A thread🧵 on JUBILANT INGREVIA

Please like share and re-tweet for wider reach

I'm sure many of you have heard the name of this company, 3-4 months ago, it was darling of the market but not many people many are taking about it anymore.

Why?

Please like share and re-tweet for wider reach

I'm sure many of you have heard the name of this company, 3-4 months ago, it was darling of the market but not many people many are taking about it anymore.

Why?

Let's try to find out.

1st we're gonna take a look at the business and do a deep dive on what they actually do and after that the reason why not many people are taking about it anymore.

First let's start with the company's HISTORY -

1st we're gonna take a look at the business and do a deep dive on what they actually do and after that the reason why not many people are taking about it anymore.

First let's start with the company's HISTORY -

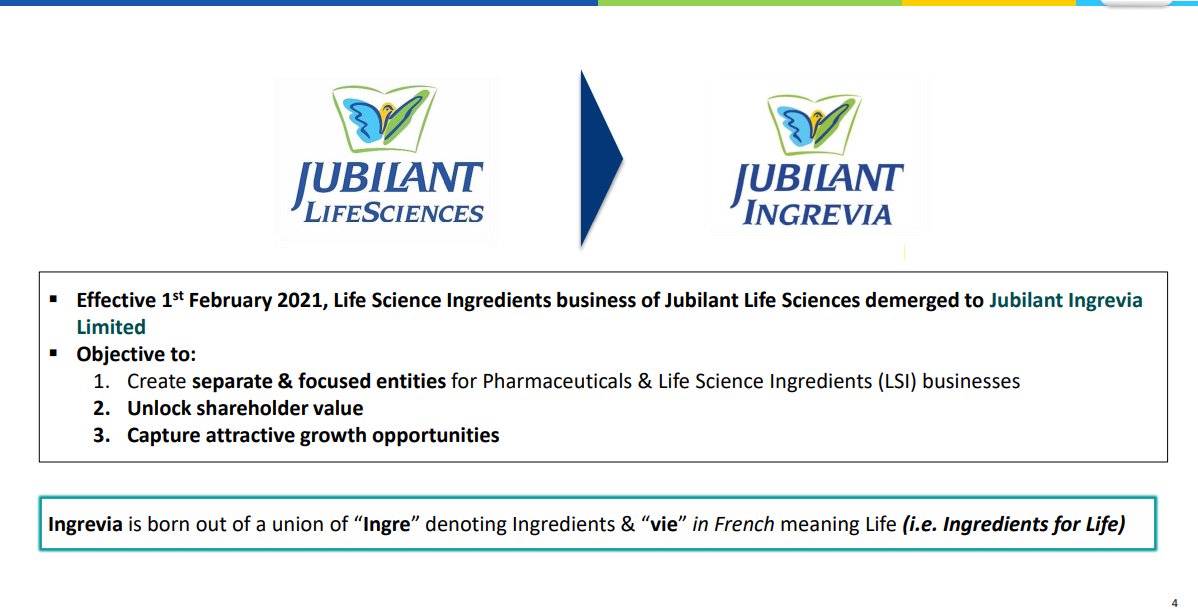

Jubilant Ingrevia was formed after the de-merger of erstwhile Jubilant Life sciences.

Jubilant Lifesciences was de-merged into two separate listed entities -

1. Jubilant Ingrevia (Which holds their life sciences and specialty chemical business)

Jubilant Lifesciences was de-merged into two separate listed entities -

1. Jubilant Ingrevia (Which holds their life sciences and specialty chemical business)

2. Jubilant Pharmova (Specialty Pharmaceuticals

Radiopharma, Allergy Immunotherapy, CDMO, Generics)

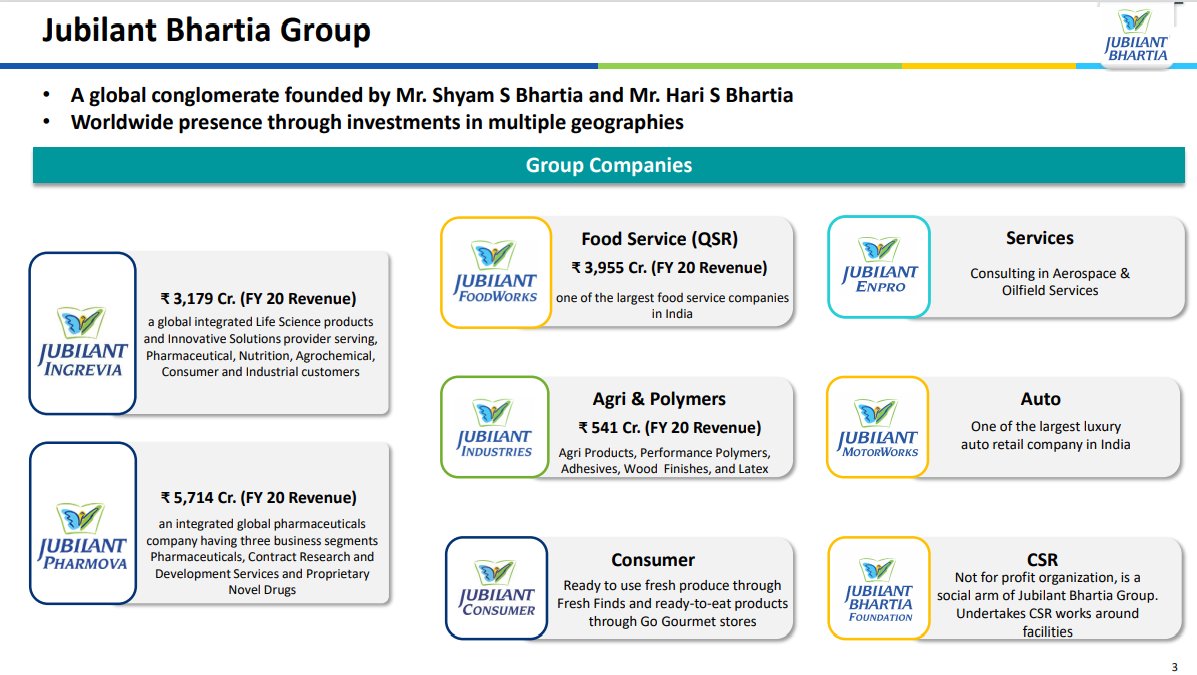

Jubilant Ingrevia is a part of Jubilant Bhartia Group which is diversified group present in QSR, Agri, Consumer, Services & Auto business.

Radiopharma, Allergy Immunotherapy, CDMO, Generics)

Jubilant Ingrevia is a part of Jubilant Bhartia Group which is diversified group present in QSR, Agri, Consumer, Services & Auto business.

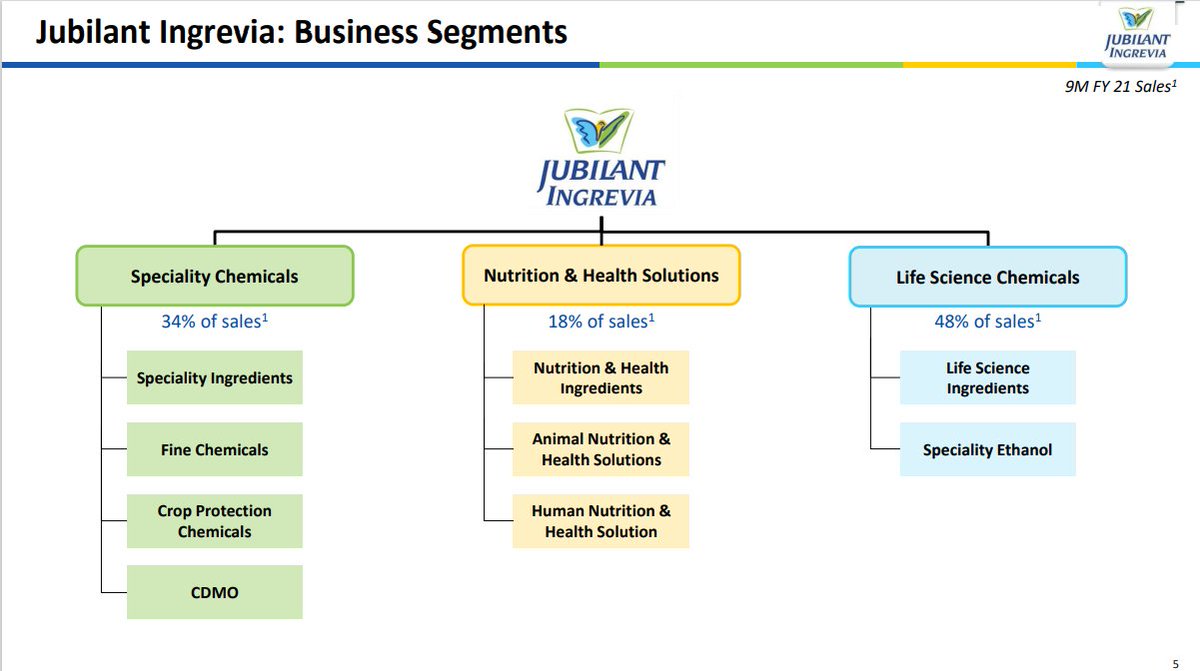

BUSINESS SEGMENTS -

They have mainly three business segments -

Specialty chemicals

Nutrition & Health

Life sciences Chemicals

Let's break down all the three business segments and analyze them separately

They have mainly three business segments -

Specialty chemicals

Nutrition & Health

Life sciences Chemicals

Let's break down all the three business segments and analyze them separately

1st is Specialty chemicals (34% of the sales)

Their specialty chemicals business is further divided into 4 parts, namely -

Specialty ingredients

Fine chemicals

Crop Protection Chemicals

CDMO

Their specialty chemicals business is further divided into 4 parts, namely -

Specialty ingredients

Fine chemicals

Crop Protection Chemicals

CDMO

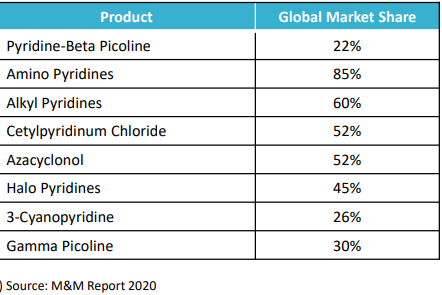

Company offers Specialty building blocks including Pyridine and Picolines (22% global market share), Cyanopyridines (26% global market share)

Globally they have the largest rage of products in Pyridine, picoline & it's derivatives (70 products)

Globally they have the largest rage of products in Pyridine, picoline & it's derivatives (70 products)

Globally amongst top 2 in Pyridine - beta globally

No. 1 in 11 Pyridine derivatives

Customer base of 420 global clients

45% of Pyridine & picoline volumes used inhouse for value added products.

