A Thread🧵on INDIAN HEALTHCARE SECTOR and my top pick.

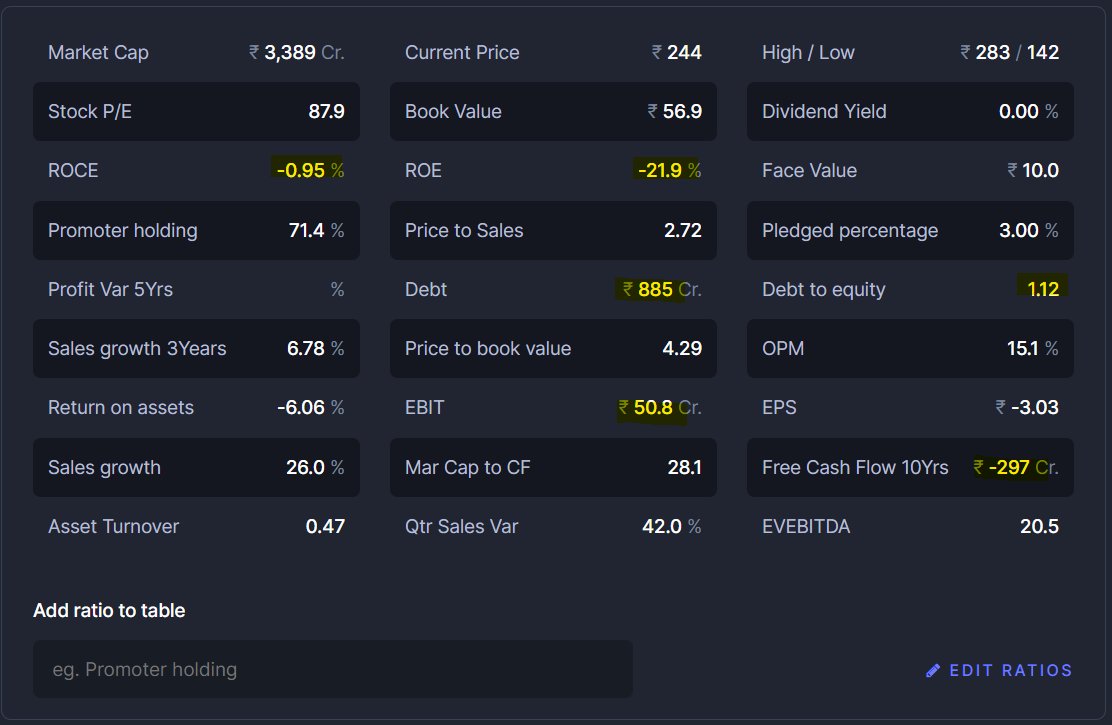

So before starting the analysis, I wanna show the financials of this company and ask you will you invests in this company?

Loss making

Negative EPS

-21% ROE

-ve ROCE

1.12 D/E

So before starting the analysis, I wanna show the financials of this company and ask you will you invests in this company?

Loss making

Negative EPS

-21% ROE

-ve ROCE

1.12 D/E

Looking at these figures, I won't even invest a penny in it.

But why I still think that it's a great opportunity and it's worth investing?

Let's explore -

1. Indian healthcare Industry

2. Hospital Segment

3. Medical Tourism

4. Divers of growth

But why I still think that it's a great opportunity and it's worth investing?

Let's explore -

1. Indian healthcare Industry

2. Hospital Segment

3. Medical Tourism

4. Divers of growth

5. Cancer situation (World)

6. Cancer situation (India)

7. Business Segments

8. Financials

9. Management

10. Thesis

11. Anti Thesis

6. Cancer situation (India)

7. Business Segments

8. Financials

9. Management

10. Thesis

11. Anti Thesis

1. INDIAN HEALTHCARE INDUSTRY -

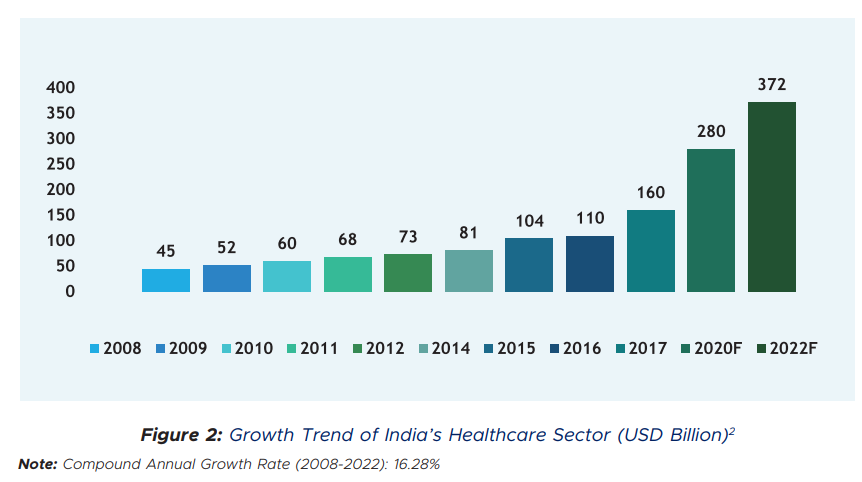

India’s healthcare industry has been growing at a Compound Annual Growth Rate of around 22% since 2016. At this rate, it is expected to reach USD 372 Billion in 2022.

India’s healthcare industry has been growing at a Compound Annual Growth Rate of around 22% since 2016. At this rate, it is expected to reach USD 372 Billion in 2022.

In 2015, the healthcare sector became the fifth largest employer, employing 4.7 Million people directly.

As per estimates by the National Skill Development Corporation (NSDC) healthcare can generate 2.7 Million additional jobs in India between 2017-22 -- over 500,000 new jobs PY

As per estimates by the National Skill Development Corporation (NSDC) healthcare can generate 2.7 Million additional jobs in India between 2017-22 -- over 500,000 new jobs PY

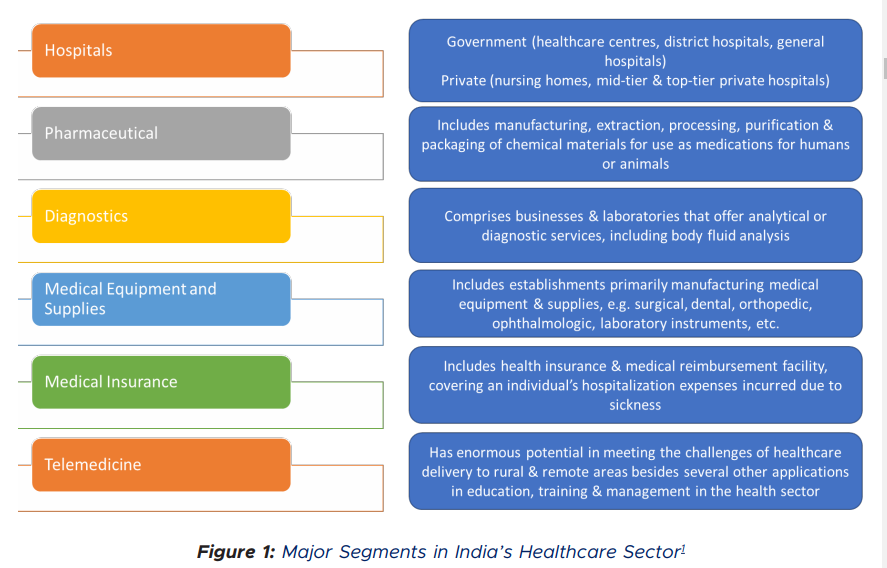

India’s healthcare industry comprises hospitals, medical devices and equipment, health

insurance clinical trials telemedicine and medical tourism

On the policy front, the Indian Government is undertaking deep structural and sustained

reforms to strengthen the healthcare sector

insurance clinical trials telemedicine and medical tourism

On the policy front, the Indian Government is undertaking deep structural and sustained

reforms to strengthen the healthcare sector

In fact, India’s FDI regime has been liberalised

extensively. Currently, FDI is permitted up to 100% under the automatic route in the hospital sector and in the manufacture of medical devices.

In the pharmaceutical sector, FDI is permitted up to 100% in greenfield projects

extensively. Currently, FDI is permitted up to 100% under the automatic route in the hospital sector and in the manufacture of medical devices.

In the pharmaceutical sector, FDI is permitted up to 100% in greenfield projects

and 74% in brownfield projects under the automatic route.

The healthcare sector, in particular, has received heightened interest from investors over the last few years, with the transaction value increasing from USD 94 Million (2011) to USD 1,275 Million (2016)

The healthcare sector, in particular, has received heightened interest from investors over the last few years, with the transaction value increasing from USD 94 Million (2011) to USD 1,275 Million (2016)

– a jump of over 13.5 times.

The Aatmanirbhar Bharat Abhiyaan packages include several short-term and longer-term

measures for the health system, including Production-Linked Incentive (PLI) schemes for

boosting domestic manufacturing of pharmaceuticals and medical devices

The Aatmanirbhar Bharat Abhiyaan packages include several short-term and longer-term

measures for the health system, including Production-Linked Incentive (PLI) schemes for

boosting domestic manufacturing of pharmaceuticals and medical devices

In the hospital segment, the expansion of private players to Tier 2 and Tier 3 locations, beyond

metropolitan cities, offers an attractive investment opportunity. According to Invest India’s

Investment Grid, there are nearly 600 investment opportunities worth USD 32 Billion

metropolitan cities, offers an attractive investment opportunity. According to Invest India’s

Investment Grid, there are nearly 600 investment opportunities worth USD 32 Billion

(INR 2.3 Lakh Crore) in the country’s hospital/medical infrastructure sub-sector.

With respect to pharmaceuticals, India has the opportunity to boost domestic manufacturing,

supported by recent Government schemes with performance-linked incentives, as part of the

Aatmanirbhar

With respect to pharmaceuticals, India has the opportunity to boost domestic manufacturing,

supported by recent Government schemes with performance-linked incentives, as part of the

Aatmanirbhar

Bharat (Self-Reliant India) initiative. Further, between 2018 and 2024, patents

worth USD 251 Billion are expected to expire globally, presenting a lucrative opportunity

for the country’s pharmaceutical sector, including the patent market.

worth USD 251 Billion are expected to expire globally, presenting a lucrative opportunity

for the country’s pharmaceutical sector, including the patent market.

A report by WHO suggests that each dollar spent in the health sector results in an additional USD 0.77 contribution to economics growth as a result of indirect and induced effects.

POLICY LANDSCAPE -

India is committed to achieving Universal Health Coverage as part of the Sustainable

Development Goals. In the Union Budget 2021-22, the Government allocated a sum of INR 2,23,846 Crore for health and wellbeing

India is committed to achieving Universal Health Coverage as part of the Sustainable

Development Goals. In the Union Budget 2021-22, the Government allocated a sum of INR 2,23,846 Crore for health and wellbeing

up from the 2020-21 budgetary allocation of INR 94,452

Crore.12 Between FY15-FY21 BE, India’s public health expenditure as a percentage of GDP increased

from 1.2% to 1.8%.12

Crore.12 Between FY15-FY21 BE, India’s public health expenditure as a percentage of GDP increased

from 1.2% to 1.8%.12

Currently, out-of-pocket expenditure constitutes more than 60% of all health expenses, a major challenge in a country like India where a large segment of the population is poor. It is estimated that approximately 63 Million people fall into poverty every year due to lack of

financial protection for their healthcare needs.

Indian govt launched PM-JAY, Ayushman Bharat, National Digital Health Mission (NDHM) to tackle these challenges.

Indian govt launched PM-JAY, Ayushman Bharat, National Digital Health Mission (NDHM) to tackle these challenges.

PM-JAY is the world’s largest non-contributory Government-sponsored health insurance

scheme that enables increased access to inpatient healthcare for poor and vulnerable families

in secondary and tertiary facilities.

scheme that enables increased access to inpatient healthcare for poor and vulnerable families

in secondary and tertiary facilities.

Ayushman Bharat scheme provides 500 Million beneficiaries with an annual hospitalization cover of up to INR 500,000 per family.6 Over 24,000 hospitals have been empanelled under the scheme, as of 23 February, 2021 and over 16 Million hospital admissions have been covered.

In addition to reforming the governance mechanisms for medical education in the country, the

Government is also expanding the number of medical and nursing colleges for meeting the

demand for health professionals.14 In November 2020, the number of medical colleges in India

Government is also expanding the number of medical and nursing colleges for meeting the

demand for health professionals.14 In November 2020, the number of medical colleges in India

increased to over 560 from 412 in FY16.

