Lux Industries conducted the conference call for Q3 FY22.

"Mr Todi will demonstrate to SEBI for no violation & will not attend any Board Meeting until matter resolved.

There is no criminal liability announced till now"

Here are the conference call highlights

🧵👇

"Mr Todi will demonstrate to SEBI for no violation & will not attend any Board Meeting until matter resolved.

There is no criminal liability announced till now"

Here are the conference call highlights

🧵👇

Business Updates:

• Co. has outperformed indusry with increasing market share.

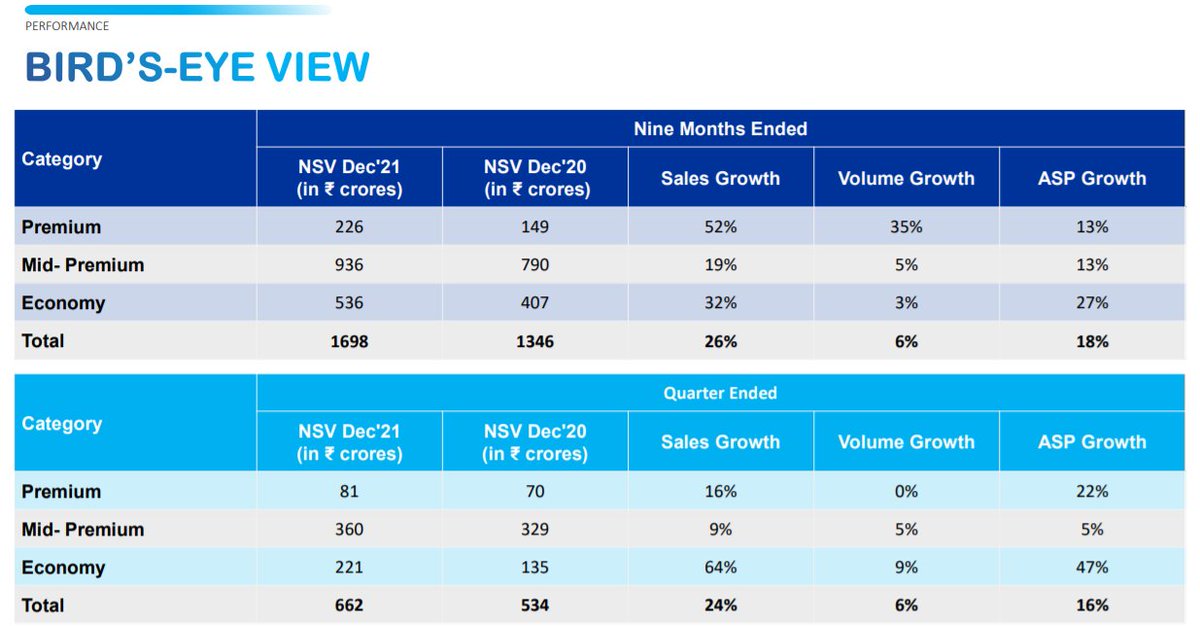

• Premium & Economy category has best quarter: Growing 16% & 64% respectively on YoY basis.

• Mid-Premium segment grew 9%, however thermal wear witness slight weakness, due to change in season.

• Co. has outperformed indusry with increasing market share.

• Premium & Economy category has best quarter: Growing 16% & 64% respectively on YoY basis.

• Mid-Premium segment grew 9%, however thermal wear witness slight weakness, due to change in season.

Industry Updates:

• Rising consumption was across all region.

• Economic activity expected to recover to normal resulting in increasing in business.

• Women's market share of Lux is increasing due to better quality than competitors.

• Mgmt expect to beat the industry by 2-3%

• Rising consumption was across all region.

• Economic activity expected to recover to normal resulting in increasing in business.

• Women's market share of Lux is increasing due to better quality than competitors.

