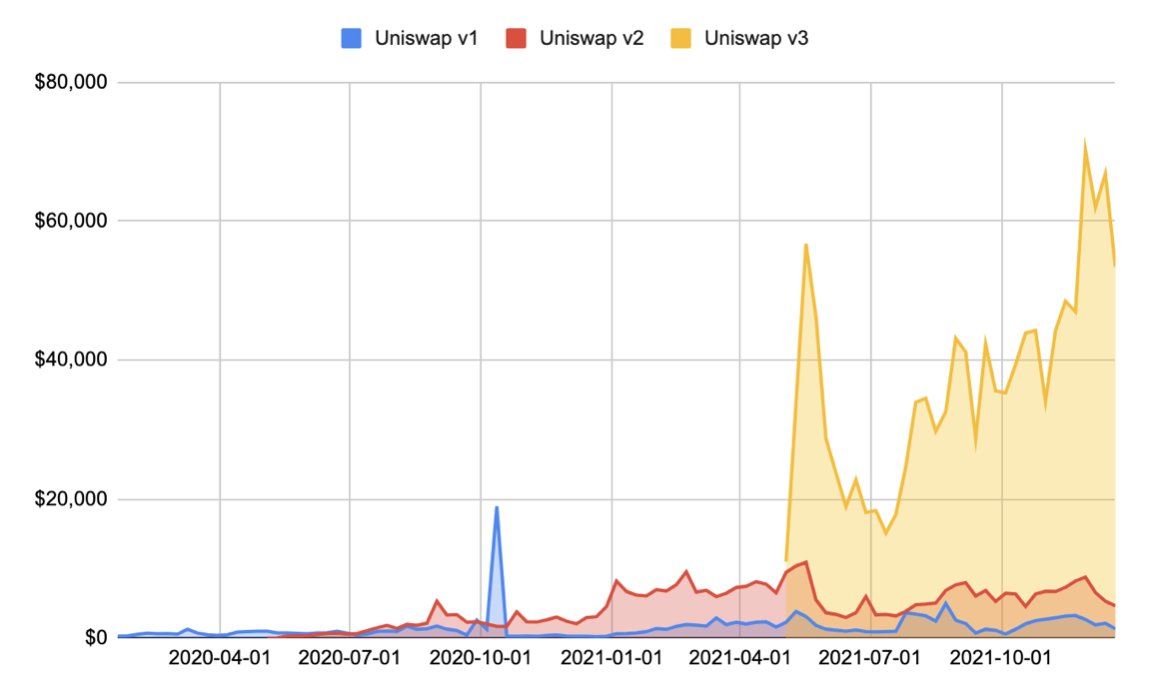

46/ It is clear that v3 is a protocol for pros. The average transaction size is ~30x higher than that in v2 reaching a whopping $60k average towards the end of the year.

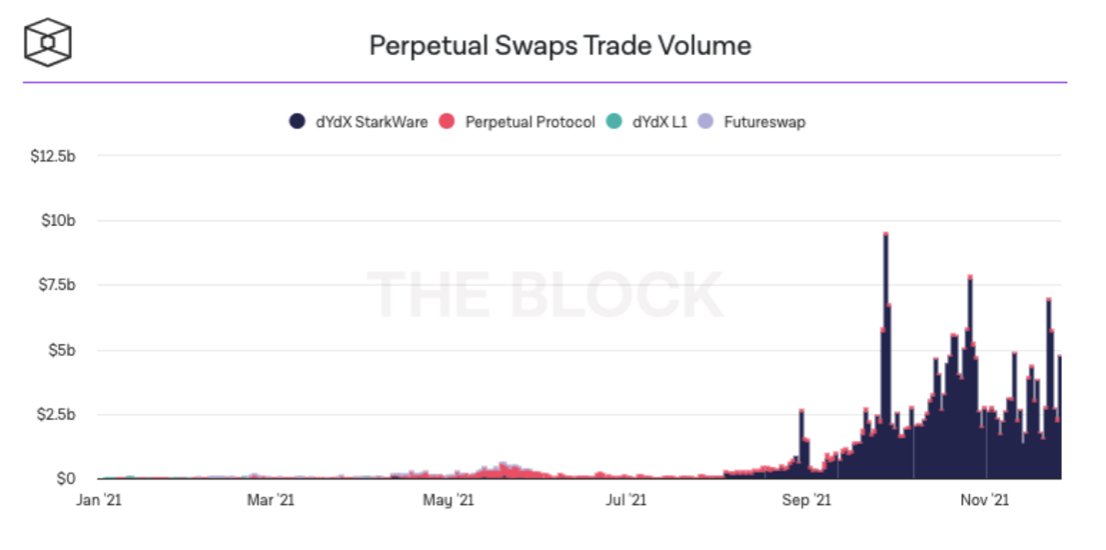

47/ The promise of on-chain derivatives started to shine through in 2021, with dydx’s StarkEx deployment showing that L2s can and most likely will help developers introduce a lot more computationally expensive applications to the universe of open web3.

Exciting stuff!

Exciting stuff!

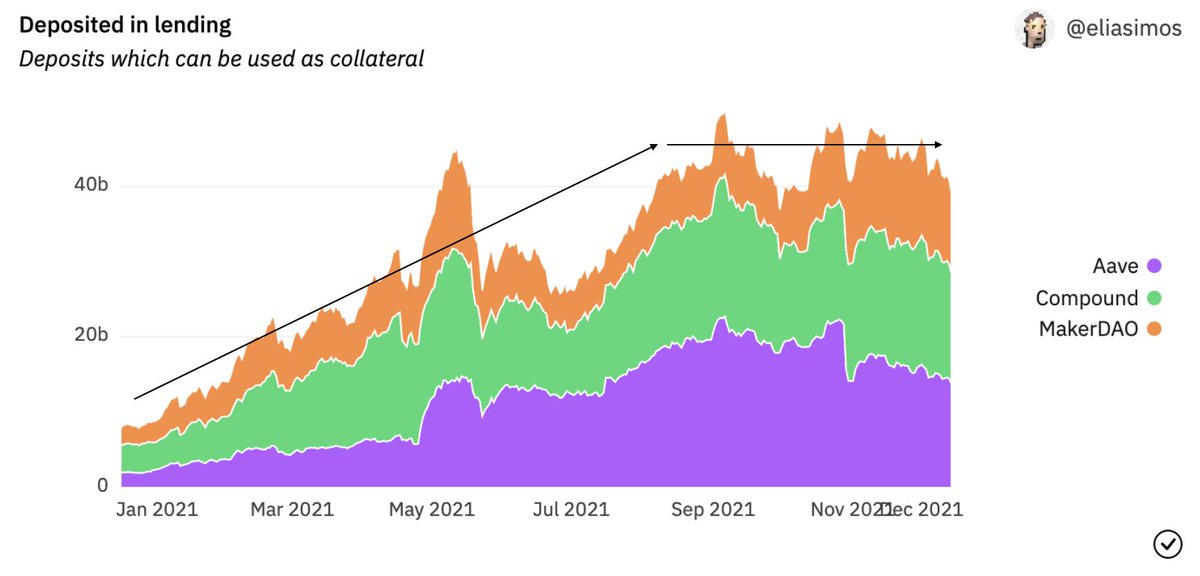

48/ Lending protocols on the other hand showed less explosive growth in 2021, and even less of it was attributable to asset deposits as opposed to growth in the price of assets vs the USD.

