A thread🧵 on Piramal Enterprises and upcoming special situation.

A classic tale of "Beauty and the beast".

A business that everybody wants to own and the one nobody wants to own.

Let's go for a deep dive -

A classic tale of "Beauty and the beast".

A business that everybody wants to own and the one nobody wants to own.

Let's go for a deep dive -

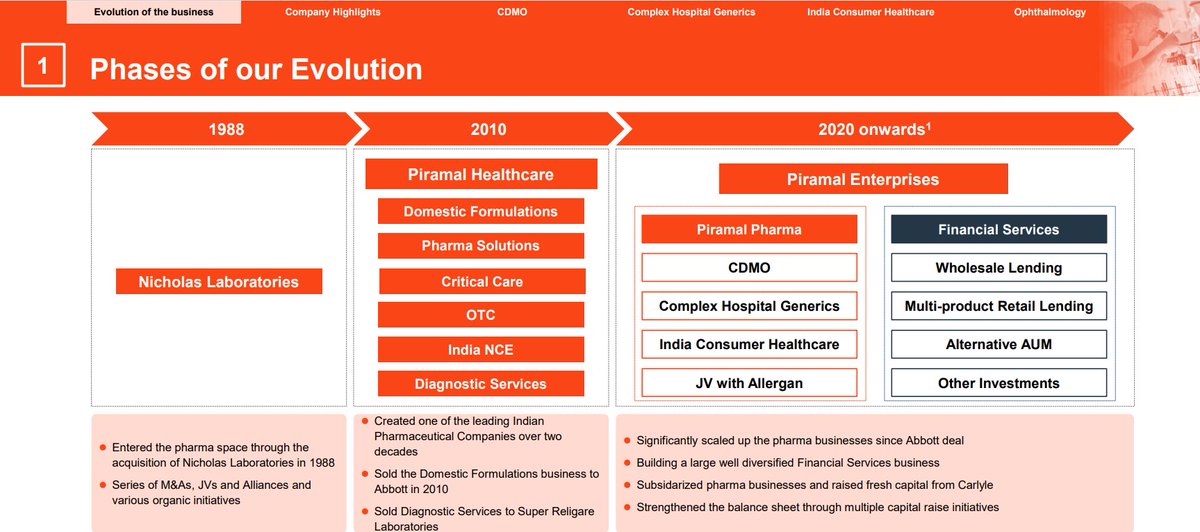

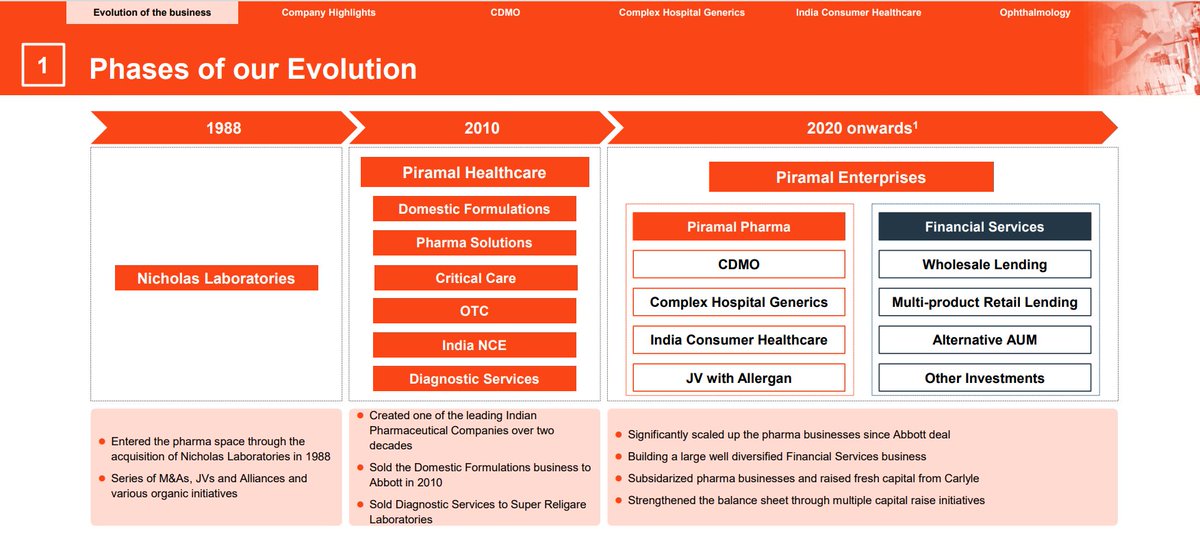

1st let's start with the history of Piramal Group and specifically one entrepreneur - Mr Ajay Piramal.

Piramal Enterprises was incorporated as Indian Schering Limited in 26th April of the year 1947 under British Schering Ltd.

Piramal Enterprises was incorporated as Indian Schering Limited in 26th April of the year 1947 under British Schering Ltd.

The name of the company was changed from Indian Schering Ltd to Nicholas Laboratories India Ltd with effect from 27th September of the year 1979.

In 1992, the company's name was changed from Nicholas Laboratories to Nicholas Piramal Limited.

In 1992, the company's name was changed from Nicholas Laboratories to Nicholas Piramal Limited.

In 1980 one passionate entrepreneur Ajay Piramal takes the lead of the group and since then the group has transformed into one of the biggest corporate groups on India.

In 2008, the name was changed to Piramal Healthcare limited.

By 2010, it became one of the biggest formulations pharma company in India.

By 2010, it became one of the biggest formulations pharma company in India.

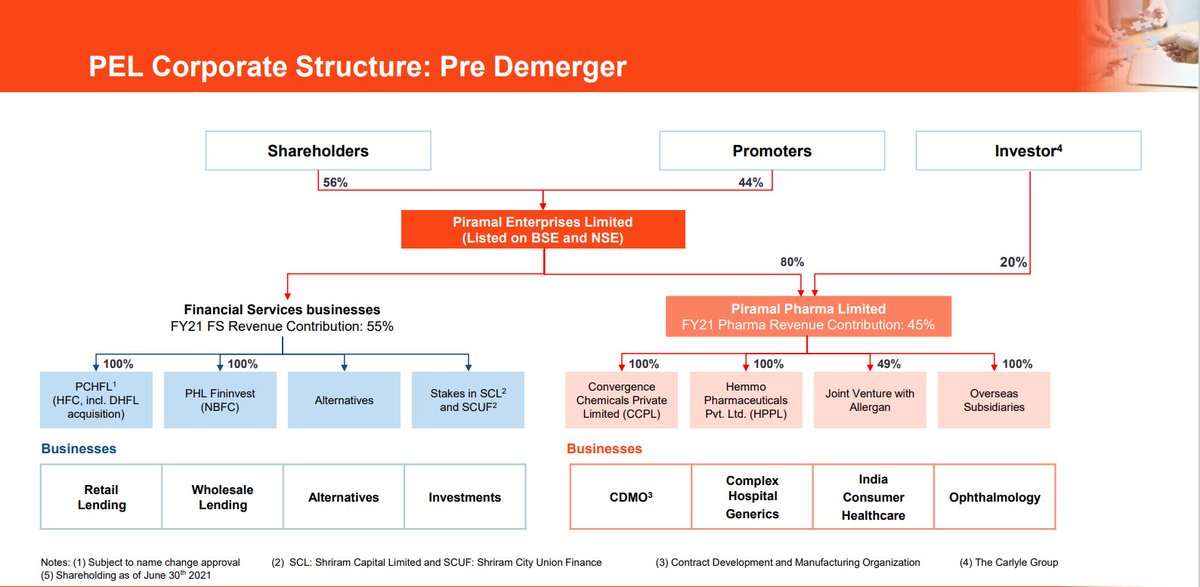

Currently they have 3 main businesses -Piramal Financial Services, Piramal Pharma and Piramal Realty.

Piramal Financial Services and Piramal Pharma comes under a single entity called "Piramal Enterprises" which is gonna get de-merged by the end of this year.

Piramal Financial Services and Piramal Pharma comes under a single entity called "Piramal Enterprises" which is gonna get de-merged by the end of this year.

This is the current corporate structure - 44% is with the promoter and 56% is with the shareholders.

2019 created a new entity called Piramal Pharma ltd in which they transferred their entire pharma business and sold in 2020, sold 20% stake to "Carlyle group"

2019 created a new entity called Piramal Pharma ltd in which they transferred their entire pharma business and sold in 2020, sold 20% stake to "Carlyle group"

at valuation of 3.2$ Billion.