No. 1 in 11 Pyridine derivatives

Customer base of 420 global clients

45% of Pyridine & picoline volumes used inhouse for value added products.

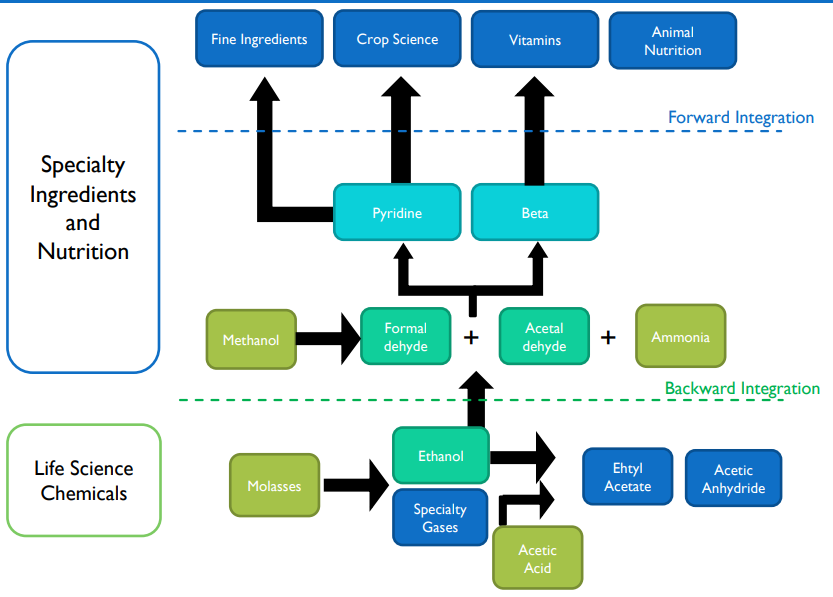

Company is both forward and backward integrated.

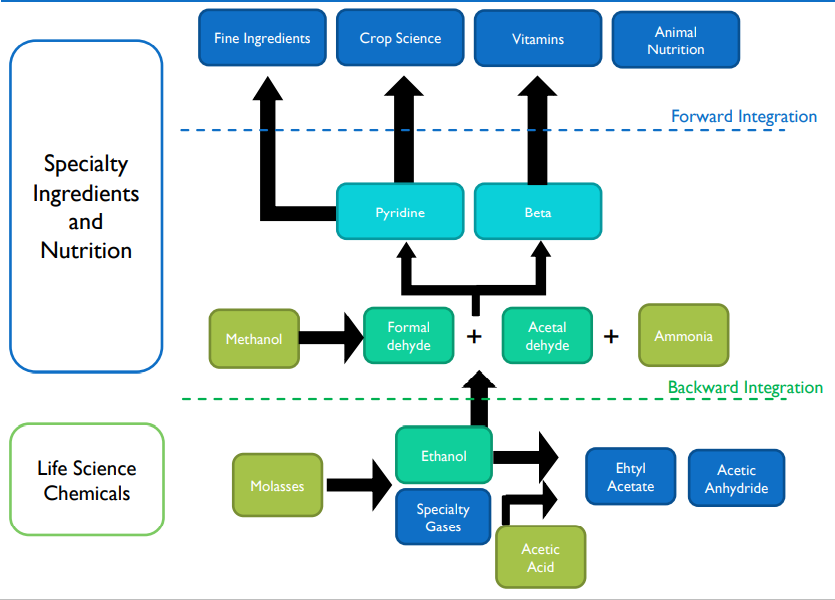

Let's take a look at the value chain of their main products.

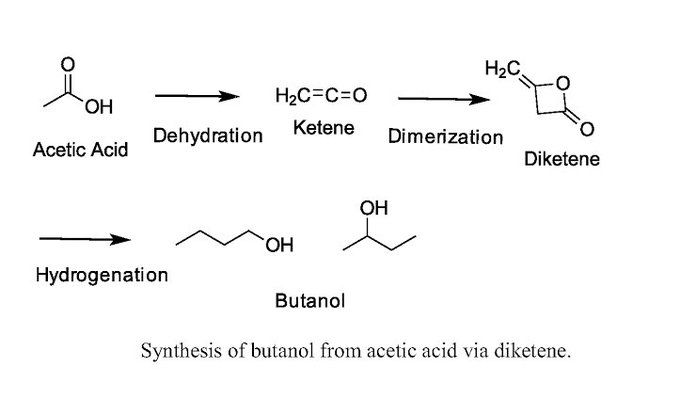

The basic raw material is molasses, from that they manufacture specialty ethanol and from that they manufacture Ethyle Acetate & Acetic Anhydride

Let's take a look at the value chain of their main products.

The basic raw material is molasses, from that they manufacture specialty ethanol and from that they manufacture Ethyle Acetate & Acetic Anhydride

Another raw material they use is Acetic Acid.

From ethanol they also manufacture - Formal Dehyde and Acetal dehyde which is further used to manufacture Pyridine and Beta Picoline.

From Beta Picoline they further manufacture Vitamine b3 & b4

From ethanol they also manufacture - Formal Dehyde and Acetal dehyde which is further used to manufacture Pyridine and Beta Picoline.

From Beta Picoline they further manufacture Vitamine b3 & b4

(Jubilant is the largest producer of Niacinamide and amongst global top two manufacturers of Vitamin B3 and India’s largest manufacturer of Vitamin B4)