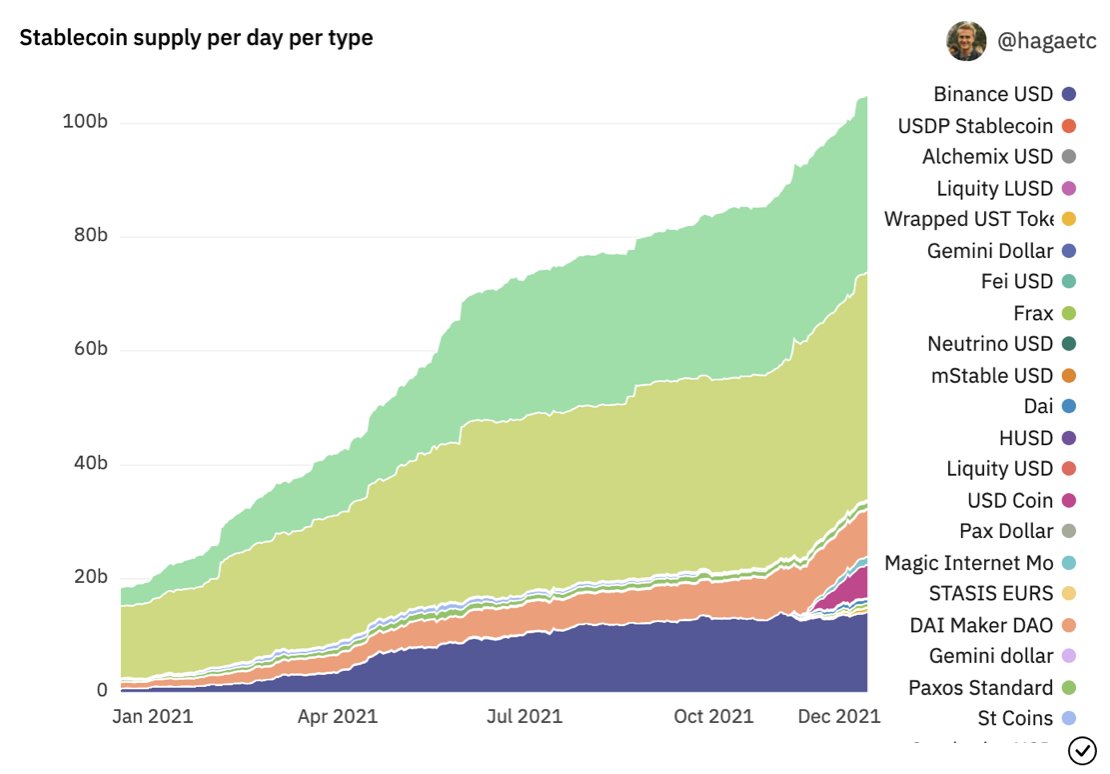

49/ Not the same can be said about stablecoins. The category on Ethereum alone grew 5x bringing increasingly more utility to the world of on-chain interactions.

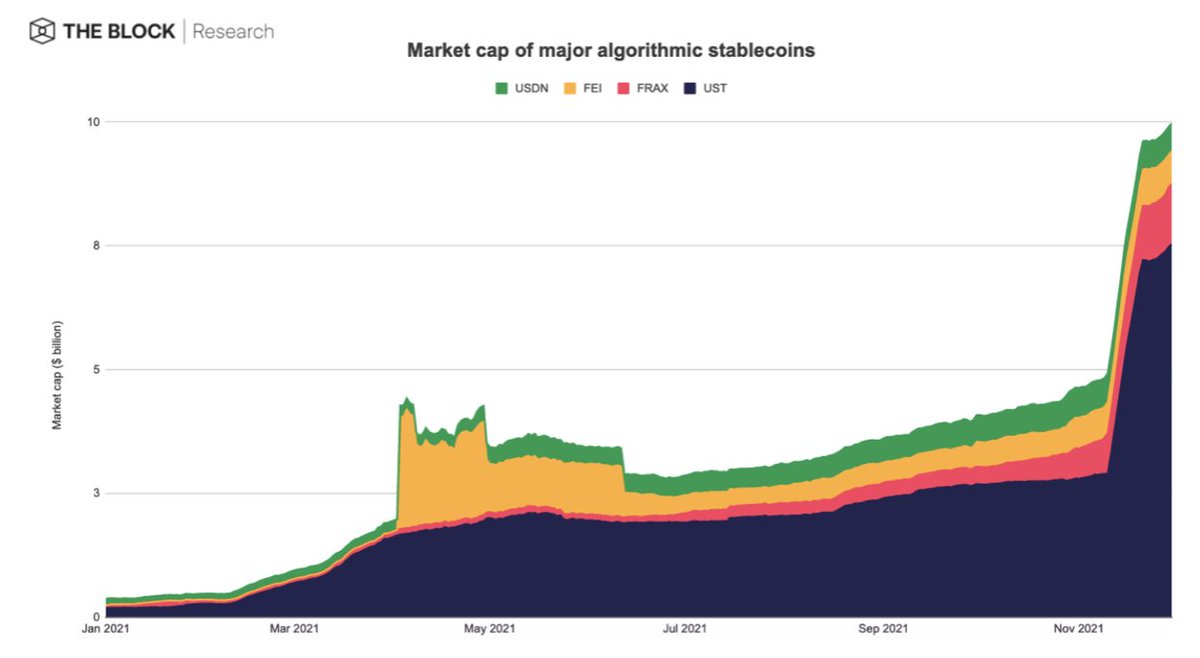

50/ And of course you can’t look at the category and not underline the fact that it’s been a breakout year for algo stablecoins, with $UST leading the charge.

After a series of experiments, algo models are getting more and more mature–though are yet to be tested in a bear.

After a series of experiments, algo models are getting more and more mature–though are yet to be tested in a bear.