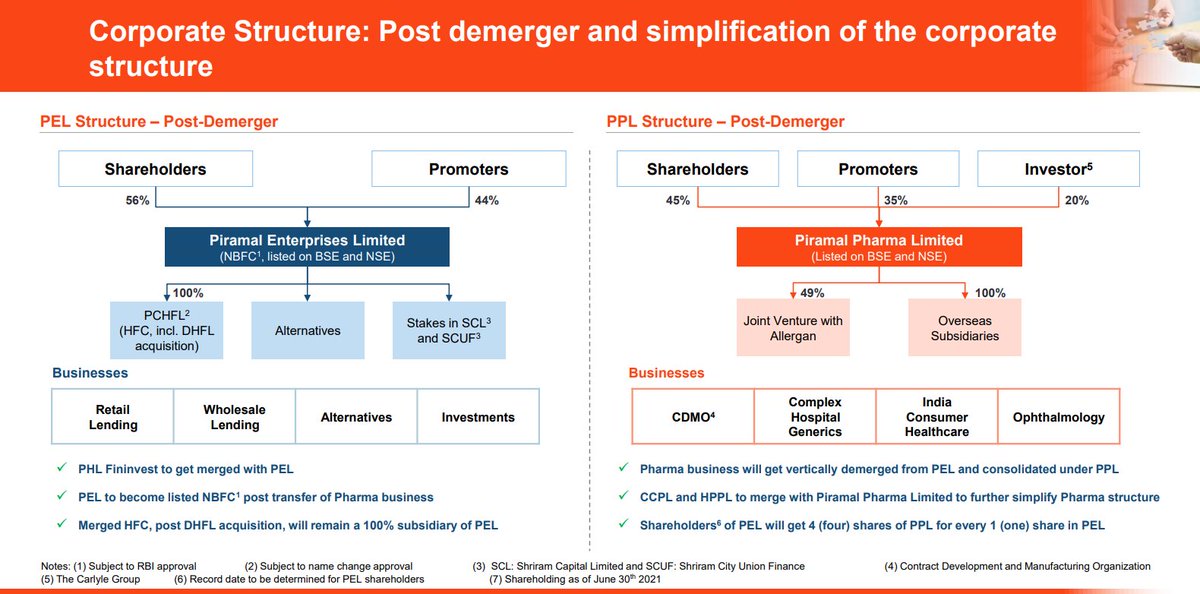

This the how the corporate structure is gonna be after the De-merger -

This the how the corporate structure is gonna be after the De-merger -

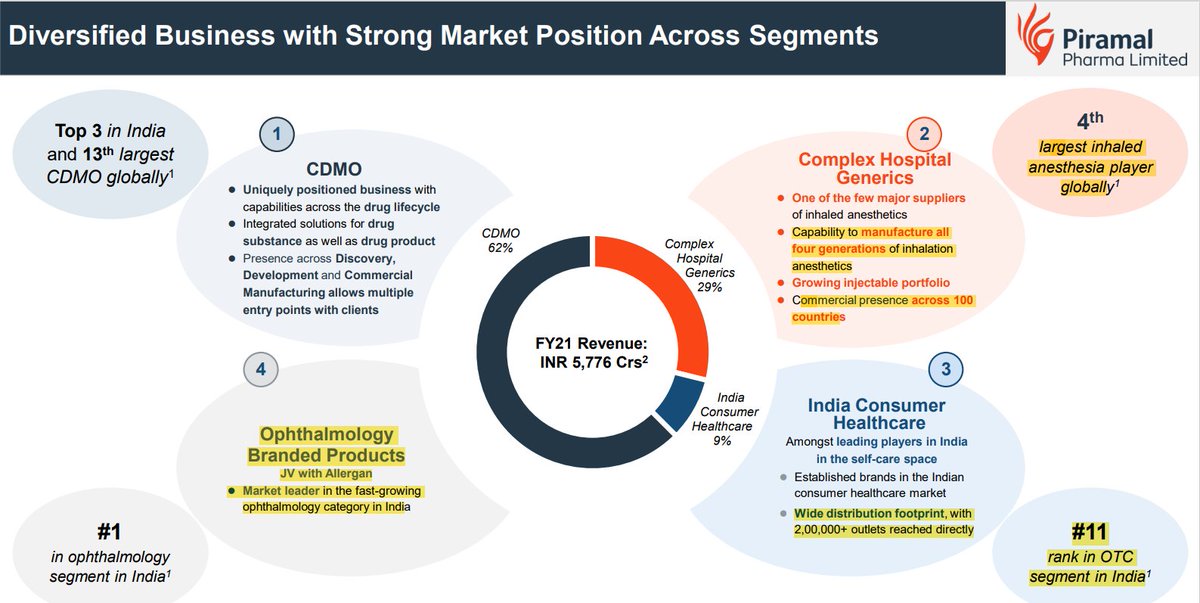

Now first let's talk about the "Beauty" part of the business, which is The Pharma Business and one that everybody wants to own.

So they have 4 main business segments in their Pharma Business -

CDMO

Complex Hospital generics

Indian Consumer Business

JV with Allergan

So they have 4 main business segments in their Pharma Business -

CDMO

Complex Hospital generics

Indian Consumer Business

JV with Allergan

1st let's take a look at the journey of their Pharma business.

So a you know they had this JV with Nicholas group back in 1980s when it was called Nicholas Laboratories.

Through many Mergers and Acquisitions they became one of the top Formulations pharma company of India.

So a you know they had this JV with Nicholas group back in 1980s when it was called Nicholas Laboratories.

Through many Mergers and Acquisitions they became one of the top Formulations pharma company of India.

In 2010 they sold their formulations business to ABBOTT INDIA for 3.2$ Billion.

They retained Indian Consumer healthcare, Complex hospital generics and CDMO business.

And from the cash they got from selling the Formulations business, they Did a big share buyback

They retained Indian Consumer healthcare, Complex hospital generics and CDMO business.

And from the cash they got from selling the Formulations business, they Did a big share buyback

Invested some of the money in CDMO and their other businesses (Financial Services) and paid rest of the money as dividends back to the share holders.

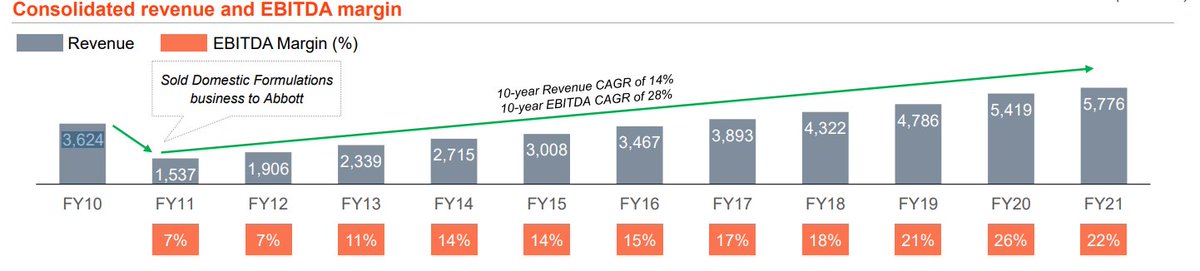

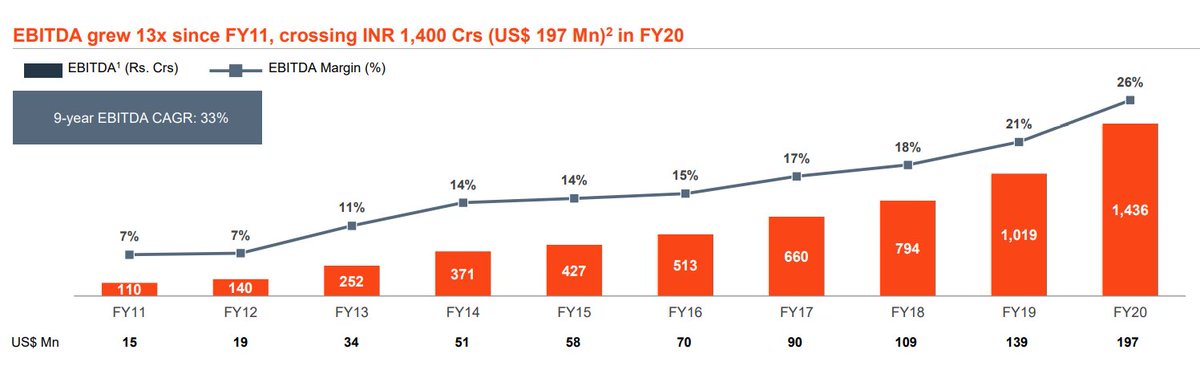

So in 2011 they had a revenue of 1537Cr.

It was a new start for them, and since then the has increased with 15% CAGR

So in 2011 they had a revenue of 1537Cr.

It was a new start for them, and since then the has increased with 15% CAGR

From 1537Cr in 2011 to 5419Cr in 2020.

EBITDA has grown from 110Cr in 2011 to 1436Cr in 2020 with EBITDA margins expanding from 7% to 26%. (simply amazing)

EBITDA has grown from 110Cr in 2011 to 1436Cr in 2020 with EBITDA margins expanding from 7% to 26%. (simply amazing)

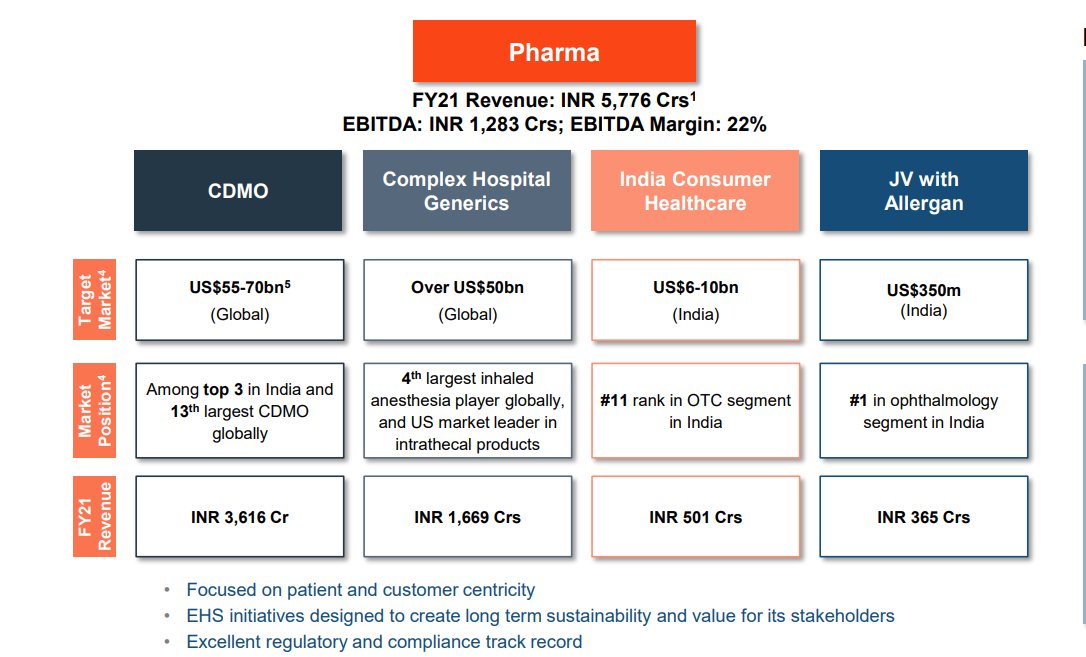

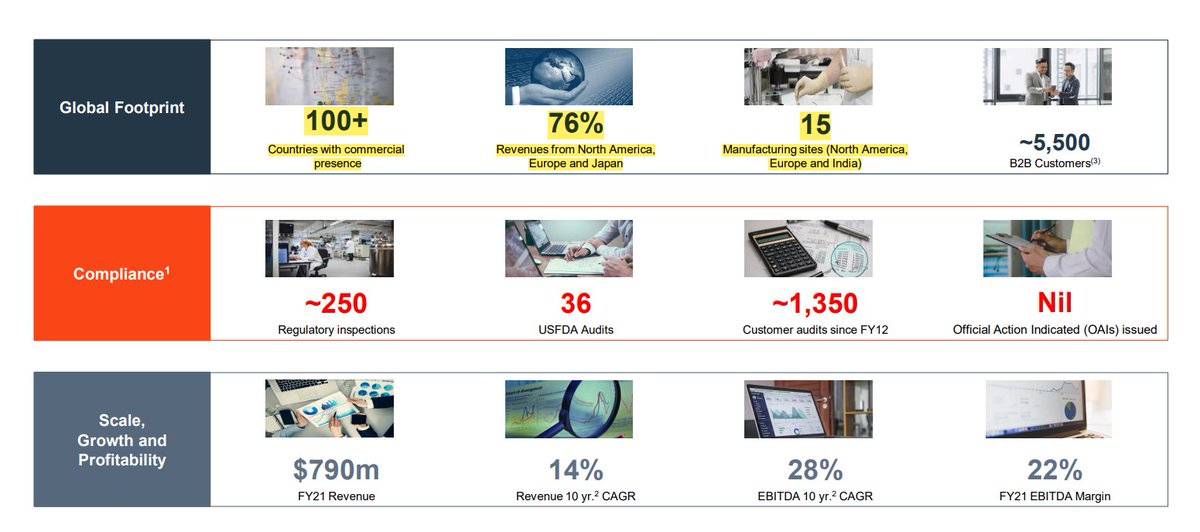

In FY21 their revenue was 5776Cr with 22% EBIDTA margins

They're 3rd largest CDMO in India and 13th largest Globally

4th Largest Anesthesia Player

1st in Ophthalmology (eye care) ( JV with Allergan)