Market share in Pyridine and it's derivatives -

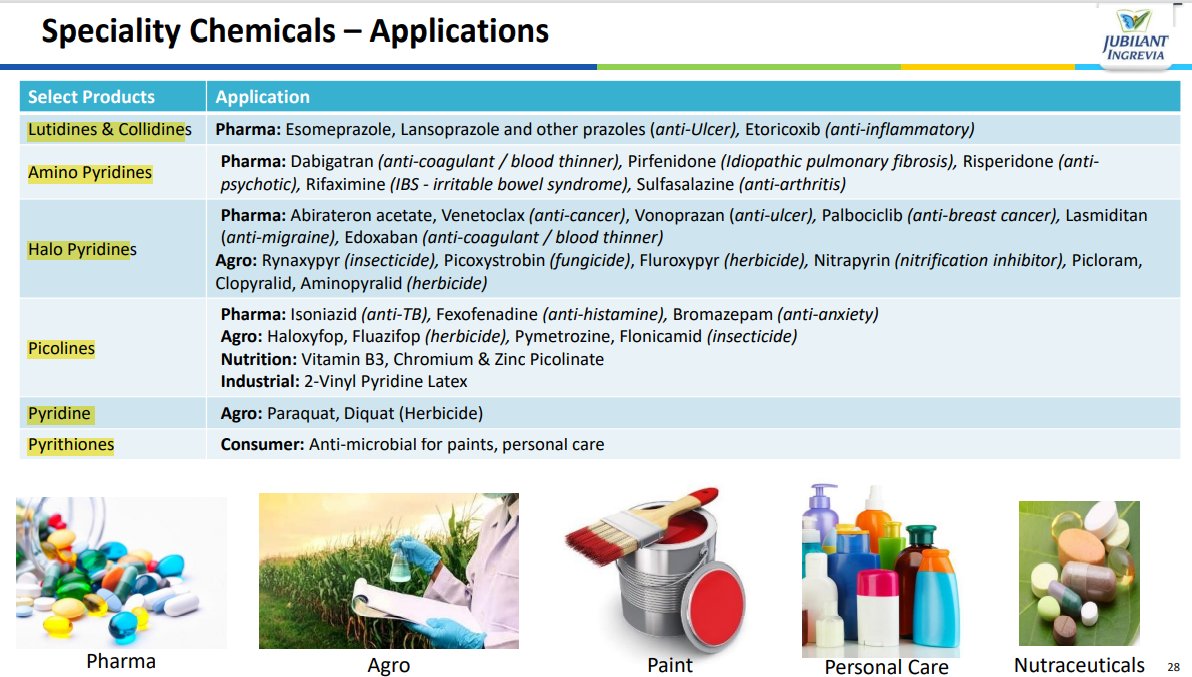

Specialty Chemicals end user industry

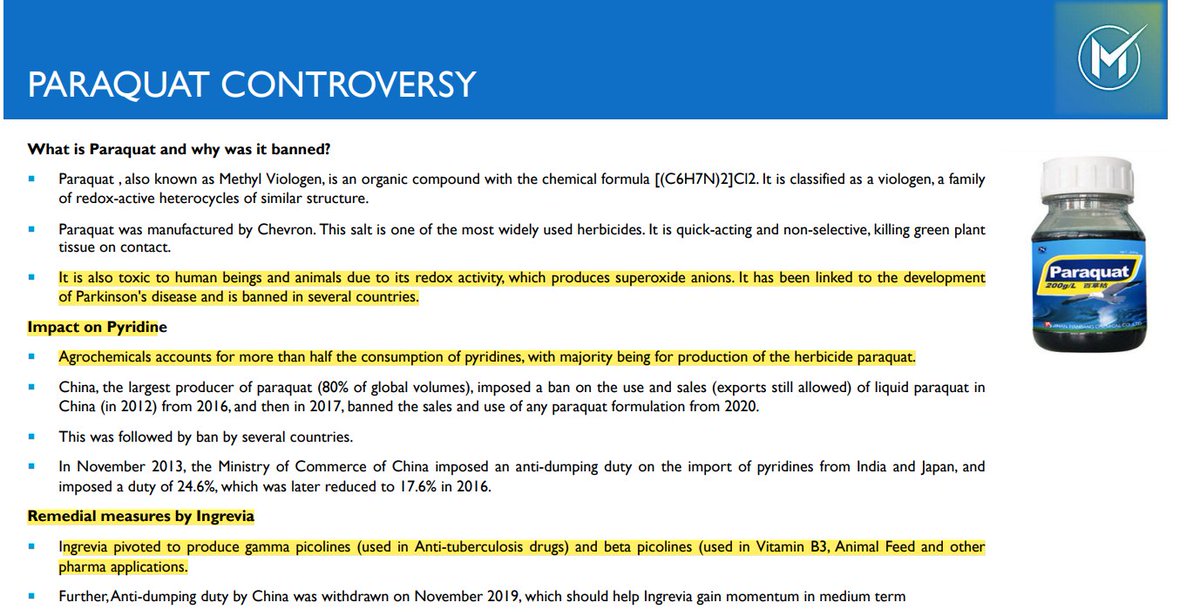

About 70% of Pyridine finds application is in the most popular herbicides in the world, namely paraquat & diquat.

About 70% of Pyridine finds application is in the most popular herbicides in the world, namely paraquat & diquat.

Our Gamma Picoline (30% global market share) and its key derivative 4 Cyano Pyridine is used by customers in making anti-tuberculosis drugs (~70% of global Gamma consumption), which help in eradication of TB.

We offer products which are used in more than 12 herbicides, fungicides, and insecticides, whose market is growing at ~3.5% from 2020-2025. (Source: M&M Industry Report).

end-use of Pyridine is for manufacturing herbicides in agrochemical industry, Beta Picoline finds its major application in the most important nutritional product Vitamin B3. While Alpha Picoline is used in manufacture of agrochemicals and many industrial

applications.

applications.

Growth prospects of End user industries -

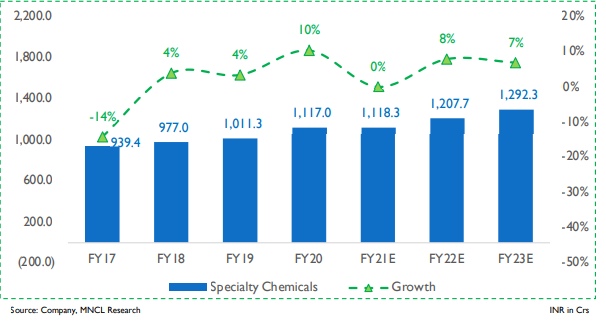

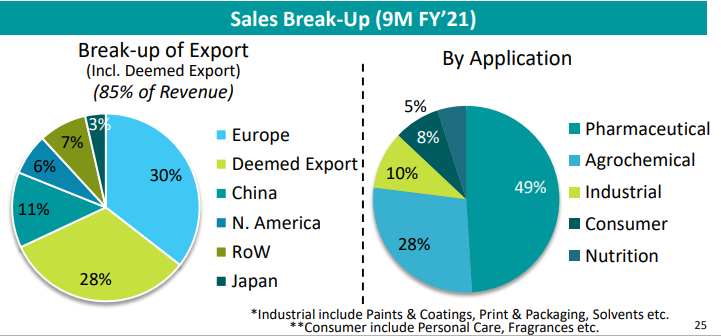

Specialty chemicals revenue trajectory & sales breakup -

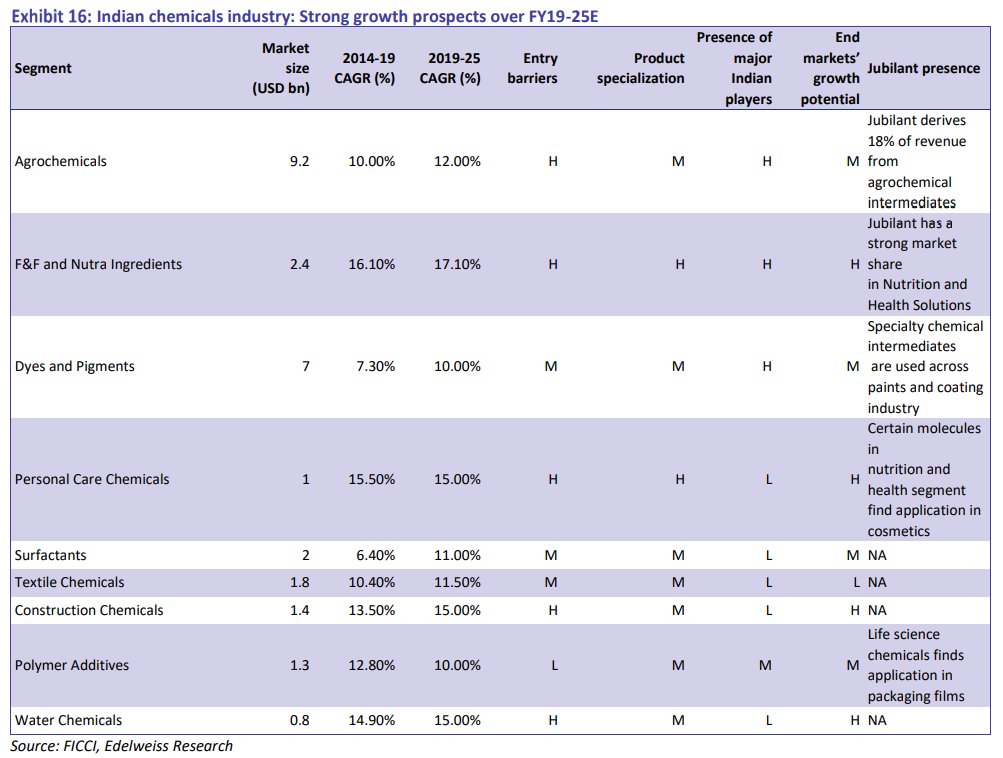

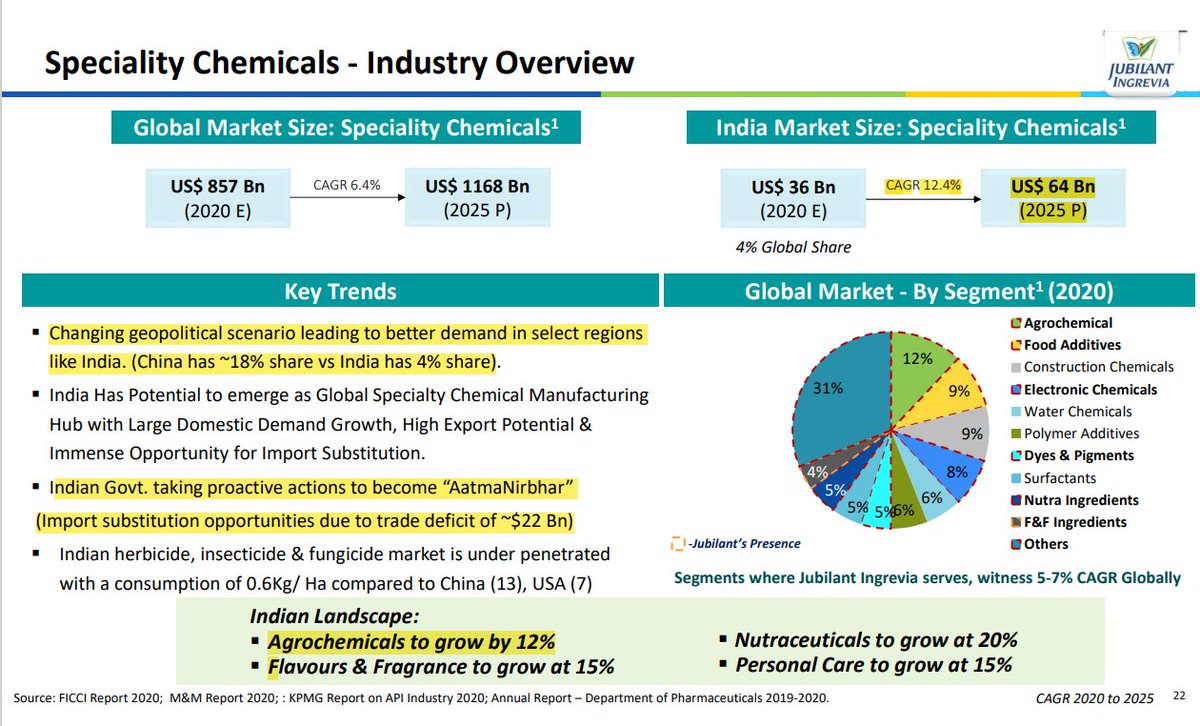

Indian Specialty chemicals market likely to grow to 64Bn $ by 2025, growing at the rate of 12.4% CAGR (Double the global market)

Various initiatives by Govt like - atmanirbhar bharat, PLI scheme, make in India will aid growth

Various initiatives by Govt like - atmanirbhar bharat, PLI scheme, make in India will aid growth