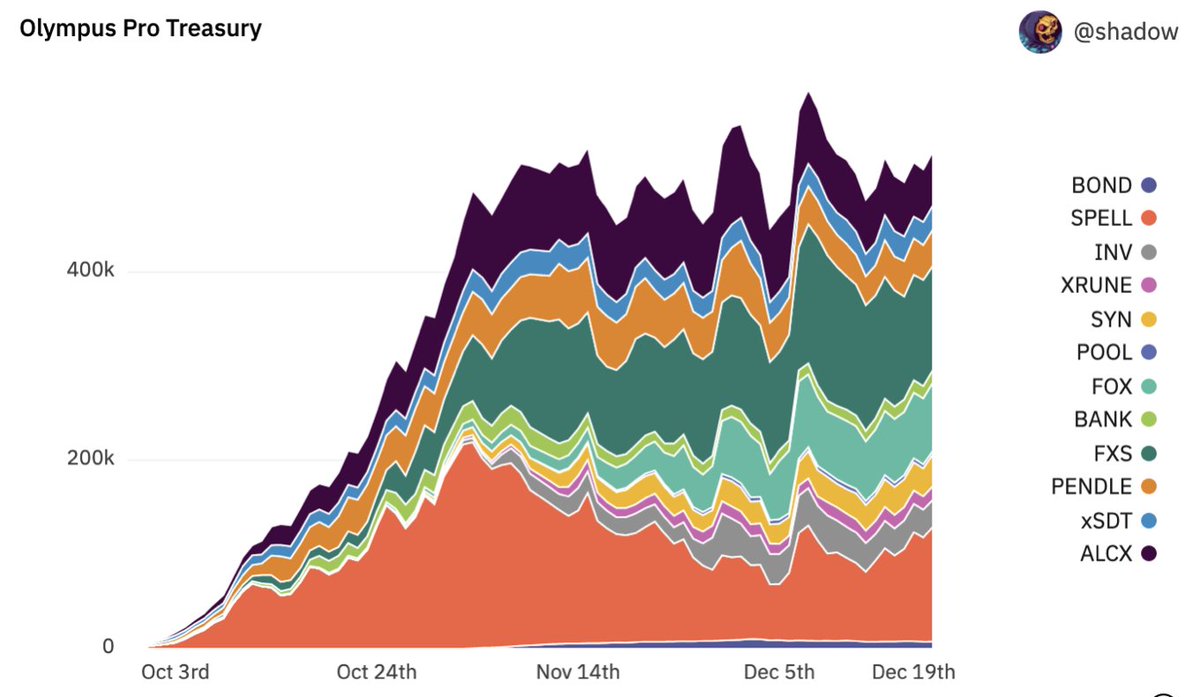

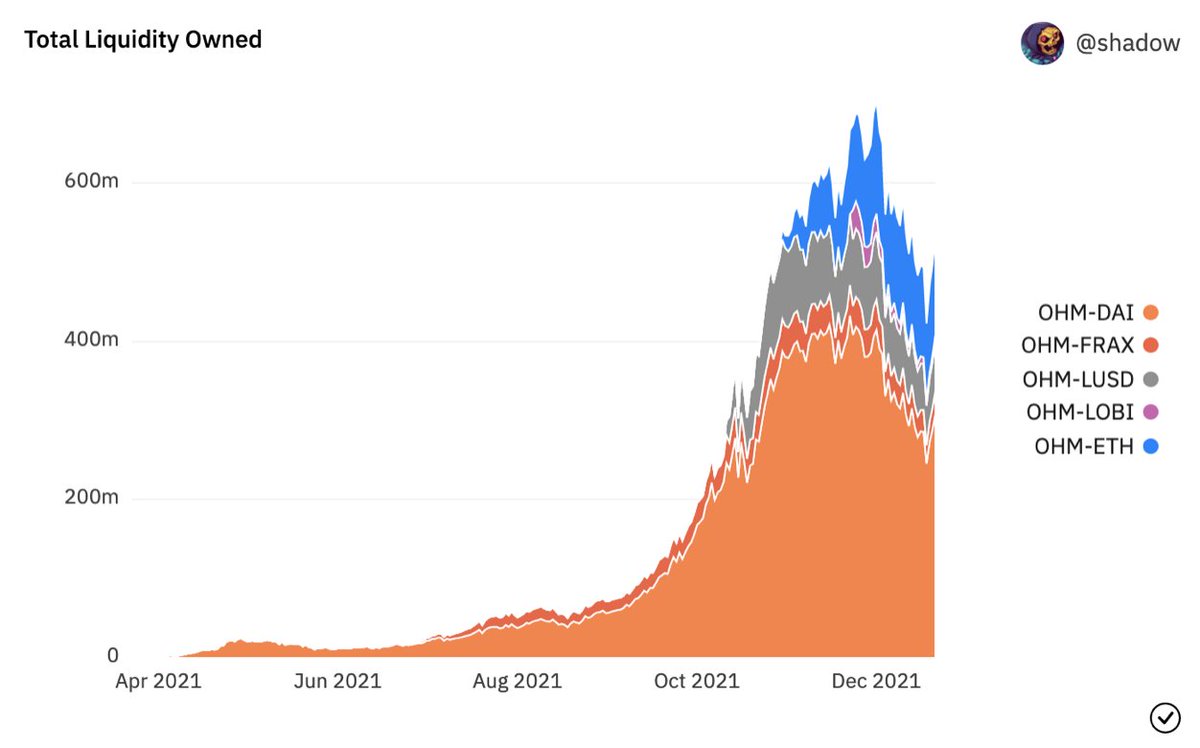

51/ Also can’t talk about DeFi without shining a light on OlympusDAO.

Complexity theater or huge innovations in core liquidity mechanisms, you be the judge of that.

To me it looks more the latter and less the former.

Complexity theater or huge innovations in core liquidity mechanisms, you be the judge of that.

To me it looks more the latter and less the former.

52/ Whichever way you cut it, you can’t ignore that the OHMies have built up a massive stockpile of stable assets backing OHM.

This is a clear nod to the fact that the massive treasuries that protocols have amassed in 2021 will play a big part in the happenings of 2022.

This is a clear nod to the fact that the massive treasuries that protocols have amassed in 2021 will play a big part in the happenings of 2022.

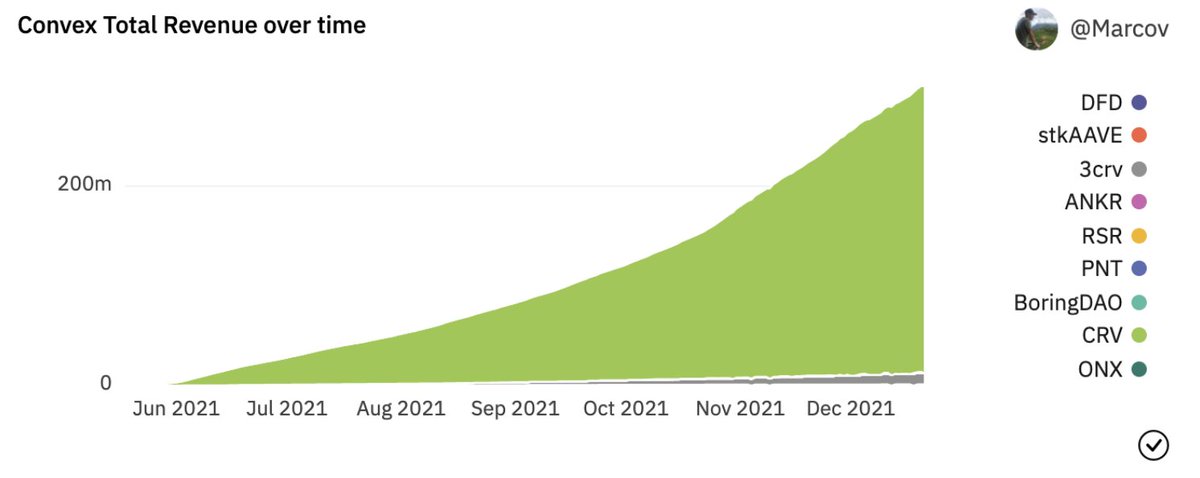

53/ Finally, you can’t look at DeFi in 2021 and not single out the rise and rise of Curve and Convex

These two protocols that are paving the way for “valuable” governance tokens.

Entities are scrambling to acquire CRV and CVX to get access to cheap(er) liquiditity incentives.

These two protocols that are paving the way for “valuable” governance tokens.

Entities are scrambling to acquire CRV and CVX to get access to cheap(er) liquiditity incentives.

54/ Ok, DeFi is cool. But you know what's cooler?