11th in OTC (Over the counter - drugs for which you don't need prescription)

They're 3rd largest CDMO in India and 13th largest Globally

4th Largest Anesthesia Player

1st in Ophthalmology (eye care) ( JV with Allergan)

11th in OTC (Over the counter - drugs for which you don't need prescription)

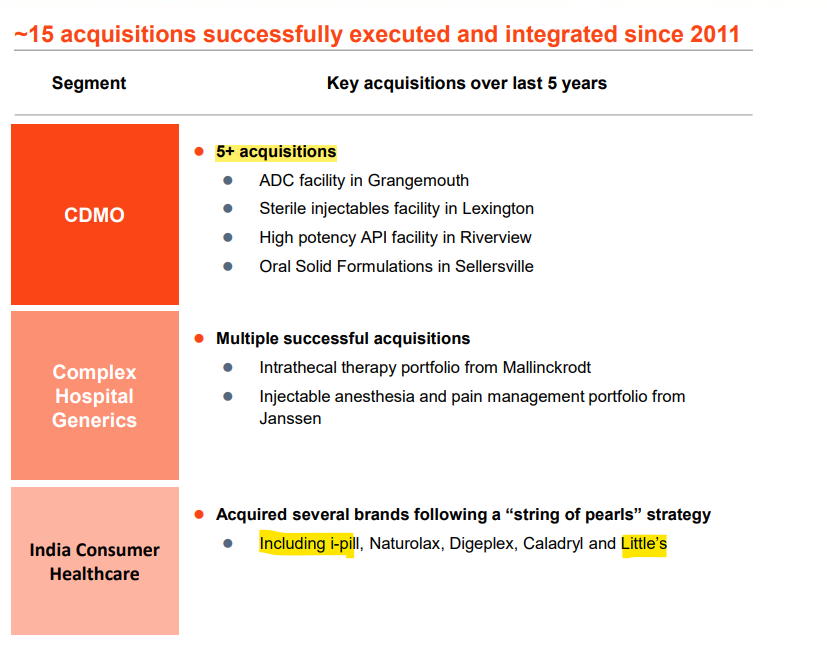

They have done 15 Acquisitions since 2011 and transformed their business in a world class CDMO business.

They did 5 acquisitions in CDMO segment.

Acquired the brands like i-pill and Little's(Baby care) in their Indian consumer business.

They did 5 acquisitions in CDMO segment.

Acquired the brands like i-pill and Little's(Baby care) in their Indian consumer business.

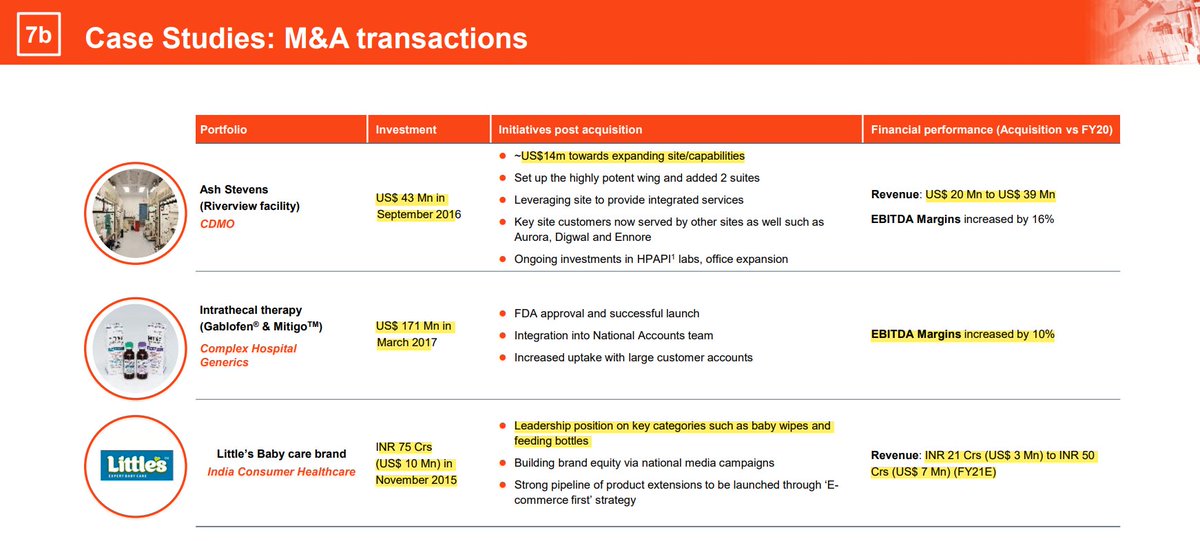

Few case studies of their past M&As

In 2016 acquired a facility in riverview for their CDMO business for 43$Mn.

Since the acquisition it's revenue has increased from 20$Mn to 39$Mn in 2021.

In 2015, acquired baby care brand called little's for 75Cr.

Current revenue - 50Cr

In 2016 acquired a facility in riverview for their CDMO business for 43$Mn.

Since the acquisition it's revenue has increased from 20$Mn to 39$Mn in 2021.

In 2015, acquired baby care brand called little's for 75Cr.

Current revenue - 50Cr

Their Regulatory track record is one of the best in industry.

With 36 USFDA inspections till date, 186 other regulatory inspections and 1203 customer audits since 2012.

They have got 0 OAI "Official Action Indicated" from USFDA till date.

With 36 USFDA inspections till date, 186 other regulatory inspections and 1203 customer audits since 2012.

They have got 0 OAI "Official Action Indicated" from USFDA till date.

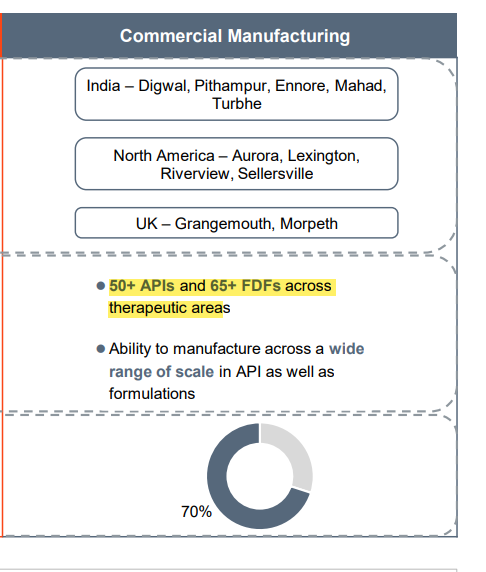

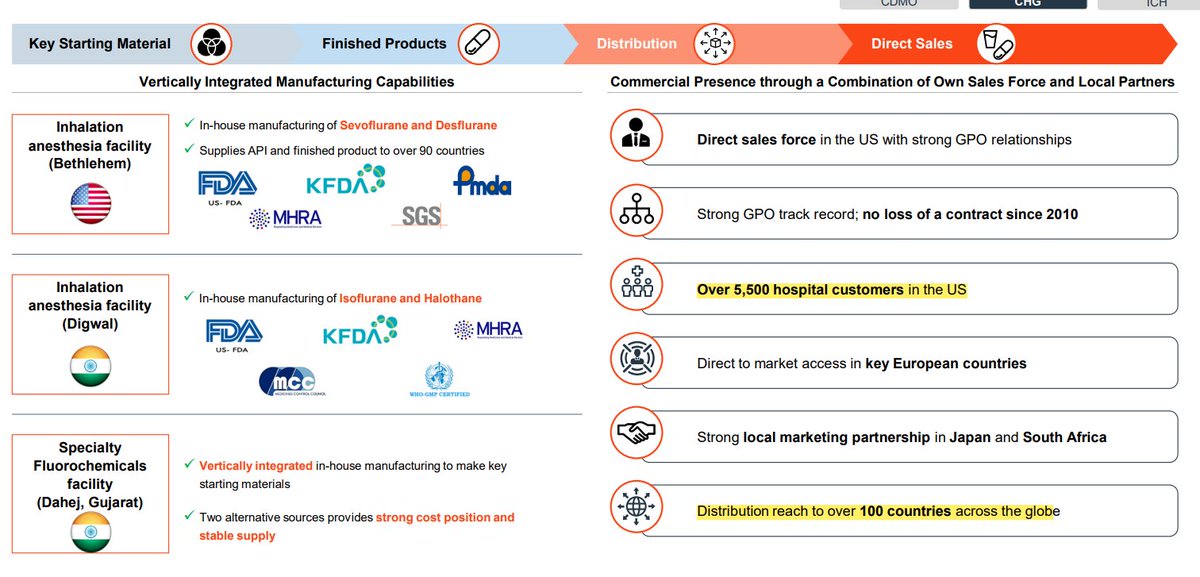

They have 15 manufacturing facilities spread across India, north America and Europe.

6 facilities in India with 1 for discovery services in ahemdabad.

76% revenue comes from regulated market and have presence in 100+ countries.

6 facilities in India with 1 for discovery services in ahemdabad.

76% revenue comes from regulated market and have presence in 100+ countries.

Now let's take a look at the each segment separately.

