Economy

Finance

Investing

Mutual Funds

Economic Outlook

Sectoral Analysis

Equity Market

FIIs

Equity Research

(1/10)

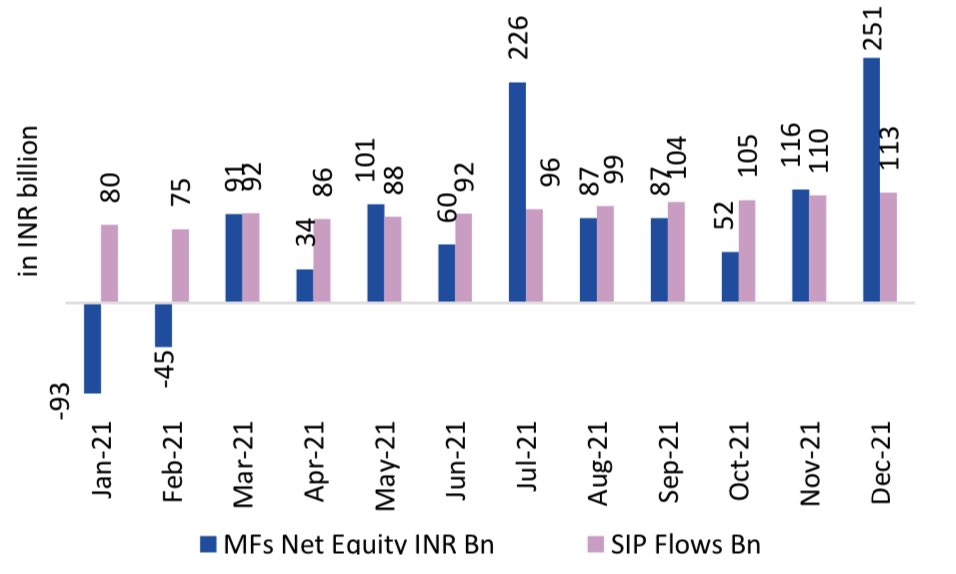

• December Equity MFs saw net inflows of ₹250Bn, a record high. SIP flows also increased to an all-time high of ₹113Bn in Dec-21.

• FII’s continued to be sellers within the Equity market with an outflow of $1.7Bn in December. They were also sellers in the Debt market.

• December Equity MFs saw net inflows of ₹250Bn, a record high. SIP flows also increased to an all-time high of ₹113Bn in Dec-21.

• FII’s continued to be sellers within the Equity market with an outflow of $1.7Bn in December. They were also sellers in the Debt market.

(2/10)

• On a sectoral basis, BFSI, FMCG, Automobiles continued to see major outflows in December extending the trend seen last month.

•Out of the 11 major sectors, only Chemical and Transportation sector registered inflows in Dec-21.

• On a sectoral basis, BFSI, FMCG, Automobiles continued to see major outflows in December extending the trend seen last month.

•Out of the 11 major sectors, only Chemical and Transportation sector registered inflows in Dec-21.

(3/10)

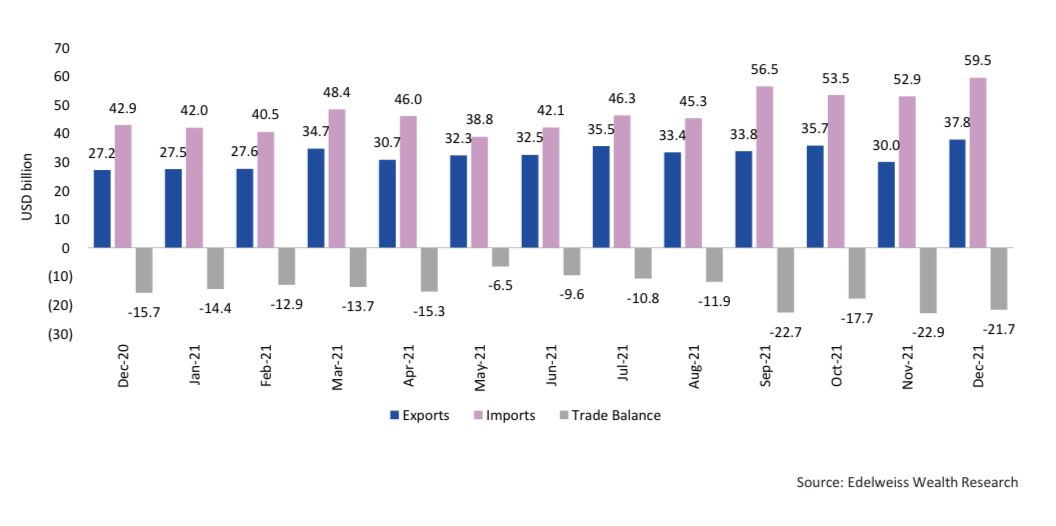

Let’s look at the December Import-Export data:

• Imports up 38.55% YoY to a record high of $59.48Bn

(Higher purchases of POL items, oil and gold)

• Exports up 38.91% YoY to an all-time high of $37.81Bn

(Higher sales of petroleum items, engineering goods, and chemicals

Let’s look at the December Import-Export data:

• Imports up 38.55% YoY to a record high of $59.48Bn

(Higher purchases of POL items, oil and gold)

• Exports up 38.91% YoY to an all-time high of $37.81Bn

(Higher sales of petroleum items, engineering goods, and chemicals

(4/10)

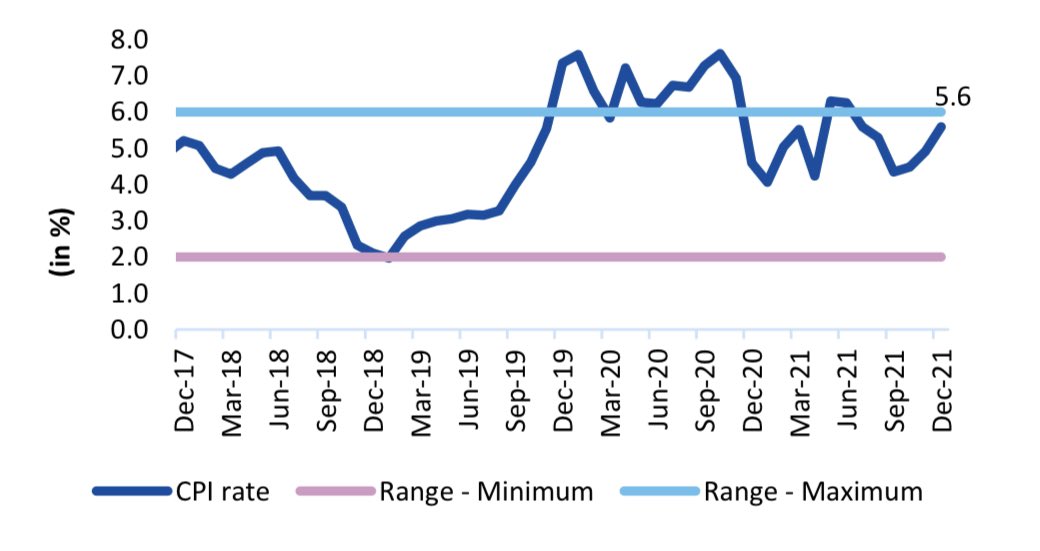

December Inflation Data:

• CPI at a 5-month high of 5.59% YoY (vs 4.91% in November)

•WPI eased to 13.56% YoY driven by a fall in price of fuel items.

•Core inflation (food and fuel) remained largely flat at 6.1% MoM, remaining above 6% for three consecutive months.

December Inflation Data:

• CPI at a 5-month high of 5.59% YoY (vs 4.91% in November)

•WPI eased to 13.56% YoY driven by a fall in price of fuel items.

•Core inflation (food and fuel) remained largely flat at 6.1% MoM, remaining above 6% for three consecutive months.

(5/10)

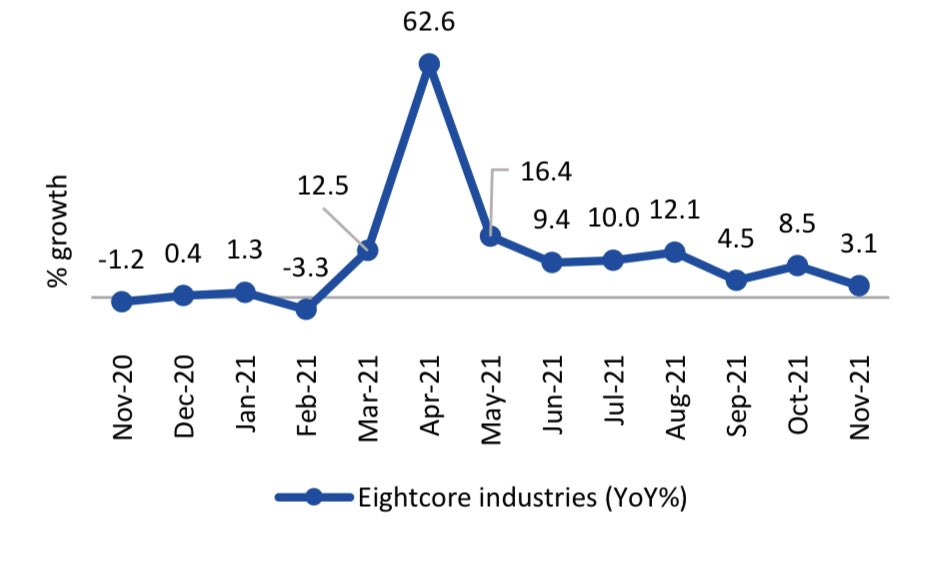

IIP Numbers:

• IIP growth reached a 9-month low of 1.4% YoY, largely due to the waning low base effect and weak manufacturing momentum. Only primary goods coupled with infrastructure/construction goods provided some support to growth in industrial output.