EN-EFF-TEES

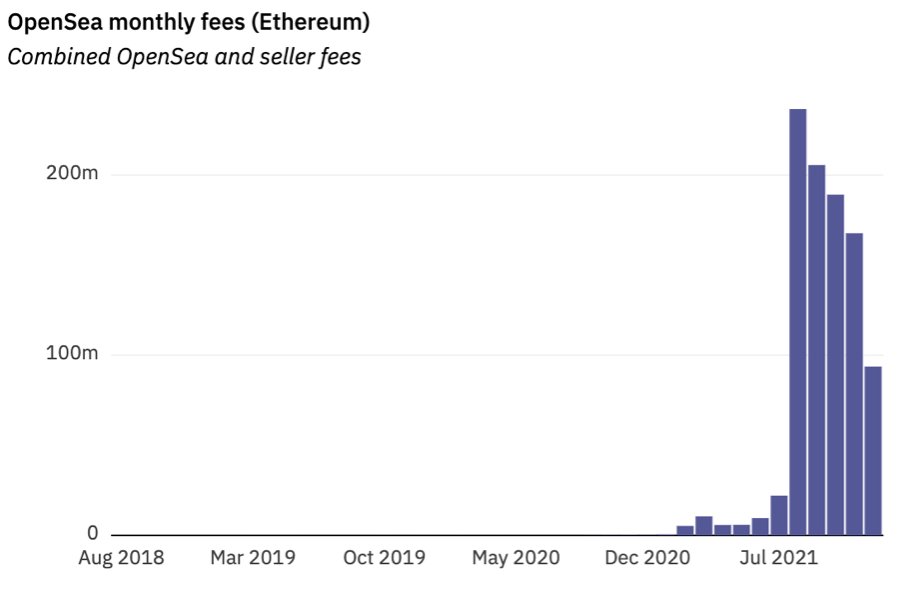

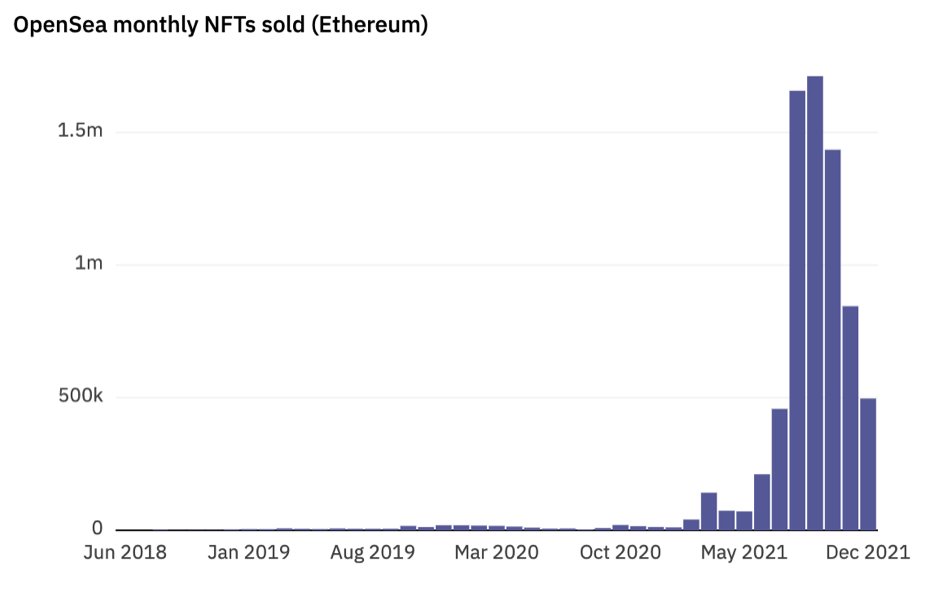

Probably the biggest story of web3 in 2021. Activity on the defacto dominant marketplace @OpenSea speaks for itself.

On the linear scale, activity from previous years isn’t even visible.

Big wow!

EN-EFF-TEES

Probably the biggest story of web3 in 2021. Activity on the defacto dominant marketplace @OpenSea speaks for itself.

On the linear scale, activity from previous years isn’t even visible.

Big wow!

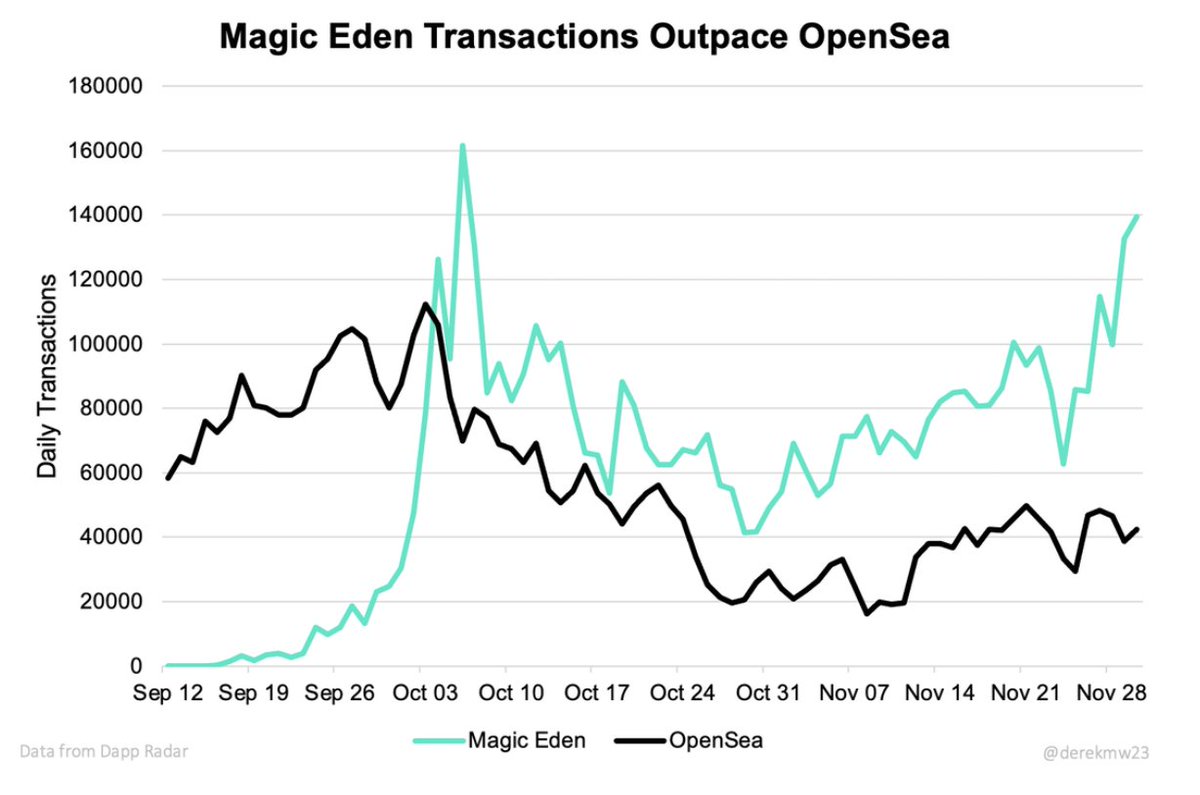

55/ NFT marketplaces are springing up on all kinds of chains, and the lower fee environments are allowing for different types of user activity than on Ethereum.

56/ Can't talk NFTs without mentioning the OGs.

