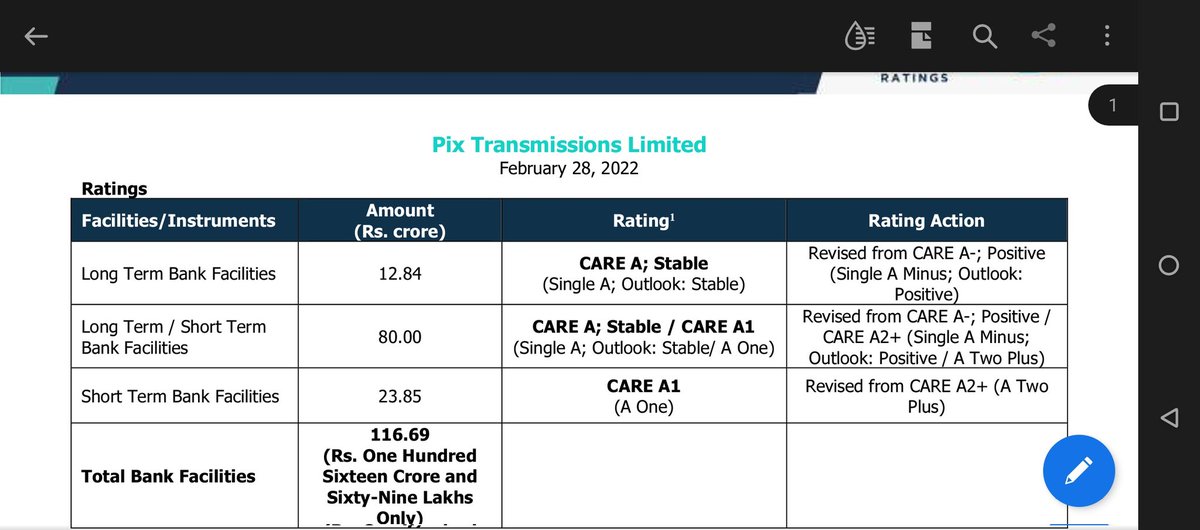

Pix rating has been upgraded to A/A1.

The rating report lauds the stable margins despite 100% increase in rubber (raw material) prices.

The rating report lauds the stable margins despite 100% increase in rubber (raw material) prices.

In FY21, the company had undertaken capex to the tune of ~Rs.25 crore which was mainly towards technology upgradation. As per the management, improvement in technology has led the company to phase out older machinery with latest technology.

It is also commendable to see operating margin has only gone down 2% or so while rubber prices have gone up 100% over last few years. Operating margin are expected to be sustainable above 25%.

As per the management, entire current capex project is expected to be completed by Q1FY23.

Capex for FY23-FY24 is still under consideration stage and will focus mainly on upgrading machinery and equipment for meeting market demand as well as introducing new products to make PTL as one-stop shop for its industrial customers.

The company would assess the demand situation and accordingly decide on the capex. The capex for FY23-24 is expected to be funded through internal accruals owing to strong cash generation ability of the company.

With normalization in business operations, company’s operating expenses are also expected to go up. Despite the same, PTL is expected to report operating margin above 25% on sustained basis for near term.

Disc : invested & biased this is not a buy or sell reco

Disc : invested & biased this is not a buy or sell reco

Loading suggestions...