Business

Economics

employment

Industry

Textile Industry

textiles

Manufacturing sector

Export industry

Contents:

1) Why r we discussing this

2) The trigger - a strong one

3) Value chain and positioning

4) Cyclicality - how to ride a dragon

5) Interesting valuation

6) Antithesis

1) Why r we discussing this

2) The trigger - a strong one

3) Value chain and positioning

4) Cyclicality - how to ride a dragon

5) Interesting valuation

6) Antithesis

1) Why this:

Textile is India's oldest manufacturing sector. World's 2nd largest producer, 5th exporter and 2nd domestic employer - all these cos world's cheapest raw cotton availability here. So a fragmented market with many small players as barrier to entry becomes low.

Textile is India's oldest manufacturing sector. World's 2nd largest producer, 5th exporter and 2nd domestic employer - all these cos world's cheapest raw cotton availability here. So a fragmented market with many small players as barrier to entry becomes low.

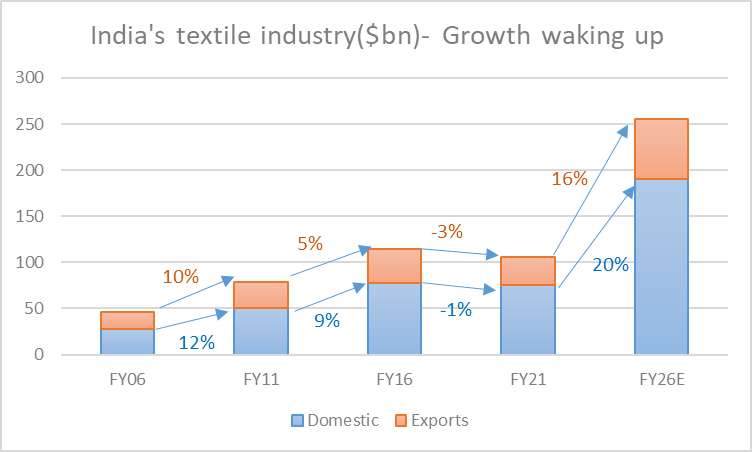

1a) Govt was expecting this slow growing sector to get a domestic consumption boost - thnks to ecom penetration - but something else unfolded in 2021

2) The Trigger in Textile:

China is the largest exporter ($250b) and USA the consumer, but US banned Xinjiang cotton siting human rights labor issues - well Xinjiang produces 85% of Chinese cotton. India has 25% of world's cotton production, hence a boost to cotton & yarn export

China is the largest exporter ($250b) and USA the consumer, but US banned Xinjiang cotton siting human rights labor issues - well Xinjiang produces 85% of Chinese cotton. India has 25% of world's cotton production, hence a boost to cotton & yarn export

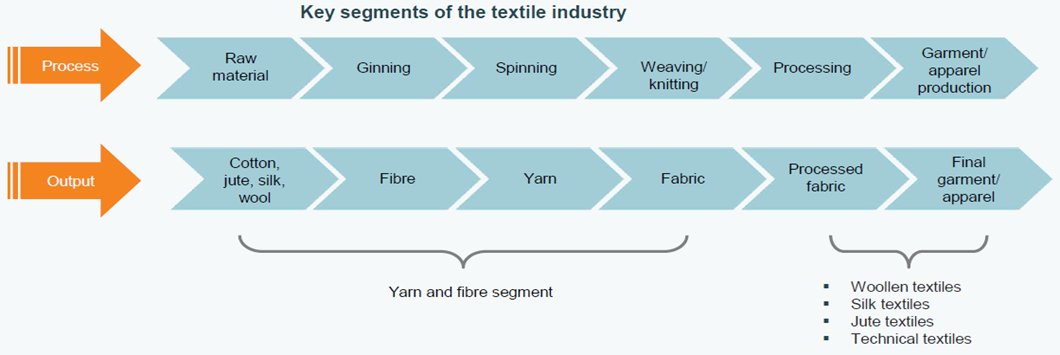

Lets und the value chain quickly before further details

3) Value chain:

Cotton is used to make yarn and fibers which are processed to make garments. Raw cotton is used in a spindle to make yarn in multiple blends (with polyester/rayon etc) as needed.

3) Value chain:

Cotton is used to make yarn and fibers which are processed to make garments. Raw cotton is used in a spindle to make yarn in multiple blends (with polyester/rayon etc) as needed.