IIP Numbers:

• IIP growth reached a 9-month low of 1.4% YoY, largely due to the waning low base effect and weak manufacturing momentum. Only primary goods coupled with infrastructure/construction goods provided some support to growth in industrial output.

(6/10)

• Overall credit growth stood at 6.9% Y-o-Y for the second month in a row while the credit to industry /services grew by 3.8% /3.6% YoY respectively. Overall credit growth continues to show green shoots of recovery on a 2Y CAGR basis.

• Overall credit growth stood at 6.9% Y-o-Y for the second month in a row while the credit to industry /services grew by 3.8% /3.6% YoY respectively. Overall credit growth continues to show green shoots of recovery on a 2Y CAGR basis.

(7/10)

• Manufacturing PMI dipped to a 3-month low although a rise in sales and new orders continued. There is a concern around further supply chain disruptions and inflationary pressures

• Service industry grew but at a slower pace with PMI recording a drop to 55.5 from 58.1

• Manufacturing PMI dipped to a 3-month low although a rise in sales and new orders continued. There is a concern around further supply chain disruptions and inflationary pressures

• Service industry grew but at a slower pace with PMI recording a drop to 55.5 from 58.1

(8/10)

• The Auto segment continues to remain weak with only Vans and utility vehicles showing positive growth on a 2 Year CAGR. Non POL imports surged to an all-time high in December at 22.5% on a 2Year CAGR basis indicating domestic demand continues to remain in recovery mode

• The Auto segment continues to remain weak with only Vans and utility vehicles showing positive growth on a 2 Year CAGR. Non POL imports surged to an all-time high in December at 22.5% on a 2Year CAGR basis indicating domestic demand continues to remain in recovery mode

(9/10)

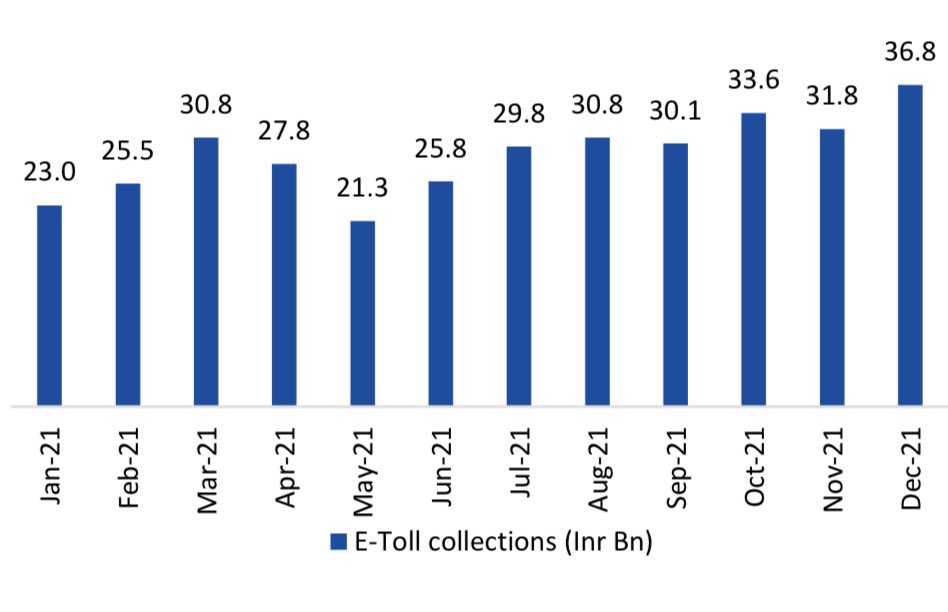

• E-way bills in Dec are the 2nd highest so far at ₹7.2Cr indicating a pick up in economic activities. GST revenue have also remained near the ₹1.3 tn mark for the 3rd month in a row.

•E-toll at an all-time high of ₹36.8Bn is a sign of normalising economic activity

• E-way bills in Dec are the 2nd highest so far at ₹7.2Cr indicating a pick up in economic activities. GST revenue have also remained near the ₹1.3 tn mark for the 3rd month in a row.

•E-toll at an all-time high of ₹36.8Bn is a sign of normalising economic activity

(10/10)

The economy is seen in a recovery mode, but covid might play a role with uncertainty around new variants and thereby causing supply chain disruptions affecting the future outlook.

Happy Reading! 🙂

The economy is seen in a recovery mode, but covid might play a role with uncertainty around new variants and thereby causing supply chain disruptions affecting the future outlook.

Happy Reading! 🙂

Loading suggestions...