The number of registered

medical doctors increased to 1,255,786 in September 2020 from 827,006 in 2010.

NATIONAL DIGITAL HEALTH MISSION (NDHM) aims to create a management mechanism to process digital health data.

The number of registered

medical doctors increased to 1,255,786 in September 2020 from 827,006 in 2010.

NATIONAL DIGITAL HEALTH MISSION (NDHM) aims to create a management mechanism to process digital health data.

2. HOSPITALS AND INFRASTRUCTURE -

The hospital industry in India accounts for 80% of the total healthcare market.

It was valued at USD 61.79 Billion in FY17 and is expected to reach USD 132 Billion by

2023, growing at a CAGR of 16%-17%

The hospital industry in India accounts for 80% of the total healthcare market.

It was valued at USD 61.79 Billion in FY17 and is expected to reach USD 132 Billion by

2023, growing at a CAGR of 16%-17%

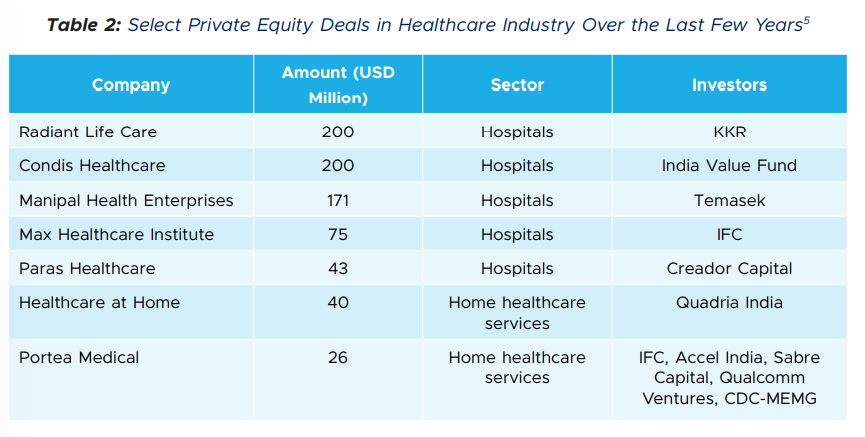

Private Equity deals over the years in Indian healthcare Industry -

It is noteworthy that around 65% of hospital beds in India cater to almost 50% of the population

concentrated in Uttar Pradesh, Maharashtra, Karnataka, Tamil Nadu, Telangana, West Bengal

and Kerala. The other 50% of the country’s population living in the remaining 21

concentrated in Uttar Pradesh, Maharashtra, Karnataka, Tamil Nadu, Telangana, West Bengal

and Kerala. The other 50% of the country’s population living in the remaining 21

sates and 8 union territories has access to only 35% of hospital beds.

The Department of Economic Affairs, Government of India, introduced “the Scheme for

Financial Support to PPPs in Infrastructure” in 2006.

The Department of Economic Affairs, Government of India, introduced “the Scheme for

Financial Support to PPPs in Infrastructure” in 2006.

Under the existing scheme 64 projects have been accorded final approval with a total

project cost of INR 34,228 crore and Viability Gap Funding (VGF) of INR 5,639 Crore.

project cost of INR 34,228 crore and Viability Gap Funding (VGF) of INR 5,639 Crore.

A sum of INR 2,100 Crore has been allocated for VGF in social infrastructure projects till

2024-25, split into two sub-schemes.

The Central Government can provide a maximum of 30% of capital

cost as VGF with the State Government/Sponsoring Central Ministry/Statutory Entity

2024-25, split into two sub-schemes.

The Central Government can provide a maximum of 30% of capital

cost as VGF with the State Government/Sponsoring Central Ministry/Statutory Entity

providing an equivalent additional amount (up to 30% of the capital cost).

The hospital industry in India is witnessing huge demand from both global and domestic

investors.

The Government’s plans to increase budgetary allocation for public health spending

to 2.5%

The hospital industry in India is witnessing huge demand from both global and domestic

investors.

The Government’s plans to increase budgetary allocation for public health spending

to 2.5%

of the country’s GDP by 2025, will benefit the hospital sector as well.

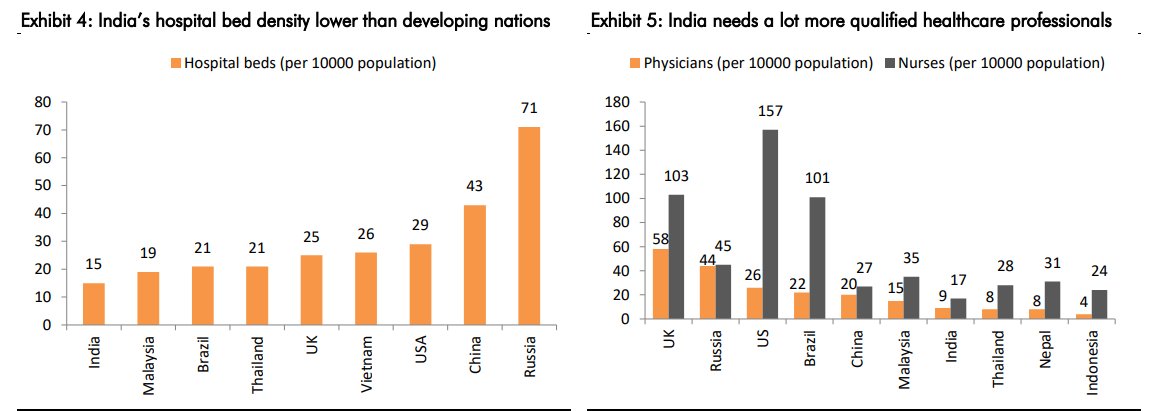

India’s hospital bed density is less than half the global average of 3 hospital beds per 1,000 population, implying that an estimated 2.2 Million beds will be required over the next 15 years.

India’s hospital bed density is less than half the global average of 3 hospital beds per 1,000 population, implying that an estimated 2.2 Million beds will be required over the next 15 years.

There are nearly 600 investment opportunities worth USD 32 Billion (INR 2.3 Lakh Crore)

in the hospital/medical infrastructure sub-sector on Indian Investment Grid (IIG), a platform

maintained by Invest India for showcasing investment opportunities by sector.

in the hospital/medical infrastructure sub-sector on Indian Investment Grid (IIG), a platform

maintained by Invest India for showcasing investment opportunities by sector.

India's bed capacity not only falls far behind the global median of 29 beds per 10,000 people but also lags behind that of other developing countries such as Brazil, Malaysia and Vietnam as of 2018.

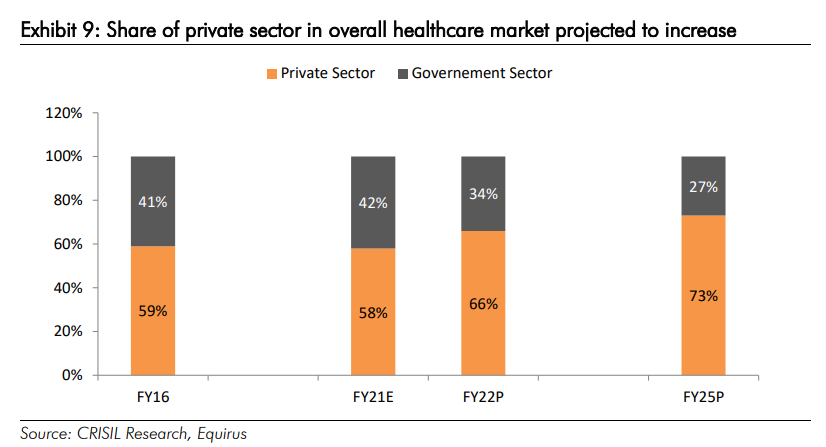

Private sector share in healthcare market to increase from just 58% in FY21 to 73% in FY25.

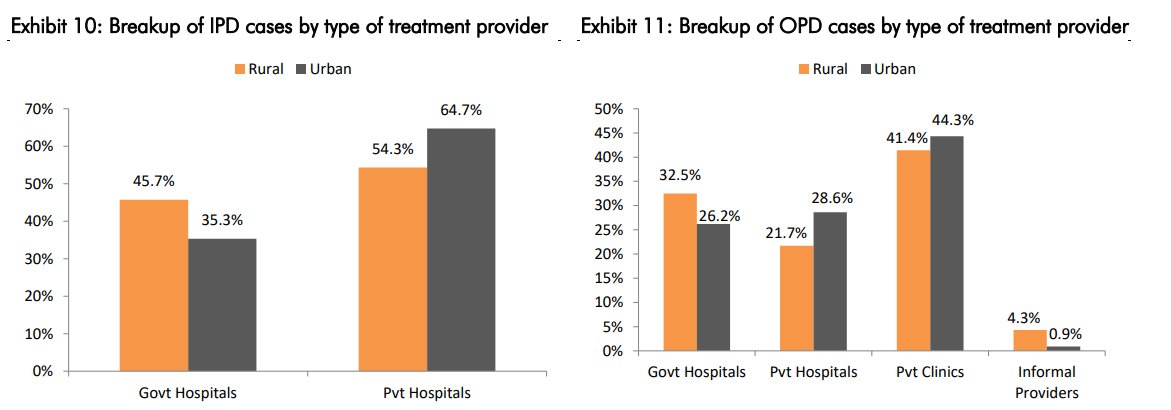

As per the NSS 75th round survey, in rural areas, 45.7% of IPD treatments were carried out in

government hospitals while the rest 54.3% in private hospitals. In case of urban areas, 35.3%

As per the NSS 75th round survey, in rural areas, 45.7% of IPD treatments were carried out in

government hospitals while the rest 54.3% in private hospitals. In case of urban areas, 35.3%

and 64.7% of IPD cases were treated at government and private hospitals respectively.

In most hospitals, OPD contributes

75% of total volumes but IPD 70% of

total revenues.

In most hospitals, OPD contributes

75% of total volumes but IPD 70% of

total revenues.

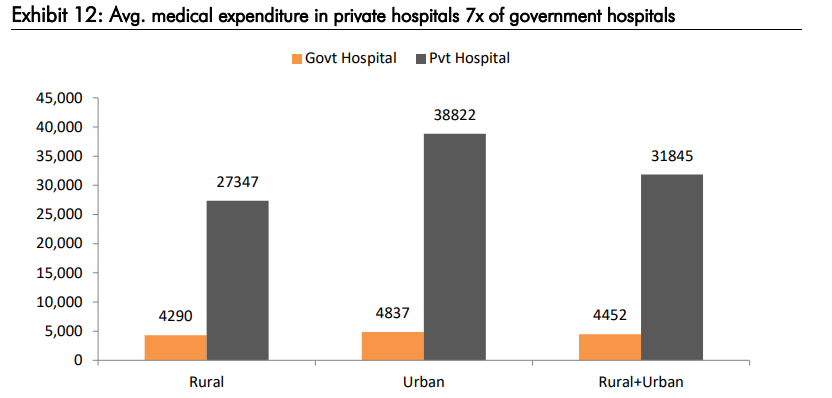

While the all-India average medical expenditure per hospitalization case in public hospitals is low at

Rs 4,452, the same for private hospitals is as high as Rs 31,845.

Rs 4,452, the same for private hospitals is as high as Rs 31,845.