3a) Most large exporters except China (esp Bangladesh & Vietnam) are prominent in garments with smaller yarn capacity vs India. Also, importing yarn is more viable than cotton for them. So Indian yarn spinners got exceptional export demand from all over all of a sudden.

3b) Covid19 took out 5-6% of Indian spinning capacity which is a plus.

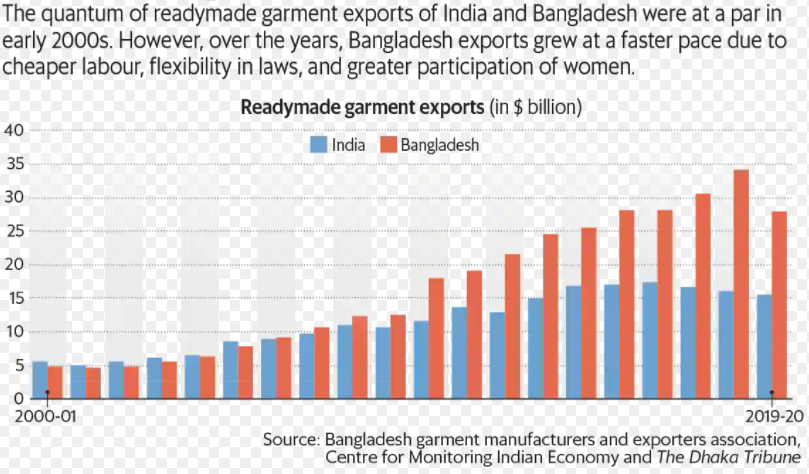

Similar story for Indian apparel players as US's import duty is 9.5% for India vs 11% Bangla, 13% Vietnam. So China+1 demand started coming in. in EU & UK, Bangla and Viet are leaders given there signed FTAs

Similar story for Indian apparel players as US's import duty is 9.5% for India vs 11% Bangla, 13% Vietnam. So China+1 demand started coming in. in EU & UK, Bangla and Viet are leaders given there signed FTAs

4) Cyclicality: How to ride and exit

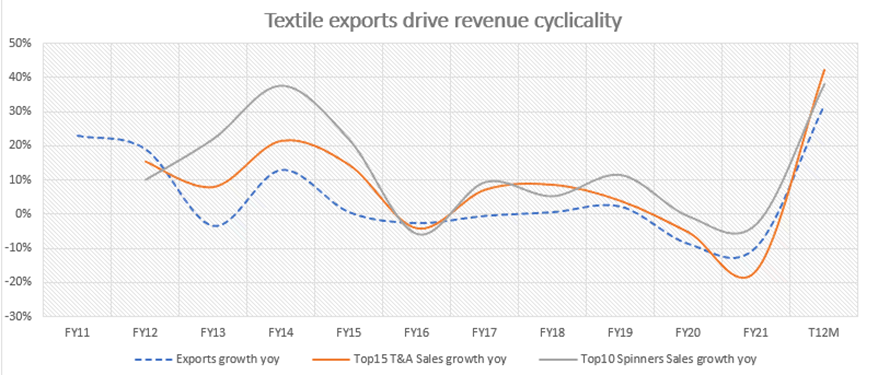

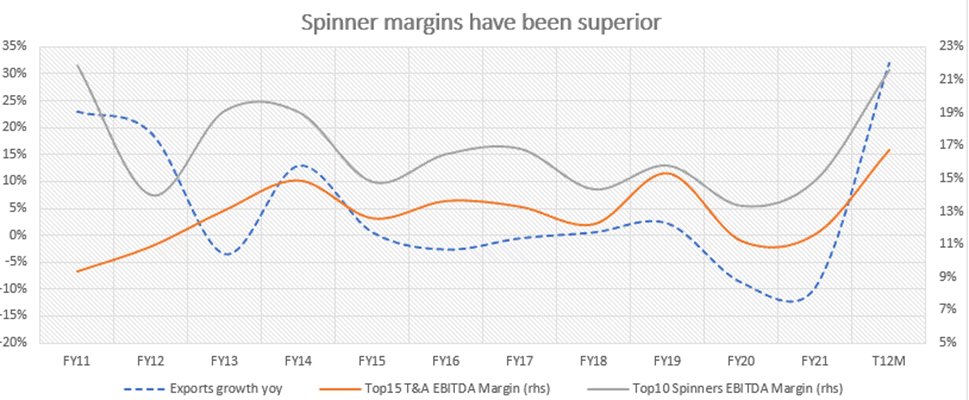

Lets address the elephant - spinning is still commoditized and cyclical. I aggregated 15 large listed T&A players and 10 listed specialist spinners to gain this interesting insight 👇

Sorry if it's bit technical for some-read the conclusion

Lets address the elephant - spinning is still commoditized and cyclical. I aggregated 15 large listed T&A players and 10 listed specialist spinners to gain this interesting insight 👇

Sorry if it's bit technical for some-read the conclusion

4a) Exports are the drivers of cycles historically - they drive the topline heavily. But spinners have been managing margins better than the industry. is that dexterity in fixed cost management that I am seeing?

