Let's talk about the latest entrant into my portfolio.

IIFL Finance.

Small positions, for big dreams.

Please consider retweeting if you find it useful :D

🧵🧵🧵⤵️

IIFL Finance.

Small positions, for big dreams.

Please consider retweeting if you find it useful :D

🧵🧵🧵⤵️

Outline

0. What is IIFL Finance?

1. Business segments

2. Digitisation

3. Co-lending

4. Asset Quality

5. Growth

6. Profitability

7. Management Management Management

8. Anti-thesis

9. Valuations

10. Thesis

0. What is IIFL Finance?

1. Business segments

2. Digitisation

3. Co-lending

4. Asset Quality

5. Growth

6. Profitability

7. Management Management Management

8. Anti-thesis

9. Valuations

10. Thesis

0. What is IIFL Finance?

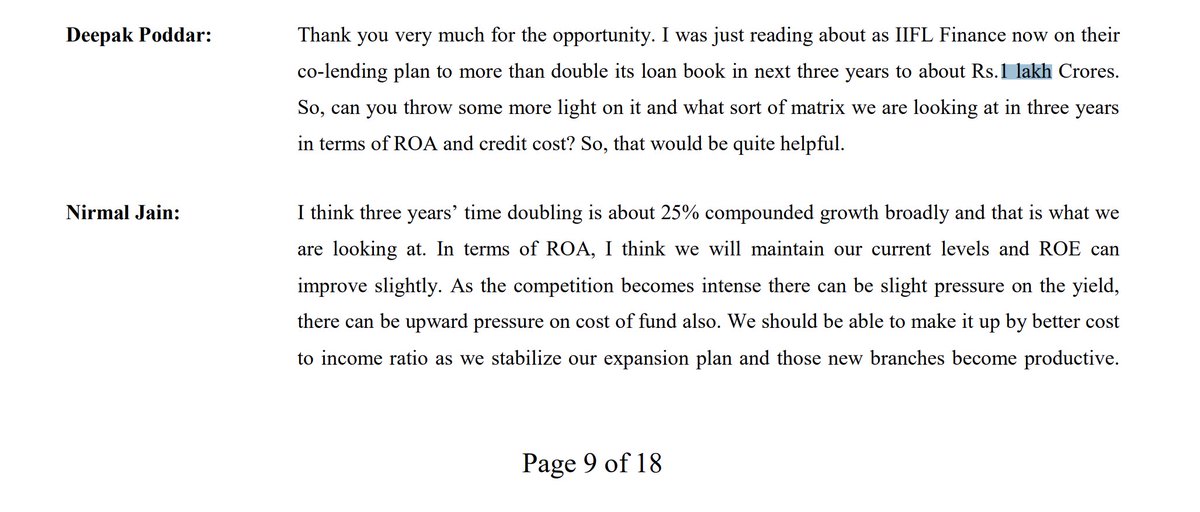

IIFL Finance is a diversified NBFC. Home Loans, Gold Loans, Business Loans (MSME), Micro Finance.

>70% of the loans are backed by collateral.

They have a 46,000 cr loan book.

They want to have a 1 lakh cr loan book after 3 years.

IIFL Finance is a diversified NBFC. Home Loans, Gold Loans, Business Loans (MSME), Micro Finance.

>70% of the loans are backed by collateral.

They have a 46,000 cr loan book.

They want to have a 1 lakh cr loan book after 3 years.

1. Business Segments

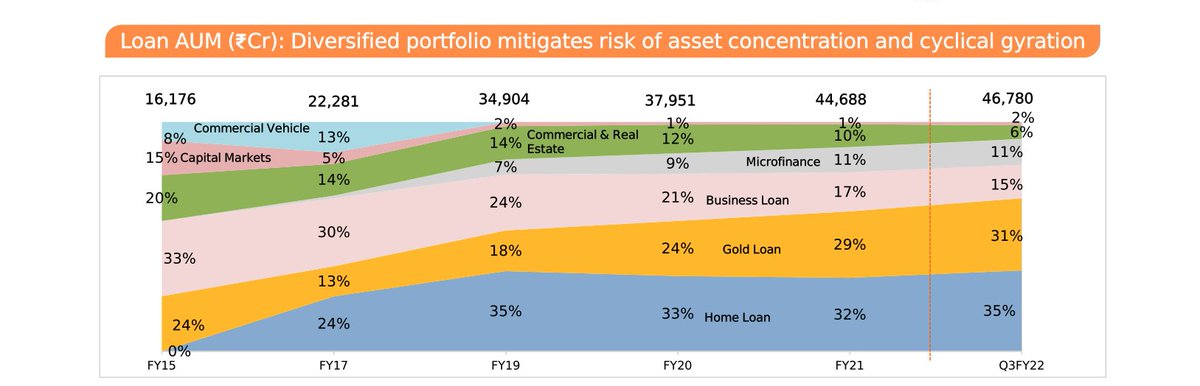

The loans they give can be divided into 5 segments:

(i) Home loans

(ii) Gold loans

(iii) MSME business loans

(iv) Micro Finance

(v) Legacy: Construction & capital markets

The loans they give can be divided into 5 segments:

(i) Home loans

(ii) Gold loans

(iii) MSME business loans

(iv) Micro Finance

(v) Legacy: Construction & capital markets

You can see home loans & gold loans grow. You can see legacy part shrink. You can see business loans also shrink. You can see MFI part being stable. This gives us a rough idea of how IIFL is evolving.