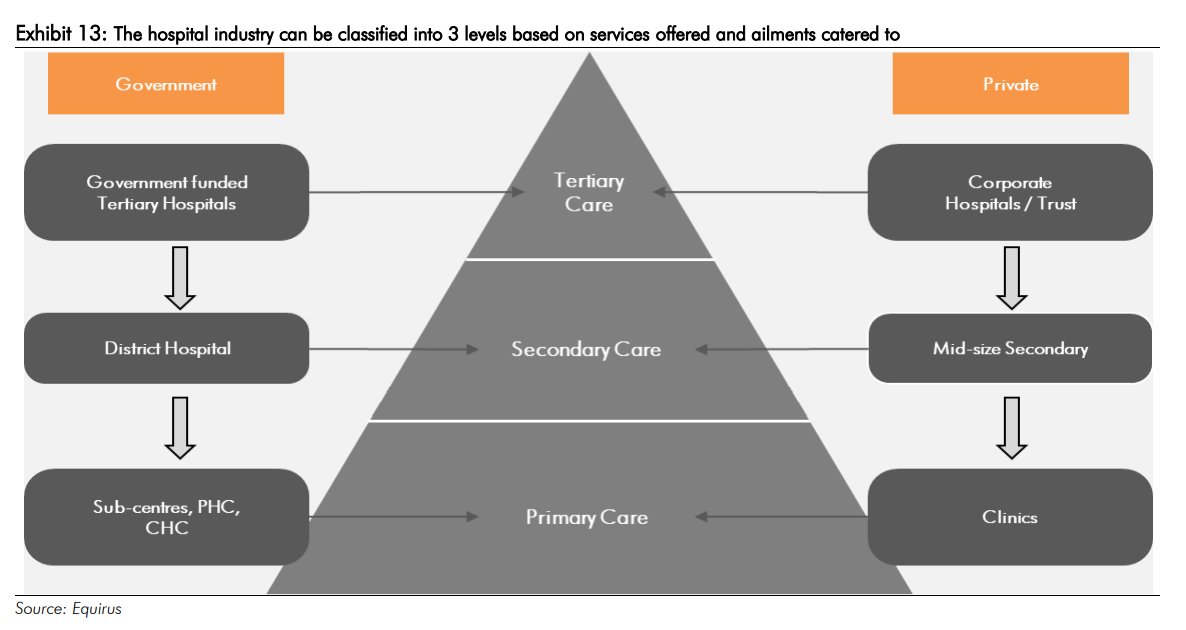

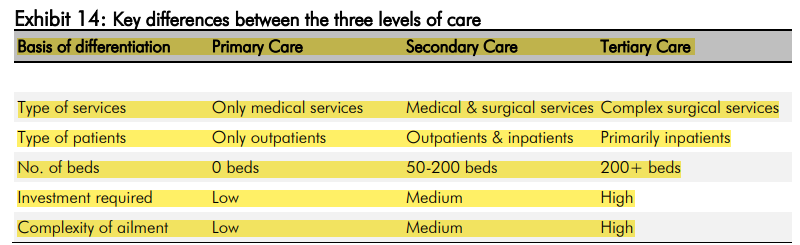

Hospital Industry can be classified into 3 levels based on services offered and ailments catered to.

1. Primary - Primary care facilities are outpatient units that offer basic, point-of-contact medical and preventive healthcare services, wherein patients come for routine health

1. Primary - Primary care facilities are outpatient units that offer basic, point-of-contact medical and preventive healthcare services, wherein patients come for routine health

screenings and vaccinations.

2. Secondary - There are two types of secondary care hospitals – general and specialty care. General hospitals treat

common ailments and have 50-100 in-patient beds, a tenth of which are allocated to ICUs. Specialty

care hospitals typically have a

2. Secondary - There are two types of secondary care hospitals – general and specialty care. General hospitals treat

common ailments and have 50-100 in-patient beds, a tenth of which are allocated to ICUs. Specialty

care hospitals typically have a

strength of 100-200 beds, of which 15% are reserved for critical care units.

3. Tertiary - Tertiary care hospitals provide advanced healthcare services, usually on referral from primary or

secondary medical care providers.

3. Tertiary - Tertiary care hospitals provide advanced healthcare services, usually on referral from primary or

secondary medical care providers.

3. KEY GROWTH DRIVERS -

a. Rising Per capita GDP

b. Improvement in life expectancy

c. Rise in NCDs

d. Increase in health insurance penetration

e. Favorable govt policies

f. Demand supply gap

a. Rising Per capita GDP

b. Improvement in life expectancy

c. Rise in NCDs

d. Increase in health insurance penetration

e. Favorable govt policies

f. Demand supply gap

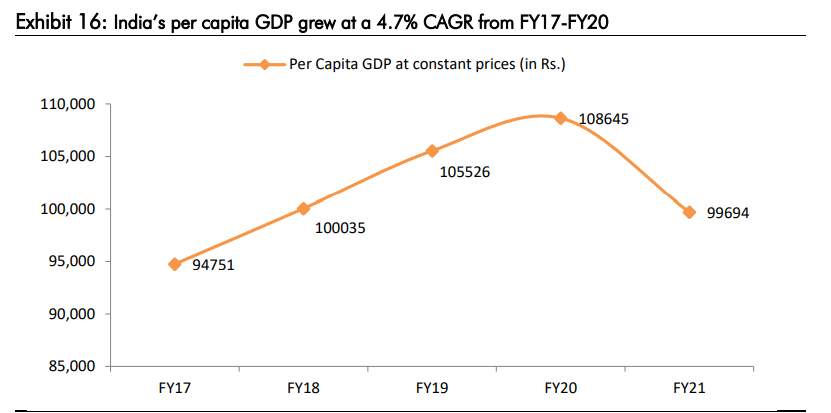

A. Rising per capita GDP -

India’s per capita GDP is rising, which eventually leads to more demand for healthcare

services. From FY17-FY20, per capita GDP grew at a 4.7% CAGR

It is expected that 8% Indians will earn more

than USD 12,000 per annum by 2026.

India’s per capita GDP is rising, which eventually leads to more demand for healthcare

services. From FY17-FY20, per capita GDP grew at a 4.7% CAGR

It is expected that 8% Indians will earn more

than USD 12,000 per annum by 2026.

B. Improving life expectancy -

Life expectancy in India is likely to exceed 70 years by 2022 and the country’s population is projected to increase to 1.45 Billion by 2028 With improving life expectancy, India’s demographic profile is also witnessing a change.

Life expectancy in India is likely to exceed 70 years by 2022 and the country’s population is projected to increase to 1.45 Billion by 2028 With improving life expectancy, India’s demographic profile is also witnessing a change.

As of 2011, nearly 8% of India’s population was of 60 years or more, and this is expected to surge to 12.5% by 2026. Higher vulnerability of this age group to health-related issues will boost demand for healthcare-related services.

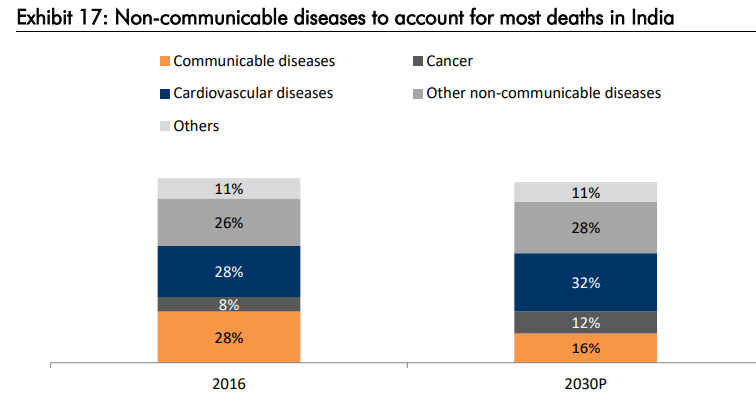

C. Rise in Non Communicable Diseases (NCDs) -

India currently has around 60 Million diabetics, a number that is expected to swell to 90

Million by 2025. It is estimated that every fourth individual in India aged above 18 years has

hypertension.

India currently has around 60 Million diabetics, a number that is expected to swell to 90

Million by 2025. It is estimated that every fourth individual in India aged above 18 years has

hypertension.

Nearly 5.8 Million Indians die from NCDs (heart and lung diseases, stroke,

cancer and diabetes) every year.10,14 The rising NCD burden is estimated to cost India USD

4.58 Trillion before 2030.

cancer and diabetes) every year.10,14 The rising NCD burden is estimated to cost India USD

4.58 Trillion before 2030.

D. Higher Insurance penetration -

As per IRDAI, health insurance coverage has risen from 17% in FY12 to 36% in FY20. Also, with the PMJAY scheme and other growth drivers, insurance

coverage in India is expected to increase to 46% by FY25.

As per IRDAI, health insurance coverage has risen from 17% in FY12 to 36% in FY20. Also, with the PMJAY scheme and other growth drivers, insurance

coverage in India is expected to increase to 46% by FY25.

E. Favorable govt Policies - Launch of PM-JAY, Ayushman Bharat, National Digital Health mission.

The government has raised its healthcare budget for FY22 to Rs 2,238.5bn, keeping in line

with its goal to raise its healthcare spending to 2.5% of GDP by 2025 l

The government has raised its healthcare budget for FY22 to Rs 2,238.5bn, keeping in line

with its goal to raise its healthcare spending to 2.5% of GDP by 2025 l

The Ayushman Bharat scheme seeks to comprehensively strengthen the healthcare system,

right from primary to tertiary care. This scheme provides healthcare assurance of Rs 0.5mn

per family (on floater basis) to nearly 107.4mn families.

right from primary to tertiary care. This scheme provides healthcare assurance of Rs 0.5mn

per family (on floater basis) to nearly 107.4mn families.

As of Nov’20, nearly 14mn treatments had taken place under Ayushman Bharat since its inception in Sep’18.

As of Nov’20, nearly 14mn treatments had taken place under Ayushman Bharat since its inception in Sep’18.

As of Nov’20, nearly 14mn treatments had taken place under Ayushman Bharat since its inception in Sep’18.

It is anticipated that over the next 10 years, an incremental economic value of over US$ 200bn can be unlocked for the health sector through rigorous

implementation of the NDHM.

implementation of the NDHM.

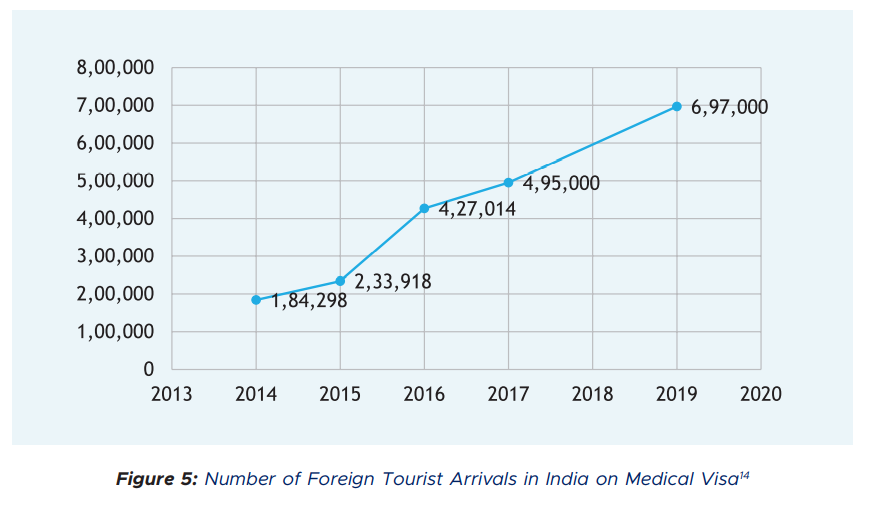

F. Medical Tourism - A thriving sector globally, medical tourism is estimated to have a market size of USD 44.8 billion in 2019, with some 1.40 crore people traveling to different countries for better medical treatment, essentially forming the medical tourism sector.

India is ranked 10th out of the top 46 countries in the world in the Medical Tourism Index 2020-21 by Medical Tourism Association. While MVT for India was projected to be USD 9 billion by 2020

despite the debilitating impact of the COVID-19 pandemic on the tourism and hospitality industry, the medical tourism sector is estimated to have been worth USD 5–6 billion. MVT in India is expected to grow to USD 13 billion by 2022.

The number of Foreign Tourist Arrivals (FTAs) in India on medical visa grew to an estimated

697,000 in 2019 from 495,056 in 2017.33 India’s medical visitors have historically come

primarily from Afghanistan, Pakistan, Oman, Bangladesh, Maldives, Nigeria, Kenya and Iraq

REASON?

697,000 in 2019 from 495,056 in 2017.33 India’s medical visitors have historically come

primarily from Afghanistan, Pakistan, Oman, Bangladesh, Maldives, Nigeria, Kenya and Iraq

REASON?

“We are blessed to be living in a country where the cost of healthcare is the lowest in the world.” ~Dr. Devi Shetty, Narayana Health

Check out this table -

Check out this table -

In 2018, the Government established a dedicated fund of INR 5,000 Crore for enhancing 12 “Champion Services Sectors”, MVT being one of them.28 The e-tourist visa launched in September, 2014 for easing the visa regime was subsequently expanded to include medical visits as well.