1st let's start with CDMO division -

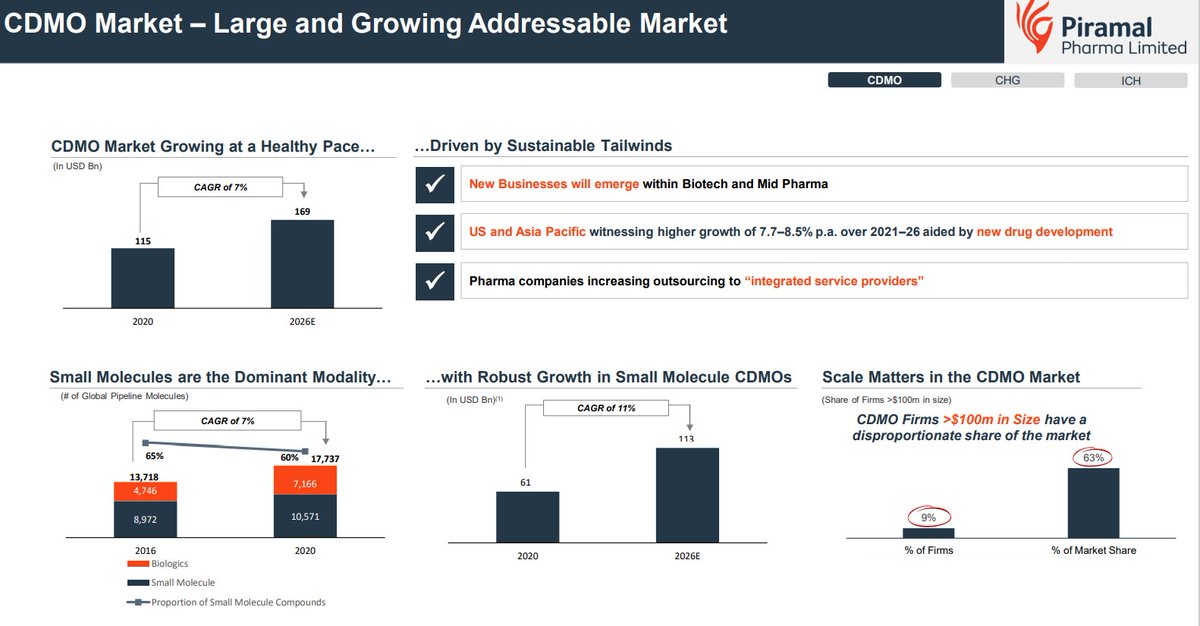

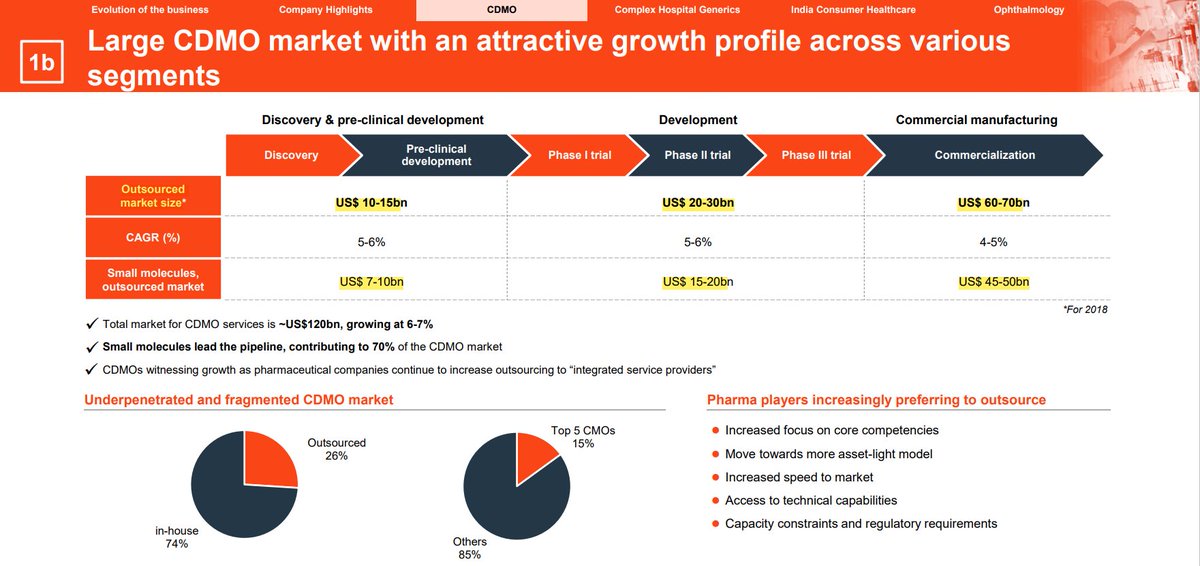

The current CDMO market is valued at around 115-120$ Billion and growing at 7% CAGR to reach 169$ Billion by 2026.

1st let's start with CDMO division -

The current CDMO market is valued at around 115-120$ Billion and growing at 7% CAGR to reach 169$ Billion by 2026.

US and Asia Pacific region is growing faster at 7.7-8.% CAGR.

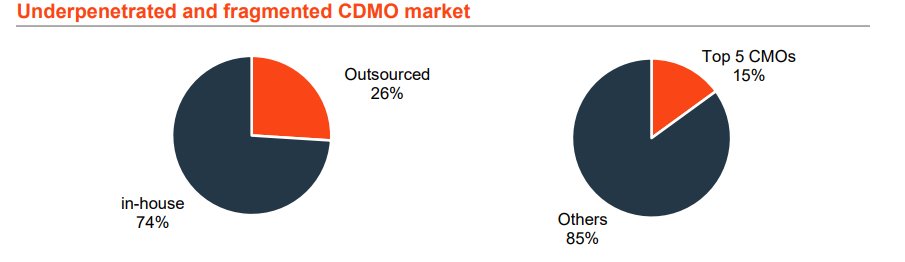

Only 26% work is Outsourced and 74% is still In-house.

Small Molecules are fastest growing at a CAGR of 11%

Only 26% work is Outsourced and 74% is still In-house.

Small Molecules are fastest growing at a CAGR of 11%

CDMO market is 3 main segments -

Discovery Services - Market size - 10-15$bn

Development Services - 20-30$bn

Commercial Manufacturing - 60-70$Bn

Small molecules contribute 70% of the pipeline of the CDMO market.

Discovery Services - Market size - 10-15$bn

Development Services - 20-30$bn

Commercial Manufacturing - 60-70$Bn

Small molecules contribute 70% of the pipeline of the CDMO market.

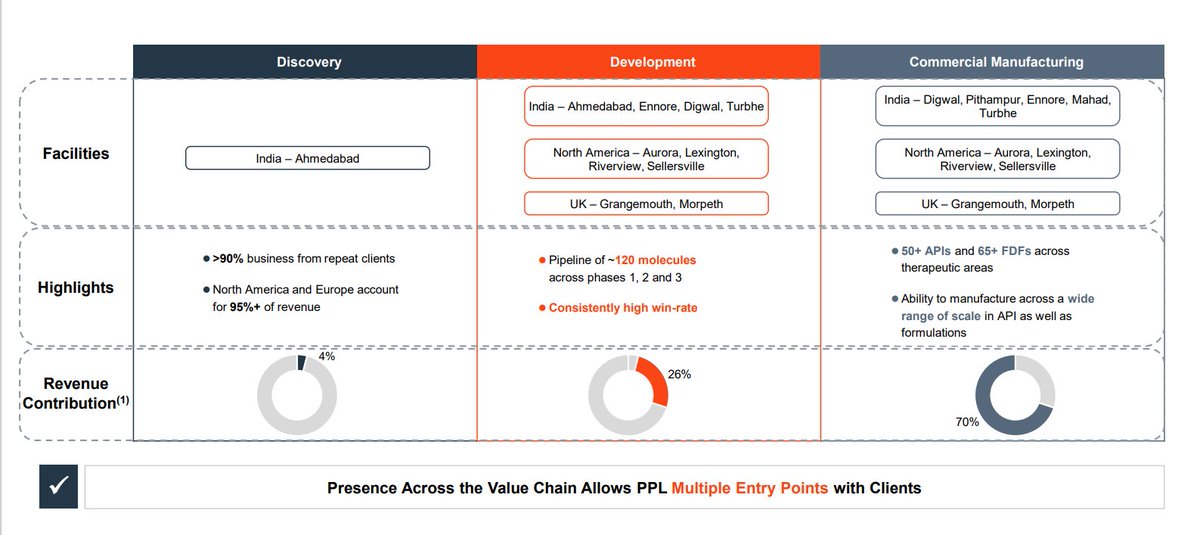

Piramal Pharma is present across the entire value chain of CDMO from discovery services to commercial manufacturing.

Have 1 facility for discovery services in Ahmedabad Gujarat.

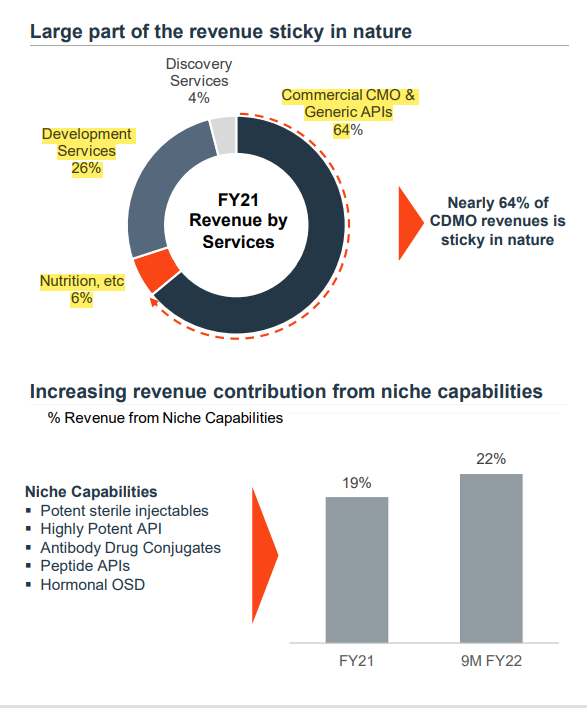

Only 4% of the revenues in CDMO segment comes from discovery services.

90% of the business is repeat

Have 1 facility for discovery services in Ahmedabad Gujarat.

Only 4% of the revenues in CDMO segment comes from discovery services.

90% of the business is repeat

business with USA & EUROPE contributing 94%.

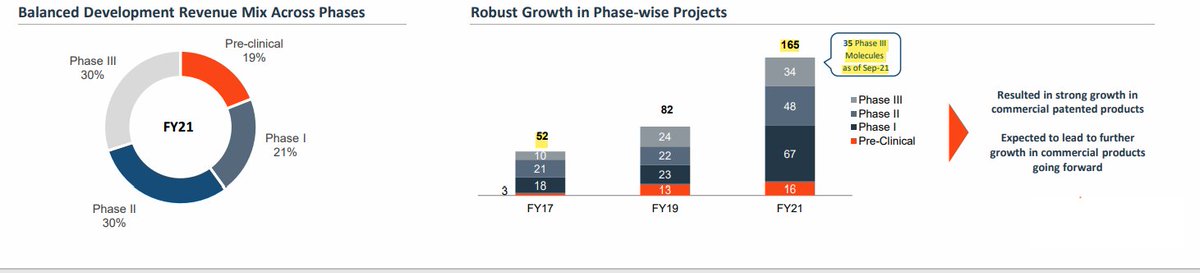

26% of the revenue comes from Development services which includes - Clinical trials, Phase I, Phase II and Phase III trials.

Currently have 34 projects in Phase III up from 10 In 2017.

Total molecules in Development phase - 165

26% of the revenue comes from Development services which includes - Clinical trials, Phase I, Phase II and Phase III trials.

