VRL Logistics conducted the conference for Q3 FY22.

Here are the conference call highlights

🧵👇

Here are the conference call highlights

🧵👇

Business Updates:

• Business volume increased in Good Transport business.

• Overall diesel cost reduced by 12Rs per litre due to govt. reduction of duties. Cost of diesel restricted to 29%, else it would be higher.

• Post this bio-diesel was not feasible, hence share reduced.

• Business volume increased in Good Transport business.

• Overall diesel cost reduced by 12Rs per litre due to govt. reduction of duties. Cost of diesel restricted to 29%, else it would be higher.

• Post this bio-diesel was not feasible, hence share reduced.

Industry Updates:

• With expansion in different geographies, revenue will be expected to increase.

• Major growth contribution is coming from textile, where contribution has increased from 16% to 19%.

• Agriculture Commodities share increased from 8% to 12%.

• With expansion in different geographies, revenue will be expected to increase.

• Major growth contribution is coming from textile, where contribution has increased from 16% to 19%.

• Agriculture Commodities share increased from 8% to 12%.

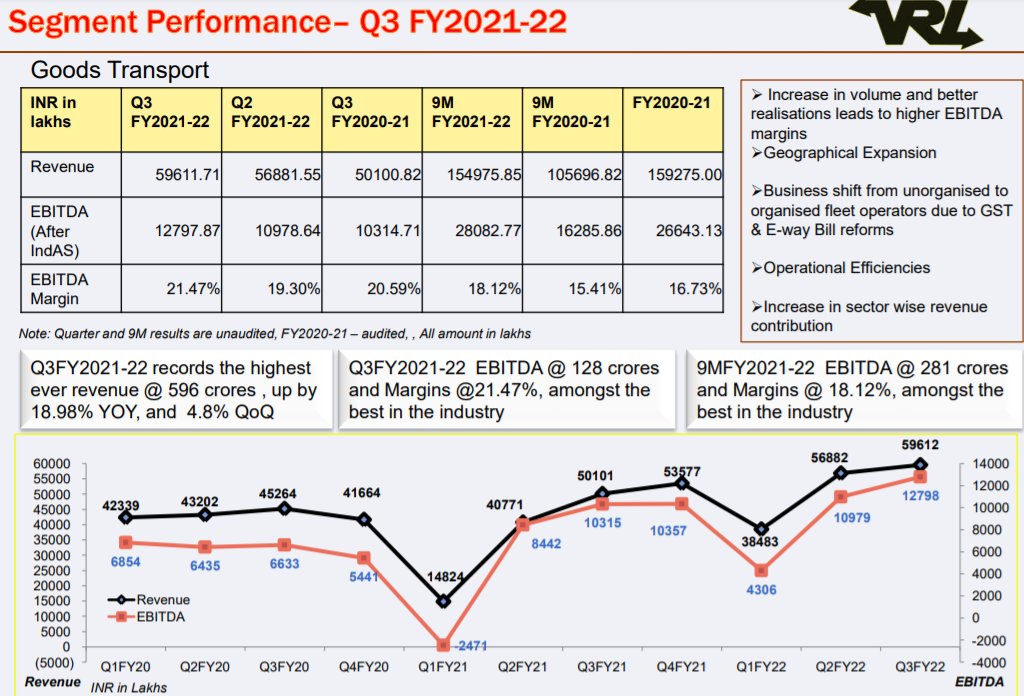

Good Transport Business

• YoY Growth: 19% (Realization growth 7%, increase in tonnage 11).

• Increase in tonnage was on account of addition of new customer, expansion in untap market & shifting of customer from unorganized market to organized market.

• YoY Growth: 19% (Realization growth 7%, increase in tonnage 11).

• Increase in tonnage was on account of addition of new customer, expansion in untap market & shifting of customer from unorganized market to organized market.