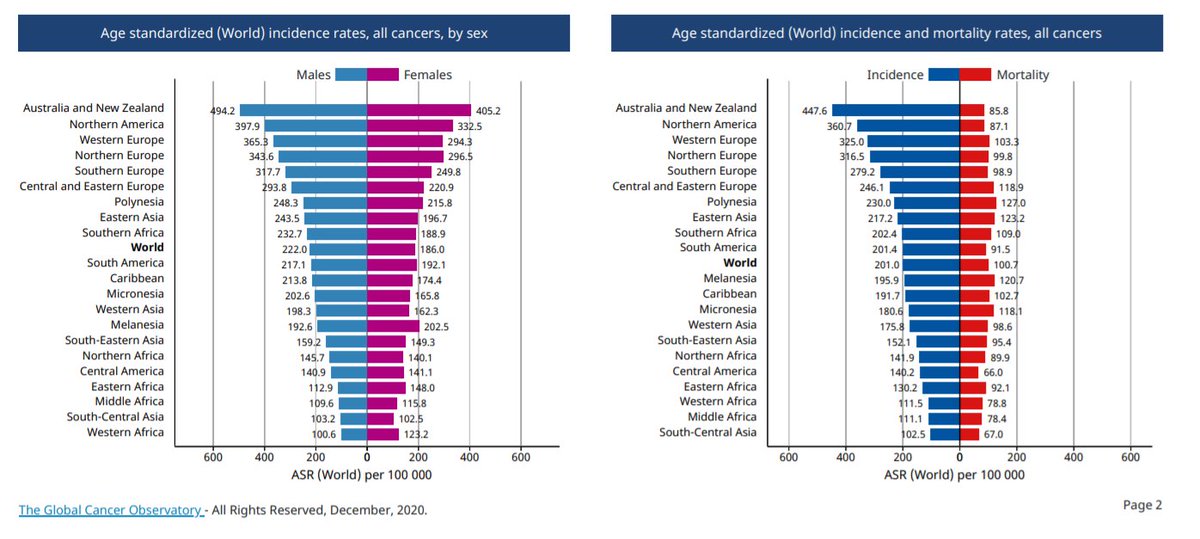

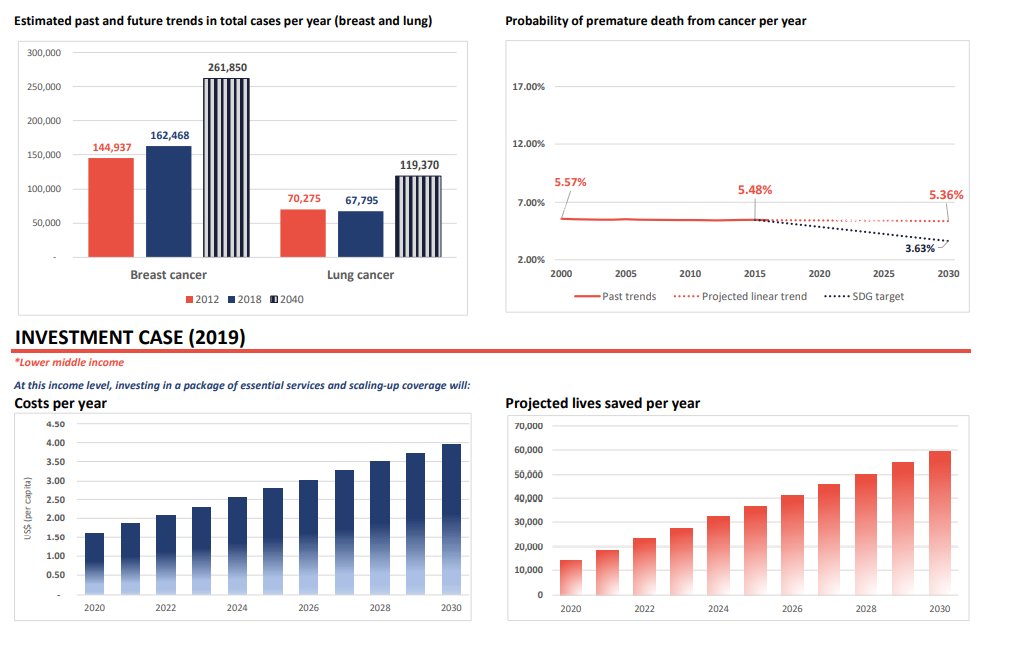

5. Cancer Situation (World) -

• Around one-third of deaths from cancer are due to tobacco use, high body mass index, alcohol use, low fruit and vegetable intake, and lack of physical activity.

Cancer-causing infections, such as hepatitis and human papillomavirus (HPV)

• Around one-third of deaths from cancer are due to tobacco use, high body mass index, alcohol use, low fruit and vegetable intake, and lack of physical activity.

Cancer-causing infections, such as hepatitis and human papillomavirus (HPV)

are responsible for approximately 30% of cancer cases in low- and lower-middle-income countries.

Late-stage presentation and lack of access to diagnosis and treatment are common, particularly in low- and middle-income countries. Comprehensive treatment is reportedly available in

Late-stage presentation and lack of access to diagnosis and treatment are common, particularly in low- and middle-income countries. Comprehensive treatment is reportedly available in

more than 90% of high-income countries but less than 15% of low-income countries.

The economic impact of cancer is significant and increasing. The total annual economic cost of cancer in 2010 was estimated at US$ 1.16 trillion.

The economic impact of cancer is significant and increasing. The total annual economic cost of cancer in 2010 was estimated at US$ 1.16 trillion.

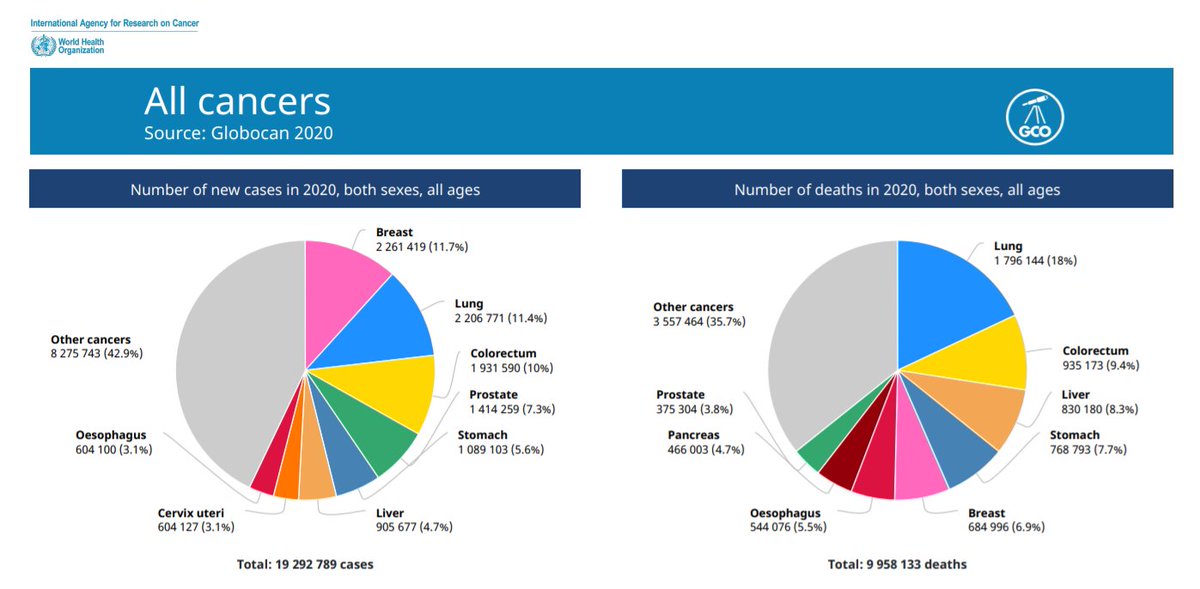

Cancer is a leading cause of death worldwide, accounting for nearly 10 million deaths in 2020 (1). The most common in 2020 (in terms of new cases of cancer) were:

• breast (2.26 million cases);

• lung (2.21 million cases);

• colon and rectum (1.93 million cases);

• breast (2.26 million cases);

• lung (2.21 million cases);

• colon and rectum (1.93 million cases);

• prostate (1.41 million cases);

• skin (non-melanoma) (1.20 million cases); and

• stomach (1.09 million cases).

The most common causes of cancer death in 2020 were:

• lung (1.80 million deaths);

• colon and rectum (935 000 deaths);

• liver (830 000 deaths);

• skin (non-melanoma) (1.20 million cases); and

• stomach (1.09 million cases).

The most common causes of cancer death in 2020 were:

• lung (1.80 million deaths);

• colon and rectum (935 000 deaths);

• liver (830 000 deaths);

• stomach (769 000 deaths); and

• breast (685 000 deaths).

• breast (685 000 deaths).

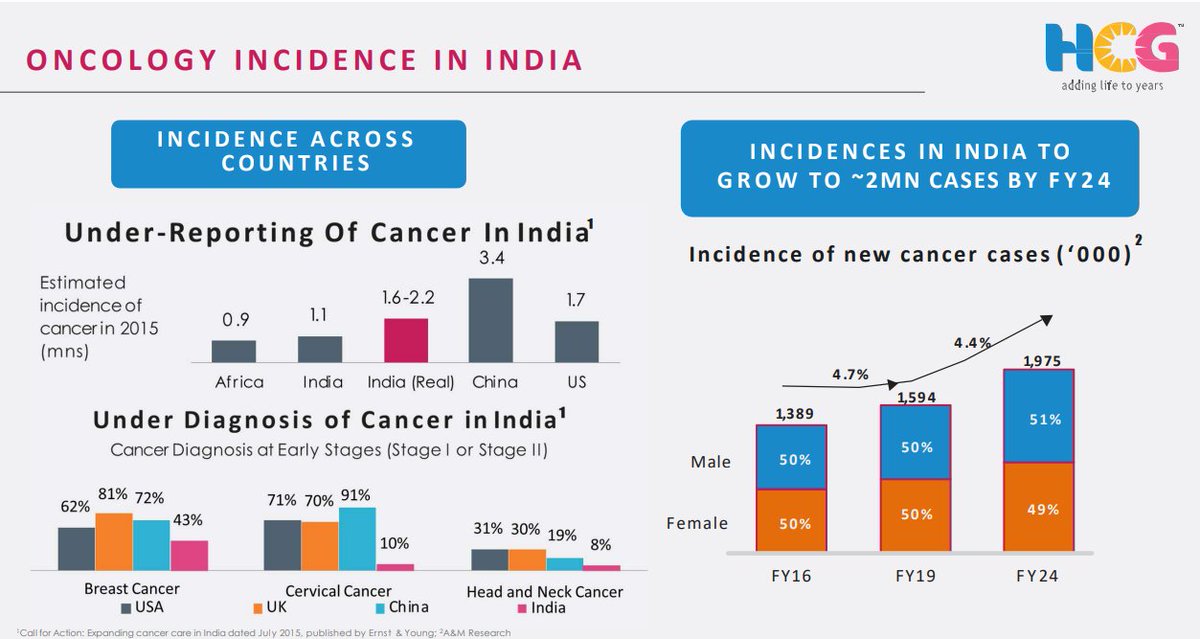

6. CANCER SITUATION (INDIA) -

India will witness more than 17.3 lakhs new cases of cancer and more than 8.8 lakh Indians would die because of it. Unfortunately, a majority of the patients visit hospitals for diagnosis or treatment in the advanced stages of the illness.

India will witness more than 17.3 lakhs new cases of cancer and more than 8.8 lakh Indians would die because of it. Unfortunately, a majority of the patients visit hospitals for diagnosis or treatment in the advanced stages of the illness.

The Indian Council of Medical Research (ICMR) data has explicitly cited the number of cancer cases to increase at an estimated number of 1.45 million new cases every year.

The treatment of the commonest forms of cancer in India – head and neck cancer – usually costs between Rs. 15,000-20,000 (US$210 to US$280) a month, in government hospitals. Whereas, the cost of treatment in private hospitals is “forbiddingly high”

According to the World Bank, the average monthly income of a person in India is close to Rs 10,000 (US$139). Thus, the affordability gap is huge.