Currently have 34 projects in Phase III up from 10 In 2017.

Total molecules in Development phase - 165

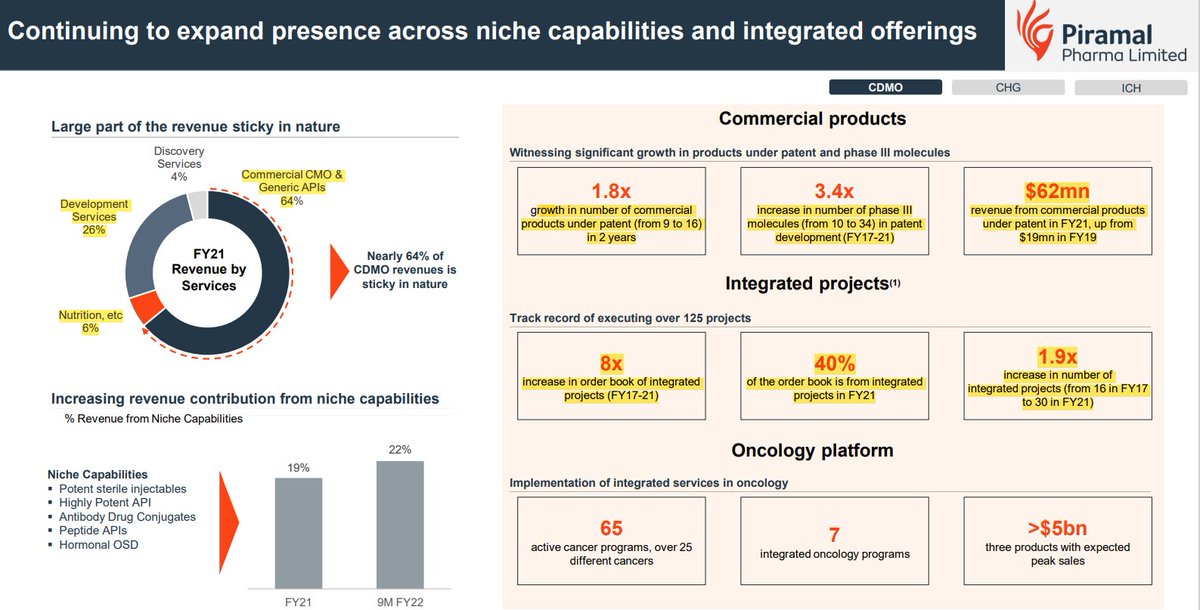

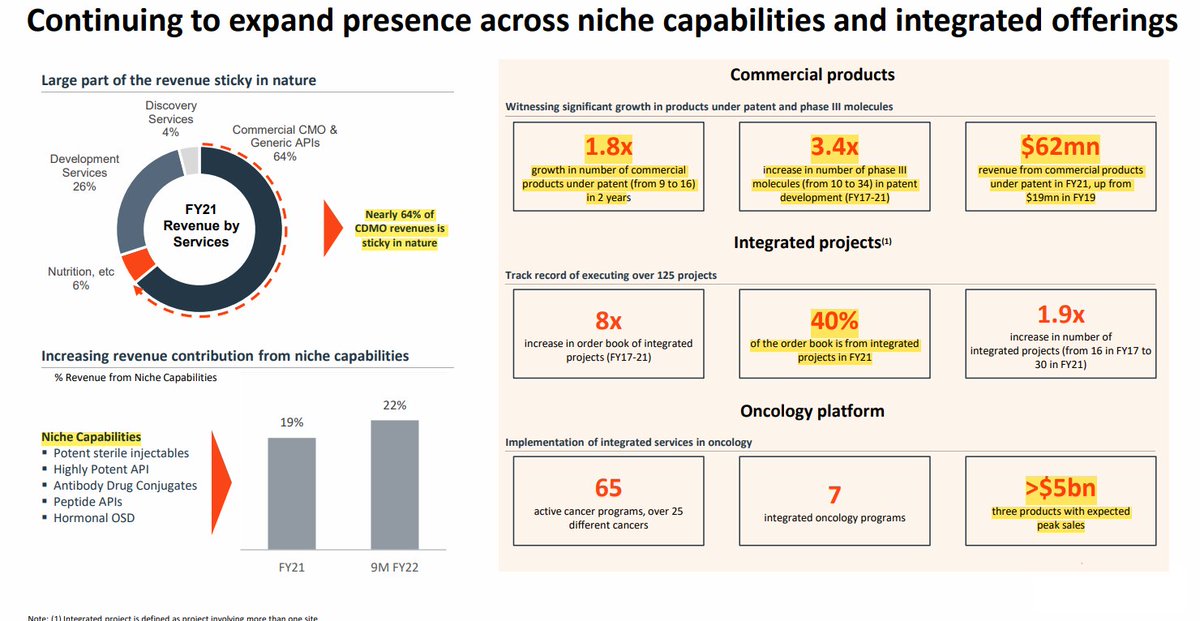

Have Niche capabilities like - Peptides, Injectables, Hormone OSD, HPAPI and anti body drugconjugets (Which helps in destroying the cancer cells without damaging the other cells).

70% revenues comes from Commercial Manufacturing.

22% is from Niche capabilities.

64% of the revenues is sticky in nature, most of it being for generic APIs and Commercial CMO (Contract manufacturing)

22% is from Niche capabilities.

64% of the revenues is sticky in nature, most of it being for generic APIs and Commercial CMO (Contract manufacturing)

This is what they do, have presence across the entire value chain of CDMO.

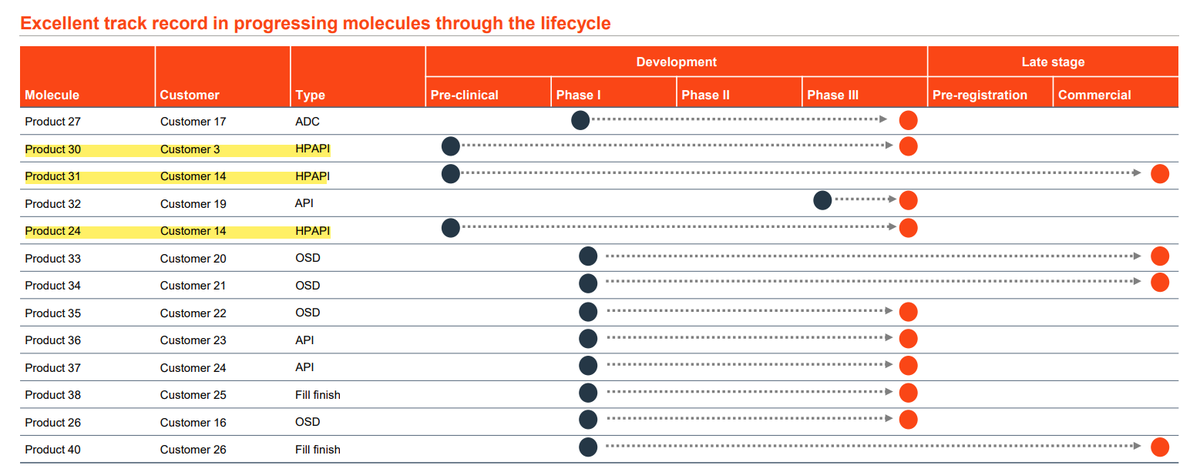

Developed High potent API from 3 customers from Pre-clinical to Commercialization phase.

Developed High potent API from 3 customers from Pre-clinical to Commercialization phase.

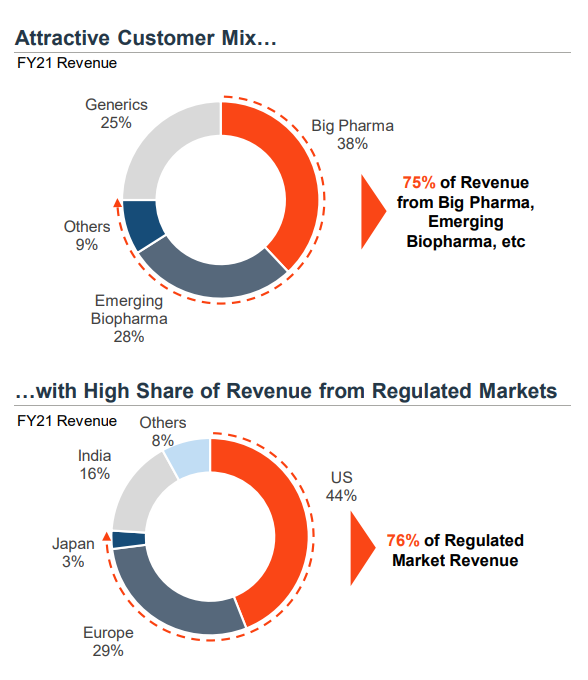

38% revenue comes from Big pharma and 285 from Biopharma.

765 from regulated markets.

Have long term relationships with clients 7-10 years.

Contribution from top 20 clients increasing, currently at 26%.

765 from regulated markets.

Have long term relationships with clients 7-10 years.

Contribution from top 20 clients increasing, currently at 26%.

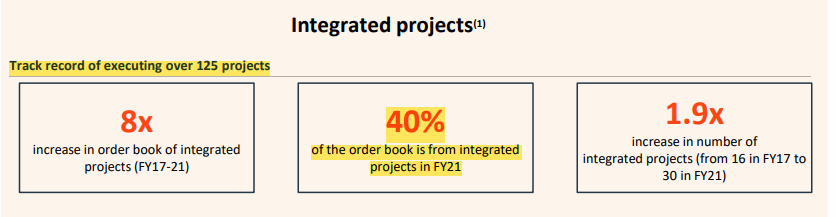

Started executing Integrated projects in 2017.

Since then have completed 125 projects and 40% of the order book is of Integrated projects.

(Integrated means - From discovery to commercialization)

Since then have completed 125 projects and 40% of the order book is of Integrated projects.