1.(i) home loans

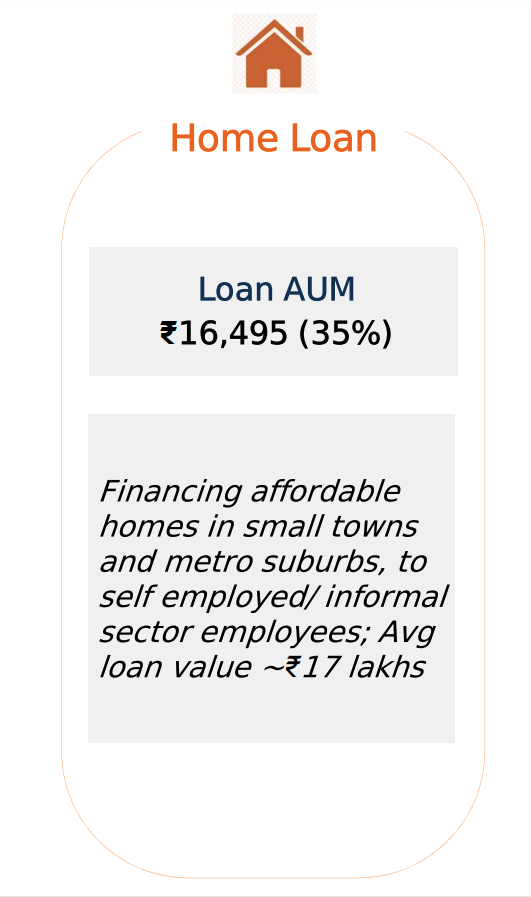

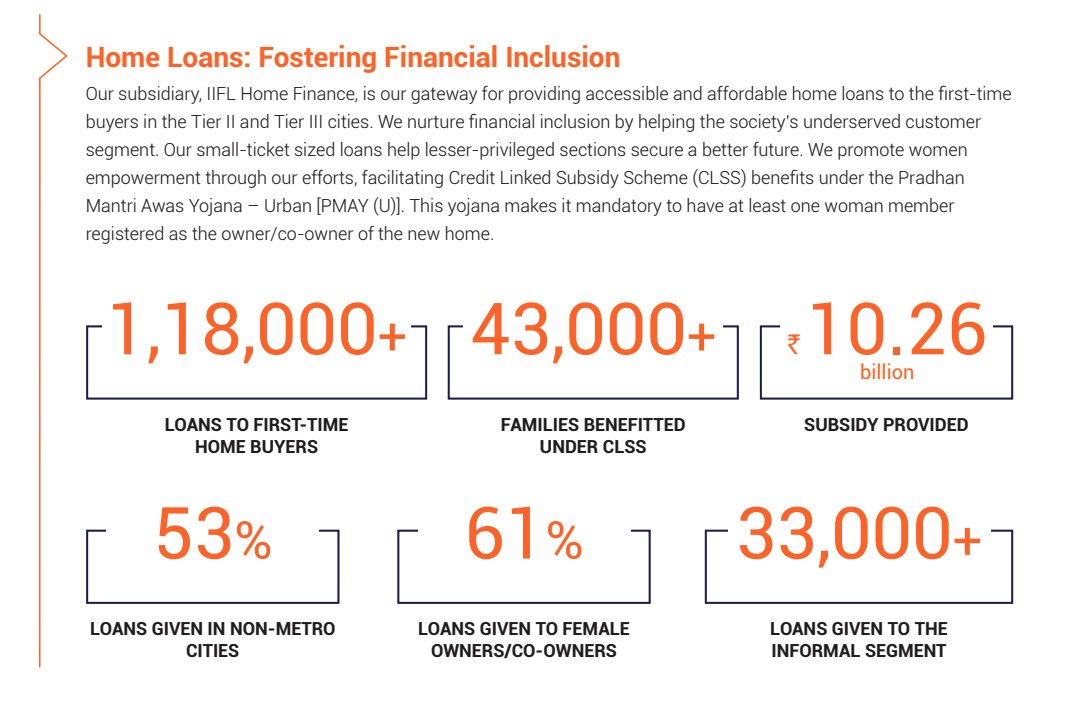

35% of Loan book.

Purely into affordable homes. Operate in small towns, metro sub-urbs. Loans to self employed & informal sector employees.

Average size 17 lakh.

Average Rate of Interest of 10.1%. For comp: Big banks give home loans at 6.5-8%. Aavaas at 13%.

35% of Loan book.

Purely into affordable homes. Operate in small towns, metro sub-urbs. Loans to self employed & informal sector employees.

Average size 17 lakh.

Average Rate of Interest of 10.1%. For comp: Big banks give home loans at 6.5-8%. Aavaas at 13%.

Key Driver in this segment: Govt's Housing for all through Credit-linked Subsidy scheme.

pmay-urban.gov.in

pmay-urban.gov.in

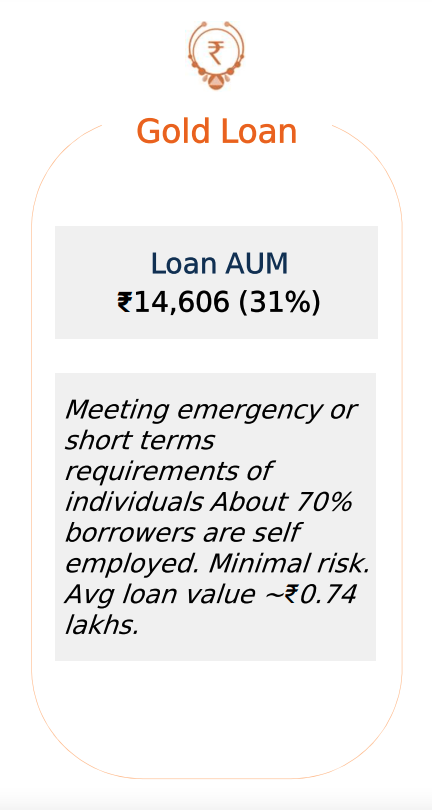

1.(ii) Gold loans

31% of loan book.

Good Geographical diversification in North, West, South. Given for personal loan & business loans.

Average size 74k.

Average yield of 17.4%. Muthoot average yield is 22%.

31% of loan book.

Good Geographical diversification in North, West, South. Given for personal loan & business loans.

Average size 74k.

Average yield of 17.4%. Muthoot average yield is 22%.

An interesting insight i gleaned from @varinder_bansal sir interview is that part of their Gold Loan business is quite sticky coz they give it as a small business loan. Working capital Loan. Customer keeps coming back. Sticky. Repeatable.

youtube.com

youtube.com

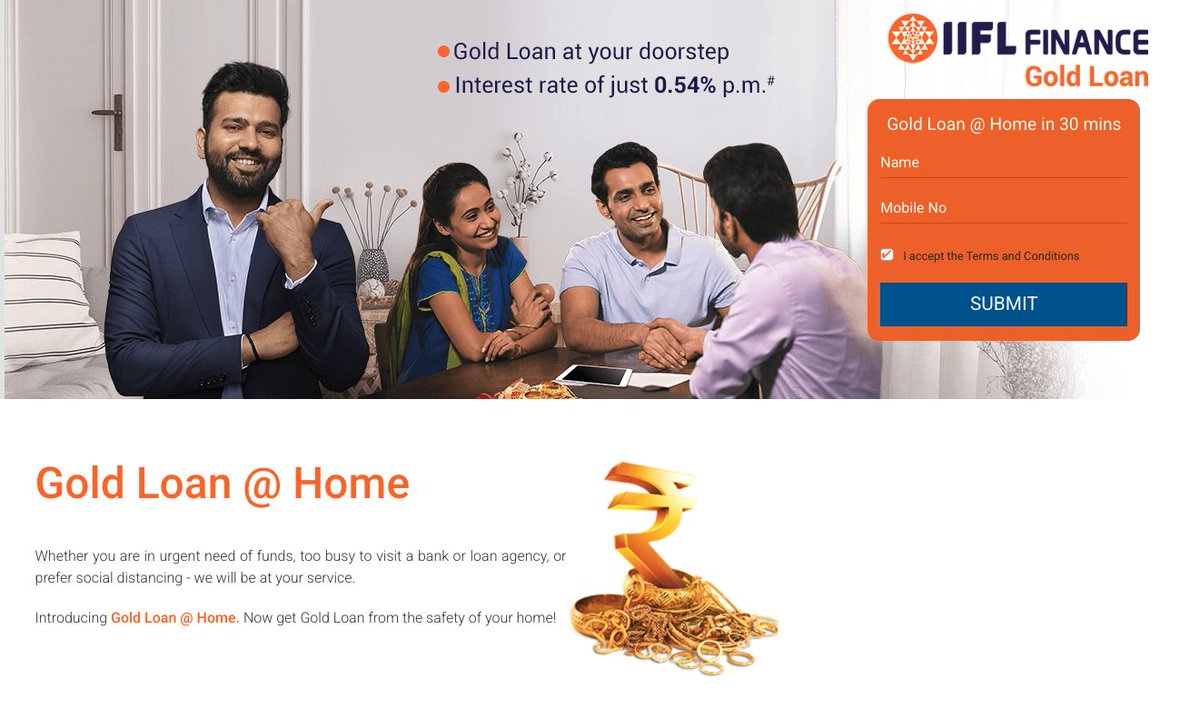

IIFL is a pioneer in creating new markets here. North india is one example. Gold loan @ home is another such initiative (gold can be collected @ home, money disbursed electronically).