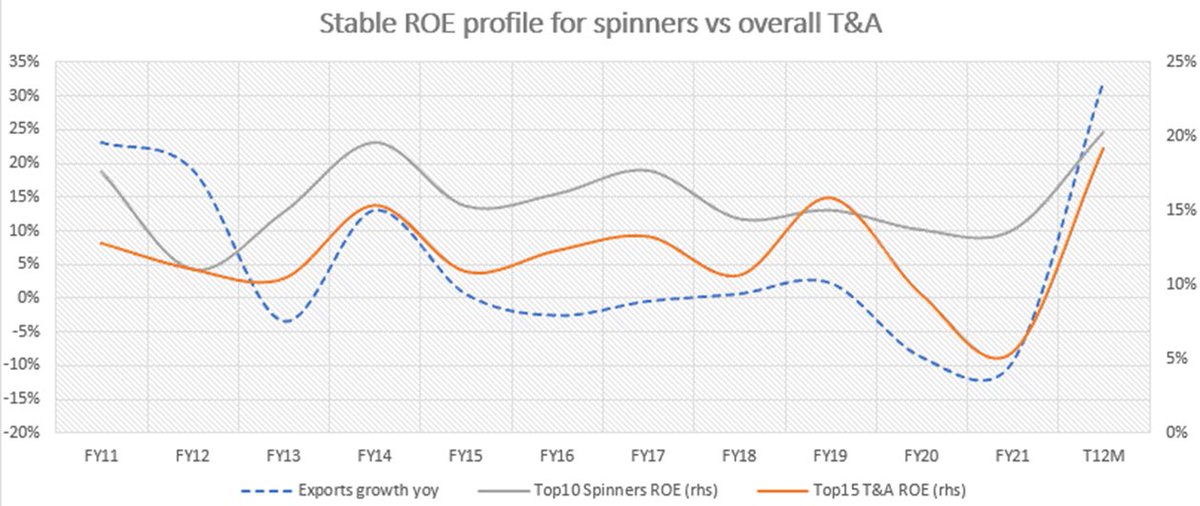

4b) Surprised to see consistent returns in the most perceived commoditized business of spinning when garments seem more inconsistent. I don't mind a trough 10% roe if my peak could go to 30%+

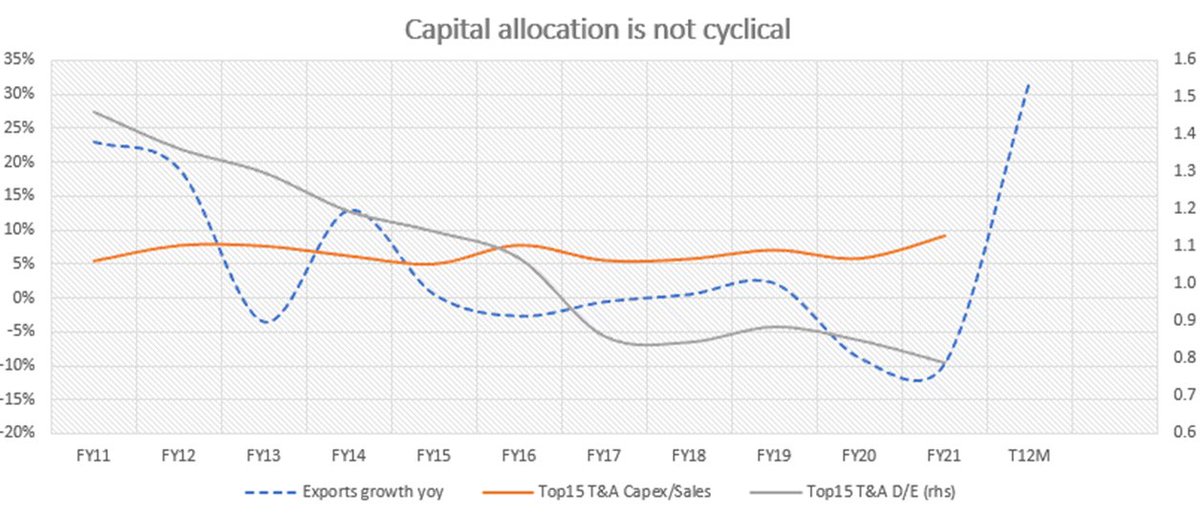

4c) Overall industry has been consistently deleveraging while capex is not much. This export demand could spur some capex and hence growth.