• Mgmt expect to beat the industry by 2-3%

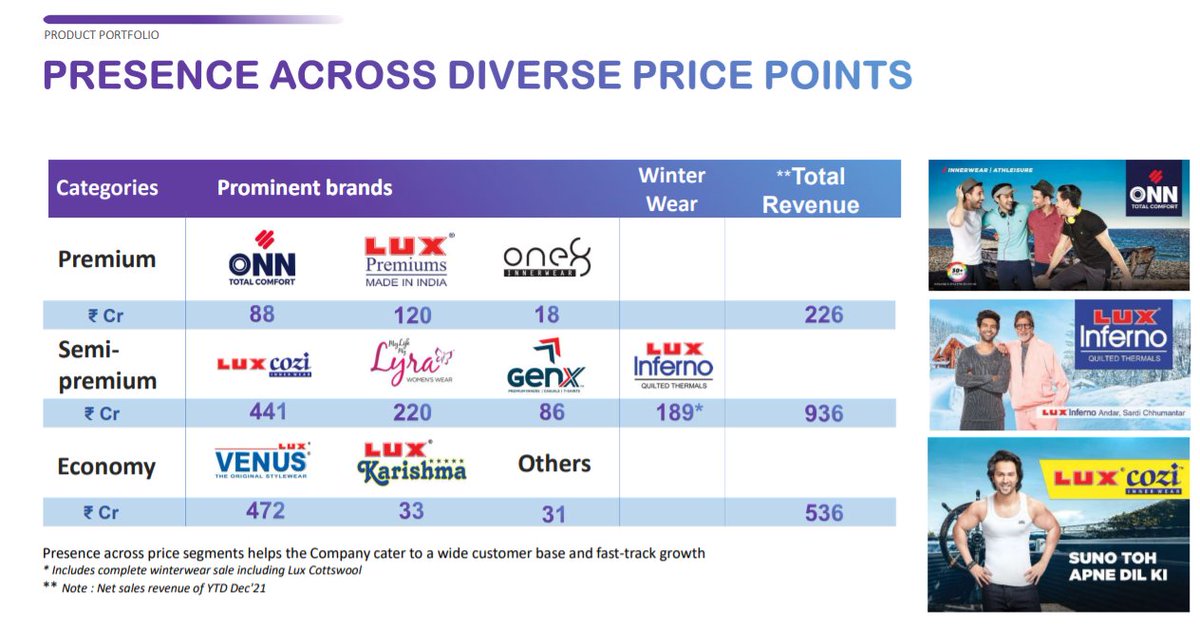

Revenue Share

- Premium Wear: 13% (11% last year)

- Mid Premium: 55%

- Economy: 32%

Volume:

- Total Volume growth:6%

- ASP Growth 16%.

• Winter wear sales didn't work that well for the industry.

• In Q4 Economy will have good volume growth (esp in Feb & march).

- Premium Wear: 13% (11% last year)

- Mid Premium: 55%

- Economy: 32%

Volume:

- Total Volume growth:6%

- ASP Growth 16%.

• Winter wear sales didn't work that well for the industry.

• In Q4 Economy will have good volume growth (esp in Feb & march).

Lyra:

• Lyra: 13% of net sales.

With increase in product basket target remains to make it 500cr brand. 80% bottom wear & 10% each for inner wear and Lounge wear.

• Inner ware in Lyra brand is expected to show more contribution.

• Lyra: 13% of net sales.

With increase in product basket target remains to make it 500cr brand. 80% bottom wear & 10% each for inner wear and Lounge wear.

• Inner ware in Lyra brand is expected to show more contribution.

Segmental Growth:

• Premium wear market is consolidating with few player.

• Mid Premium wear has very few player, where mgmt expect Lyra would see good recognition due to new marketing spend.

• Mgmt expect premium category to growth with expectation of increase in 5-6%.

• Premium wear market is consolidating with few player.

• Mid Premium wear has very few player, where mgmt expect Lyra would see good recognition due to new marketing spend.

• Mgmt expect premium category to growth with expectation of increase in 5-6%.