Now this brings us to the Company I wanna talk about -

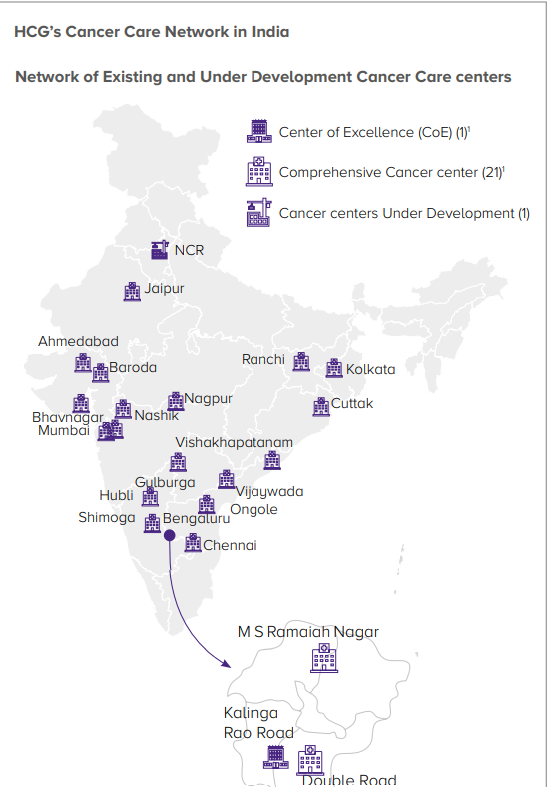

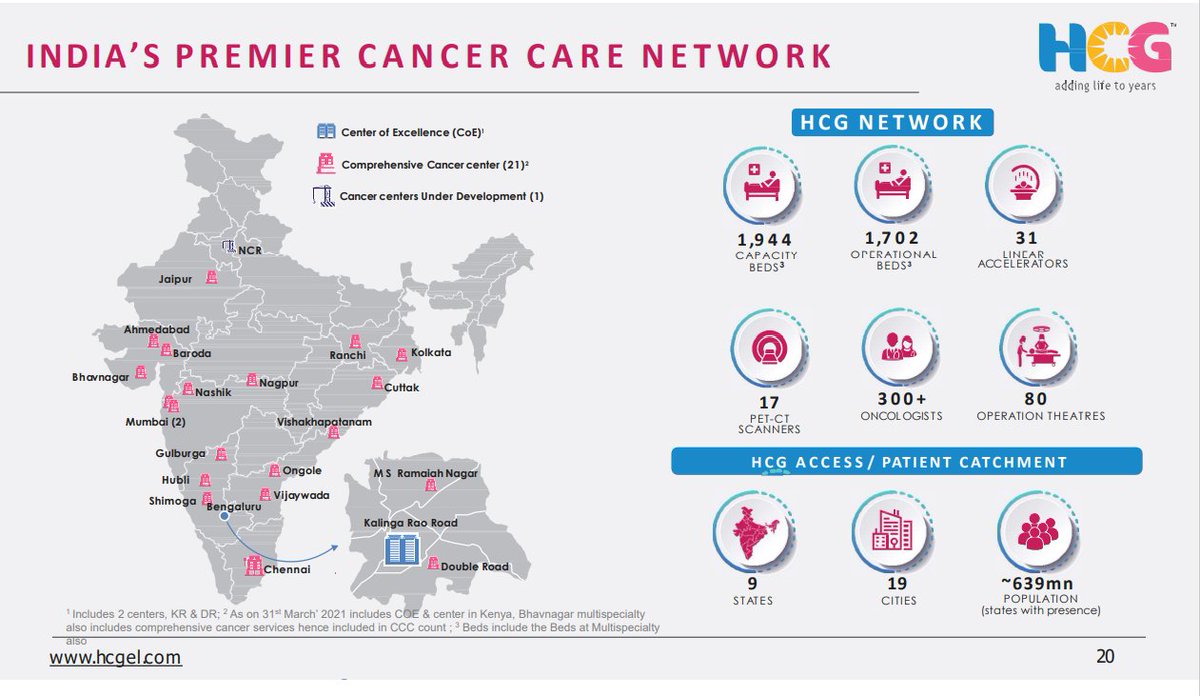

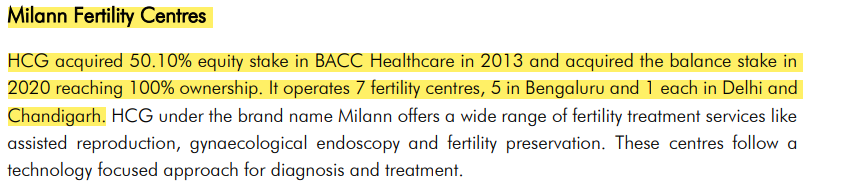

HEALTHCARE GLOBAL ENTERPRISES (HCG) - The Company is the largest provider of cancer care in India under the “HCG” brand.

HEALTHCARE GLOBAL ENTERPRISES (HCG) - The Company is the largest provider of cancer care in India under the “HCG” brand.

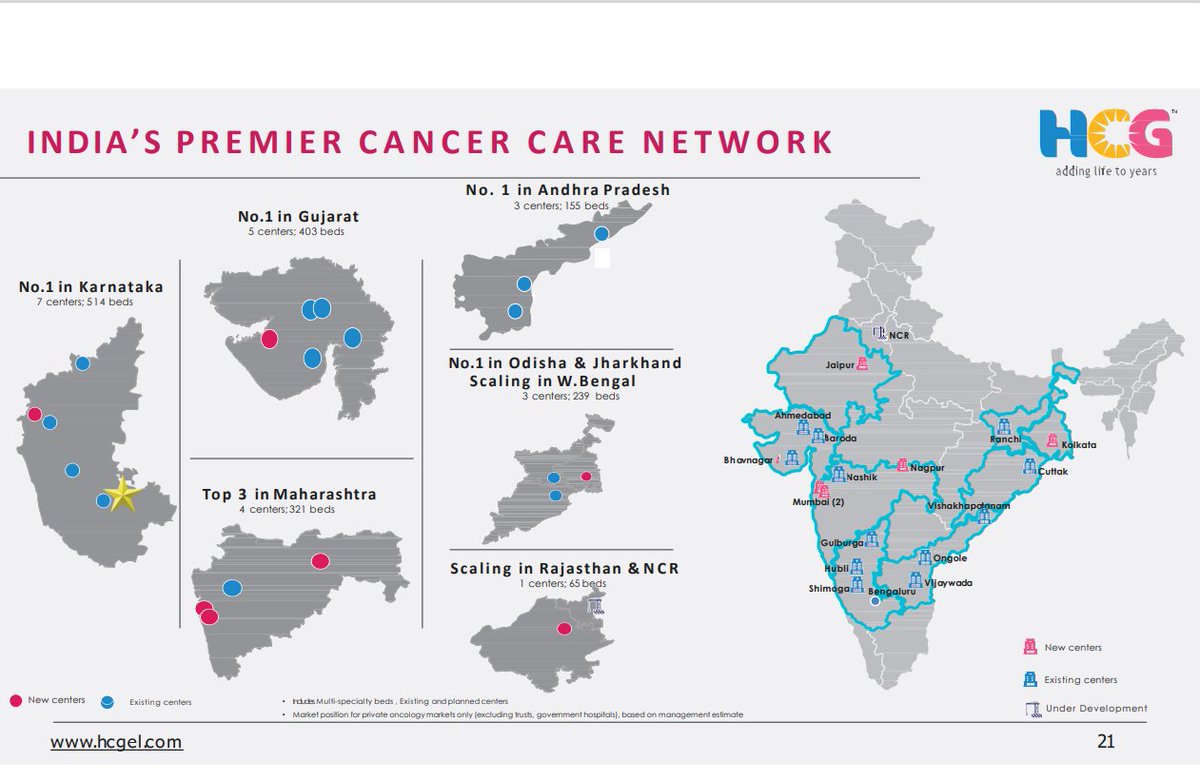

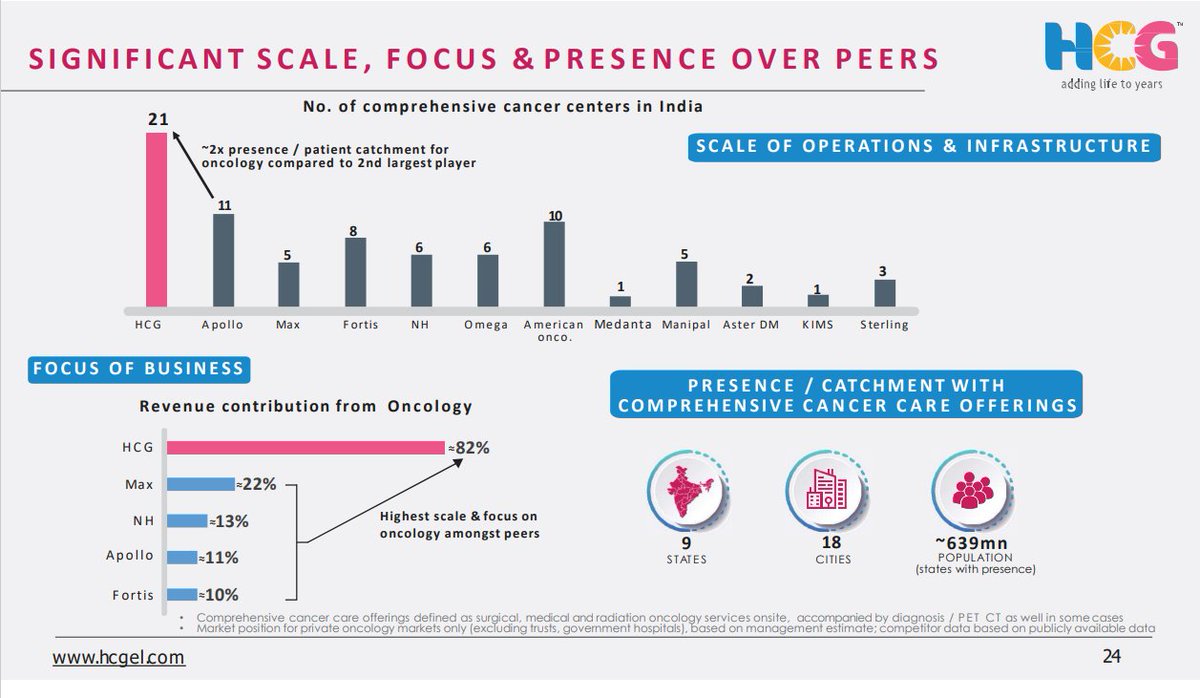

It owns and operates comprehensive cancer diagnosis and treatment services (through radiation therapy, medical oncology and surgery). As of March 31st, 2021, HCG network consisted of 21

comprehensive cancer centers, including center of excellence in Bengaluru

comprehensive cancer centers, including center of excellence in Bengaluru

and 1 center in Africa.

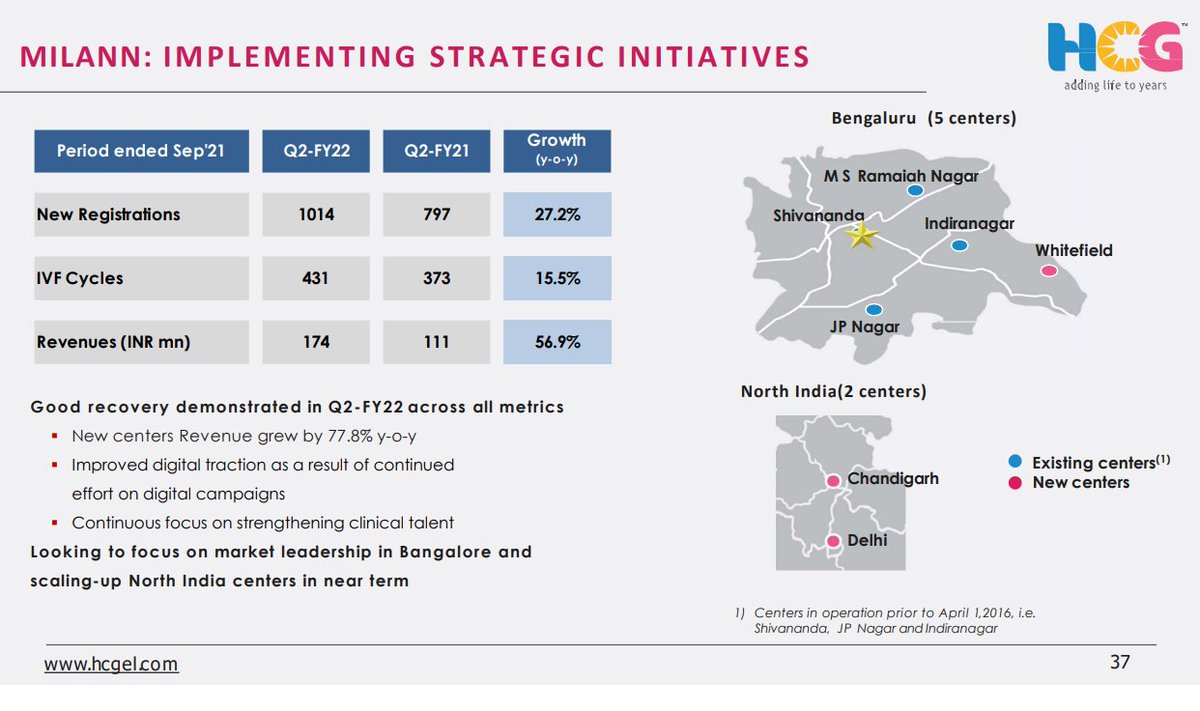

7. BUSINESS SEGMENTS - 95% of the revenue comes from Oncology segment and only 5% revenue comes from Milan Fertility center.