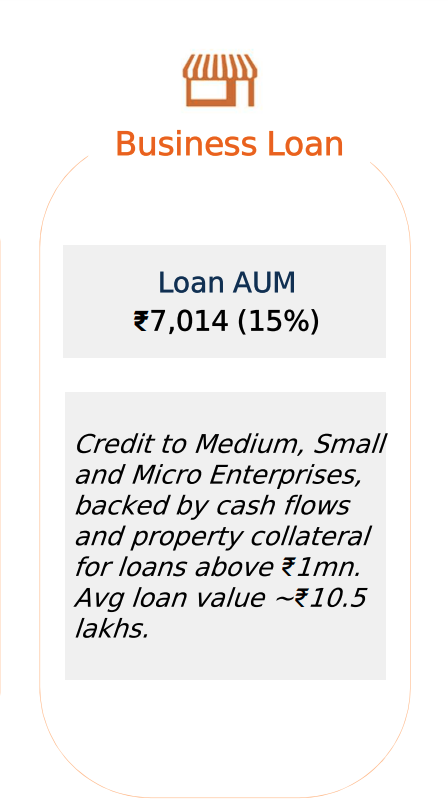

1.(iii) MSME Biz Loans

15% of AUM

Provide Large secured loan (Loan Against Property) for > 10 lakh loan & cashflow based small ticket loans (< 10 lakh loan) for Working capital (inventory, receivables), capex.

Average size 10.5 lakh.

Average yield: 15.3%.

15% of AUM

Provide Large secured loan (Loan Against Property) for > 10 lakh loan & cashflow based small ticket loans (< 10 lakh loan) for Working capital (inventory, receivables), capex.

Average size 10.5 lakh.

Average yield: 15.3%.

An interesting tidbit is that some of these loans are a part of Government's Guaranteed Emergency Credit Line (GECL).

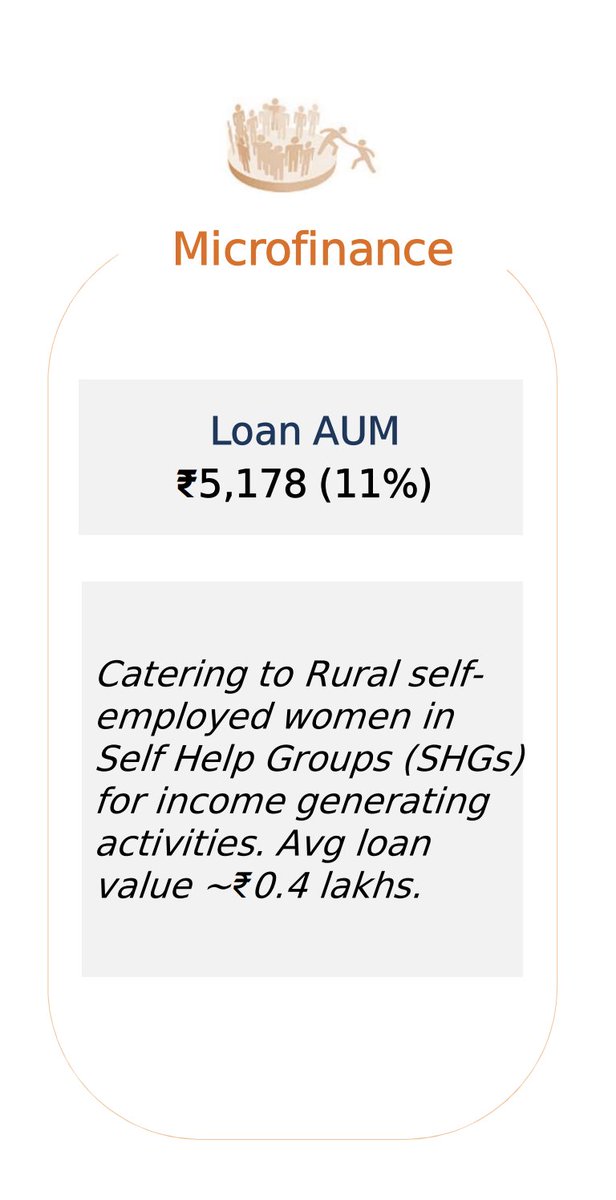

1.(iv) Microfinance

11% of AUM.

Provide small income generating loans to rural women in self help groups.

Average size of 40 thousand.

Average yield of 22%.

11% of AUM.

Provide small income generating loans to rural women in self help groups.

Average size of 40 thousand.

Average yield of 22%.

1.(v) Construction & Capital Markets

8% of AUM.

They used to finance developers across value stack including land purchases which are speculative in nature. Have streamlined this part a lot, aligned it with construction activities. Shrunk construction significantly.

8% of AUM.

They used to finance developers across value stack including land purchases which are speculative in nature. Have streamlined this part a lot, aligned it with construction activities. Shrunk construction significantly.

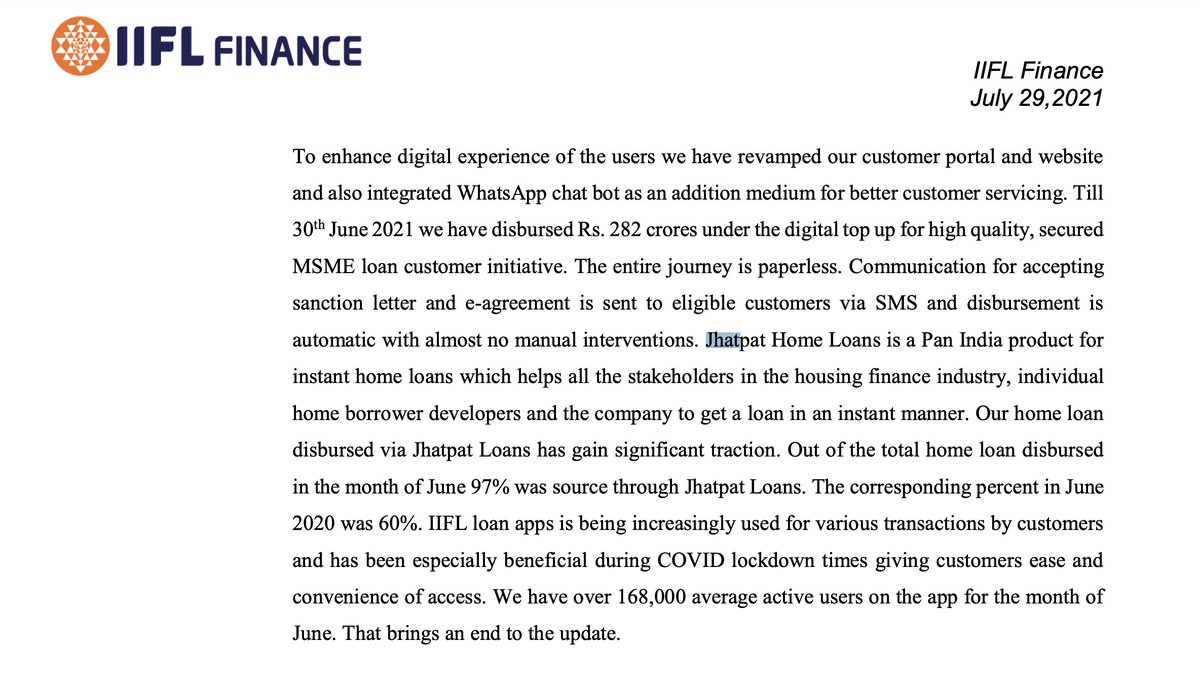

2. Digitization

(i) Gold Loan at Home.

Gold is collected from customer from their home. Money is transferred digitally to the customer. Customer can prepay. Can take top-up digitally.

137cr disbursed in Q3. 30% growth QoQ.

(i) Gold Loan at Home.

Gold is collected from customer from their home. Money is transferred digitally to the customer. Customer can prepay. Can take top-up digitally.

137cr disbursed in Q3. 30% growth QoQ.

2 (ii) DIY paperless Whats app Loans

All documents uploaded on whats app by customer. IIFL evaluates credit risk digitally. Money disbursed digitally. Collections digitally.

Just started. Disbursement growing 4x QoQ.

In 1st 10 days, got 60,000 leads organically w/o ads.

All documents uploaded on whats app by customer. IIFL evaluates credit risk digitally. Money disbursed digitally. Collections digitally.

Just started. Disbursement growing 4x QoQ.

