Indian Chemical Sector:

It’s not all plain Vanilla!

Here’s our analysis of the Indian Chemical Sector, the opportunities, the complexities and ofcourse the numbers!

Grab a cup of coffee and read the Thread Below 🧵🧵🧵👇🏻

#investing #India @caniravkaria

It’s not all plain Vanilla!

Here’s our analysis of the Indian Chemical Sector, the opportunities, the complexities and ofcourse the numbers!

Grab a cup of coffee and read the Thread Below 🧵🧵🧵👇🏻

#investing #India @caniravkaria

(1/14)

The Narrative:

• Increasing Capex is taking a toll on Asset Turnover.

• Rising Raw Material prices risks near term profitability

• Gross Margin is negatively correlated to crude prices

• High growth of specialty chemical companies is driving their share up

The Narrative:

• Increasing Capex is taking a toll on Asset Turnover.

• Rising Raw Material prices risks near term profitability

• Gross Margin is negatively correlated to crude prices

• High growth of specialty chemical companies is driving their share up

(2/14)

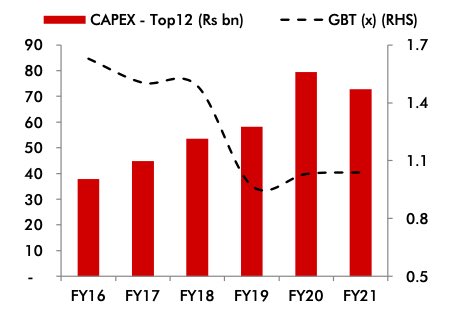

• Companies have expanded capacities into downstream products to improve growth

potential, backward integrated to mitigate RM volatility and reduce dependency on China and others.

• Asset turnover ratio(GBT) is falling after 2016 as capex was higher than revenue growth

• Companies have expanded capacities into downstream products to improve growth

potential, backward integrated to mitigate RM volatility and reduce dependency on China and others.

• Asset turnover ratio(GBT) is falling after 2016 as capex was higher than revenue growth

(3/14)

• However, companies like Deepak Nitrite, Navin Fluorine and SRF were able to improve the Asset turnover Ratio, leading to an improved ROE.

• Share of Special Chemical Segment has increased from 16% in FY16 to 29% in FY21

• However, companies like Deepak Nitrite, Navin Fluorine and SRF were able to improve the Asset turnover Ratio, leading to an improved ROE.

• Share of Special Chemical Segment has increased from 16% in FY16 to 29% in FY21

(4/14)

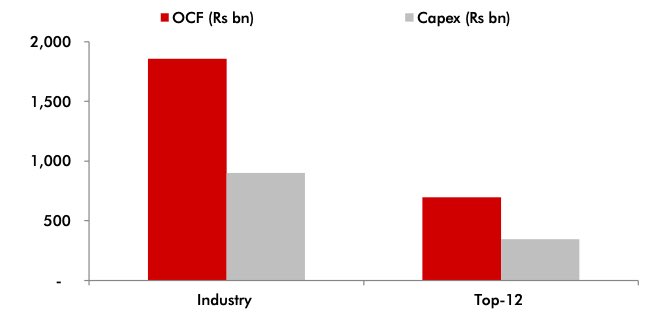

• During the last 5 years, companies (114) did a cumulative capex of ₹900Bn supported by

strong OCF of ₹1,855Bn on account of better cash conversion (OCF/EBITDA averaged 90% over FY16-21).

• During the last 5 years, companies (114) did a cumulative capex of ₹900Bn supported by

strong OCF of ₹1,855Bn on account of better cash conversion (OCF/EBITDA averaged 90% over FY16-21).

(5/14)

• Note: Liquidity in the industry was provided by a series of IPOs and QIPs in the past 3 years. These findings may indicate a consistent need for equity dilution to fund growth.

Fact: Of the total fund raised through IPO in 2021, chemical companies a/c for 12% share!

• Note: Liquidity in the industry was provided by a series of IPOs and QIPs in the past 3 years. These findings may indicate a consistent need for equity dilution to fund growth.

Fact: Of the total fund raised through IPO in 2021, chemical companies a/c for 12% share!

(6/14)

• Some near term worries:

1) Already a lot of capex is done and more is to follow.

2) China+1 theme may not play out due to limited infrastructure.

3)Volatility in Raw Material Prices remains a concern. But companies that are vertically integrated may mitigate this risk.

• Some near term worries:

1) Already a lot of capex is done and more is to follow.

2) China+1 theme may not play out due to limited infrastructure.

3)Volatility in Raw Material Prices remains a concern. But companies that are vertically integrated may mitigate this risk.

(7/14)

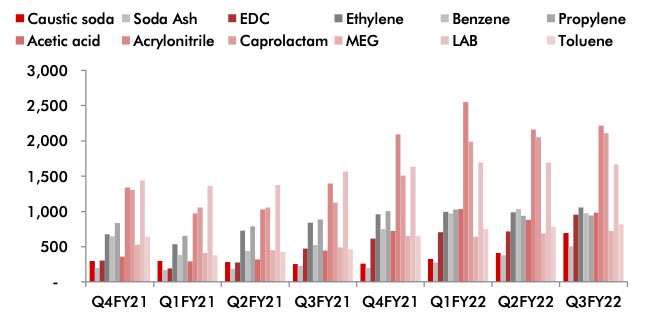

• Feedstock prices are on the rise, and may impact near term profitability.

