Neuland concall happened yesterday. 🌋🗻

Here are my key takeaways:

1. Prime segment degrew 20% compared to last year Q average

In b/w lines: there has been inventory stocking at the client side. In addition some orders for levetiracetam & mirtazapine have not come through

Here are my key takeaways:

1. Prime segment degrew 20% compared to last year Q average

In b/w lines: there has been inventory stocking at the client side. In addition some orders for levetiracetam & mirtazapine have not come through

This could be client losing market share as well. But neuland has not lost any client. They expect this to normalize in fy23.

2. Margins are down as well. Better than q4fy21 but worse than Q2fy22

in b/w lines: As they explained in last quarter concall, some of their Rae material annual contracts were expiring in Q2 so this was expected to happen. this has also been on account of logistics costs.

in b/w lines: As they explained in last quarter concall, some of their Rae material annual contracts were expiring in Q2 so this was expected to happen. this has also been on account of logistics costs.

Another reason was like in previous quarters unit 3 has only been partly utilized & the opex is hitting the p&l.

No further commentary on future margins. My assumption is that their guidance on 20% ebitda margins holds but will take time to materialize.

No further commentary on future margins. My assumption is that their guidance on 20% ebitda margins holds but will take time to materialize.

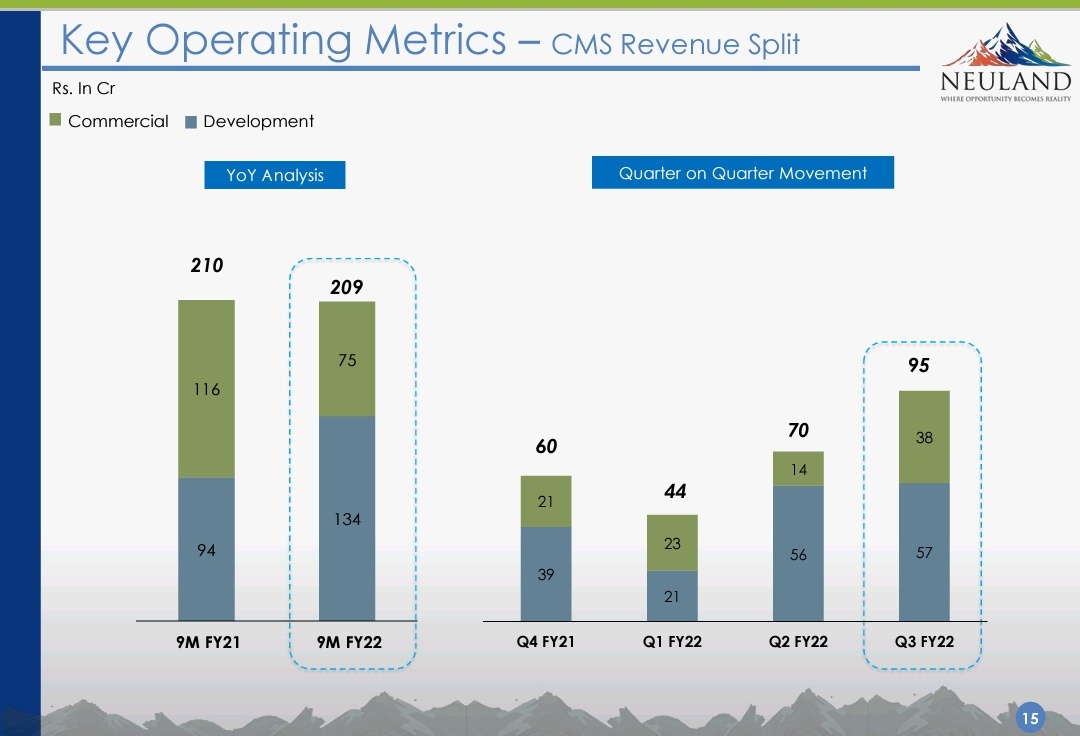

3. Cms revenues are at an all time high, near 100cr for the first time.

In b/w lines: the commercial revenues are down because of patent expiry for 1 molecule. Ex that molecule commercial revenues are growing 20-25% approx.

Pipeline is strong.

In b/w lines: the commercial revenues are down because of patent expiry for 1 molecule. Ex that molecule commercial revenues are growing 20-25% approx.

Pipeline is strong.

Quality of revenue is improving. Larger molecules. More molecules which could become blockbusters. Now guidance is for 2 of the cms molecules to get commercialized in next 18-24 months. They have been conservative in their revenue projections & capacity planning.

If need arises can always put up new capex.