(Integrated means - From discovery to commercialization)

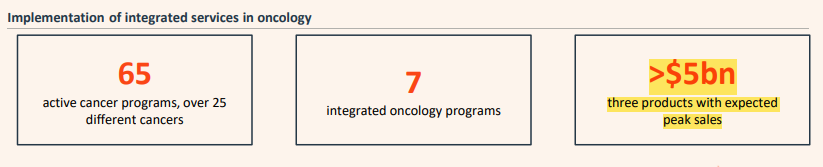

Also doing some integrated projects in Oncology with having the peak sales potential of >5$bn

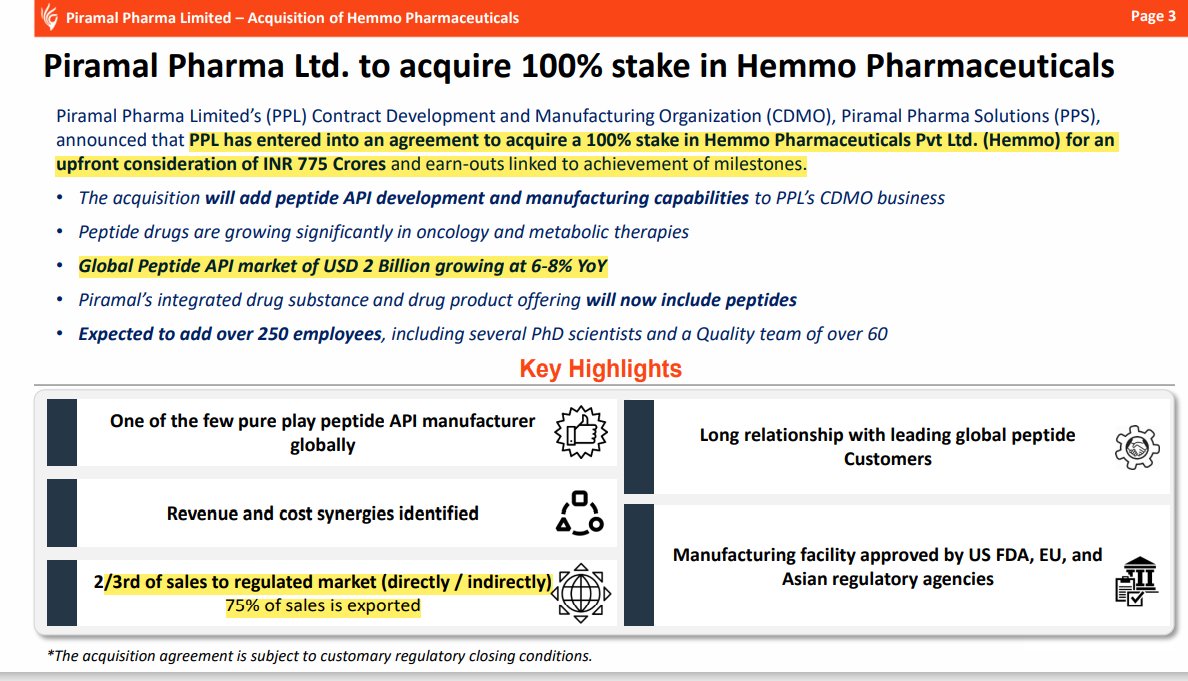

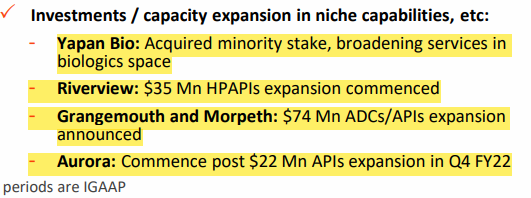

Acquired Hemmo pharma in 2021 for their capabilities in Peptide drugs.

Global API peptide market is valued at 2$Bn growing at 6-8% YoY.

Peptides are hard to manufacture as compared to small molecules and very few companies have the capability ( For example - NEULAND LABS)

Global API peptide market is valued at 2$Bn growing at 6-8% YoY.

Peptides are hard to manufacture as compared to small molecules and very few companies have the capability ( For example - NEULAND LABS)

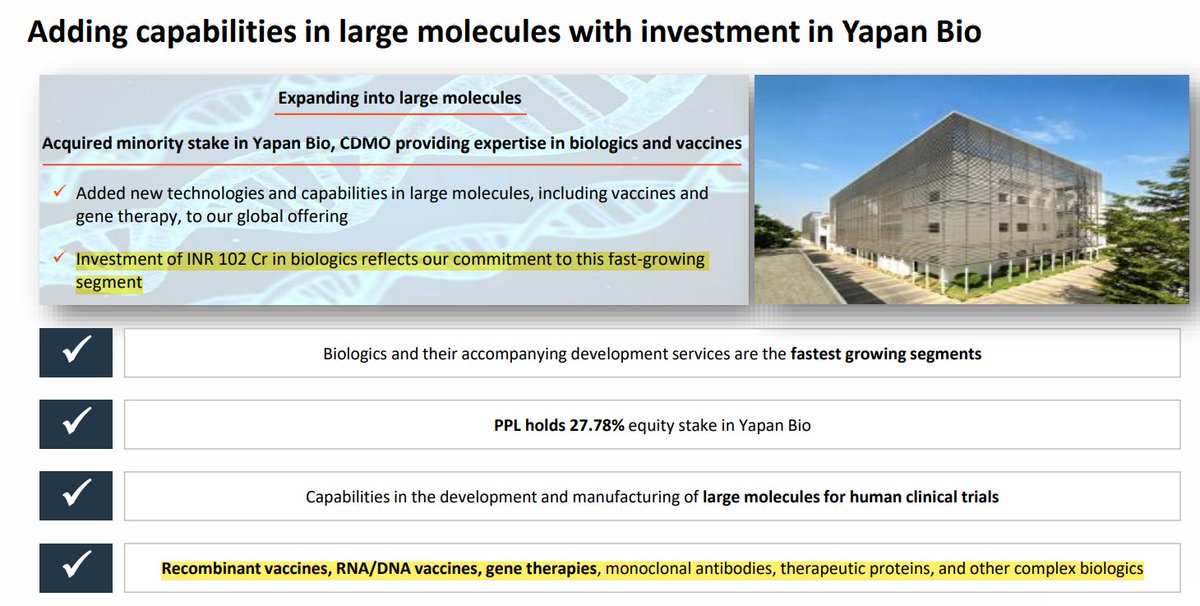

Acquired 27.78% stake in Yapan Bio for 102Cr to add the biologics (large molecules, extremely hard to manufacture) capabilities in it's portfolio.

Expanding their Riverview capacity for High Potent APIs for 35$ Mn and 74$ Mn for capacity expansion for Antibody Drug Conjugates & APIs

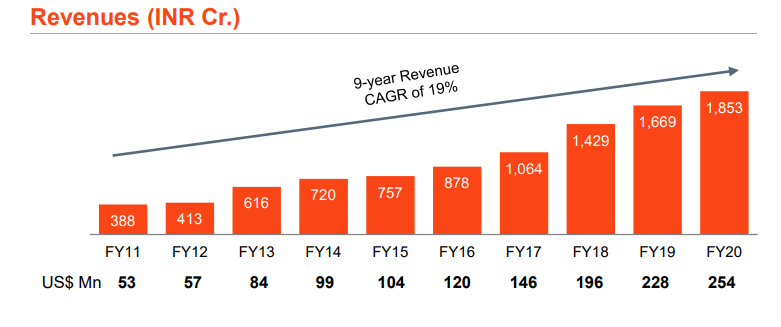

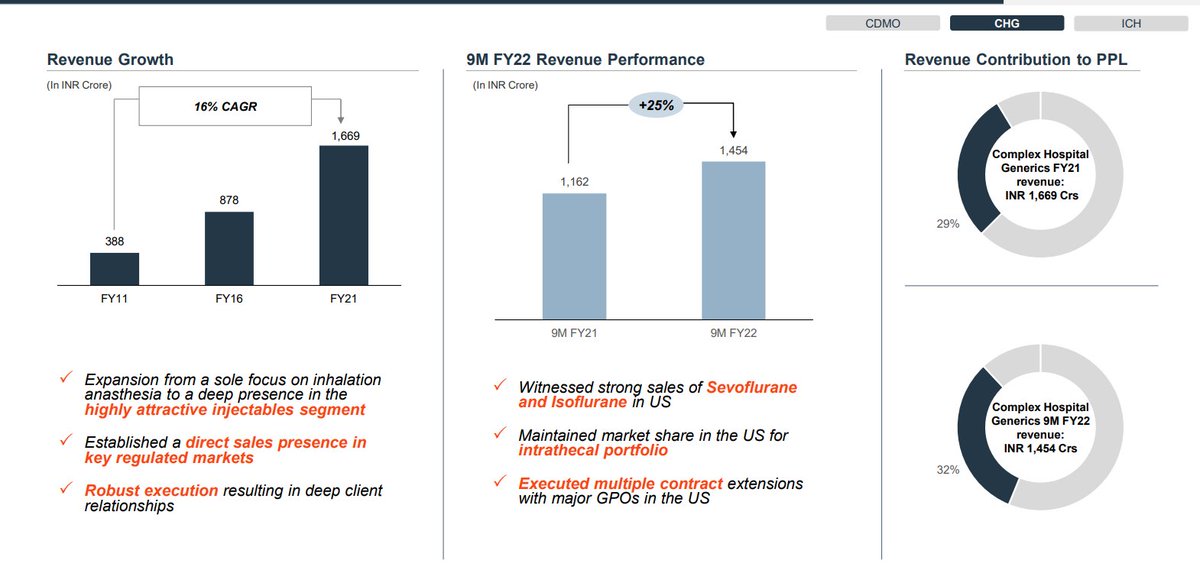

Now let's talk about the 2nd Division of Pharma Segment - COMPLEX HOSPITAL GENERICS

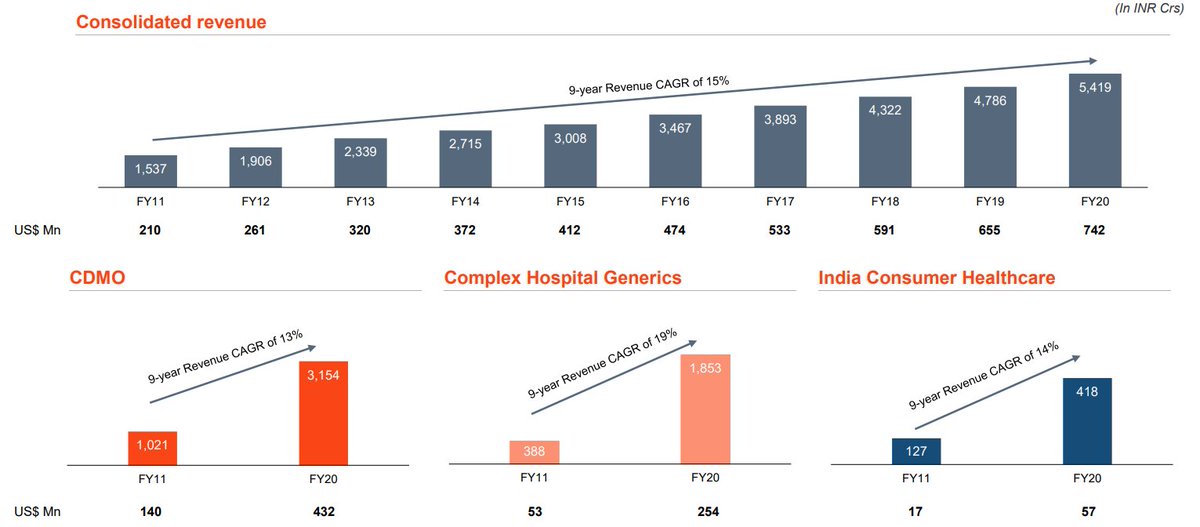

Revenue increased from 388Cr in 2011 to 1853Cr in 2020 and decreased a little in 2021 to 1669Cr due to Covid as many elective surgeries didn't happen.