In 1st 10 days, got 60,000 leads organically w/o ads.

2 (iii) Jhatpat Home loans

All home loans now happen instantly digitally. Until Q2FY21, only 60% of home loans were jhatpat. 100% of disbursements are instant now.

All home loans now happen instantly digitally. Until Q2FY21, only 60% of home loans were jhatpat. 100% of disbursements are instant now.

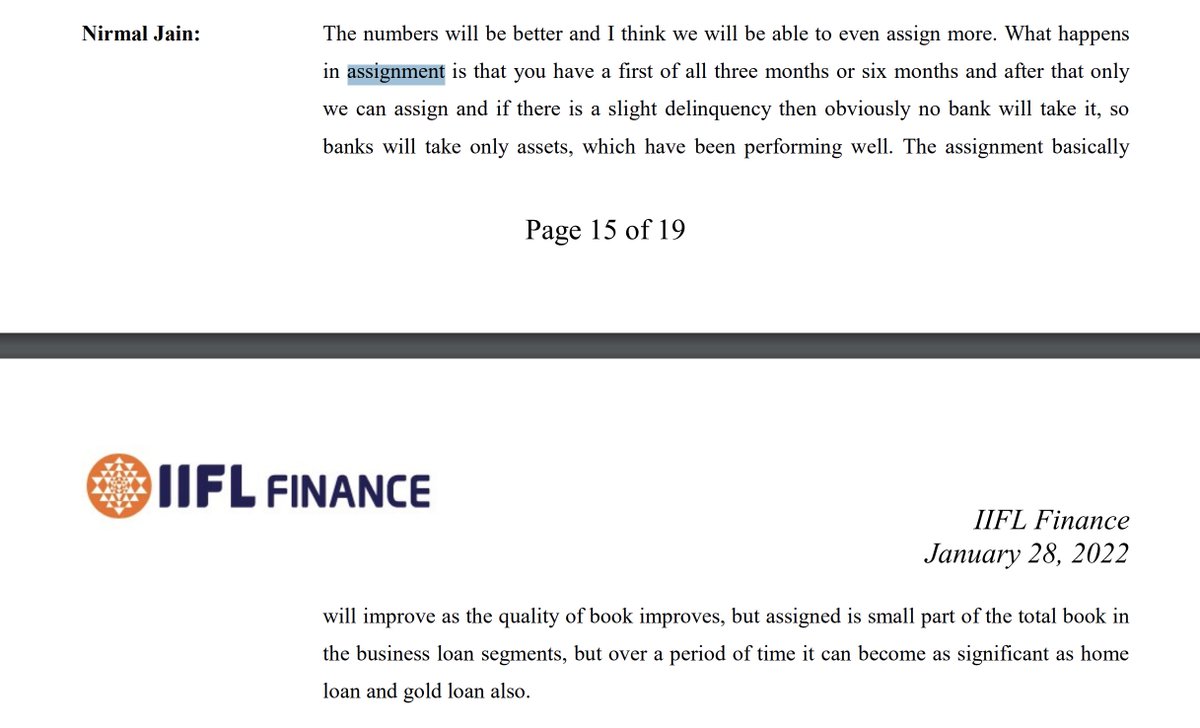

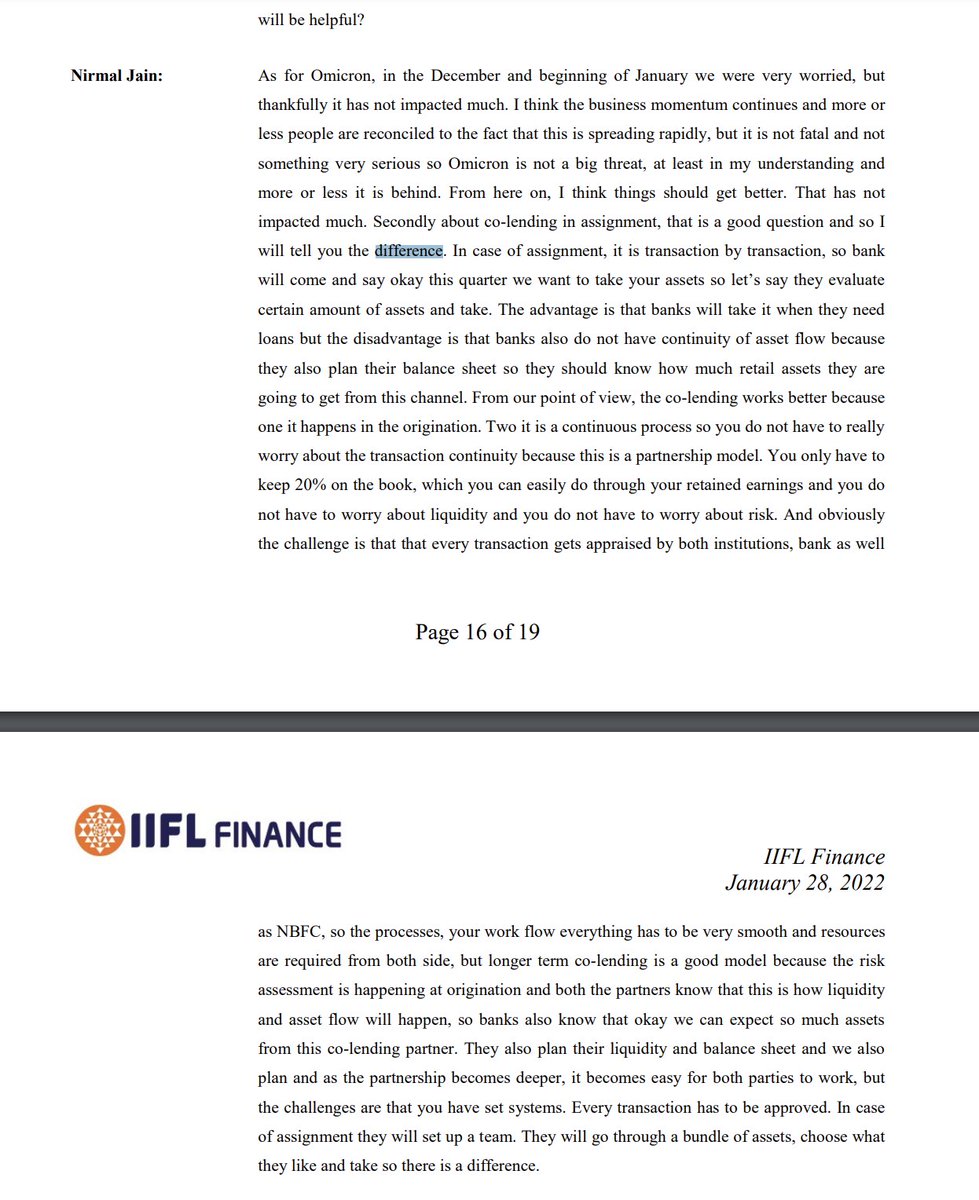

3. Co-lending

One of the biggest changes in the lending space in last few years has been co-lending, assignment, securitization.

One of best videos to understand co-lending:

youtube.com

One of the biggest changes in the lending space in last few years has been co-lending, assignment, securitization.

One of best videos to understand co-lending:

youtube.com

In a nutshell:

Assignment:

Step 1: NBFC creates a portfolio of loans.

Step 2: NBFC 'ages' that PF for 3-6 months to prove it performs well.

Step 3: NBFC starts talk to 'assign' PF to bank.

Step 4: Bank does its own due diligence at portfolio level for entire aggregate of loans.

Assignment:

Step 1: NBFC creates a portfolio of loans.

Step 2: NBFC 'ages' that PF for 3-6 months to prove it performs well.

Step 3: NBFC starts talk to 'assign' PF to bank.

Step 4: Bank does its own due diligence at portfolio level for entire aggregate of loans.