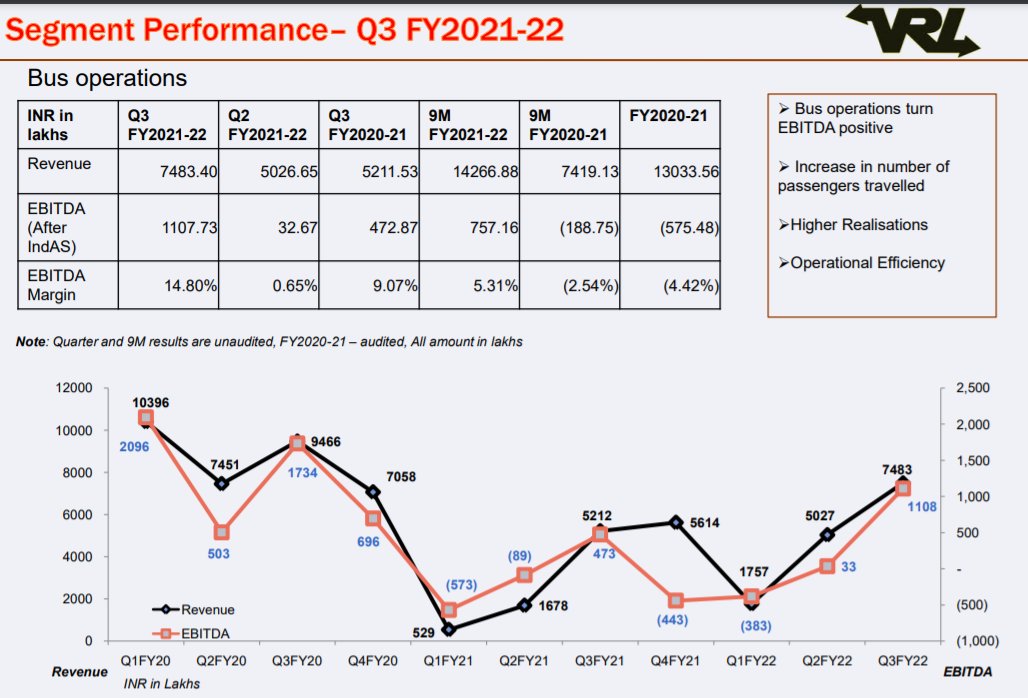

Bus Operation:

• Business grew inspite of decrease in 45 buss. Growth was witnessed due to increase in passenger, increase in seat occupation & increasing realization.

• No of bus increased to 280 buses

• With reduction in buses revenue will be less but margins will be higher

• Business grew inspite of decrease in 45 buss. Growth was witnessed due to increase in passenger, increase in seat occupation & increasing realization.

• No of bus increased to 280 buses

• With reduction in buses revenue will be less but margins will be higher

Utilization

- Hub to Hub: 100%

- Hub to Spoke: 65-70%

- Passenger Vehicle: 85% (1,100 Rs per passenger- which was 1,047 Rs in Q2)

Surat: 3Lack Tone facility, with improvement of 22% tonnage.

- Hub to Hub: 100%

- Hub to Spoke: 65-70%

- Passenger Vehicle: 85% (1,100 Rs per passenger- which was 1,047 Rs in Q2)

Surat: 3Lack Tone facility, with improvement of 22% tonnage.

Price Rise:

• There wont be reduction in the customer price for diesel cost.

• Freight rates are expected to remain at same level, hence the co. will not decrease the price.

• With respect to retail, prices of diesel will be cheaper for VRL for atleast 3-4Rs per litre.

• There wont be reduction in the customer price for diesel cost.

• Freight rates are expected to remain at same level, hence the co. will not decrease the price.

• With respect to retail, prices of diesel will be cheaper for VRL for atleast 3-4Rs per litre.

Margins:

• Employee cost are expected to increase by 10% in Q4. However with reduction in diesel price margins are expected to be maintained.

• Increase in realization in expected to be bus, which will result in increase in margin.

• Employee cost are expected to increase by 10% in Q4. However with reduction in diesel price margins are expected to be maintained.

• Increase in realization in expected to be bus, which will result in increase in margin.

Raw Material:

• Benefit of fuel price was there 2 months, if the price don't rise then there would be benefit for 1 more months.

• With Bio-fuel not feasible as of now, the share is reduce. However co. is flexible to usage in terms of price.

• Benefit of fuel price was there 2 months, if the price don't rise then there would be benefit for 1 more months.

• With Bio-fuel not feasible as of now, the share is reduce. However co. is flexible to usage in terms of price.

CAPEX:

• CAPEX: 167 cr for FY22 of which 107 cr is spend in Good Transport.

• There would be no expansion in bus segment for near term.

• With co. current cash flow co. will be able to spend capex & remaining amount be utilized to pay off the debt.

• CAPEX: 167 cr for FY22 of which 107 cr is spend in Good Transport.

• There would be no expansion in bus segment for near term.

• With co. current cash flow co. will be able to spend capex & remaining amount be utilized to pay off the debt.

Other:

• Net Debt: 101 cr. Mgmt expect Net Debt to reach to mere 30-35cr Net Debt next year- (if there are no unplanned capex)

• Plan to increase 100+ branches in eastern & north eastern market for which 60 are already open.

End

• Net Debt: 101 cr. Mgmt expect Net Debt to reach to mere 30-35cr Net Debt next year- (if there are no unplanned capex)

• Plan to increase 100+ branches in eastern & north eastern market for which 60 are already open.

End

Loading suggestions...