Revenue increased from 388Cr in 2011 to 1853Cr in 2020 and decreased a little in 2021 to 1669Cr due to Covid as many elective surgeries didn't happen.

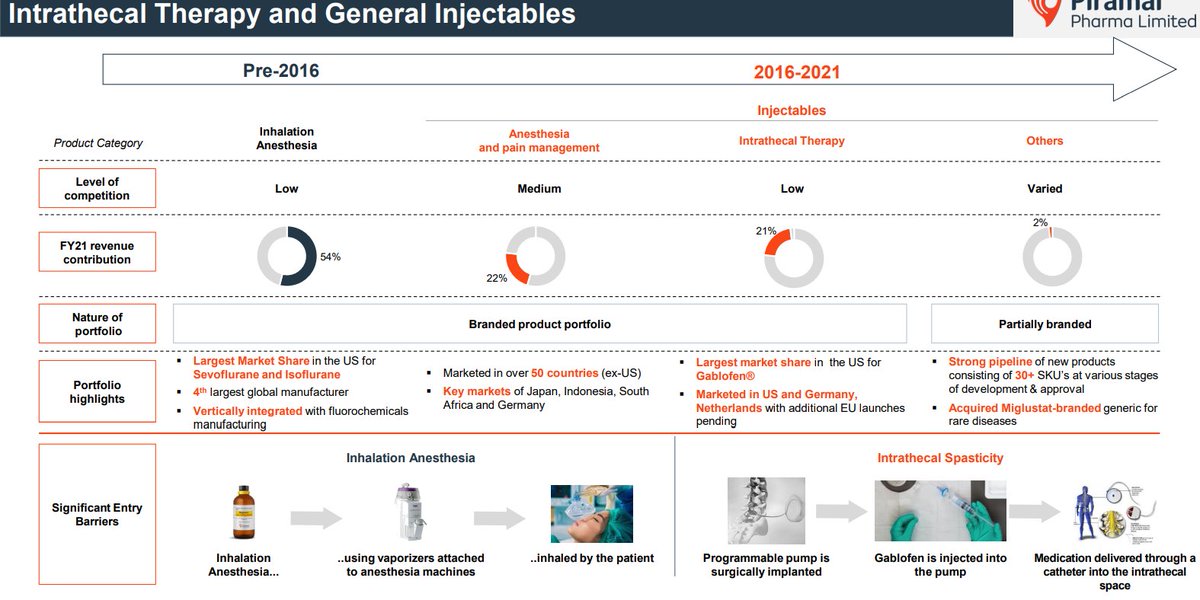

In this business segment they simply have products like Anesthesia, Injectable Anesthesia, pain management and other injectables.

( In layman language, anesthesia used while performing operations)

( In layman language, anesthesia used while performing operations)

This business segment have very high entry barriers as manufacturing injectables is not that easy and have high regulatory barriers.

Injectables have only 3.8 competitors as compared to 7 in case of oral dosage forms.

Injectables have only 3.8 competitors as compared to 7 in case of oral dosage forms.

4th largest manufacturer of anesthesia globally.

Have acquired many products over the years to reach at this position.

Have 30 new products in pipeline and 11 of them already have gotten the approval.

Have acquired many products over the years to reach at this position.

Have 30 new products in pipeline and 11 of them already have gotten the approval.

Have a strong distribution network and brand with presence in over 5500+ hospitals in US and 100+ countries.

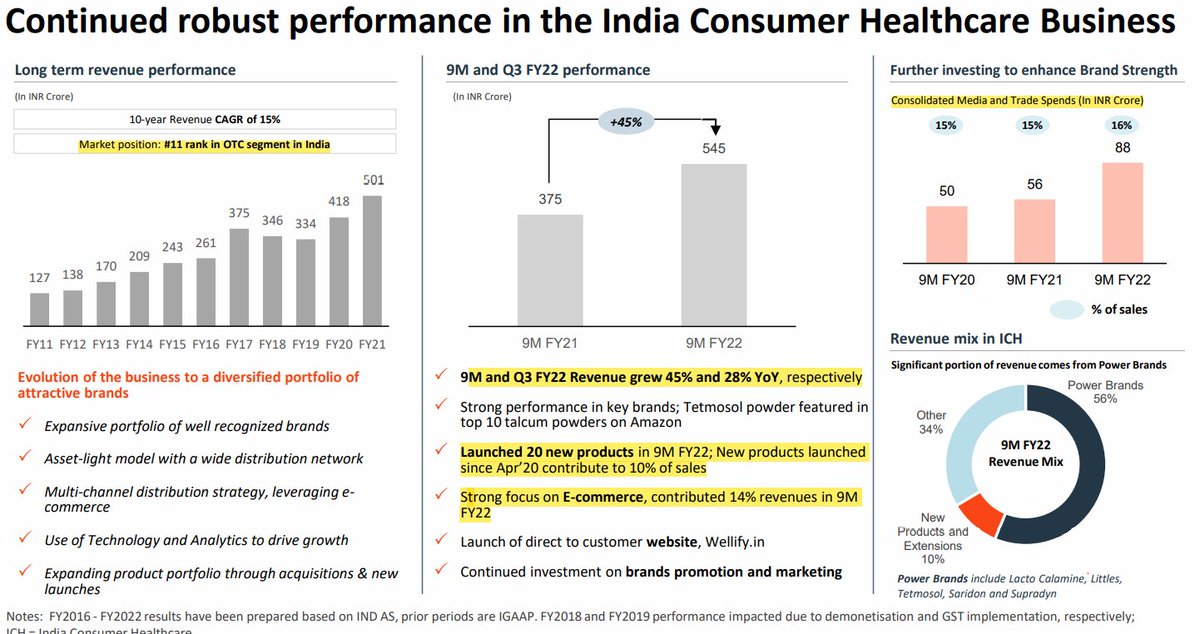

Now let's talk about the 3rd business segment that is - INDIAN CONSUMER HEALTHCARE

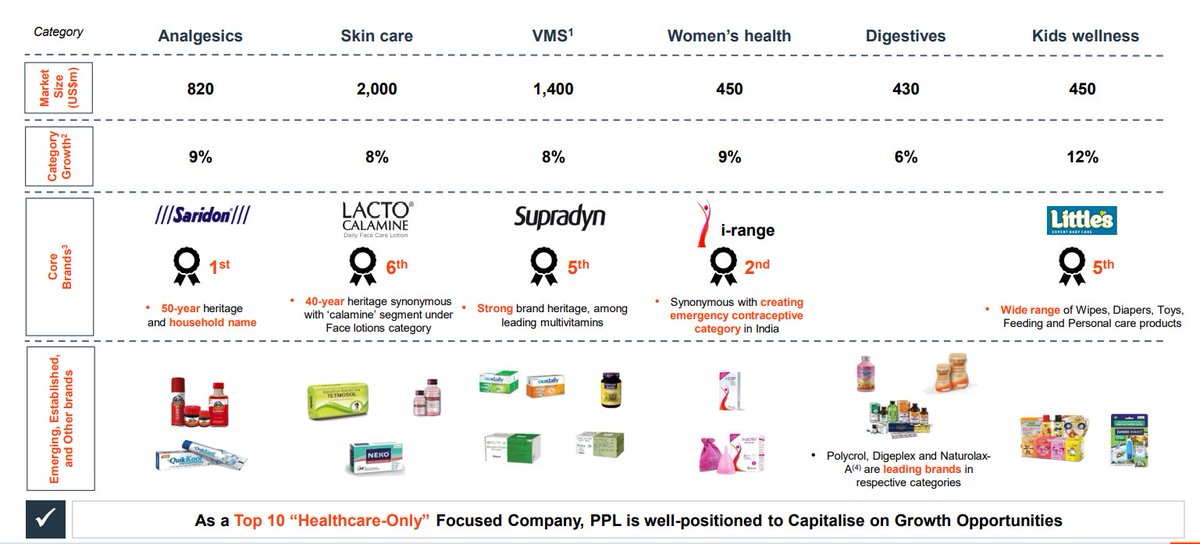

This business is just like your FMCG business, where you have a strong brand and strong brand recall.

You must have heard the name of Saridon & I-pill right?

This business is just like your FMCG business, where you have a strong brand and strong brand recall.

You must have heard the name of Saridon & I-pill right?

The revenue has increased from 127Cr in 2011 to 418Cr in 2020 and 545Cr in 9MFY22.

Currently forming only 12% of the overall revenues of Pharma business.

Currently forming only 12% of the overall revenues of Pharma business.

Over the years acquired many brands like I-pill in 2010 from CIPLA.

Little's in 2015 and digeplex in 2017.

Have a strong brand portfolio of 21 products like - Saridon, I-Pill, Lacto Calamine, Little's, Digeplex.

Little's in 2015 and digeplex in 2017.

Have a strong brand portfolio of 21 products like - Saridon, I-Pill, Lacto Calamine, Little's, Digeplex.

Have strong presence in segments like - Skin care, Anaglesics, Baby care, Women's health & Digestives.

300+Cr revenues comes from power brands and spending almost 16% of the revenues in advertisement.

300+Cr revenues comes from power brands and spending almost 16% of the revenues in advertisement.

Have presence in 200,000 chemist shops and 50,000 other general stores.

7000+ Pharmacy chains and in 22 E-Commerce platforms with 7 products in no. 1 category on Amazon.

Launched 41 New products and their own E-Commerce website - wellify.in

7000+ Pharmacy chains and in 22 E-Commerce platforms with 7 products in no. 1 category on Amazon.