The chart below shows that price rise is imminent across basic chemicals.

• Also, the closure of plants across China and USA along with logistics challenges has escalated the shortage of RM

• Feedstock prices are on the rise, and may impact near term profitability.

The chart below shows that price rise is imminent across basic chemicals.

• Also, the closure of plants across China and USA along with logistics challenges has escalated the shortage of RM

(8/14)

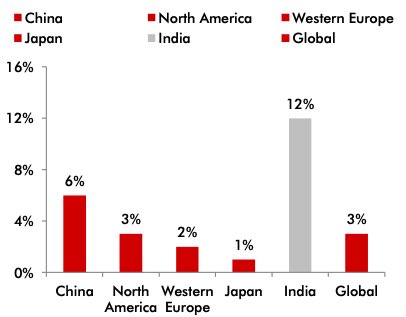

But India looks strong in the long run. Here’s why:

• Improving domestic and export demand. India has 4% share of the global chemical industry and even a marginal shift of sourcing from China (37% share of global market) will significantly boost growth of the industry.

But India looks strong in the long run. Here’s why:

• Improving domestic and export demand. India has 4% share of the global chemical industry and even a marginal shift of sourcing from China (37% share of global market) will significantly boost growth of the industry.

(9/14)

• The global specialty Chemical Market is exp to grow at 3%, while Indian market is expected to grow at 12%

• And Given supply disruption in China, we observe a favorable shift in the trade terms as innovators now desire more stability and consistency over lower prices.

• The global specialty Chemical Market is exp to grow at 3%, while Indian market is expected to grow at 12%

• And Given supply disruption in China, we observe a favorable shift in the trade terms as innovators now desire more stability and consistency over lower prices.

(10/14)

Some numbers since 2016

• Specialty Revenue grew at 14% CAGR

• Capex grew at 17% CAGR

• ROE was flat and will continue to remain so due to slowing asset return

• Higher growth of specialty segment is resulting in increased share of EBITDA.

(20% in FY16 vs 23% now)

Some numbers since 2016

• Specialty Revenue grew at 14% CAGR

• Capex grew at 17% CAGR

• ROE was flat and will continue to remain so due to slowing asset return

• Higher growth of specialty segment is resulting in increased share of EBITDA.

(20% in FY16 vs 23% now)

(11/14)

Growth Vs FCF

• Companies with higher revenue growth and high capex intensity tends to generate low FCF but have higher valuations. Thus, if chemical companies continue to post high growth along higher capex, they will have higher valuations even with limited +FCF

Growth Vs FCF

• Companies with higher revenue growth and high capex intensity tends to generate low FCF but have higher valuations. Thus, if chemical companies continue to post high growth along higher capex, they will have higher valuations even with limited +FCF

(12/14)

One Big Challenge: A need for diversification.

Here are the product concentration of major chemical companies

• Aarti Ind: ~65% revenue from benzene

• Deepak Nitrite: 55% revenue from Phenol

• Vinati: 50% revenue from ATBS

• PI: High Dependency on agrochemicals

One Big Challenge: A need for diversification.

Here are the product concentration of major chemical companies

• Aarti Ind: ~65% revenue from benzene

• Deepak Nitrite: 55% revenue from Phenol

• Vinati: 50% revenue from ATBS

• PI: High Dependency on agrochemicals

(13/14)

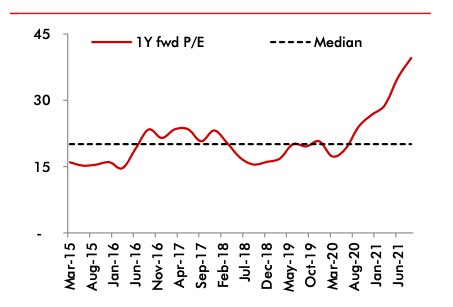

A Look at valuations:

•The market-cap weighted two year forward P/E has risen significantly over the last one year. Supported by profit growth of 30-35% (FY18-21) owing to increased capacity building, benign crude oil prices and positive sentiment around China+1 theme

A Look at valuations:

•The market-cap weighted two year forward P/E has risen significantly over the last one year. Supported by profit growth of 30-35% (FY18-21) owing to increased capacity building, benign crude oil prices and positive sentiment around China+1 theme

(14/14)

Chemical sector in the future maybe more about how individual companies perform. So selection based on integrated business models, adherence to QHSE & better execution capability will be the key.

In short, be selective and back the right business models!

Happy Reading🙂

Chemical sector in the future maybe more about how individual companies perform. So selection based on integrated business models, adherence to QHSE & better execution capability will be the key.

In short, be selective and back the right business models!

Happy Reading🙂

Loading suggestions...