Next Segment we're gonna take a look at is CDMO

Let's 1st take a look at the CDMO market size and growth opportunities -

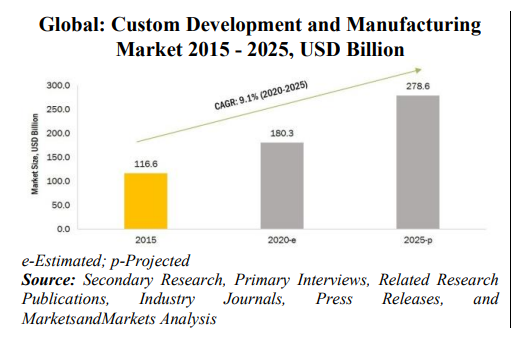

The global market for custom development and manufacturing is estimated to be USD 180.3 billion in 2020

Let's 1st take a look at the CDMO market size and growth opportunities -

The global market for custom development and manufacturing is estimated to be USD 180.3 billion in 2020

and is projected to reach a market size of USD 278.6 billion during the forecast period with a CAGR of 9.1%

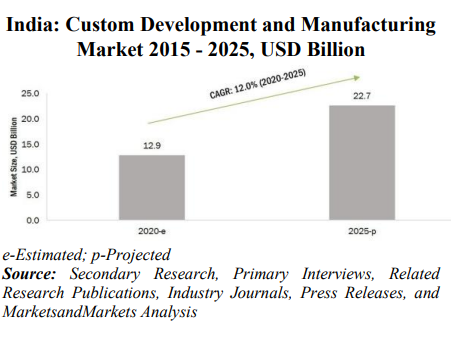

The Indian market for CDMO is estimated to be USD 12.9 billion in 2020 and is projected to reach a market size of USD 22.7 billion by 2025 with a CAGR of 12.0%

The Indian market for CDMO is estimated to be USD 12.9 billion in 2020 and is projected to reach a market size of USD 22.7 billion by 2025 with a CAGR of 12.0%

India’s CDMO market constitutes ~7% to ~8% of the global CDMO market (by value)

In 2019, ~80% of the Indian specialty chemicals CDMO market was captured by fine chemicals (by value), which are single molecule compounds that are utilized in the crop protection chemicals and API

In 2019, ~80% of the Indian specialty chemicals CDMO market was captured by fine chemicals (by value), which are single molecule compounds that are utilized in the crop protection chemicals and API

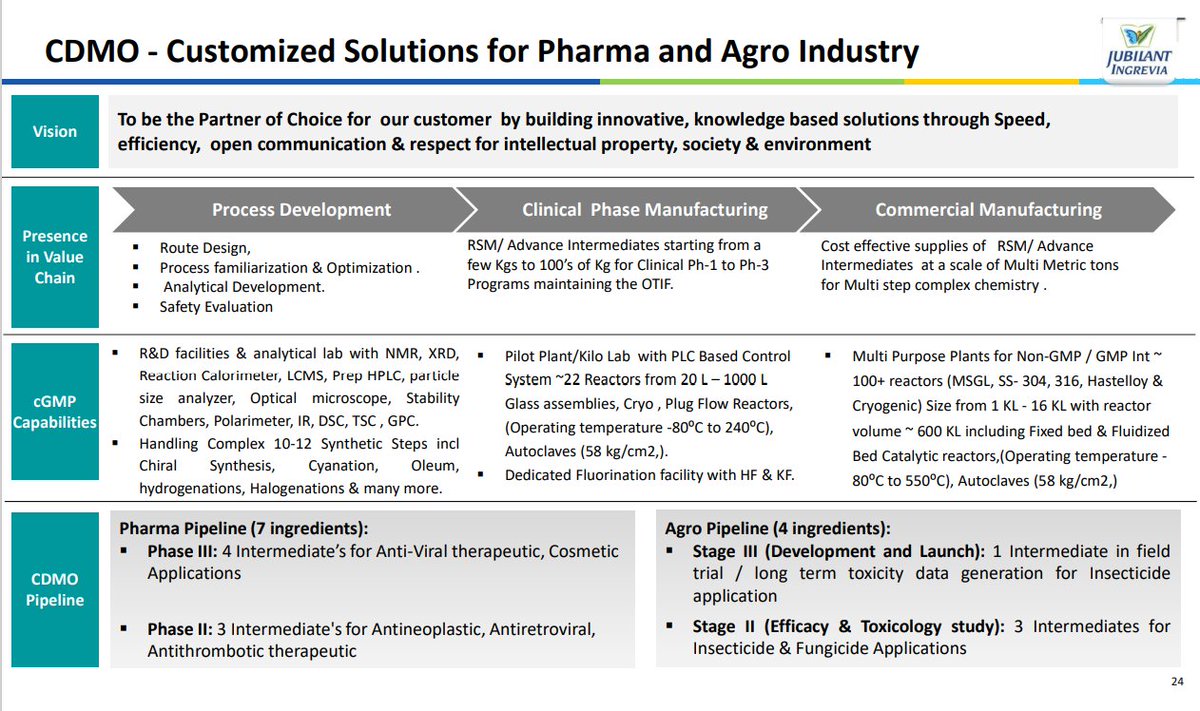

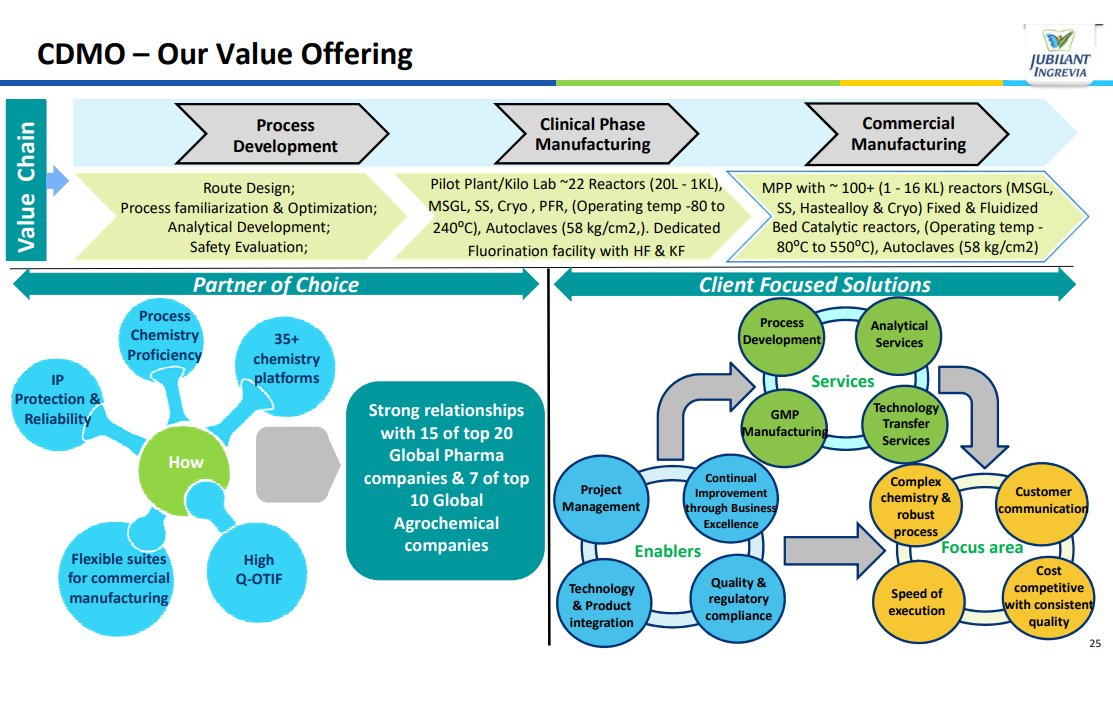

Jubilant Ingrevia offers CDMO services to Pharma and Agro chemical industry and is present across the whole value chain from Process Development to Clinical Manufacturing.

They have 7 molecules in Pharma Pipeline.

In phase III - They have 4 intermediate's for Anti-Viral & Cosmetic

In phase II - 3 intermediate's for Antineoplastic, Antiretroviral.

They have 4 molecules in Agro Pipeline - 1 In Stage III & 3 in Stage II

In phase III - They have 4 intermediate's for Anti-Viral & Cosmetic

In phase II - 3 intermediate's for Antineoplastic, Antiretroviral.

They have 4 molecules in Agro Pipeline - 1 In Stage III & 3 in Stage II

They have had more than 17+ collaborations with global pharmaceutical and biotech companies.

They have cGMP compliant pilot plant facility

operates with reactors ranging from 20 L to 1000 L (including glass, cryogenic reactors, Plug Flow Reactors, Lyophilizer and autoclaves)

They have cGMP compliant pilot plant facility

operates with reactors ranging from 20 L to 1000 L (including glass, cryogenic reactors, Plug Flow Reactors, Lyophilizer and autoclaves)

Commercial Manufacturing: We handle wide spectrum of process conditions (Temp. ranging from -80C to

300C, absolute vacuum) with variety of Mild Steel Glass Lined reactors (MSGL), Stainless Steel (SS)-316 &

Haste alloy reactors.

300C, absolute vacuum) with variety of Mild Steel Glass Lined reactors (MSGL), Stainless Steel (SS)-316 &

Haste alloy reactors.