Step 5: Banks take on credit risks. NBFC gives bank guarantee for credit risk in form of FDs (5% of AUM). NBFC keeps getting fee income from the loan. This is assignment income. NBFC credit risk is limited to extent of FD kept with bank.

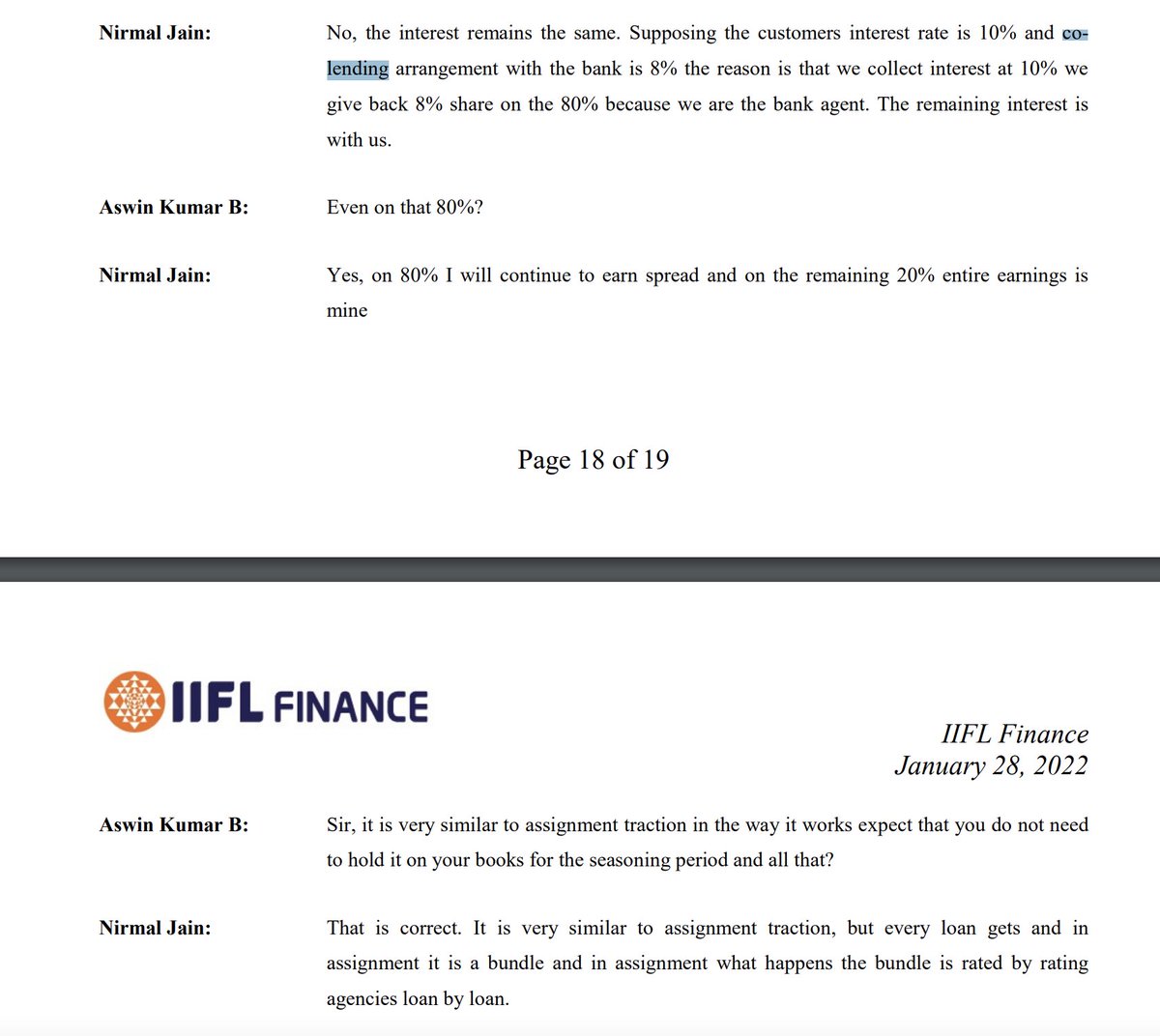

Co-lending:

Step 1: Bank & NBFC create a co-lending framework. A set of criteria they will do co-lending under. Set of customers to target etc. Rate at which bank lends etc.

Step 1: Bank & NBFC create a co-lending framework. A set of criteria they will do co-lending under. Set of customers to target etc. Rate at which bank lends etc.

Step 2: For each loan, NBFC finds the customer who needs it. If it fits co-lending criteria, NBFC makes the loan under co-lending agreement.

Step 3: NBFC streams the info in real time to the bank. Bank can now decide (at time of origination & at a case-by-case basis) whether they want to accept this loan or not. If bank does not accept the loan, NBFC keeps it on their books fully.

If bank accepts the loan, 80% of the loan resides on the books of the bank, 20% on the books of the NBFC.

Suppose the loan was of Rs 1000. Rs 200 resides on NBFC balance sheet. Rs 800 on NBFC balance sheet. Suppose bank & nbfc agreement is for bank to lend at 8%. Then, NBFC gets 2% spread on entire Rs 1000. Thats Rs 20. Bank gets 8% on Rs 800 or 64 rupees.

NBFC gets 8% on their 20% of the loan that is 16 rupees. So NBFC gets 36 rupees on a Rs 200 loan.

This 80 rupees of loan is called off-balance sheet asset under management (AUM). The fee income from it (that 2%) is called co-lending income.

This 80 rupees of loan is called off-balance sheet asset under management (AUM). The fee income from it (that 2%) is called co-lending income.

The credit risk to NBFC is limited to the 20% of the loan. Why is this a win-win?

Since Banks typically have much lower cost of capital (IDFC First has 5% cost of capital to IIFL's 8.7%), they are able to lend at a lower rate of interest. Banks get growth.

Since Banks typically have much lower cost of capital (IDFC First has 5% cost of capital to IIFL's 8.7%), they are able to lend at a lower rate of interest. Banks get growth.

NBFCs get ROE accretive assignment/co-lending fees income. This makes the NBFC more asset light. Restricts the downside protection (80% of credit risk sits on bank balance sheet).

This is why i am personally quite excited about co-lending model & what impact it can have on NBFC valuations if executed well.