Geographic Revenue Share:

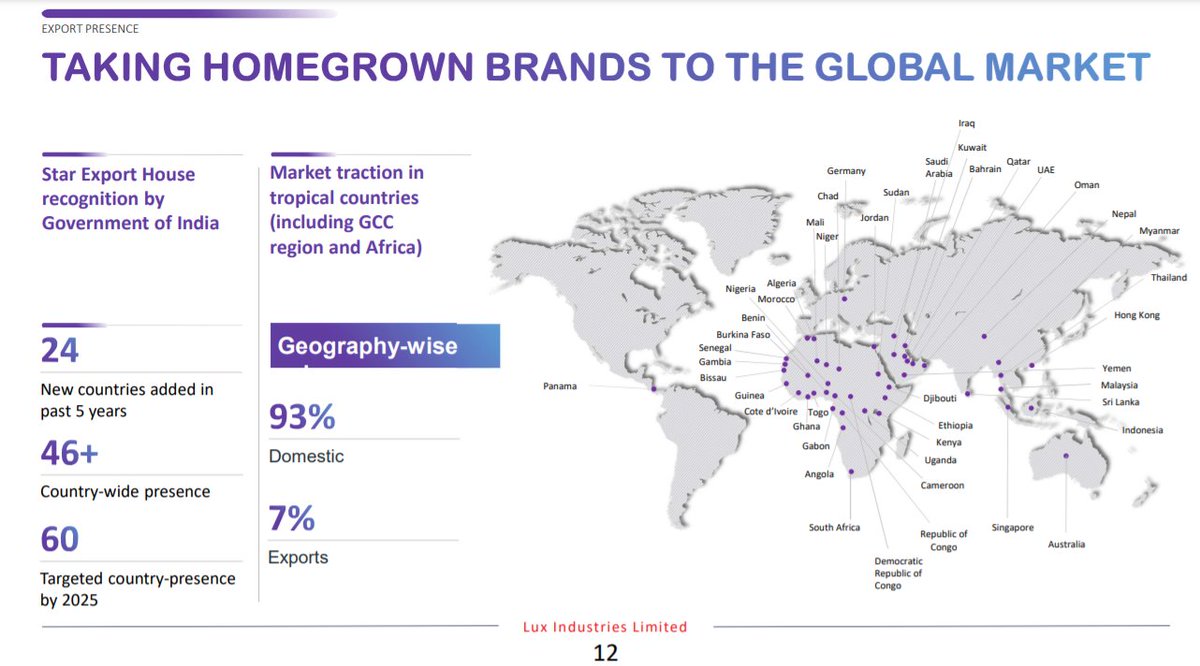

• In Domestic Market volume growth in ON (Premium segment) was 9-10%+, however the export market has de-growth.

• Export market remain very tight in terms of competition where it is difficult for co. to pass on the prices to customer.

• In Domestic Market volume growth in ON (Premium segment) was 9-10%+, however the export market has de-growth.

• Export market remain very tight in terms of competition where it is difficult for co. to pass on the prices to customer.

Margin:

• Margins remain best in the industry and mgmt expect it to remain same.

• Gross Margins improved due to product mix and gain from old raw material at lower cost.

• For new raw material price will passed onto customer.

• Margins remain best in the industry and mgmt expect it to remain same.

• Gross Margins improved due to product mix and gain from old raw material at lower cost.

• For new raw material price will passed onto customer.