Now let's take a look at their second main business segment -

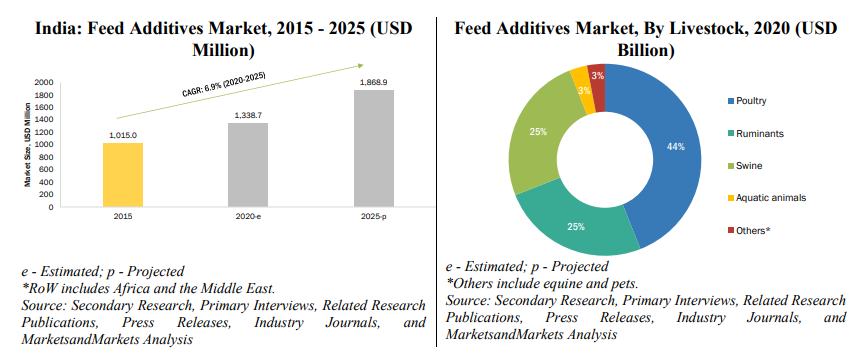

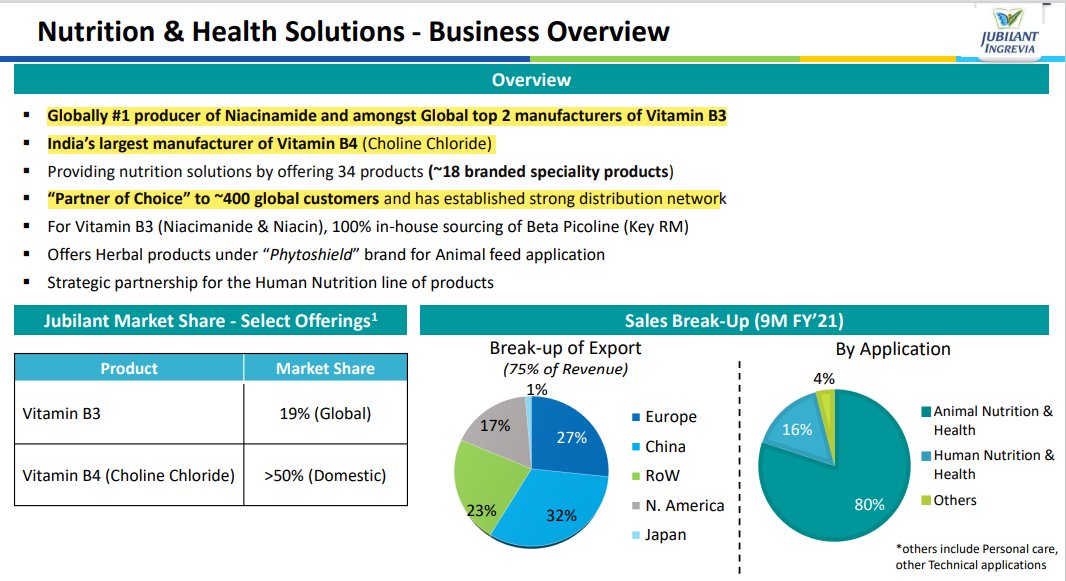

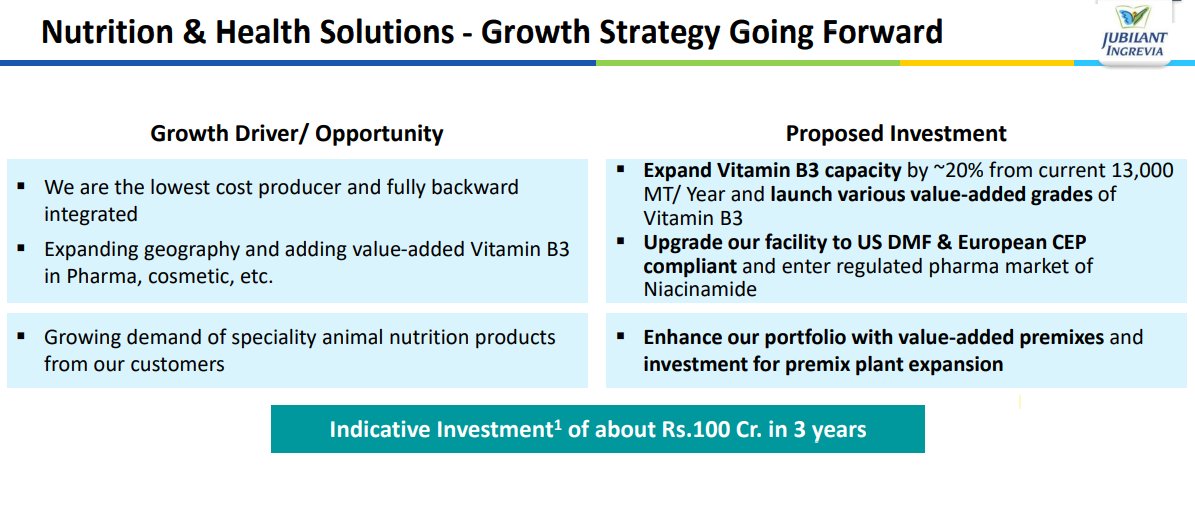

NURITION & HEALTH SOLUTIONS (18% of the revenues) - Jubilant is the largest producer of Niacinamide and amongst global top two manufacturers of Vitamin B3 and India’s largest manufacturer of Vitamin B4

NURITION & HEALTH SOLUTIONS (18% of the revenues) - Jubilant is the largest producer of Niacinamide and amongst global top two manufacturers of Vitamin B3 and India’s largest manufacturer of Vitamin B4

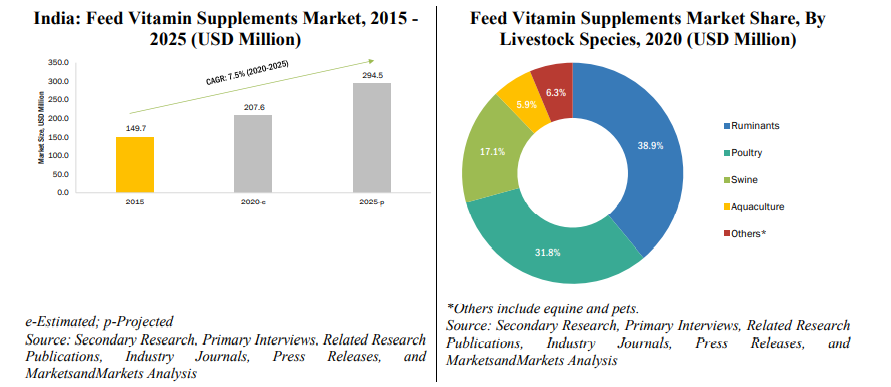

Market size and opportunity - The market for vitamin feed supplements is projected to be valued at USD

5,051.5 million by 2025 at a CAGR of 7.2% from 2020 to 2025. The Asia Pacific market accounted for the largest share of 28.4% in 2019 and is projected to grow at a CAGR of 7.4%

5,051.5 million by 2025 at a CAGR of 7.2% from 2020 to 2025. The Asia Pacific market accounted for the largest share of 28.4% in 2019 and is projected to grow at a CAGR of 7.4%

The RoW region is projected to be the fastest-growing region at a CAGR of 7.7% from 2020 to 2025.

There has been a positive trend in the annual production of meat, with the poultry sector growing at the highest rate in India; poultry, among other livestock, is most susceptible

There has been a positive trend in the annual production of meat, with the poultry sector growing at the highest rate in India; poultry, among other livestock, is most susceptible

to vitamin deficiencies.

The Indian market for vitamin feed supplements is growing at a CAGR of 7.5% during the forecast period, owing to the growing demand for animal protein and poultry products

The Indian market for vitamin feed supplements is growing at a CAGR of 7.5% during the forecast period, owing to the growing demand for animal protein and poultry products

Feed Additives - Feed additives are added to livestock feed as they improve the feed quality, prevent diseases, and improve feed utilization, thereby improving livestock performance and health.

The feed additives market is projected to grow at a CAGR of 6.1% from 2020, to reach

The feed additives market is projected to grow at a CAGR of 6.1% from 2020, to reach

USD 47.0 billion by 2025 in terms of value.

India accounted for the second-largest share of the additives market with 10.0% in 2020, in terms of volume, in the Asia Pacific region.

India accounted for the second-largest share of the additives market with 10.0% in 2020, in terms of volume, in the Asia Pacific region.

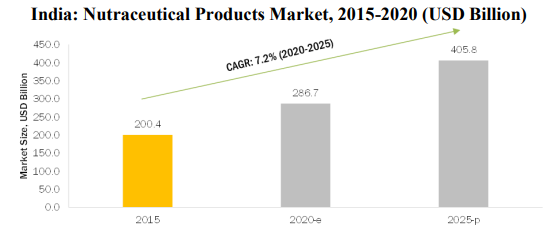

Nutraceutical Products - The nutraceutical products market is projected to grow at a CAGR of 7.2% from 2019 to reach USD 405.8 billion by 2025, in terms of value.

The global functional food ingredients market is projected to grow at a CAGR of 6.6% from 2020 to 2025, in terms

The global functional food ingredients market is projected to grow at a CAGR of 6.6% from 2020 to 2025, in terms

of value, to reach USD 107.3 billion by 2025.

The dietary supplements market in India is expected to grow at a CAGR of around 20% from 2020 to 2025.

The dietary supplements market in India is expected to grow at a CAGR of around 20% from 2020 to 2025.

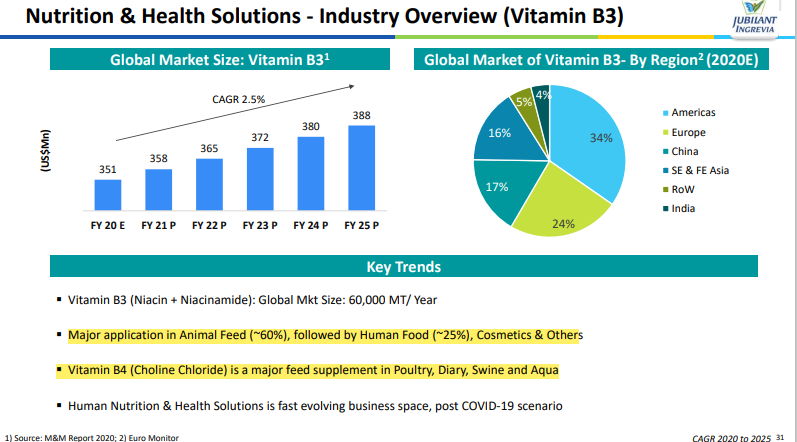

Global market size of Vitamin B3 is project to grow around 2.5% CAGR from 2020-2025.