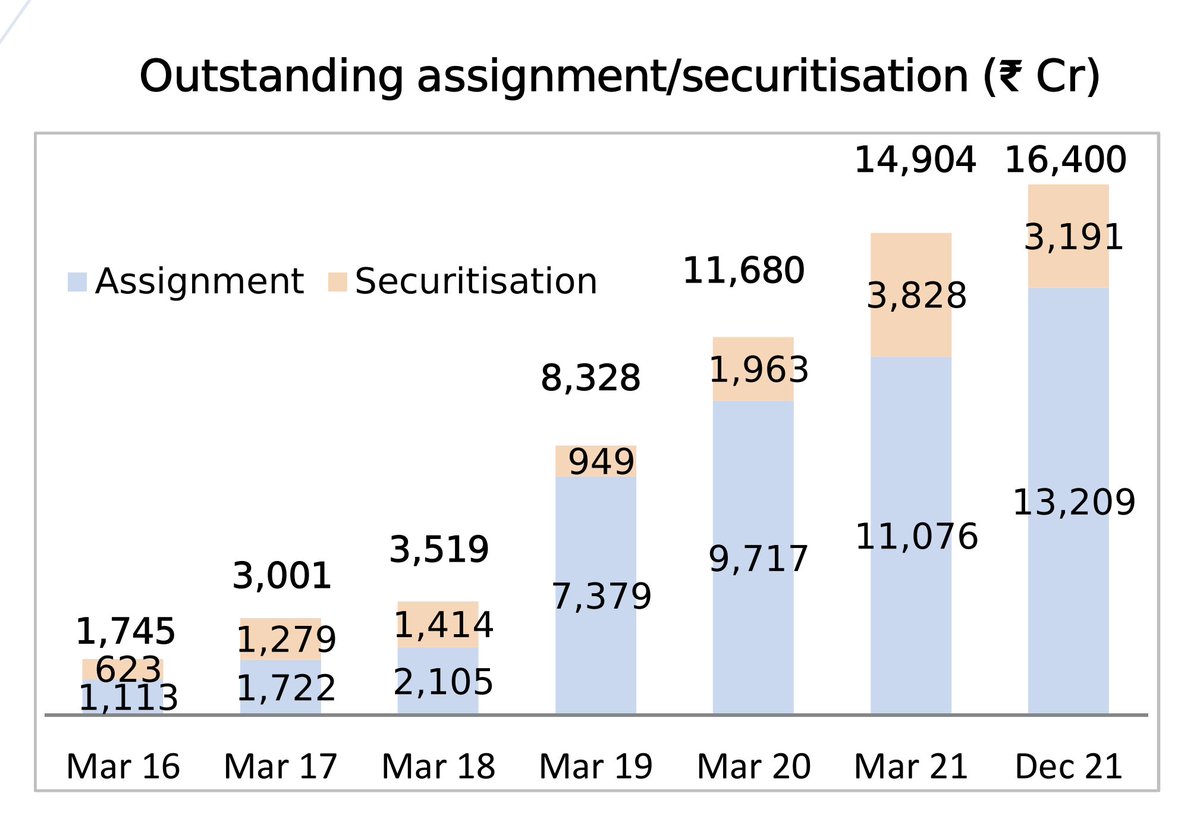

Roughly one-third of IIFL loan book is assigned/securitized/co-lent.

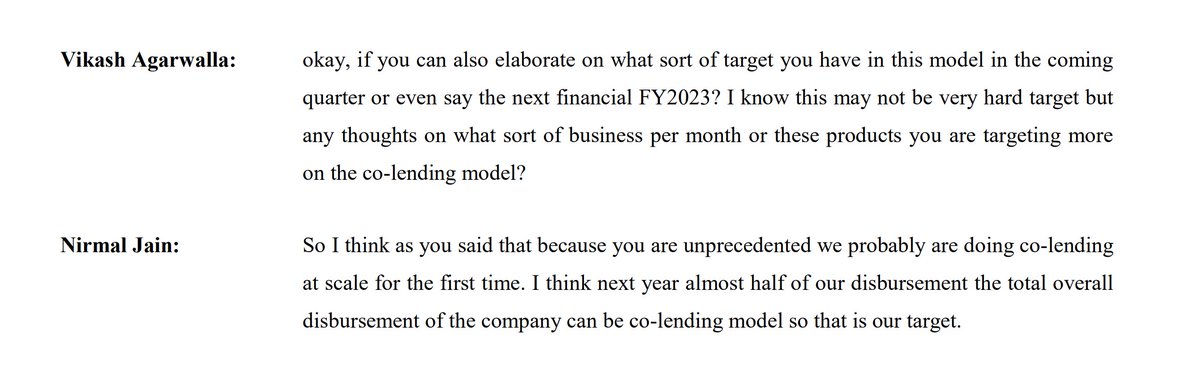

Guidance is to take this up to 50% co-lent, 50% on balance sheet disbursement next year.

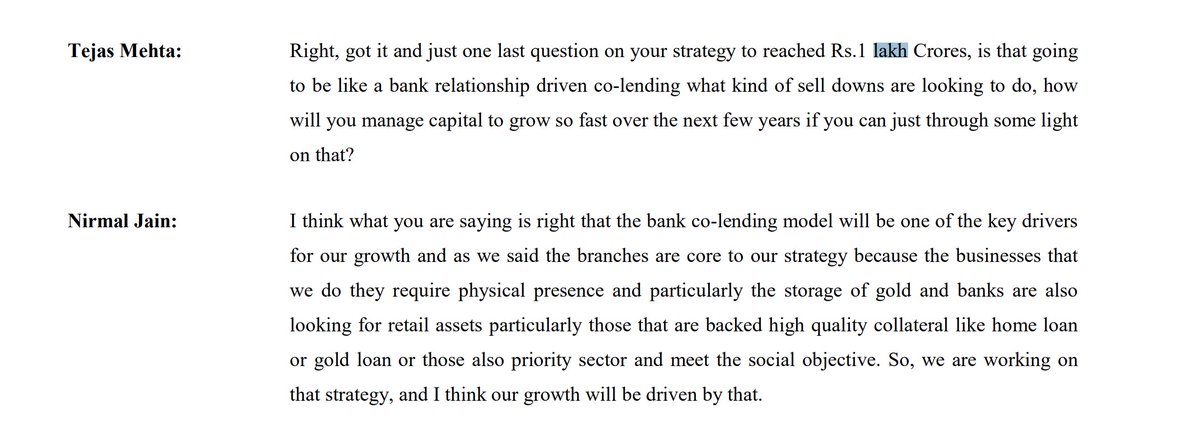

Co-lending will be a major strategy to reach 1 lakh crore loan book.

Sharing is caring has never been truer :)

Sharing is caring has never been truer :)

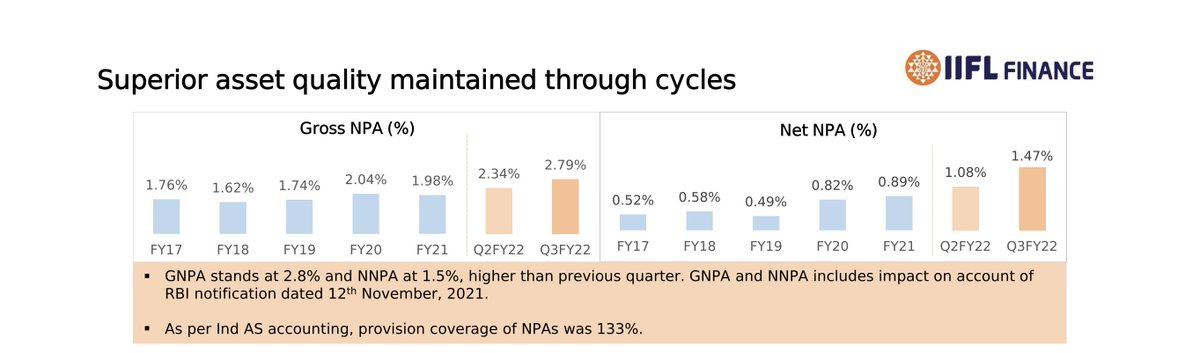

4. Asset Quality

Asset quality has been fairly stable given that we are in a once-a-century pandemic. Around 30 bps of GNPA is due to RBI circular (more on that in next tweet).

Asset quality has been fairly stable given that we are in a once-a-century pandemic. Around 30 bps of GNPA is due to RBI circular (more on that in next tweet).

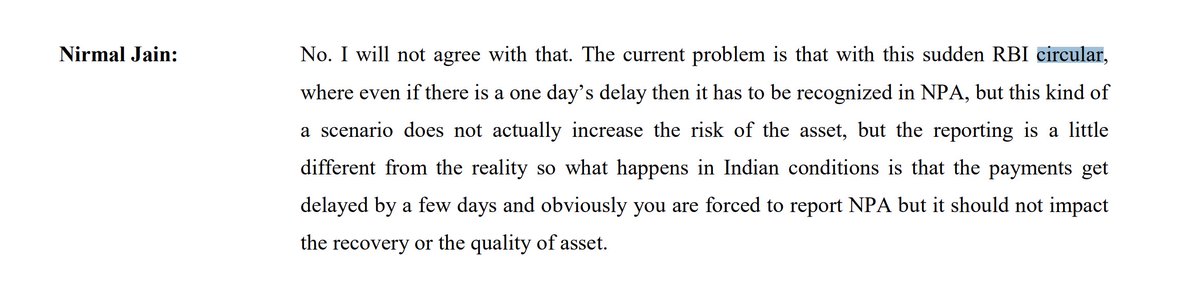

One thing worth worth mentioning is that RBI had released a circular in October which now requires NBFC to follow same norms for declaring an account as NPA as banks. If after 90 days customer has not paid back all due monies, they are classified as NPA .