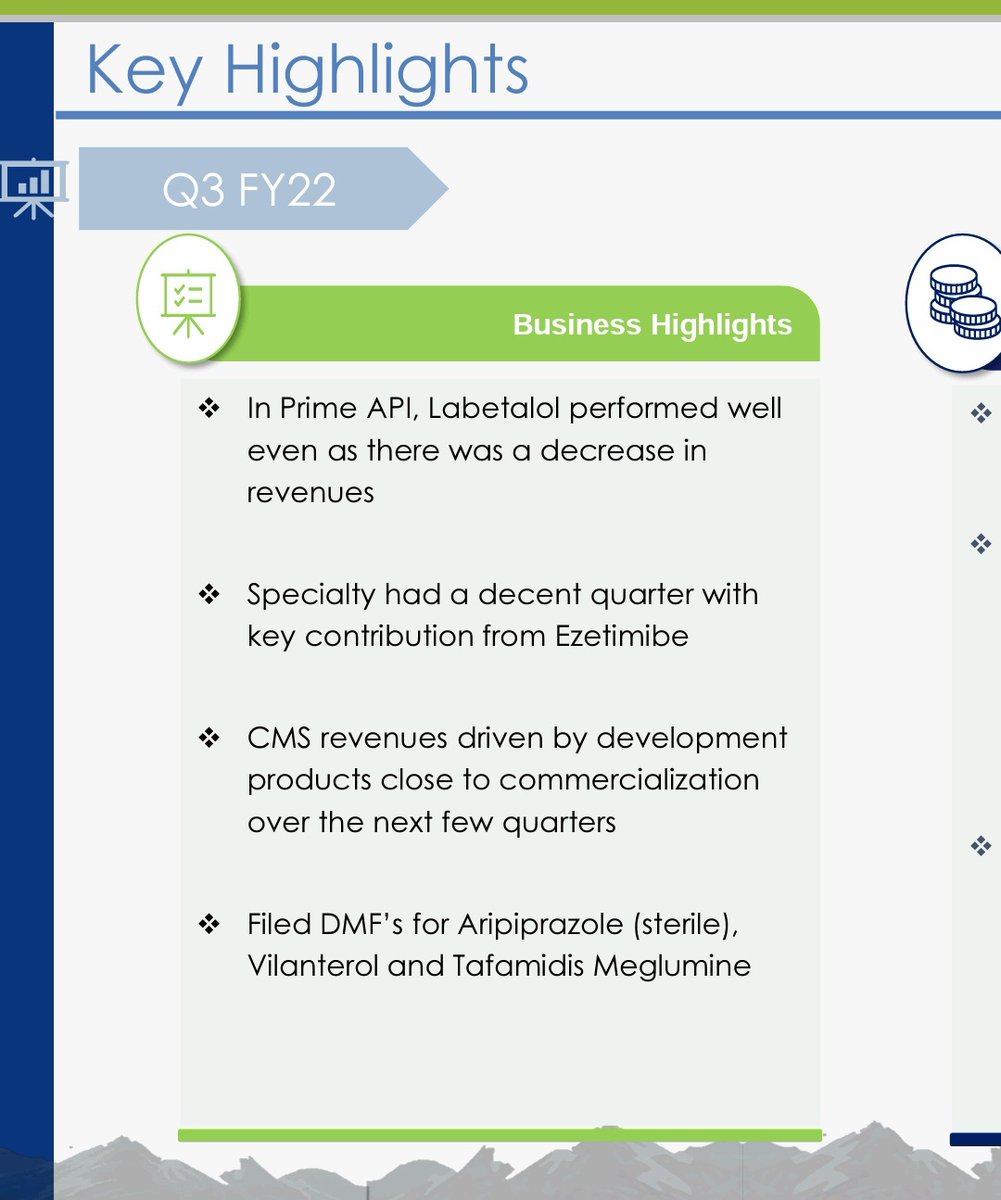

4. Gds is being strengthened with 3 new DMF filings.

In b/w lines: Aripiprazole (sterile), Vilanterol and Tafamidis Meglumine.

Each could be a 20M $ api opportunity. Patent expiry in 3 years. Will get development revenue before.

4. Gds is being strengthened with 3 new DMF filings.

In b/w lines: Aripiprazole (sterile), Vilanterol and Tafamidis Meglumine.

Each could be a 20M $ api opportunity. Patent expiry in 3 years. Will get development revenue before.

My thoughts:this is proving to be a case of a biz which is too complex to get right. If cms fires, gds disappoints, if gds delivers, cms disappoints. Such things are to be expected with a microcap of this size imo. Results have definitely been disappointing but but unexpected

We have to see how the cms pipeline pans out in next 18-24 months since that was always the thesis.

Have to see biz performance in non COVID times.

Disclaimer : i am invested & biased. This is not a reco. Do your own due diligence.

Have to see biz performance in non COVID times.

Disclaimer : i am invested & biased. This is not a reco. Do your own due diligence.

Just to add another disclaimer that no changes in my position size since results.

Might change my mind with better execution OR if valuations give more comfort.

Might change my mind with better execution OR if valuations give more comfort.

Loading suggestions...