Global Market size is 60,000MT/Year

Global Market size is 60,000MT/Year

Amongst top 2 manufacturer of Vitamin B3 and largest producer of Niacinamide.

The company is backward integrated as they manufacture Vitamin B3 from Beta Picoline which in turn they manufacture in house from acetal dehyde and formal dehyde combined with amonia and methanol.

Vitamin B3 applications

Vitamin B4 (Choline Chloride) helps maintain liver health in animals

Vitamin B4 (Choline Chloride) helps maintain liver health in animals

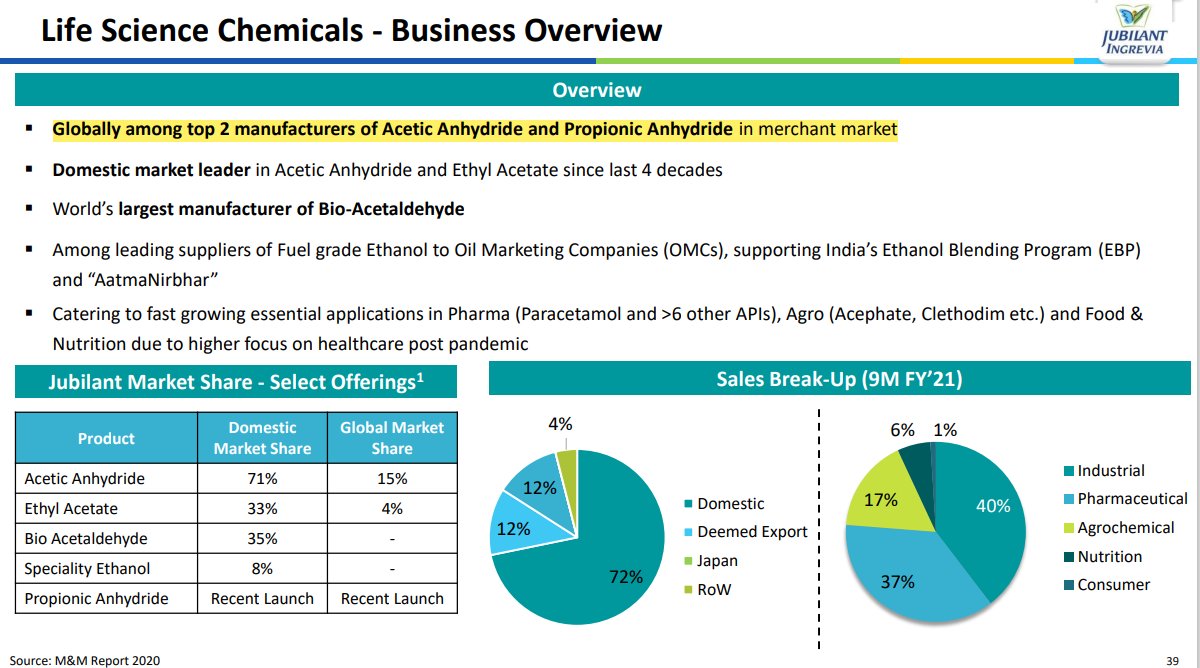

Now let's take a look at the 3rd and the largest Business segment -

Life Sciences Chemicals

1st let's take a look at the life sciences chemicals industry market size and opportunity.

Life Sciences Chemicals

1st let's take a look at the life sciences chemicals industry market size and opportunity.

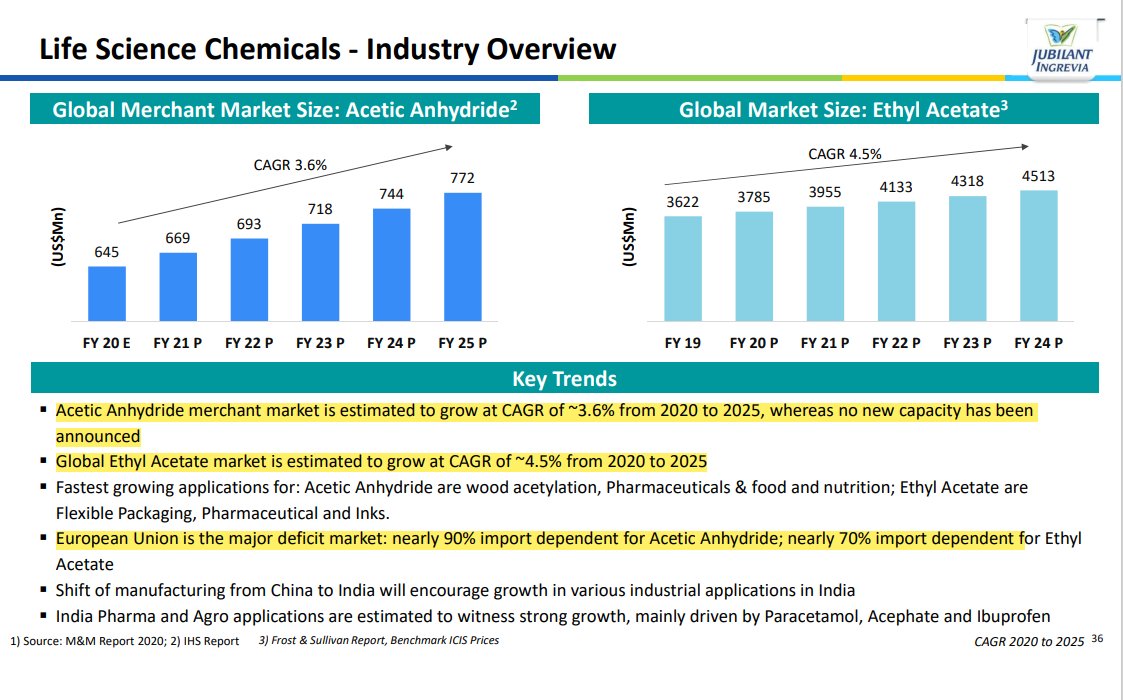

The global acetic anhydride market is estimated to grow at a CAGR of 3.0% between 2020 and 2025. The market for acetic anhydride is estimated to be USD 1,761.3 million and is projected to reach a market size of USD 2,041.8 million by 2025

The global ethyl acetate market is estimated to grow at a CAGR of 3.3% from 2020 to 2025. The market is estimated to be valued at USD 2,913.3 million in 2020 and is projected to reach USD 3,426.7 million by 2025.

Industrial applications account for

~67% of the total market,

Industrial applications account for

~67% of the total market,

followed by pharmaceuticals, which accounts for ~31% in 2019.

The Indian market for acetic anhydride is estimated to hold a market size of USD 201.5 million in 2020 and is

estimated to reach USD 249.1 million with a CAGR of 4.3% by 2025.

The Indian market for acetic anhydride is estimated to hold a market size of USD 201.5 million in 2020 and is

estimated to reach USD 249.1 million with a CAGR of 4.3% by 2025.

The Indian market for ethyl acetate is estimated at USD 118.5 million in 2020 and is projected to reach USD 139.2 million with a CAGR of 4.4% by 2025

Amongst the top 2 manufacturer of Acetic Anhydride and Propionic Anhydride

Among suppliers of fuel grade ethanol to OMCs.

Number 1 player of Acetyls in India

Among suppliers of fuel grade ethanol to OMCs.

Number 1 player of Acetyls in India

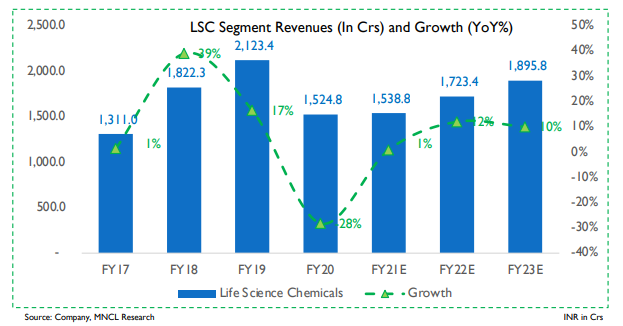

Revenues from this segment -

Now that we've understood all the business segments, let's take a look at the revenues and margin profile of all three segments.

Specialty Chem & Nutrition is high margins business - High double digit margins

Life sciences is a low margin business - Single or low double digit.

Specialty Chem & Nutrition is high margins business - High double digit margins

Life sciences is a low margin business - Single or low double digit.

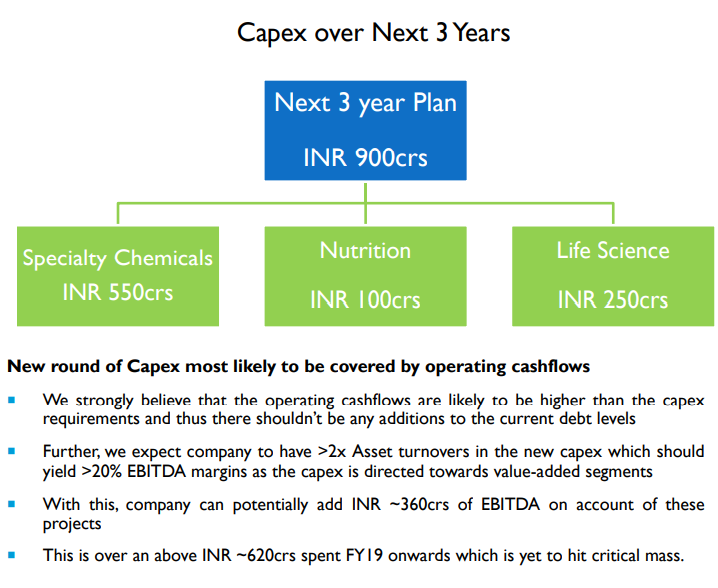

The company has planned a capex of 950 Cr for next three years, of which 550Cr is for specialty chemicals,

100Cr in Nutrition & 250Cr for Life sciences chemicals.