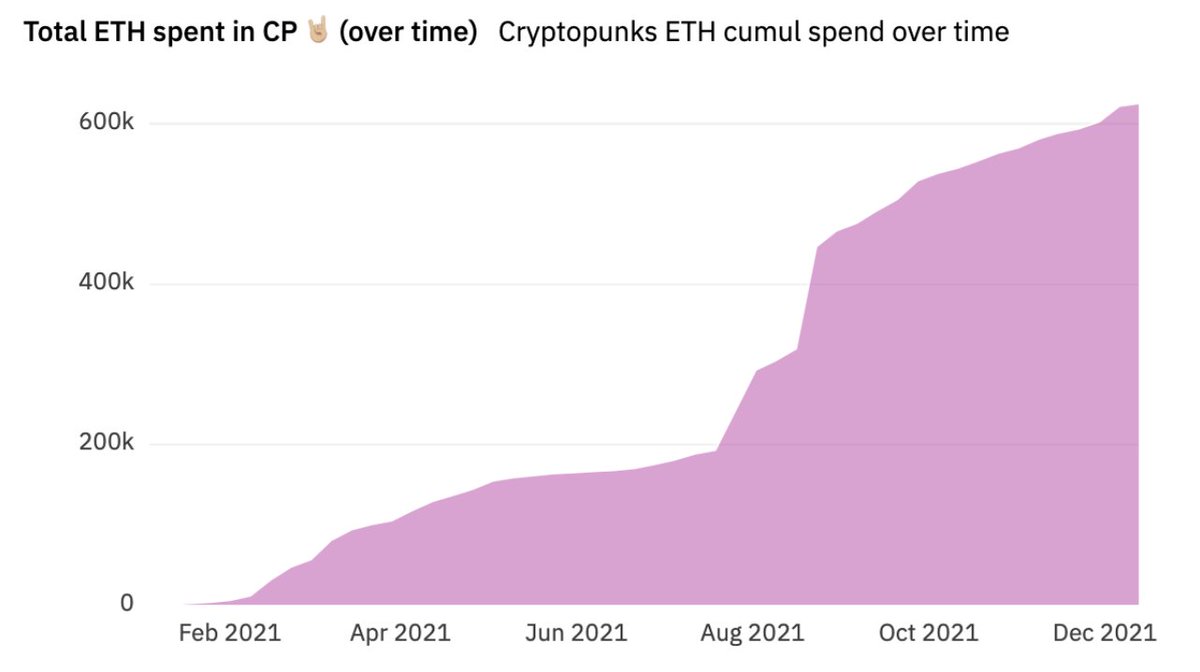

Total trade volume going through the CryptoPunk contract exploded to 60x to what it was in the beginning of 2021–reaching a total of 650k ETH.

This is not including private sales, wrapped Punk sales etc.

Total trade volume going through the CryptoPunk contract exploded to 60x to what it was in the beginning of 2021–reaching a total of 650k ETH.

This is not including private sales, wrapped Punk sales etc.

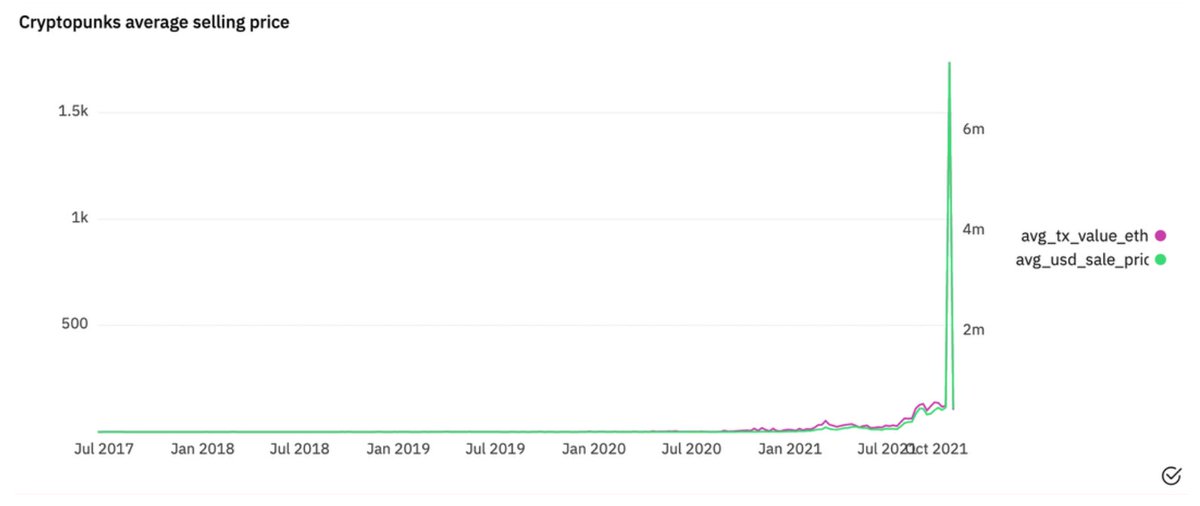

57/ Amongst all the sales that pushed CPs to these stratosperic highs, the most notable one was the flashloan powered wash sale of punk #9998 for~125K ETH or 500M USD.

An important token of how much subjectivity there is in on-chain data.

An important token of how much subjectivity there is in on-chain data.

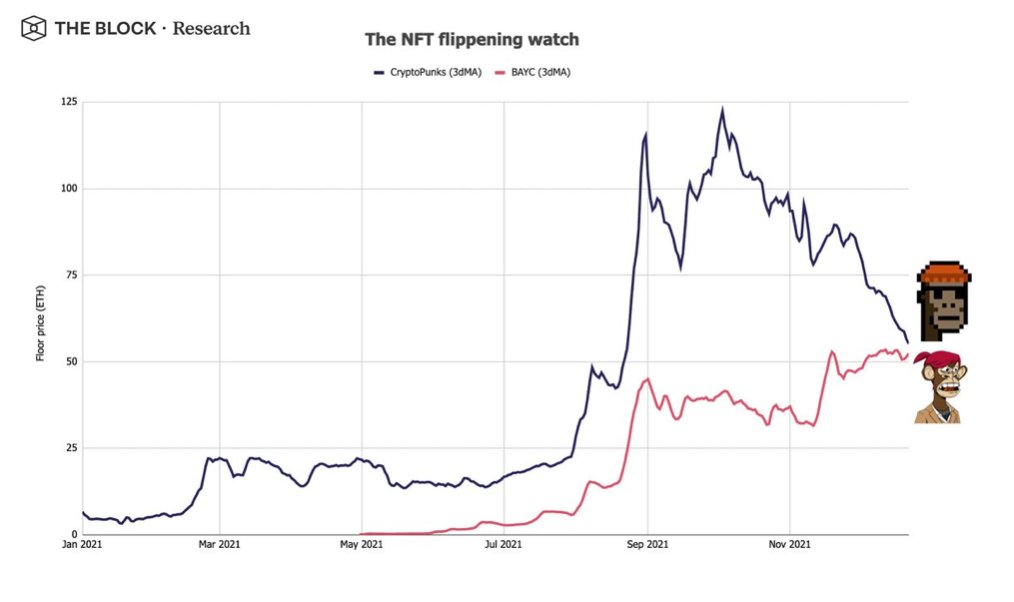

58/ The other big pfp NFT story this year was BAYC.

From niche community to a horde of celebrities and seed phrases given away, this story was rife of drama.

Not to mention that the Apes momentarily flipped Punks’ floor price.

From niche community to a horde of celebrities and seed phrases given away, this story was rife of drama.

Not to mention that the Apes momentarily flipped Punks’ floor price.