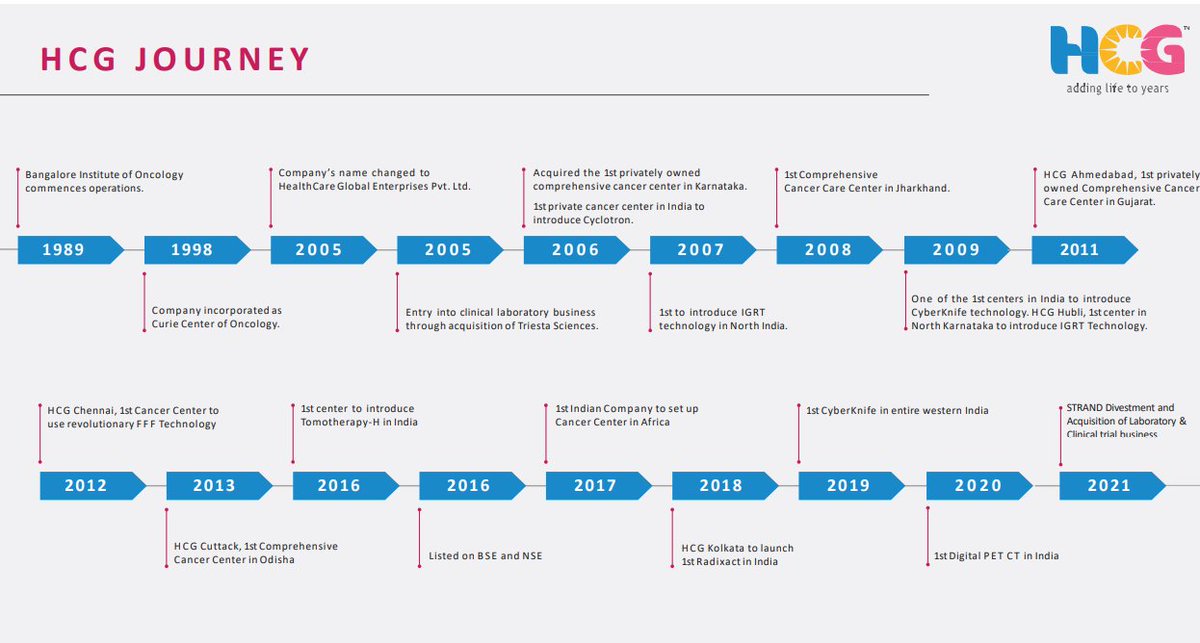

History - Started their journey in 1989 and now have 22 cancer centers including 4 multispeciality hospitals.

Mostly concentrated in southern and western region -

Karnataka - 7 centers

Gujarat - 5 centers

Maharashtra - 4 centers

Andhra Pradesh - 3 centers

Rajasthan - 1 center

Odisha, WB, Jharkhand - 3 centers

Gurgaon - 1 center under construction

Karnataka - 7 centers

Gujarat - 5 centers

Maharashtra - 4 centers

Andhra Pradesh - 3 centers

Rajasthan - 1 center

Odisha, WB, Jharkhand - 3 centers

Gurgaon - 1 center under construction

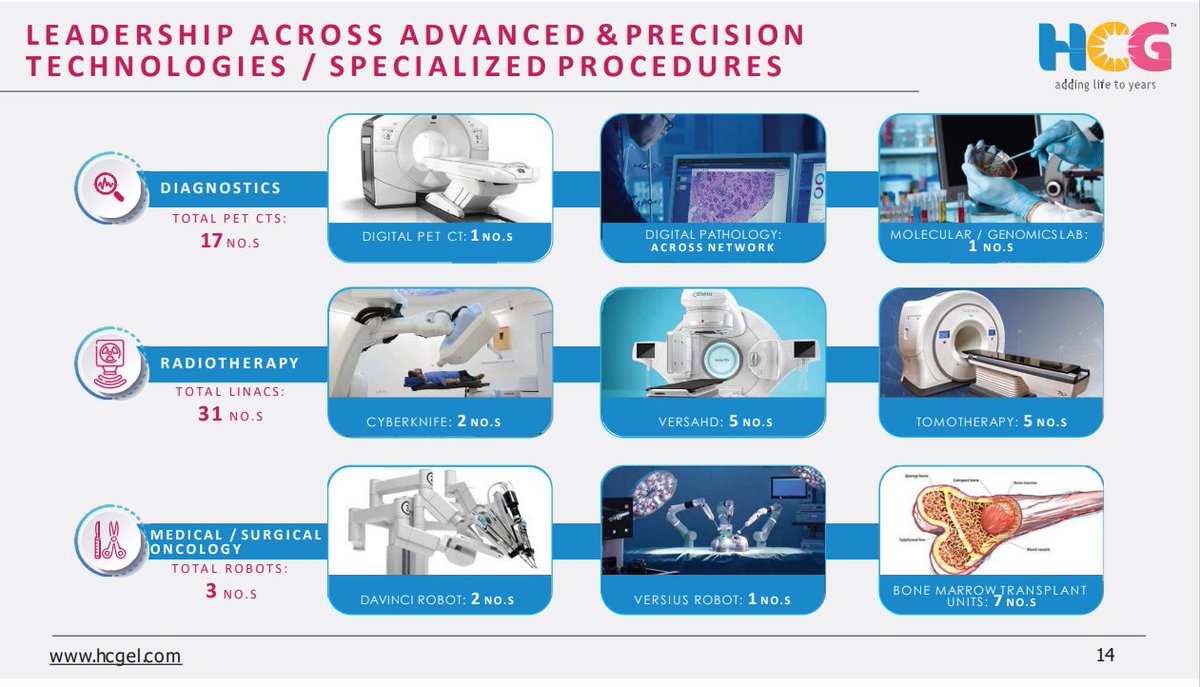

They have 17 PET CT scans ( Only 120 available in INDIA).

So their business model is mostly a revenue or profit sharing model. The idea is to get into a partnership model with hospital/doctors who already have a reputation in oncology in that area. HCG then adds beds, equipment, doctors,etc. These hospitals are capable of Diagnosis and

treatment but once in awhile the patient might have to be referred to the Hub for more high end treatment. Doctors can also use the expertise of the Hub for better diagnosis.

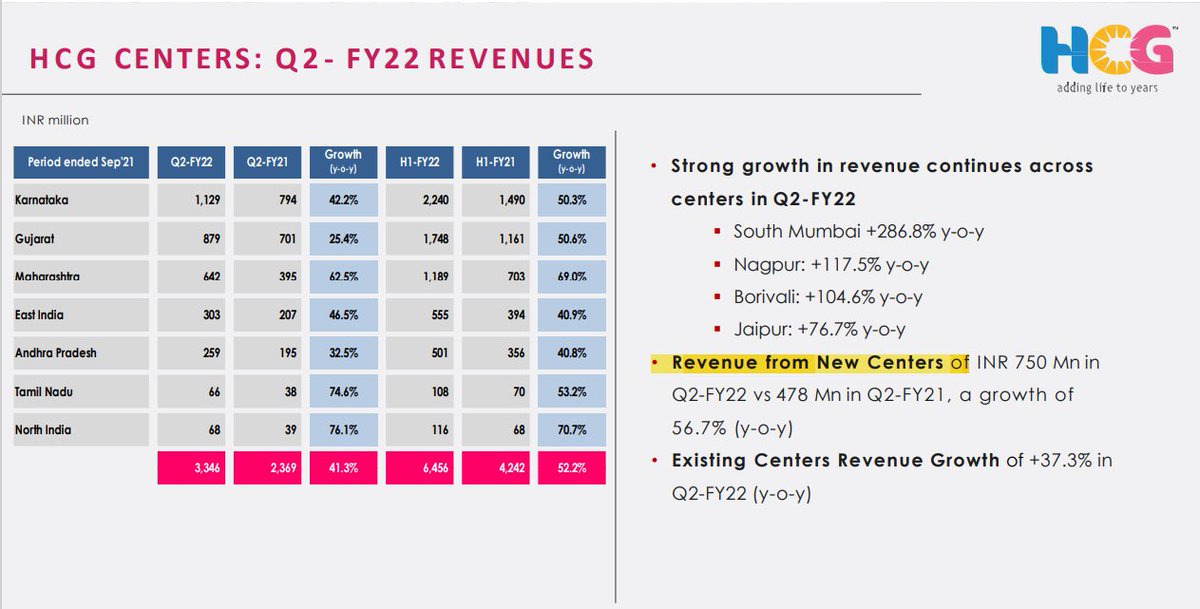

The revenue contribution from their Karnataka cluster is - 34%

Gujarat cluster - 26%

Andhra Pradesh - 8%

East India - 9%

Maharashtra - 19%

Tamil Nadu - 2%

North India - 2%

Gujarat cluster - 26%

Andhra Pradesh - 8%

East India - 9%

Maharashtra - 19%

Tamil Nadu - 2%

North India - 2%

Revenue from international patients is around 15-20% in their center of excellence at Bengaluru which has dropped to 5% due to Covid restrictions.

Before getting into more details, let's understand few terminologies related to hospital business -

Before getting into more details, let's understand few terminologies related to hospital business -

IPD - In patient - those who need to get hospitalized.

OPD - out patient - those who don't need to get hospitalized

ALOS - Average length of stay ( The no. of days patient remains hospitalized)

Occupancy Rate - How many beds are occupied at a time

OPD - out patient - those who don't need to get hospitalized

ALOS - Average length of stay ( The no. of days patient remains hospitalized)

Occupancy Rate - How many beds are occupied at a time

ARPOB - Average revenue per operational bed

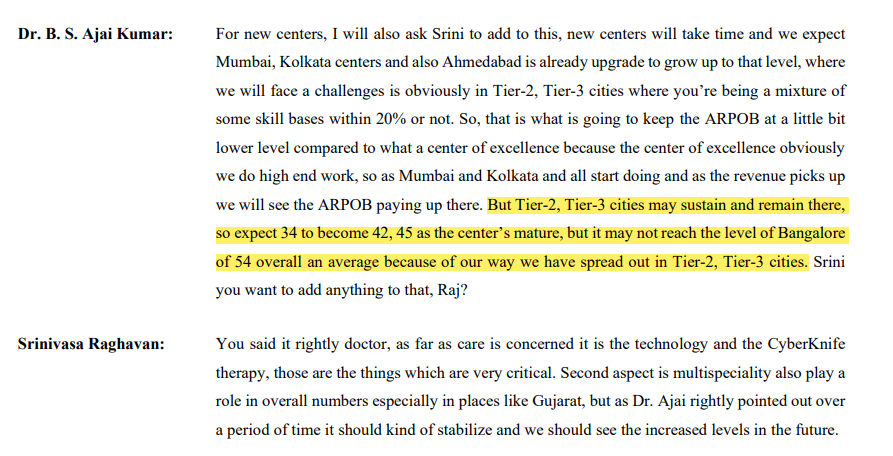

So in case of their ARPOB of their Bengaluru center of excellence is around 54K and on average latest ARPOB is around 38K.

Reason?

So in case of their ARPOB of their Bengaluru center of excellence is around 54K and on average latest ARPOB is around 38K.

Reason?

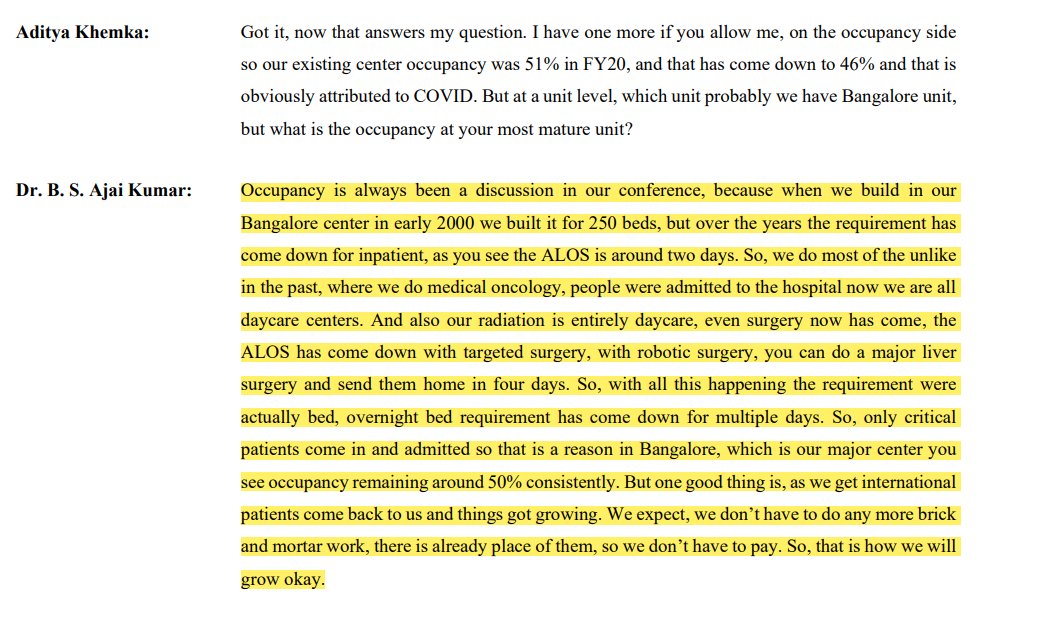

The Average Occupancy Rate for them is around 53% which is low as 50% of the beds are empty and not generating any revenue but the cost is fixed.