100Cr in Nutrition & 250Cr for Life sciences chemicals.

In specialty chemicals segment they're entering Into the Diketene derivatives and setting up a new facility for 6 diketene derivatives.

CDMO expansion for Pharma & Agro Chem

And a new facility for pesticides.

CDMO expansion for Pharma & Agro Chem

And a new facility for pesticides.

Why does it make sense for company to invest in for a new capacity for Diketenes?

With the forward integration, the company can enter Ketene chemistry and from that they can further integrate into Diketenes.

With the forward integration, the company can enter Ketene chemistry and from that they can further integrate into Diketenes.

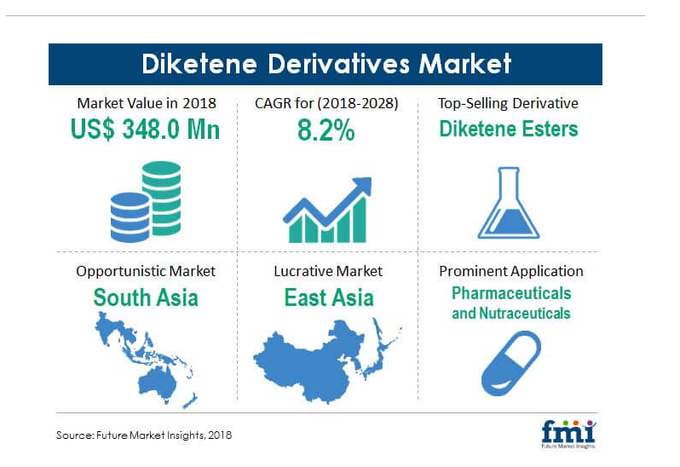

Global market for Diketene Derivatives was valued around 348$Bn IN 2018 and is growing at 8.2% CAGR.

The Indian market for these chemicals is ~US$ 230mn growing at 5-7% over the last five years, and is expected to grow at a similar rate till 2024.

The Indian market for these chemicals is ~US$ 230mn growing at 5-7% over the last five years, and is expected to grow at a similar rate till 2024.

About 40% of this demand is serviced through imports from USA, China and Europe. In India, there are only few players in Diketene and its derivatives with Laxmi Organic (~55% market share), Lonza (30-35% market share).

The companies strategy is to become the import substitutor

The companies strategy is to become the import substitutor

Overall capacity is going to be around 6,000-

7,000 tons per annum.

They're gonna start the production from next quarter (Q4FY22) and reach the 80-90% capacity utilization in next 1.5 Years.

7,000 tons per annum.

They're gonna start the production from next quarter (Q4FY22) and reach the 80-90% capacity utilization in next 1.5 Years.

The 100Cr capex they're doing in Nutrition segment is to increase the Vitamin B3 capacity by 20% from current 13000/MT

Key risk is the overcapacity will lead to reduced pricing that will dent the margins.

Key risk is the overcapacity will lead to reduced pricing that will dent the margins.

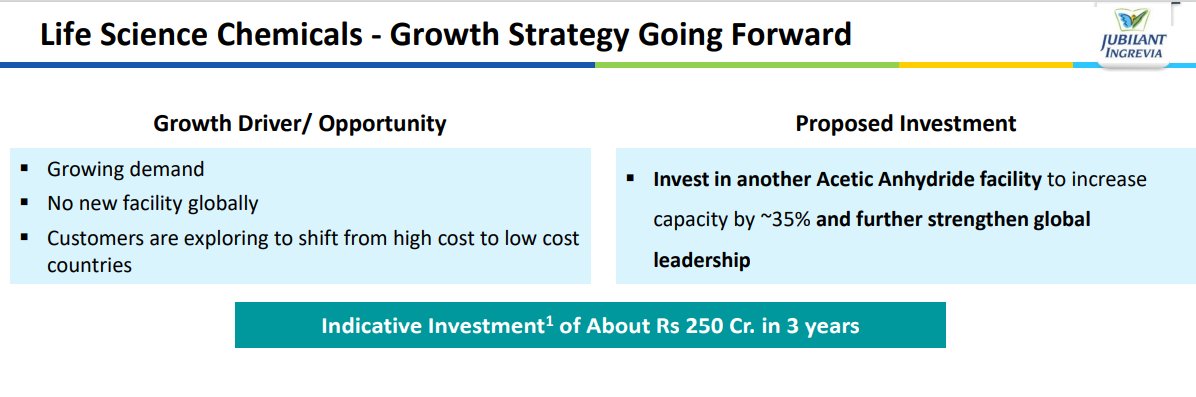

And in the 3rd segment, they're gonna increase the capacity for acetic anhydride by 35%.

CDMO multipurpose plant to come online in Q1 FY23

Acetic Anhydride capacity expansion by Q4 FY23

Niacinamide (Vitamin B3) capacity expansion by Q1 FY24

Food grade acetic acid by Q1FY23

Current capacity utilization is around 70% which is expected to reach 90% by end of FY23

Acetic Anhydride capacity expansion by Q4 FY23

Niacinamide (Vitamin B3) capacity expansion by Q1 FY24

Food grade acetic acid by Q1FY23

Current capacity utilization is around 70% which is expected to reach 90% by end of FY23

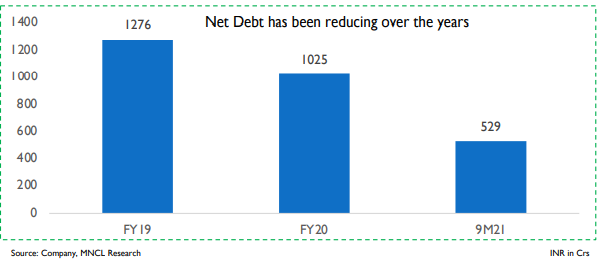

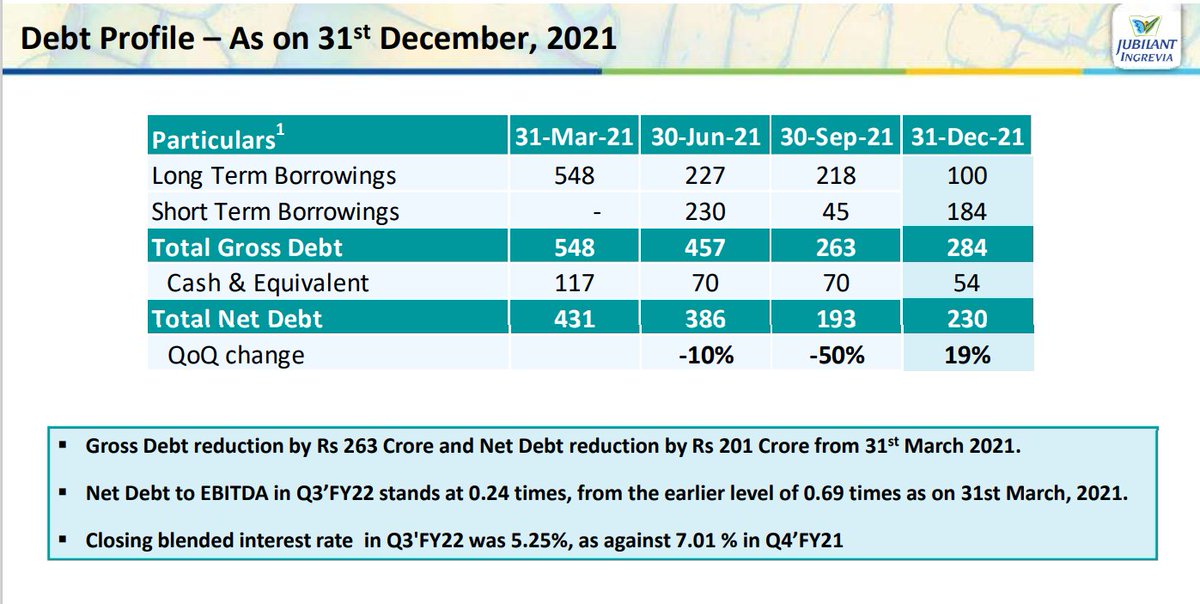

And the interesting thing is, the company is deleveraging at the same time and most of the capex is funded through internal accurals.