Earlier, customer could pay just 1 instalment & escape becoming an NPA.

This circular does not impact asset quality but rather the accounting of asset quality, making it more conservative.

This circular does not impact asset quality but rather the accounting of asset quality, making it more conservative.

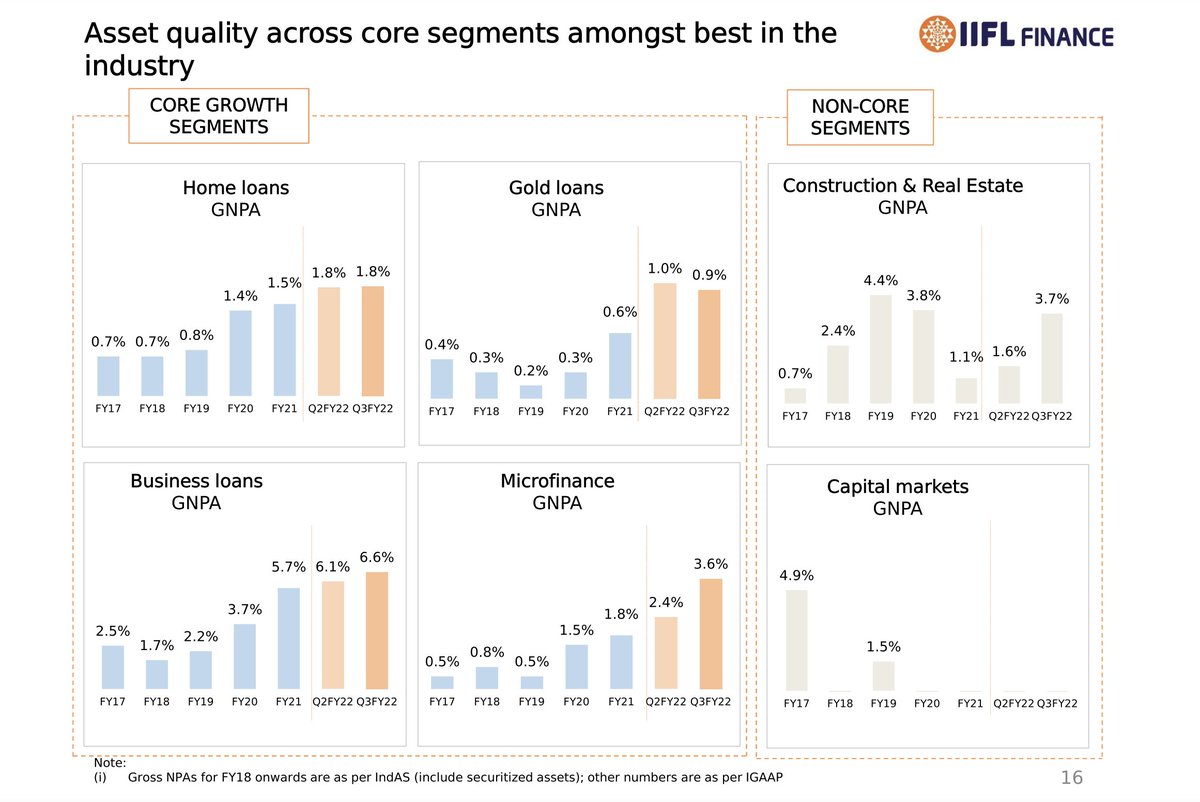

Their core segment of home & gold loans have quite low GNPAs.

More importantly, they have fairly high provision coverage.

The provision they have taken is as per ECL norms which are stricter than RBI norms. Provision coverage ratio is 133%. Meaning, they have provisions for 133% of GNPA.

The provision they have taken is as per ECL norms which are stricter than RBI norms. Provision coverage ratio is 133%. Meaning, they have provisions for 133% of GNPA.

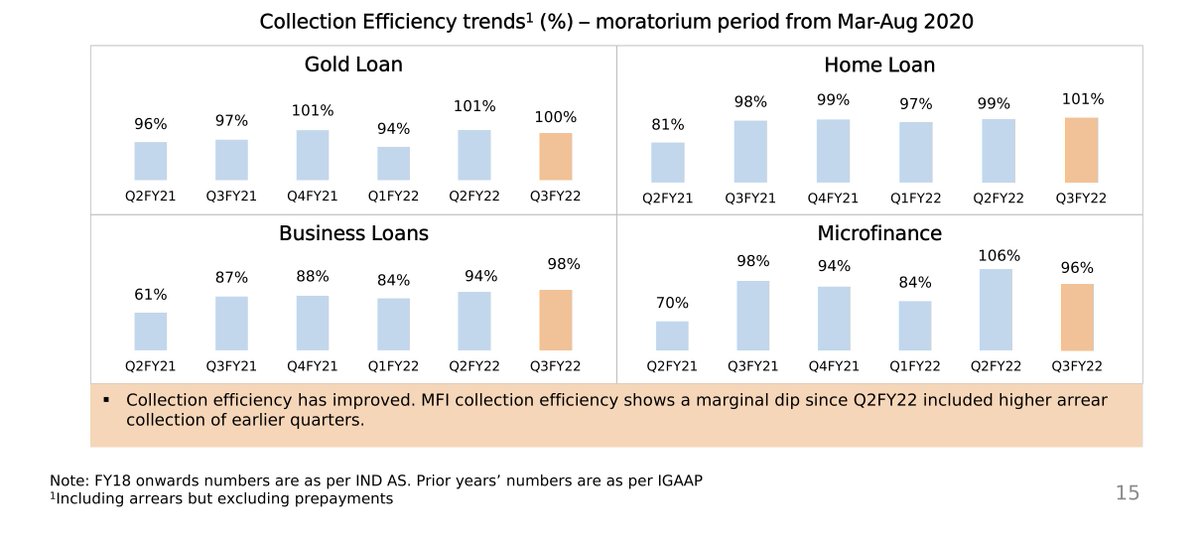

Lastly, leading indicators like collection efficiency indicate that stress might be peaking.

5. Growth

Historically, core AUM has grown at 20% CAGR which is very healthy. Now that non-core AUM has winded down & will continue to wind down, overall AUM growth can accelerate.

Historically, core AUM has grown at 20% CAGR which is very healthy. Now that non-core AUM has winded down & will continue to wind down, overall AUM growth can accelerate.

Management wants to grow AUM at 25-30% & reach 1 lakh crore AUM in 3-4 years.

I find this to be a healthy yet conservative target growth rate.

I find this to be a healthy yet conservative target growth rate.

We can see clear growth triggers. They have opened 350 new branches. They had 2500 branches. at FY21 end. Will open 300 more branches.

They had 20k employees at FY21 end. We can see the investment for growth. They hired 6000 employees in 9MFY22.

We can see their investments in digitisation as well. Whats app based end to end lending. Gold loan @ home. IIFL money app.

Another key driver of growth will be co-lending. They already have partnerships with DBS Bank and Union Bank of India for co-lending of gold loan and home loan

respectively.

Co-lending will be 50% of disbursements next FY onwards. Will will be ROE accretive.

respectively.

Co-lending will be 50% of disbursements next FY onwards. Will will be ROE accretive.