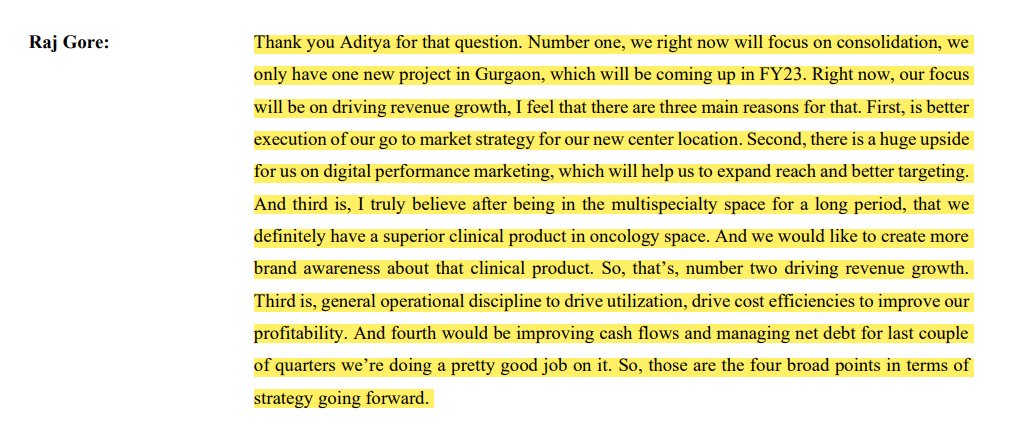

Aditya Khemka from InCred capital asked the same question.

So here's what the management have to say -

Aditya Khemka from InCred capital asked the same question.

So here's what the management have to say -

SO now let's come to the part that why I think it can be a good investment opportunity given that currently it's loss making and have high debt.

So for that 1st we need to dig a little deeper.

1st we need to understand how hospital business works.

Let's start -

So for that 1st we need to dig a little deeper.

1st we need to understand how hospital business works.

Let's start -

So hospital business is generally Asset Heavy Business ( Asset Heavy means the business that requires lots of fixed assets like factories, huge machines and stuff like that)

So a hospital needs - 1st of all land to setup new hospital, then the building, then machinery

So a hospital needs - 1st of all land to setup new hospital, then the building, then machinery

then the staff and most of this cost is fixed because a hospital won't just start generating revenue from next day.

So when the hospitals are in expansion mode, so many cost are fixed that needs to be taken care of whether you're earning any money from that hospital or not.

So when the hospitals are in expansion mode, so many cost are fixed that needs to be taken care of whether you're earning any money from that hospital or not.

For that they need to take debt and due to the interest payments and fixed costs their financials remains depressed for a very long period of time.

But then here comes the concept of operating leverage, meaning?

One your assets (new hospitals) start generating revenue

But then here comes the concept of operating leverage, meaning?

One your assets (new hospitals) start generating revenue

your bottom line shows hockey stick kind of growth.

So the best time to buy a hospital is when your capex is done and your new hospitals becomes EBITDA positive.

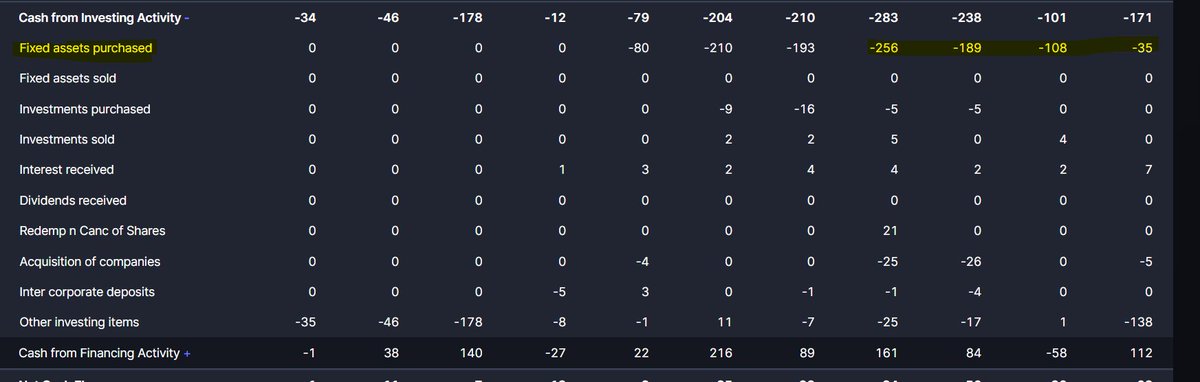

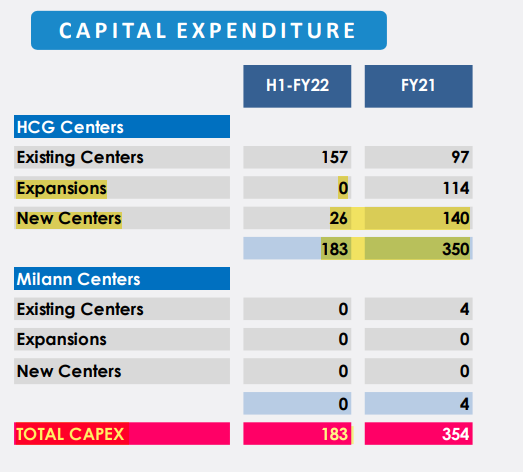

So let me show you something interesting happening in case of HCG -

So the best time to buy a hospital is when your capex is done and your new hospitals becomes EBITDA positive.

So let me show you something interesting happening in case of HCG -

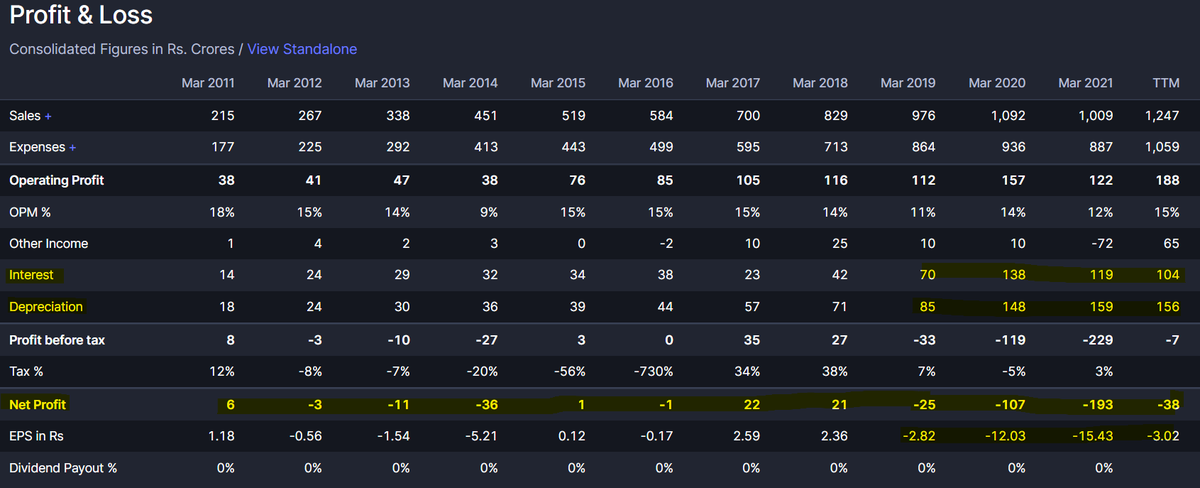

Take a look at the trend of capex. Down from 256Cr to 35Cr.

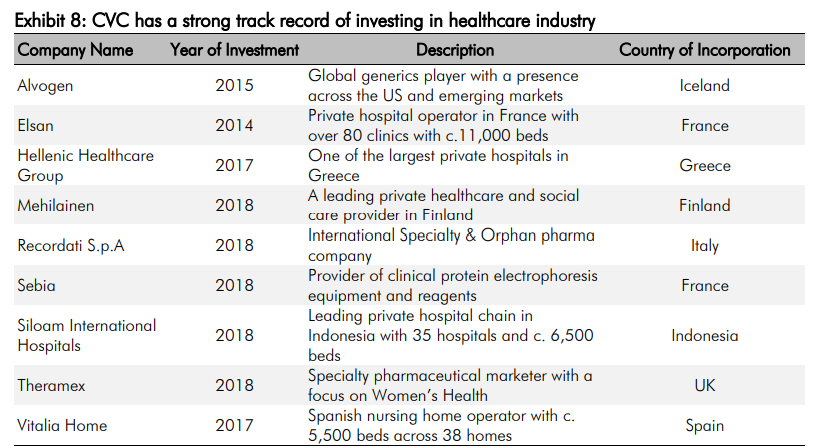

Another interesting event that took place was - Entry of PE fund.

CVC capital brought the majority stake in HCG last year and infused 6.3Bn capital and Dr Ajai (Founder) also infused 200 Mn in the company.

Post the transaction the stake of Dr Ajai has come down to 14%

CVC capital brought the majority stake in HCG last year and infused 6.3Bn capital and Dr Ajai (Founder) also infused 200 Mn in the company.

Post the transaction the stake of Dr Ajai has come down to 14%

Track Record of CVC capital -

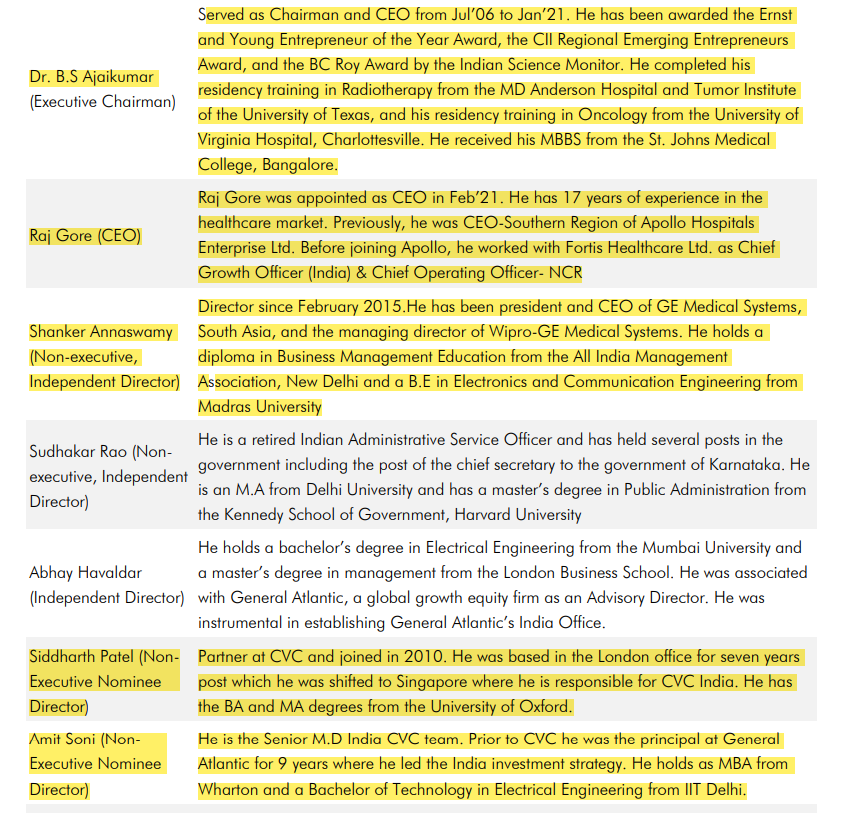

To strengthen the business model, they brought in new CEO Mr Raj Gore.