Debt is down from 1276Cr in 2019 to 529 in FY21 and total Net Debt is down to 230Cr in Q3 FY22

Interest rate is at 5.25%

Debt is down from 1276Cr in 2019 to 529 in FY21 and total Net Debt is down to 230Cr in Q3 FY22

Interest rate is at 5.25%

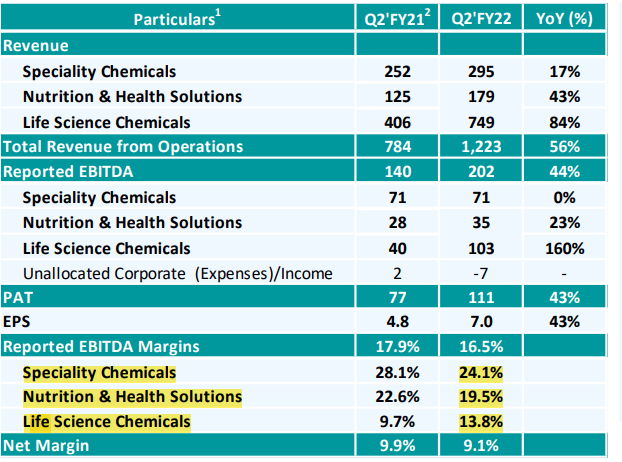

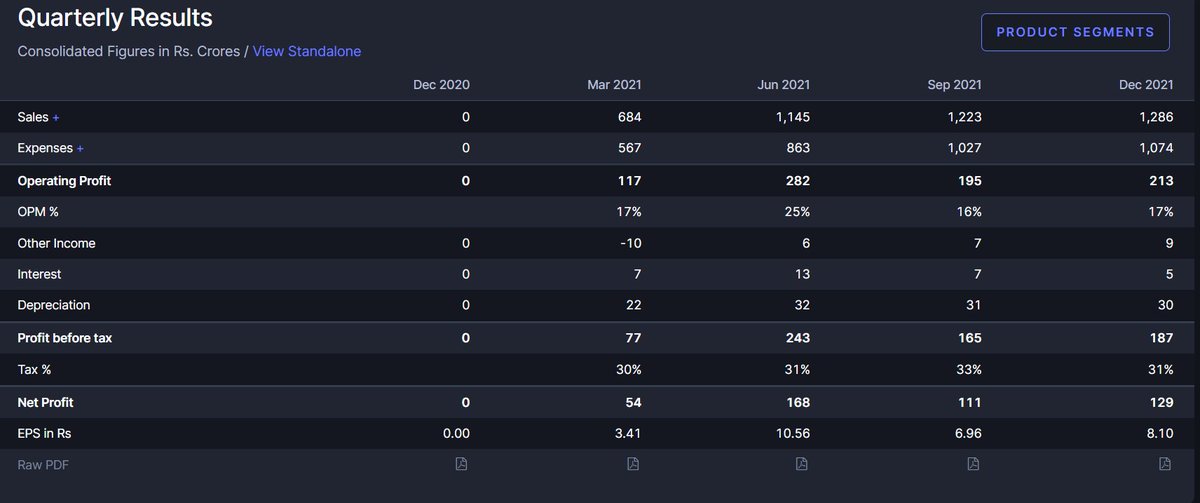

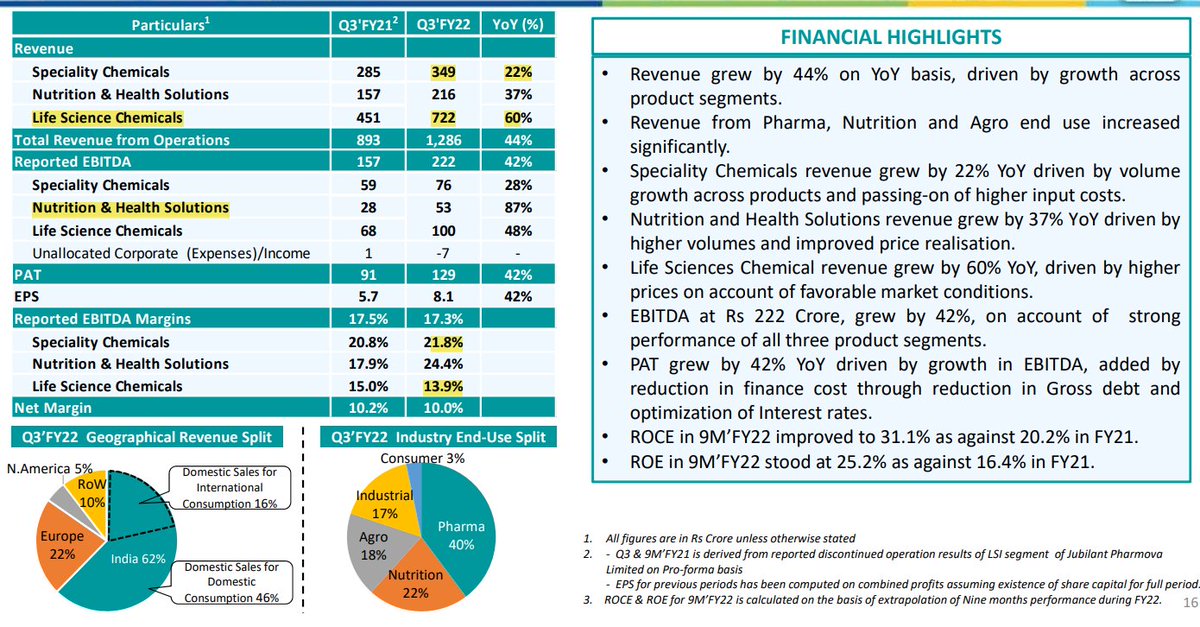

Now let's take a look at the financials - Quarterly revenues have increased from 887Cr in FY22 to 1286Cr in Q3 FY22.

Margins have increased from 12% to 17% (Had a small rise to 24% due the price increase of ethyle acetate)

Margins have increased from 12% to 17% (Had a small rise to 24% due the price increase of ethyle acetate)

And if we look at the segment wise revenues specialty chem has increased from 196 to 305Crand in the latest quarter it increased to 349Cr.

Specialty chemicals segment have stable EBIDTA margins >20% as compared to Life sciences chemicals

Specialty chemicals segment have stable EBIDTA margins >20% as compared to Life sciences chemicals

So there are lots of earnings triggers for next 2-3 years.

Management has guided to double the revenues by FY26 which i think is quite conservative.

Management has guided to double the revenues by FY26 which i think is quite conservative.

Now let's take a look at few anti thesis pointers -

1. Most of the revenues comes from Specialty chemicals business which is very volatile and commoditized.

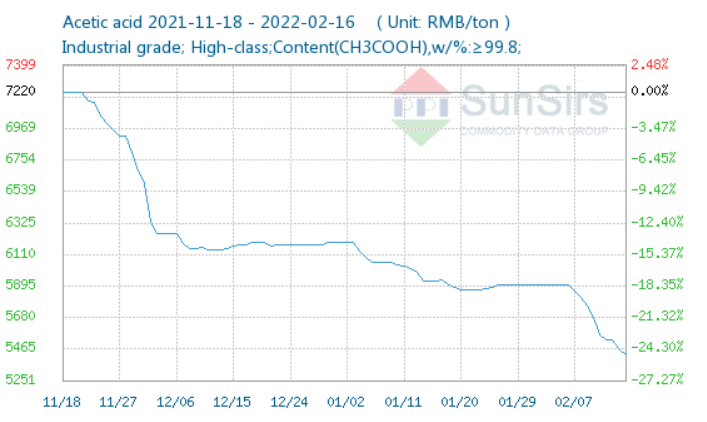

2. Raw material price fluctuation - Prices of acetic acid went high few months back.

1. Most of the revenues comes from Specialty chemicals business which is very volatile and commoditized.

2. Raw material price fluctuation - Prices of acetic acid went high few months back.

3. Product ban or regulatory risk - USFDA,WHO customer audits

4. Execution risk - Company is doing capacity expansion right now and any delay in that will dent the cash flows further and debt will dent the profitability.

5. They're increasing capacity of Vitamin B3 which may lead to over capacity as troubles in china settles.

5. They're increasing capacity of Vitamin B3 which may lead to over capacity as troubles in china settles.

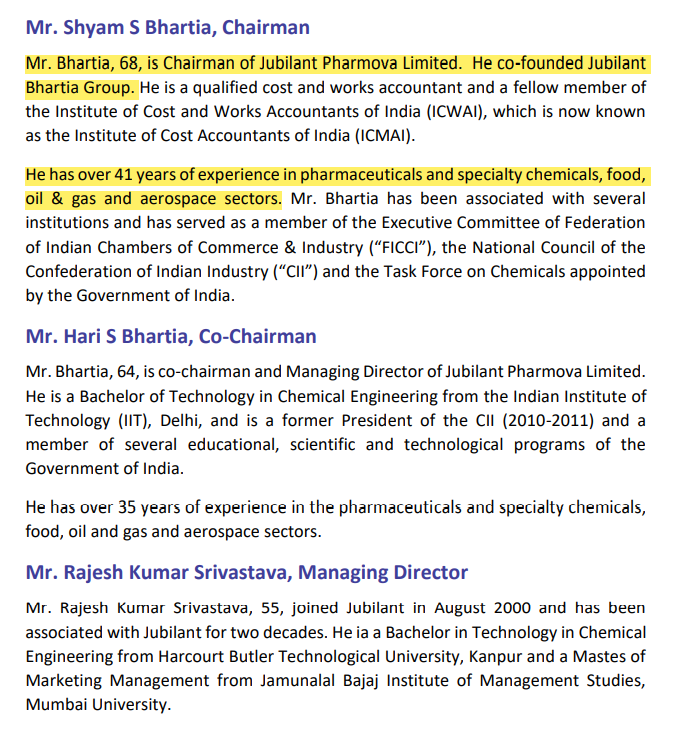

PROMOTOR AND MANAGEMENT - Promotor is Jubilant Bhartia Group and Mr Rjesh Sirvastava is the CEO

Mr Shyam S bhartia is the chairman

Mr Shyam S bhartia is the chairman

Like and retweet the 1st tweet for wider reach -

@shubhfin @caswapnilkabra @soicfinance @ishmohit1 @drprashantmish6 @unseenvalue @punitbansal14 @suru27 @Falak_Kalyani

@shubhfin @caswapnilkabra @soicfinance @ishmohit1 @drprashantmish6 @unseenvalue @punitbansal14 @suru27 @Falak_Kalyani

Another Risk

Loading suggestions...