Saregama Antithesis:

A thread (1/18)

A thread (1/18)

From May, 2021, I started tracking Saregama and business model was explained in this thread.

(2/18)

(2/18)

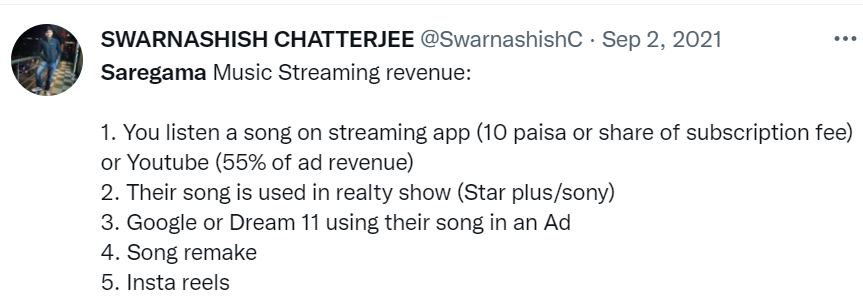

In current thread, only music streaming business will be discussed. In my opinion it has two sub division.

1. Existing Music IP, a great business.

2. New music acquisitions, maybe not a great one.

(3/18)

1. Existing Music IP, a great business.

2. New music acquisitions, maybe not a great one.

(3/18)

1.Existing music IP: The library of 130k songs is literally cash printing engine and by each passing year return on original invested capital is increasing.

Basically with easier availability of data & cheaper Smartphone, number of users listening to music is flourishing

(4/18)

Basically with easier availability of data & cheaper Smartphone, number of users listening to music is flourishing

(4/18)

These cash flow along with external capital is being invested to acquire new music

2. New music acquisitions: Average Payback period is five years which means if a song is acquired with Rs 100, within first 5 years it will make cumulative operating cash of Rs 100.

(5/18)

2. New music acquisitions: Average Payback period is five years which means if a song is acquired with Rs 100, within first 5 years it will make cumulative operating cash of Rs 100.

(5/18)

Imagine a good manufacturing business with 20% ROE (assuming no inflation and no taxation).

Invested Capital: Rs 100

Net Profit: Rs 20

Depreciation: Rs 5

Operating cash flow = 20 + 5 =25

Maintenance capex = Rs 5 (Zero inflation scenario)

Free cash flow = 25 – 5 =20

(6/18)

Invested Capital: Rs 100

Net Profit: Rs 20

Depreciation: Rs 5

Operating cash flow = 20 + 5 =25

Maintenance capex = Rs 5 (Zero inflation scenario)

Free cash flow = 25 – 5 =20

(6/18)

This Rs 20 cr free cash flow will be consistent for each year and payback period will also be 5 years. First 5 years cumulative free cash flow = Invested capital = Rs 100.

(7/18)

(7/18)

Now For Saregama, Cumulative operating cash flow for first five years Rs 100.

But the catch is (MOST IMPORTANT) it is not Rs 20 each year. Popularity of a new song (it is not evergreen RD Barman retro music) decreases by each year.

(8/18)

But the catch is (MOST IMPORTANT) it is not Rs 20 each year. Popularity of a new song (it is not evergreen RD Barman retro music) decreases by each year.

(8/18)

No one listens to "Dhoom Machale" now and in the same way popularity of current favourites will be reducing by 2025.

The cash flow distribution is asymmetric and maybe first yr they earn Rs 50, 2nd yr Rs 25, 3rd yr Rs 10, 4th yr Rs 9 and 5th yr Rs 6 (Don't have data)

(9/18)

The cash flow distribution is asymmetric and maybe first yr they earn Rs 50, 2nd yr Rs 25, 3rd yr Rs 10, 4th yr Rs 9 and 5th yr Rs 6 (Don't have data)

(9/18)

On the 6th year free cash flow is Rs 5 on original invested capital (maybe). It may be anything but a great business.

In simple way, a 20% ROE business will generate more free cash over 60 years than Saregama (assuming 5 years payback)

docs.google.com

(10/18)

In simple way, a 20% ROE business will generate more free cash over 60 years than Saregama (assuming 5 years payback)

docs.google.com

(10/18)

Now the irony is financials will never reveal it because within first five years entire acquisition cost (Rs 100) will be amortized and ROCE will always remain inflated.

Only free cash flow will reveal the true picture.

(11/18)

Only free cash flow will reveal the true picture.

(11/18)

Another point if the XIRR of music acquisition is very high, competition won’t let you acquire at same price. The data analysis capability of Saregama is available with T series also (Regional music is definitely advantage for Saregama).

(12/18)

(12/18)

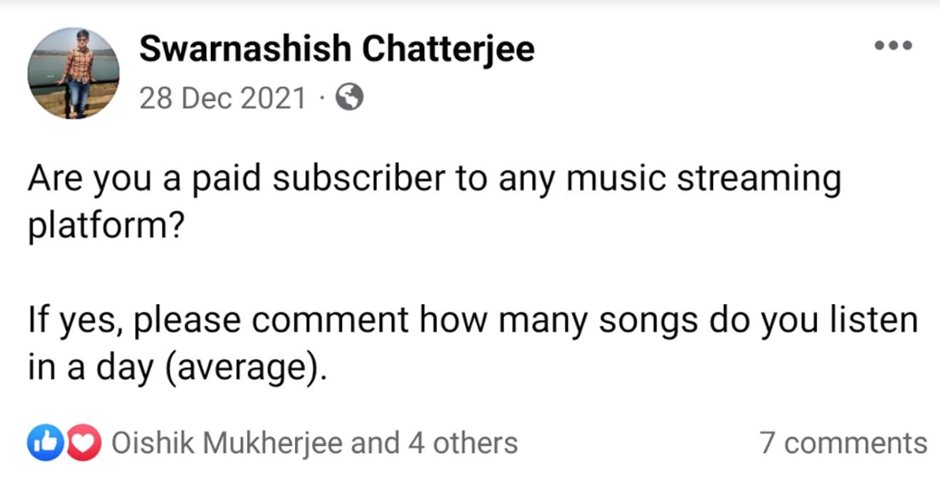

Another biggest optionality for Saregama is migration of customer from being a product (listening free songs with advertisement) to paying for product (Pay Rs 100 monthly subscription).

It is not true if only heavy music listeners switch as paid customers.

(13/18)

It is not true if only heavy music listeners switch as paid customers.

(13/18)

Imagine someone listens to song for 1.5 hours daily, means 20 songs a day, 600 songs a month and Rs 60 revenue for Saregama (10 paise per song).

If this customer switches to a monthly plan of Rs 100 to any music streaming app, Saregama gets only 50% of it i.e: Rs 50.

(14/18)

If this customer switches to a monthly plan of Rs 100 to any music streaming app, Saregama gets only 50% of it i.e: Rs 50.

(14/18)

Only if people who listens 3-4 songs daily switch as paid subscriber, it is big revenue driver for Saregma.

I did a FB poll but did not get enough response.

(15/15)

I did a FB poll but did not get enough response.

(15/15)

However the possibility of monetizing the same IP again & again (Insta Reels, MNC Ad, Remix etc) gives huge optionality especially in an inflationary environment.

(16/18)

(16/18)

You acquire a music at Rs 100 today and Spotify charges 3x after 15 years (Rs 300 monthly or 30 pasie per song) is highly beneficial.

(17/18)

(17/18)

Saregama’s focus and execution in regional music is also amazing and with less competition and saregama being only national player, it is very much possible that payback period is less than 5 years in regional music.

Disc: Invested in Saregama

(18/18)

Disc: Invested in Saregama

(18/18)

Loading suggestions...