Mr. Gore has more than 21 years of

diverse experience in business management in North America, Asia, & Africa, with a focus on

healthcare for the past 17 years. His expertise lies in business transformation

Mr. Gore has more than 21 years of

diverse experience in business management in North America, Asia, & Africa, with a focus on

healthcare for the past 17 years. His expertise lies in business transformation

and financial turnaround

of acquired healthcare companies in India, Mauritius, and Vietnam and thus, create a sustainable

growth momentum and value for these organizations. Mr. Gore has brought in several organisational

changes at HCG by hiring a new Sales Head, HR Head, CIO

of acquired healthcare companies in India, Mauritius, and Vietnam and thus, create a sustainable

growth momentum and value for these organizations. Mr. Gore has brought in several organisational

changes at HCG by hiring a new Sales Head, HR Head, CIO

and some new centre heads as well.

Previously, Mr. Gore held the position of CEO-Southern Region at Apollo Hospitals and was

responsible for the company’s largest region of business. Before working at Apollo, he was associated

with another major hospital chain of India, Fortis

Previously, Mr. Gore held the position of CEO-Southern Region at Apollo Hospitals and was

responsible for the company’s largest region of business. Before working at Apollo, he was associated

with another major hospital chain of India, Fortis

Healthcare, as a Chief Growth Officer (India) and

Chief Operating Officer (NCR). This appointment is expected to bring in a positive transformation,

which along with the capital infused by CVC Capital and Dr. Ajai augurs well for the company’

prospects.

Chief Operating Officer (NCR). This appointment is expected to bring in a positive transformation,

which along with the capital infused by CVC Capital and Dr. Ajai augurs well for the company’

prospects.

Here's what the new CEO is planning to do -

And the most important this, the management is walking the talk.

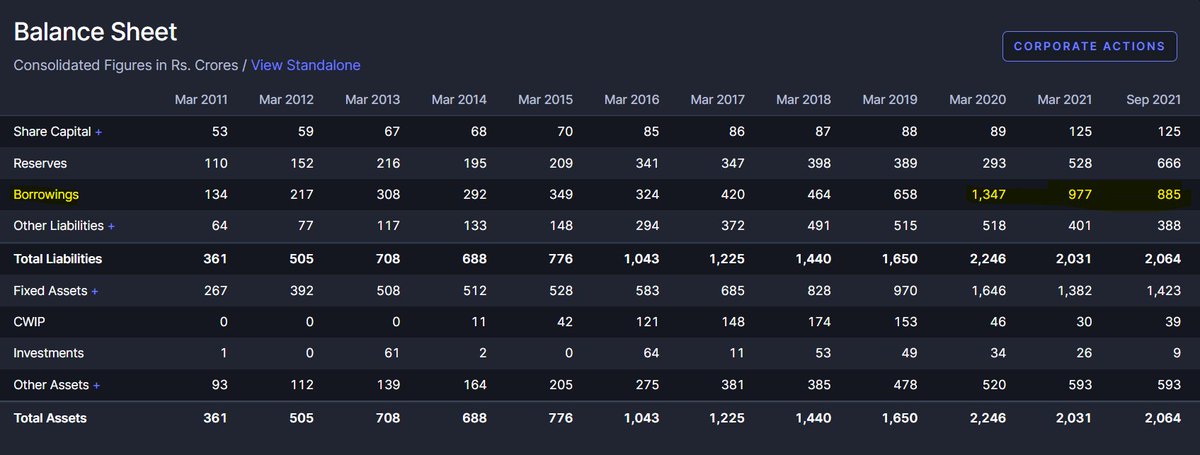

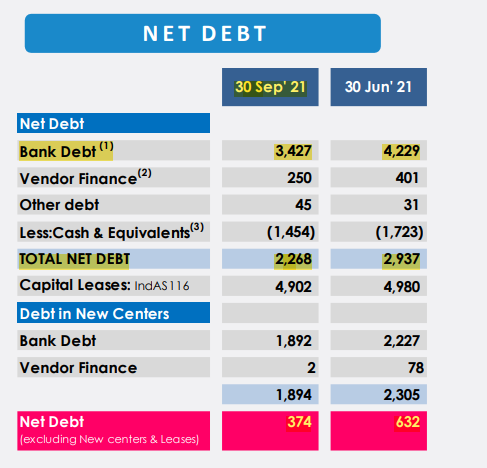

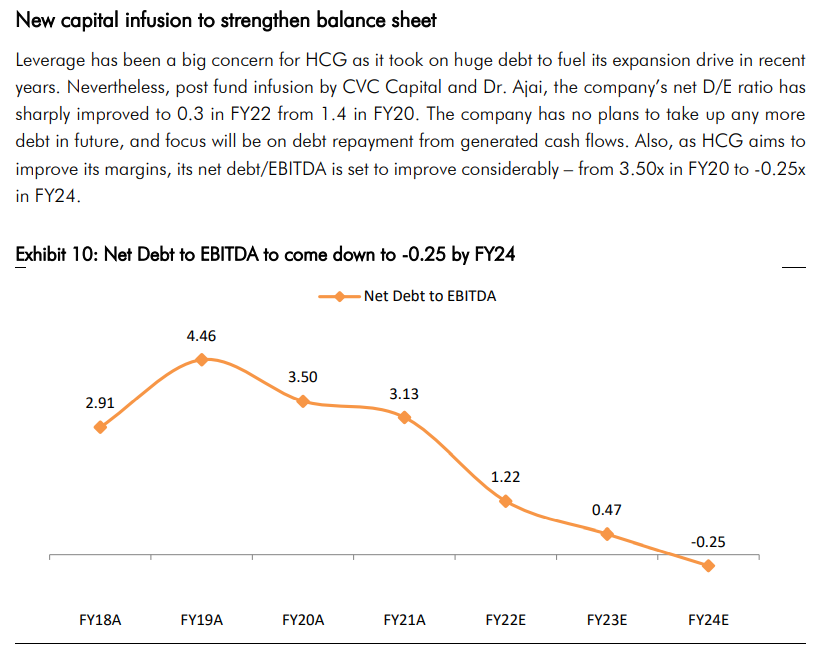

Look at the debt - Post the takeover, the debt has come down from 1325Cr to 885Cr.

Look at the debt - Post the takeover, the debt has come down from 1325Cr to 885Cr.

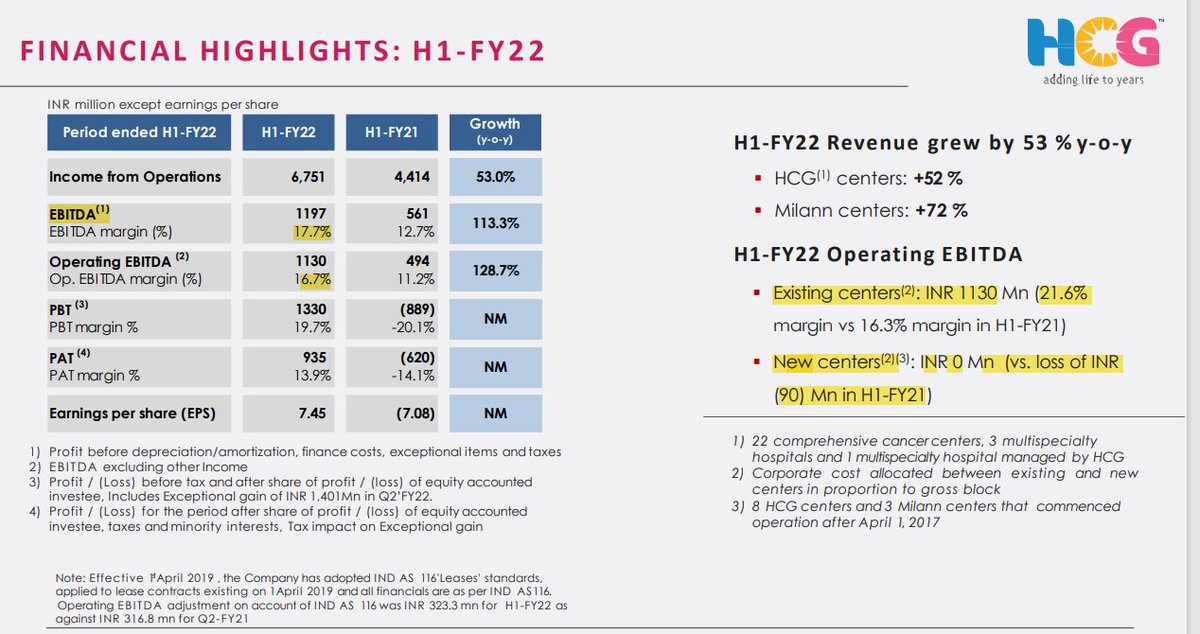

Capex is over and new centers have turned EBITDA positive - Existing Centers margins increased to 21.6%

and overall EBITDA margins increased to 17.4%.

Revenue from new centers grew 56% YoY.

ARPOD of existing centers grew to 40K

and overall EBITDA margins increased to 17.4%.

Revenue from new centers grew 56% YoY.

ARPOD of existing centers grew to 40K

Management -

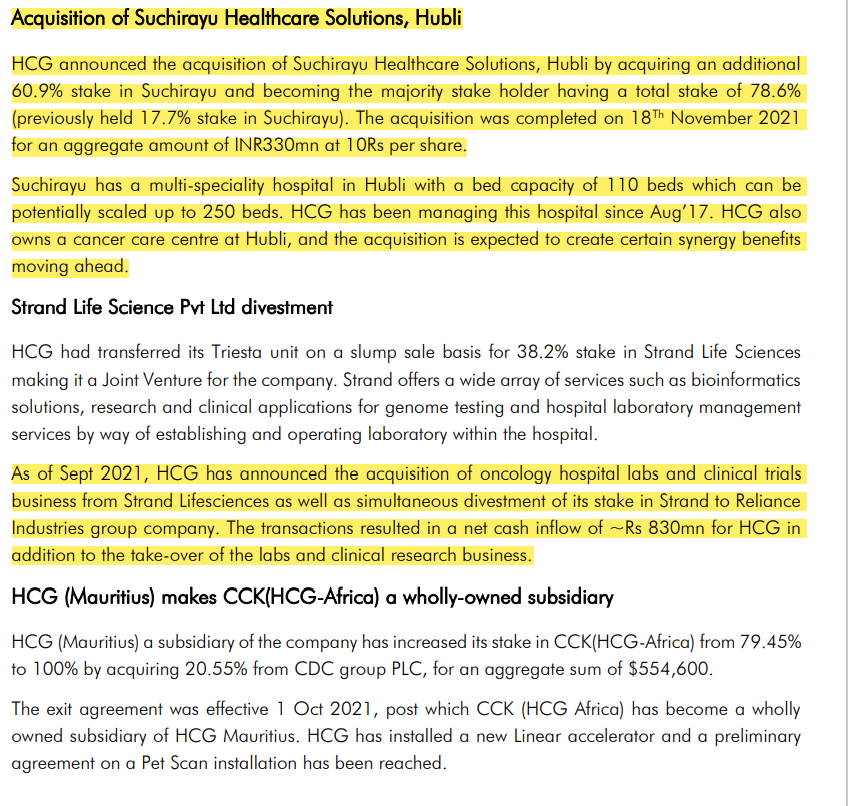

Recent Acquisitions done by the company -

Milan Fertility Centers - Currently contribution only 5% to the topline.

THESIS -

1. Capex is over and as new centers turn EBIDTA positive, bottom line will grow faster than the top line.

2. As the Debt comes down, the lower interest payment will contribute to bottom line.

3. No new capex planned for next 2-3 years and once new centers turn positiv

1. Capex is over and as new centers turn EBIDTA positive, bottom line will grow faster than the top line.

2. As the Debt comes down, the lower interest payment will contribute to bottom line.

3. No new capex planned for next 2-3 years and once new centers turn positiv

the return ratios will improve.

4. Given the future prospects, currently available at cheap valuations as compared to Apollo and Max.

ANTI THESIS -

1. Execution risk - if the new centers take longer than expected to turn positive.

2. Attrition - Doctors moving to another

4. Given the future prospects, currently available at cheap valuations as compared to Apollo and Max.

ANTI THESIS -

1. Execution risk - if the new centers take longer than expected to turn positive.

2. Attrition - Doctors moving to another

hospitals.

3. Debt remains high

4. Margins get suppressed

5. PE fund exiting sooner than expected

6. More capex, if they start expanding in Africa that would again put pressure on return ratios

3. Debt remains high

4. Margins get suppressed

5. PE fund exiting sooner than expected

6. More capex, if they start expanding in Africa that would again put pressure on return ratios

Loading suggestions...