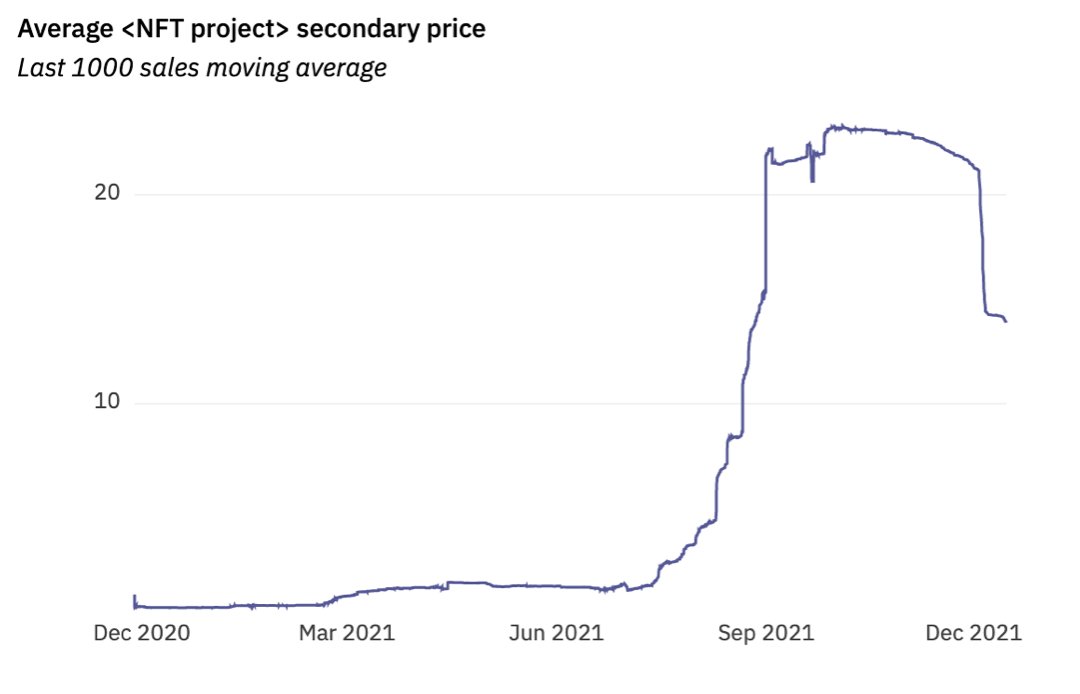

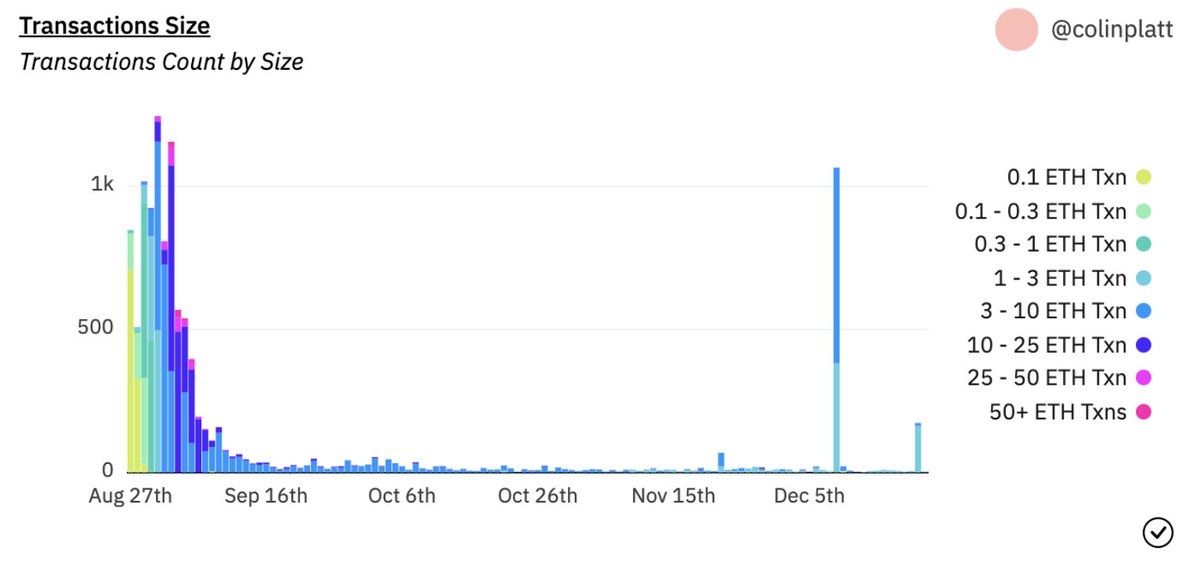

59/ In the heat of new issuances flooding the pfp game and old NFTs achieving billion dollar caps, the average price of NFTs changing hands went from sub 0.1 ETH to roughly 15 ETH.

60/ In my view the most interesting launch this year was Loot.

Sensation for a fortnight, touted the best thing after coca cola, breaking new ground in community generated lore etc etc

And then nothing…except for a bottom buyer in early December?!

Sensation for a fortnight, touted the best thing after coca cola, breaking new ground in community generated lore etc etc

And then nothing…except for a bottom buyer in early December?!

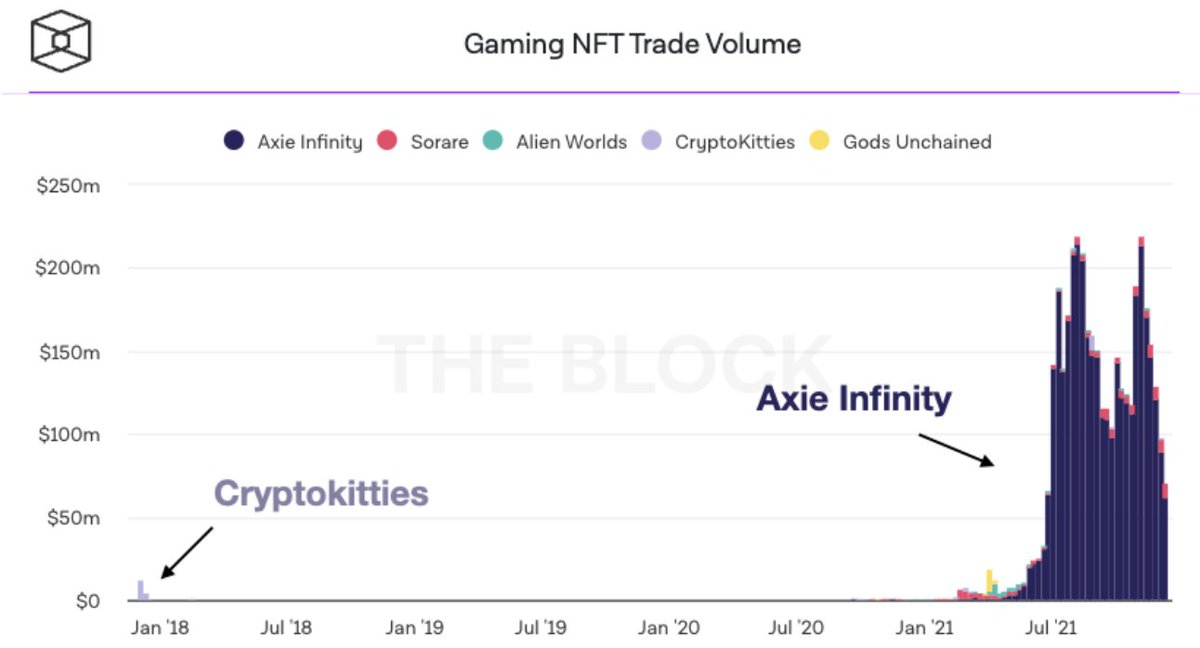

61/ Tangential to the NFT category, there's AxieInfinity.