4d) Conclusion: Spinners look to b better placed vs fiber or garment players given direct demand from china+1 and better margins across cycles (if India signs FTA with EU then apparels could improve growth and margins).

4e ) Conclusion: Spinners hv maintained margin and roe even 2-3 years into export slowdown - ample exit opportunities in my view - while upcycle brings in higher profit growth given cost management. Capex and scale after a decade of downcycle cd be a key.

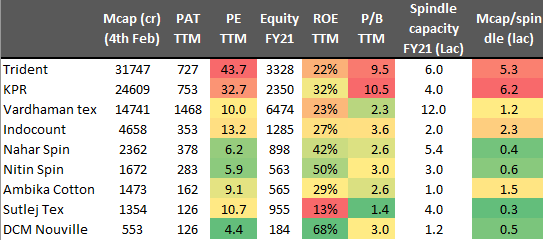

5) Valuation: subjective area alert

No view here as some could look at it as a value traps and some see rerating. (just a random list and not a reco- please do your due diligence)

No view here as some could look at it as a value traps and some see rerating. (just a random list and not a reco- please do your due diligence)

6) Antithesis:

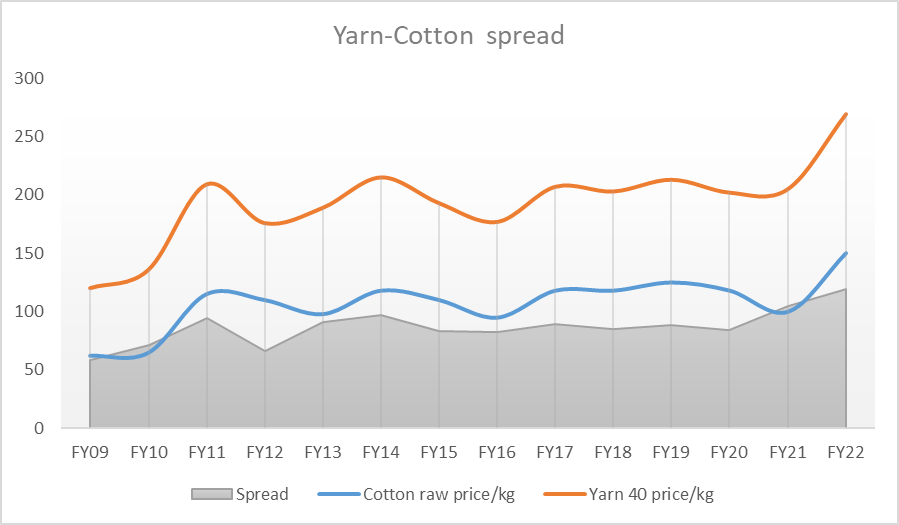

-What if cotton prices sky rocket due to unavailability of cottons from china (metal story of 2021). Spinners make money of yarn to raw cotton spread which has been good so far which shows high pricing power in an upcycle - but low in downcycles for sure.

-What if cotton prices sky rocket due to unavailability of cottons from china (metal story of 2021). Spinners make money of yarn to raw cotton spread which has been good so far which shows high pricing power in an upcycle - but low in downcycles for sure.

6a) -Bangladesh and Vietnam have lower labor cost - focus on yarn capacity expansion with favorable govt policies could slowdown India's yarn demand.

- Excess capex in upcycle could make overcapacity - happens in most commoditized industries

- Excess capex in upcycle could make overcapacity - happens in most commoditized industries

7) Disc: invested and biased, pls do your own due diligence and don't take this as any sort of reco

Source: lot of reading throughout all channels such as IBEF, industry notes, news and blogs. Thanks @screener_in, @Trendlyne & @finologyticker for handy financials and reports

Source: lot of reading throughout all channels such as IBEF, industry notes, news and blogs. Thanks @screener_in, @Trendlyne & @finologyticker for handy financials and reports

Please RT for maximum reach and benefit of knowledge seekers like us 🧐🧐

Your RTs, likes and comments are our fuel of motivation

Your RTs, likes and comments are our fuel of motivation

Loading suggestions...