6. Profitability

One of the metrics which helped me develop conviction to invest, 'clinching evidence' is the asset quality through last 2 years. Despite 133% provision, despite 2.5x the provisions required by RBI, the RoA & RoE have remained healthy.

One of the metrics which helped me develop conviction to invest, 'clinching evidence' is the asset quality through last 2 years. Despite 133% provision, despite 2.5x the provisions required by RBI, the RoA & RoE have remained healthy.

11% RoE at bottom of the cycle.

For comp, Kotak mahindra bank RoE through the years.

For comp, Kotak mahindra bank RoE through the years.

Bajaj Finance RoE was 13% in Fy21.

From bajF annual report:

"Despite significantly elevated level of losses in FY2021, the Company delivered return on assets and return on equity

of 3.1% and 12.8% respectively on a consolidated basis."

From bajF annual report:

"Despite significantly elevated level of losses in FY2021, the Company delivered return on assets and return on equity

of 3.1% and 12.8% respectively on a consolidated basis."

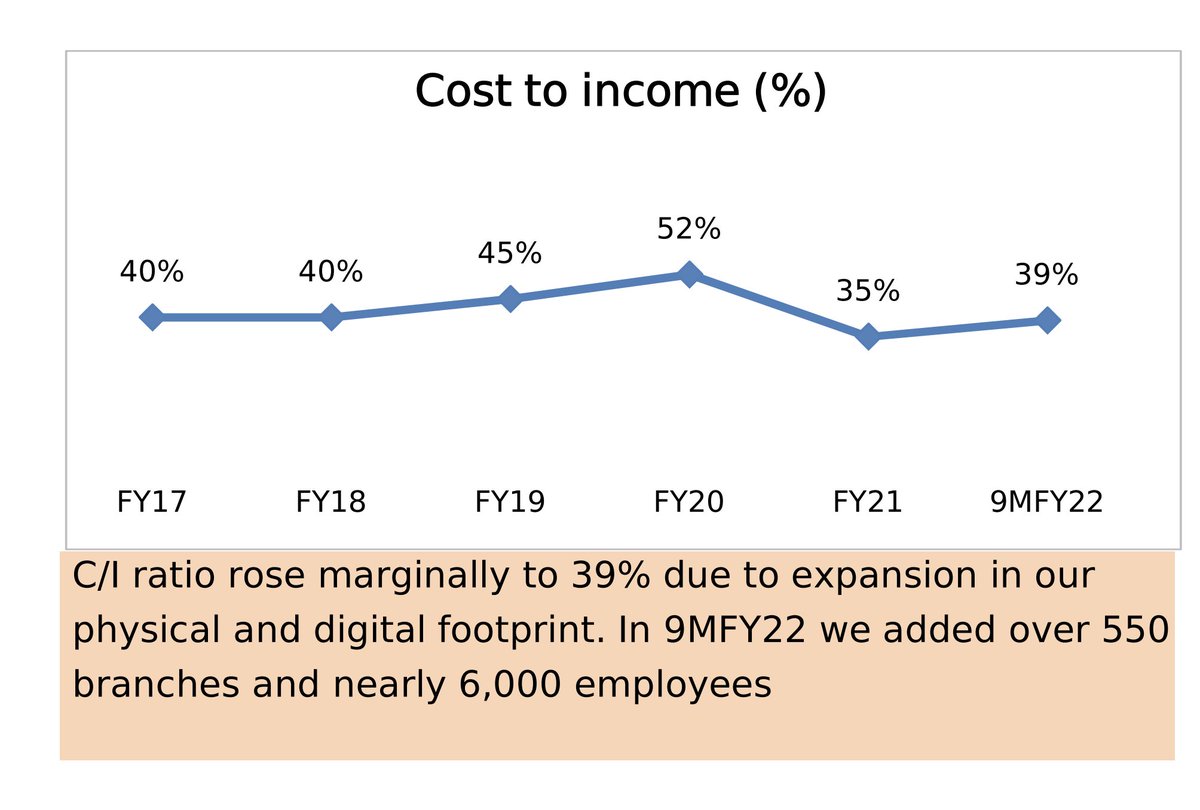

IIFL is investing for growth right now. This reflects in their elevated cost to income ratio.

They expect this to go down to 33% as investment in digitisation & branch expansion generates turns & get amortized over larger AUM.

Lower Cost to income & normalisation of asset quality & provisions will counter the downward pressure on yields due to rising competitive intensity in gold loan space.

7. Management Management Management

Most important variable in lending is management.

We can find enough & more evidence of management being conservative here.

Check out @omkaracap video for promoter background:

youtube.com

Most important variable in lending is management.

We can find enough & more evidence of management being conservative here.

Check out @omkaracap video for promoter background:

youtube.com

Lots of liquidity. Want to guard against any mishap.

Biggest signal here which i already talked about is the provisioning which is very conservative.

They also mentioned in 1 interview that they prefer to have longer term liability even at higher cost to ensure stability of loan book.

They also mentioned in 1 interview that they prefer to have longer term liability even at higher cost to ensure stability of loan book.

Management has chosen not go go after BNPL loans despite them being all the fancy today. They want to stay within their circle of competence. Dont want to run after next hot thing. Shows that they are conservative.

8. Anti-thesis

(i) Lot of competition in gold loan sector. PSU banks are entering this space. Gold loan yields have been on downward trajectory. Can they go lower?

Acc to management they will stabilize around these yields maybe 50 bps lower. But investor has to remain guarded.

(i) Lot of competition in gold loan sector. PSU banks are entering this space. Gold loan yields have been on downward trajectory. Can they go lower?

Acc to management they will stabilize around these yields maybe 50 bps lower. But investor has to remain guarded.

(ii) MFI & business loan GNPA are still rising (even accounting for RBI circular impact). Is it possible that there is more stress to come? Maybe. We must remain on guard as investors.

(iii) Any covid wave 4 could impact asset quality even more.

(iv) In the gold loan portfolio, their loan to value at portfolio level is around 65% (13600/21000 = 65%) (43.3 ton of gold = 21000 cr).

RBI norms only allow up to 75% of disbursement.

(iv) In the gold loan portfolio, their loan to value at portfolio level is around 65% (13600/21000 = 65%) (43.3 ton of gold = 21000 cr).

RBI norms only allow up to 75% of disbursement.

So any growth heree has to come from tonnage growth. Cant come from giving higher loan for same gold valuee.

9. Valuations

Due to 3 of the 4 business segments (Gold, MFI, MSME) having a poor image/perception, co gets a poor valuation. Currently at a p/e ratio of 10.8 & price. to book of 2. Despite having 20% RoE. Despite decent growth. Despite digitization.

Due to 3 of the 4 business segments (Gold, MFI, MSME) having a poor image/perception, co gets a poor valuation. Currently at a p/e ratio of 10.8 & price. to book of 2. Despite having 20% RoE. Despite decent growth. Despite digitization.

10. Thesis

As cost to income ratio normalizes , AUM grows at 25% led by co-lending & branch expansion & asset quality mean reverts (pre-covid 1% credit losses), we can expect strong profit growth. That provides us the bulk of the investment return even if there is no rerating.

As cost to income ratio normalizes , AUM grows at 25% led by co-lending & branch expansion & asset quality mean reverts (pre-covid 1% credit losses), we can expect strong profit growth. That provides us the bulk of the investment return even if there is no rerating.

Been making this thread for a week now. Do follow if you're interested in reading similar threads in the future.

List of all threads:

<End of thread>

List of all threads:

<End of thread>

Just to add the regular disclaimer: whatever I share is not ever not now not in this thread investmen advice or a buy or sell reco.

Do your own due diligence & make your own decisions.

Your risk capital, your research, your conviction, your gain, your pain. 🙏🙏

Do your own due diligence & make your own decisions.

Your risk capital, your research, your conviction, your gain, your pain. 🙏🙏

Loading suggestions...