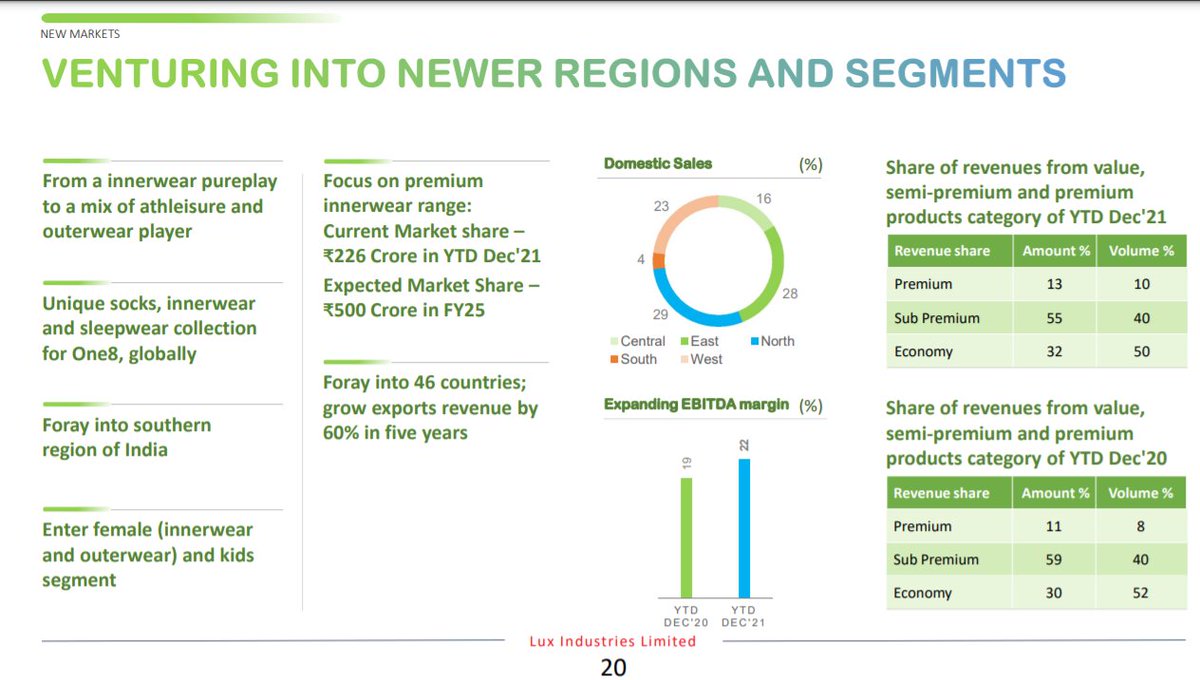

Region Wise Revenue Share:

- Northern: 29%

- Eastern: 28%

- Western: 23%

- Central: 16%

- Southern: 2%

In South India market, co. will start with entire product basket launching.

• EBO is working well, but no clear picture as of now.

- Northern: 29%

- Eastern: 28%

- Western: 23%

- Central: 16%

- Southern: 2%

In South India market, co. will start with entire product basket launching.

• EBO is working well, but no clear picture as of now.

Marketing:

• This was due to marketing & branding spend, resulting in increasing customer.

• 749 cr spent over last 5 year (8% of revenue) from which 15.7Rs was earned on 1 Rs spend.

• 108 cr was spend in FY 22 (6.4% of Net Sales).

• Marketing spend will now be subsidized

• This was due to marketing & branding spend, resulting in increasing customer.

• 749 cr spent over last 5 year (8% of revenue) from which 15.7Rs was earned on 1 Rs spend.

• 108 cr was spend in FY 22 (6.4% of Net Sales).

• Marketing spend will now be subsidized

Channel Partner:

• Distribution Channel: 1170+

• Dealer Attrition <1%

• Revenue per Distributor has increased.

• Depots & Warehouse: 12 & 19 respectively.

• Shipping 4000+ online orders per day & aim to generate 100cr in online revenue over next 3 year.

• Distribution Channel: 1170+

• Dealer Attrition <1%

• Revenue per Distributor has increased.

• Depots & Warehouse: 12 & 19 respectively.

• Shipping 4000+ online orders per day & aim to generate 100cr in online revenue over next 3 year.

Other:

• Working Capital Cycle: 168 days Higher inventory in RM & finished product.

• Mgmt expect Working Capital to decrease over coming period.

• Cash at hand: 164cr.

• Working Capital Cycle: 168 days Higher inventory in RM & finished product.

• Mgmt expect Working Capital to decrease over coming period.

• Cash at hand: 164cr.

Loading suggestions...