This was another other breakout story in 2021, ushering the P2E and GameFi narratives to the fore.

Chaos ensued in in H2 as investors scrambled to get on the hype train rocketing valuations in the process.

This was another other breakout story in 2021, ushering the P2E and GameFi narratives to the fore.

Chaos ensued in in H2 as investors scrambled to get on the hype train rocketing valuations in the process.

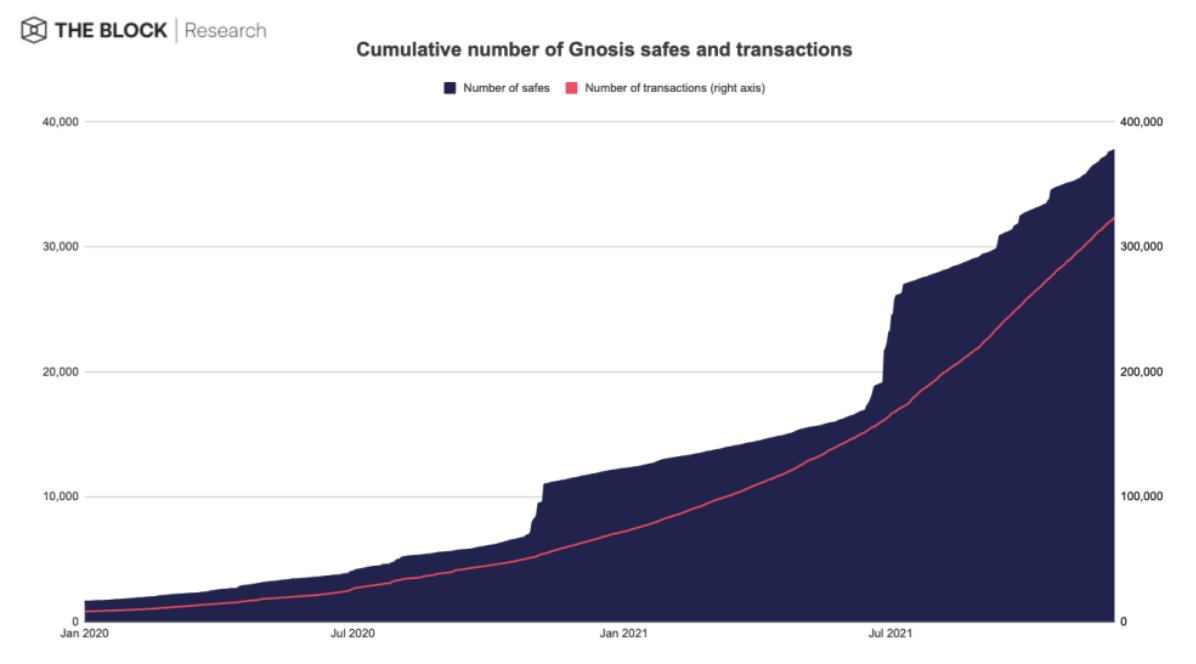

62/ Underpinning a lot of the activity discussed in this thread, is of course, DAOs.

The best stat I could find here is activity around the Gnosis Safe, arguably one of the cornerstone DAO building blocks.

3x in number of Safes and transactions executed in 2021.

The best stat I could find here is activity around the Gnosis Safe, arguably one of the cornerstone DAO building blocks.

3x in number of Safes and transactions executed in 2021.

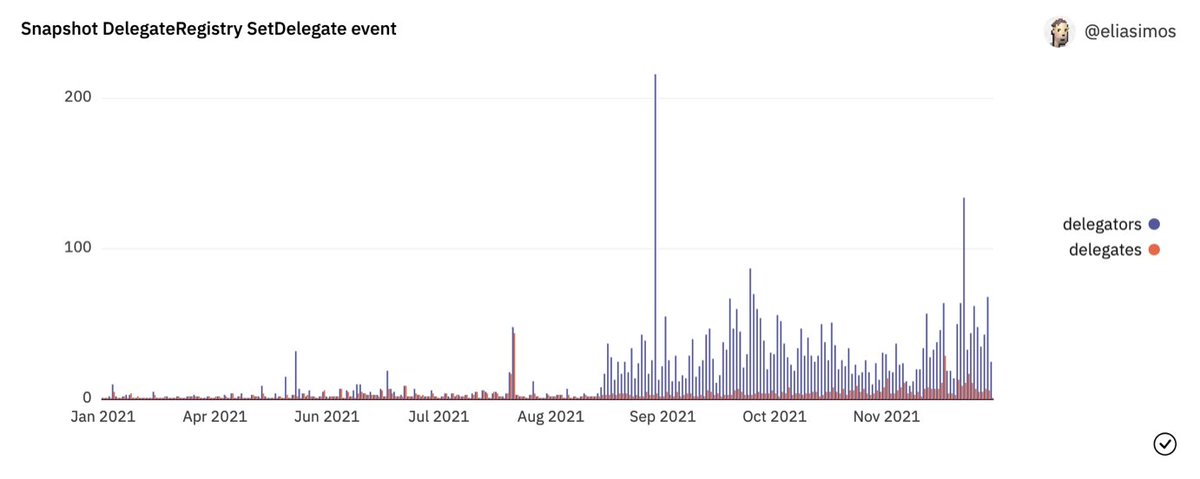

63/ The other cornerstone product for DAOs is Snapshot–a tool that helps DAOs execute off-chain votes with on-chain verification.

Activity on Snapshot has been clearly picking up since September on delegation actions, both as far as delegates and delegators go.

Activity on Snapshot has been clearly picking up since September on delegation actions, both as far as delegates and delegators go.

64/ One of the most interesting DAO launches in 2021 was the ENS DAO.

Interesting because it captures both the DAO trend, but also captures an important boostrap mechanism available to builders in web3;

the retroactive token airdrop

Interesting because it captures both the DAO trend, but also captures an important boostrap mechanism available to builders in web3;

the retroactive token airdrop

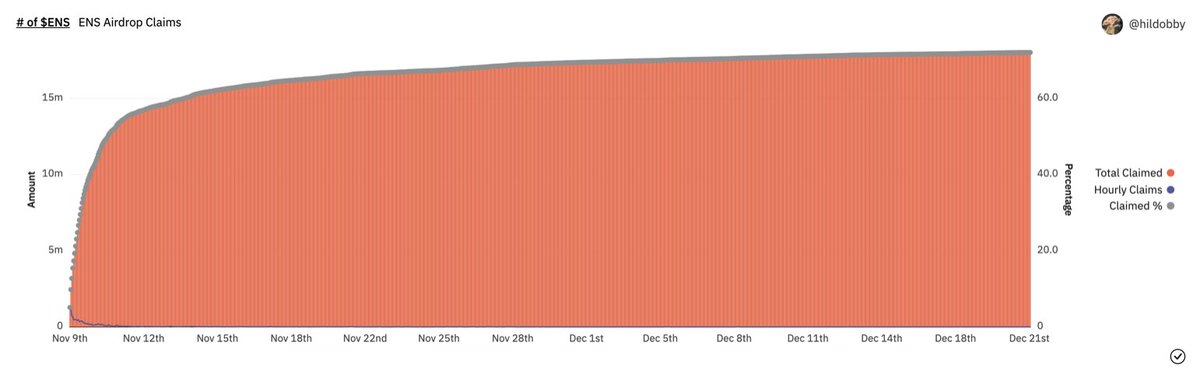

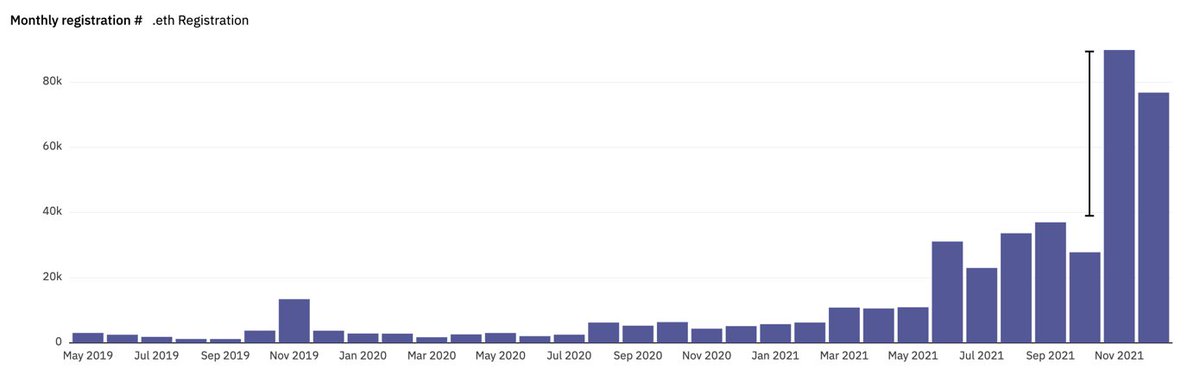

65/ The ENS dropped a whole lot of responsibility on its user base sometime in November 2021.

Soon thereafter registrations of .eth’s proceeded to more than double benchamarked on the previous 5 month average.

Some bootstrapping that is.

Soon thereafter registrations of .eth’s proceeded to more than double benchamarked on the previous 5 month average.

Some bootstrapping that is.

66/ As registrations of .eth’s ramped significantly, so did revenue for the newly minted ENS DAO Treasury.

The Treasury collected as much ETH in 2 months as it did in the remainder months in 2021 combined.

Testament to how much a well orchestrated airdrop can move the needle.

The Treasury collected as much ETH in 2 months as it did in the remainder months in 2021 combined.

Testament to how much a well orchestrated airdrop can move the needle.

67/ So where does all of this leave us?

2021 opened up new possibilities for web3 developers. Value is slowly moving towards the app layer, and at the same time new needs are emerging in the infra layer.

And there's a ton of cash and tokens to fund new protocols and products.

2021 opened up new possibilities for web3 developers. Value is slowly moving towards the app layer, and at the same time new needs are emerging in the infra layer.

And there's a ton of cash and tokens to fund new protocols and products.

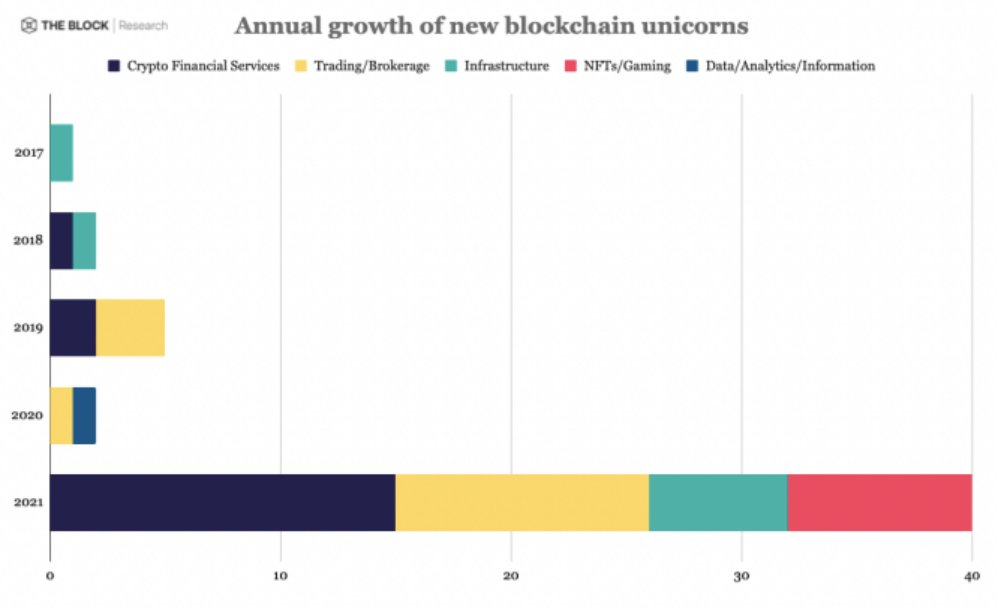

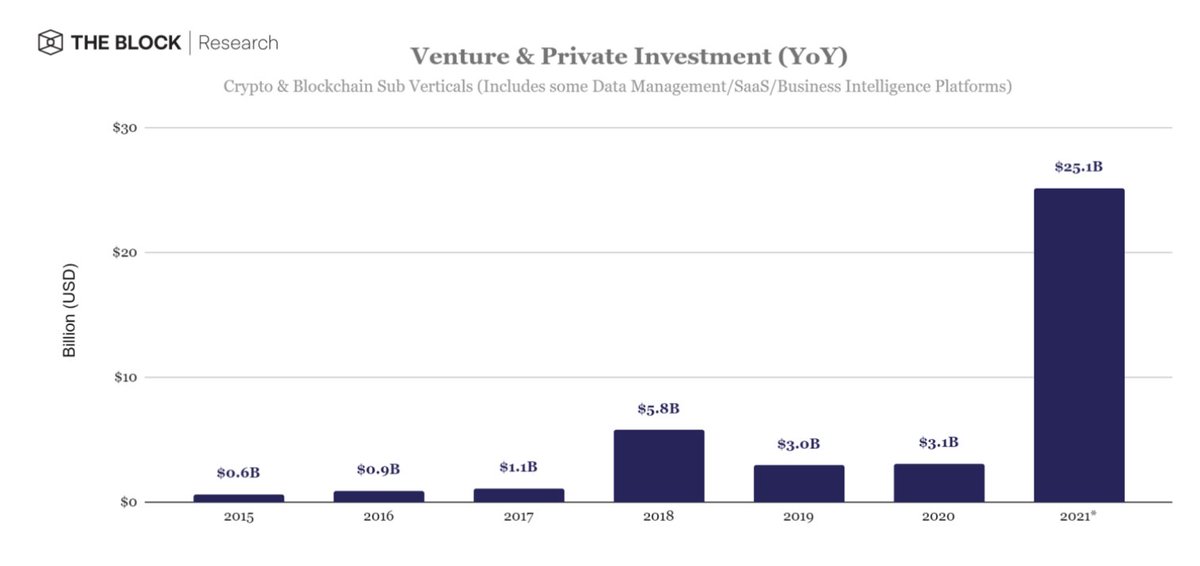

68/ 2021 was truly a breakout year for crypto/web3 minting a record number of new unicorns.

This is what adoption looks like folks.

This is what adoption looks like folks.

69/ And with heaps of venture money poured into Web3 and a great talent migration under way, 2022 is looking mighty fine.

Unless macro rugs us.

My 2c: stay healthy and learn to love the tech and the great long term.

We are winning this.

{fin}

Unless macro rugs us.

My 2c: stay healthy and learn to love the tech and the great long term.

We are winning this.

{fin}

Loading suggestions...