Launched 41 New products and their own E-Commerce website - wellify.in

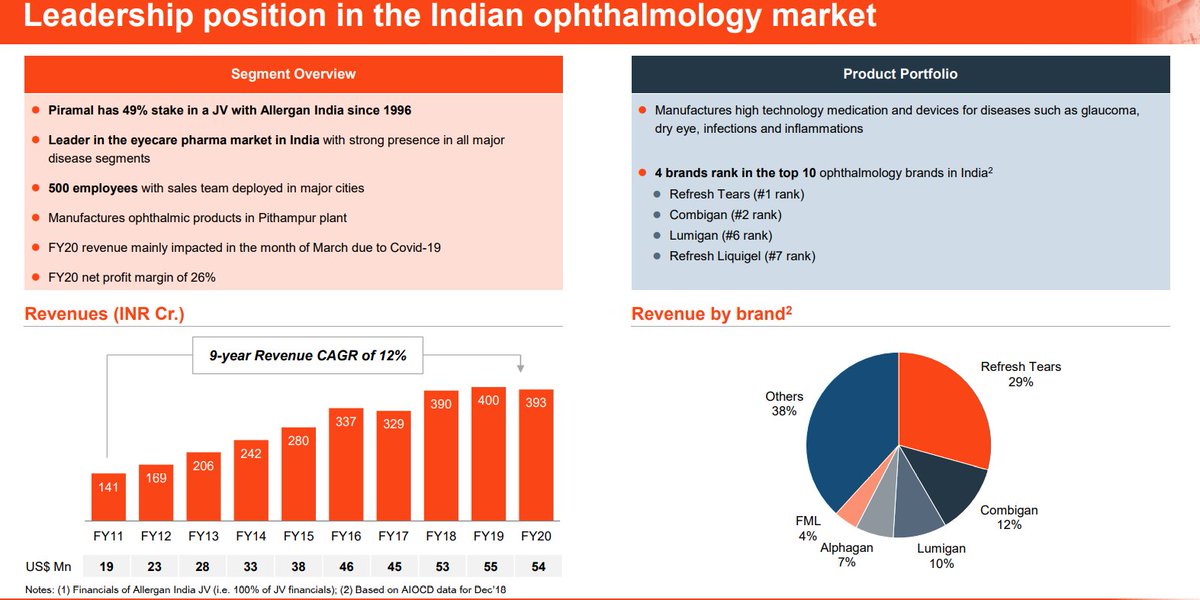

Now let's talk about the 4th division - JV WITH ALLERGAN

Partnered with ALLERGAN in 1996 and started a joint venture with 49% stake in it and a 50-50 profit sharing model.

Currently they're the market leader in Indian Ophthalmology market.

Partnered with ALLERGAN in 1996 and started a joint venture with 49% stake in it and a 50-50 profit sharing model.

Currently they're the market leader in Indian Ophthalmology market.

4 brands in top 10.

Revenue has increased from 141Cr in 2011 to 393Cr in 2020 at 12% CAGR.

Revenue has increased from 141Cr in 2011 to 393Cr in 2020 at 12% CAGR.

Now let's talk about the "Beast" the financial services business that nobody wants but maybe something is changing in that business.

Let's try to find out

Let's try to find out

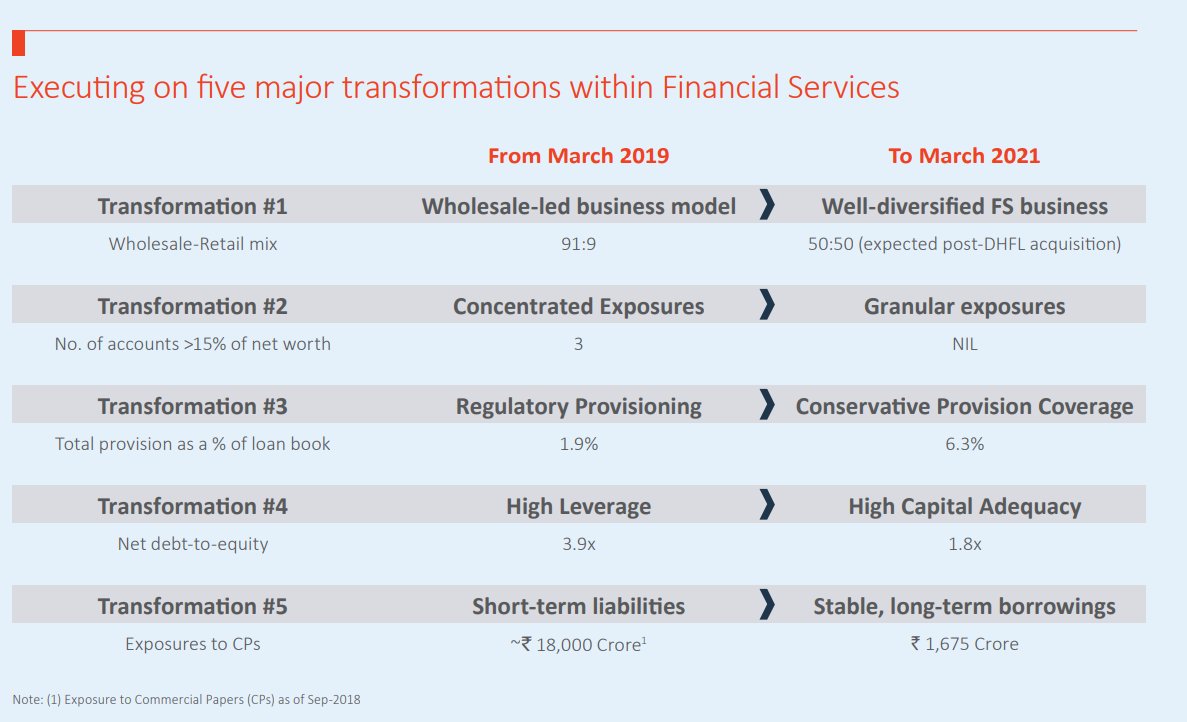

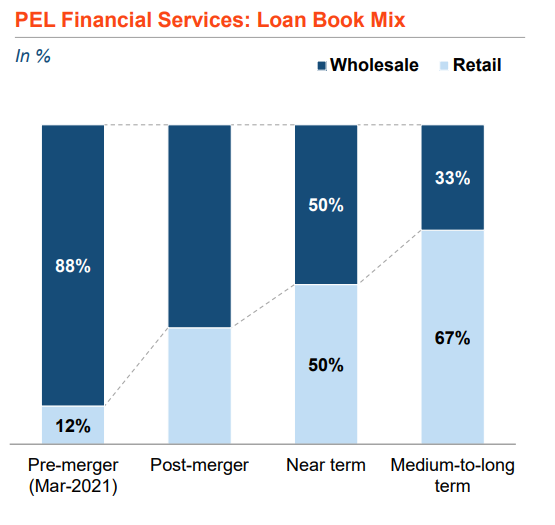

Their Financial services business is a total disaster with 90% of the total loan book being the Wholesale book ( meaning? - Developer loans)

And even that Wholesale book, more than 90% loans are given to real estate sector. ( A complete recipe for disaster)

And even that Wholesale book, more than 90% loans are given to real estate sector. ( A complete recipe for disaster)

After the whole DHFL, YES BANK & IL&FS fiasco, they realized they need to diversify.

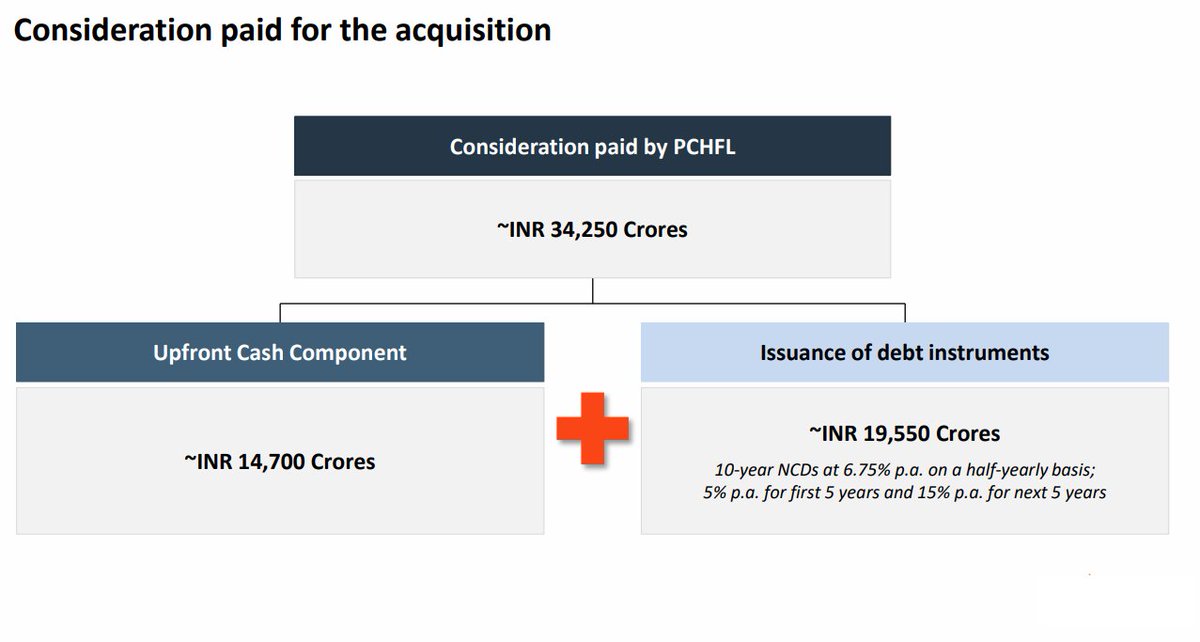

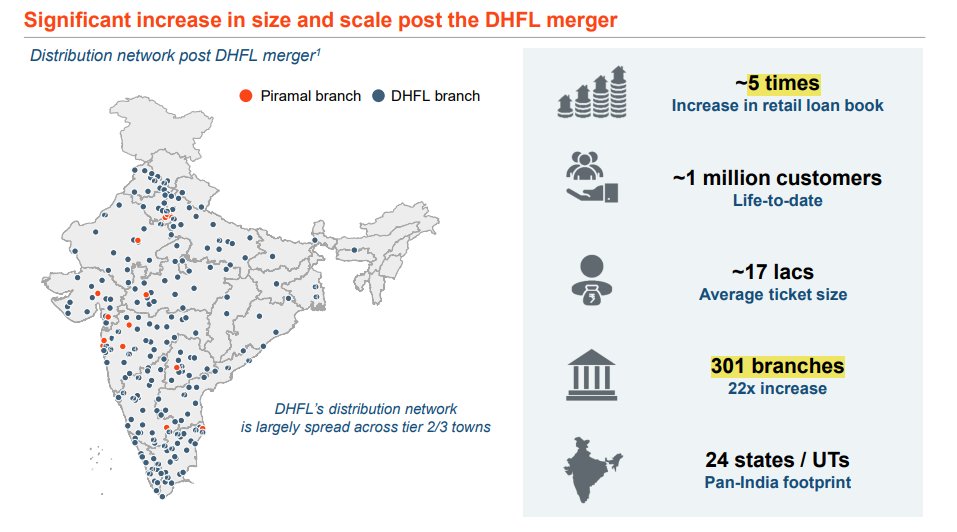

So they started expanding their Retail loan book and for doing so, they acquired DHFL for 34,250Cr

So they started expanding their Retail loan book and for doing so, they acquired DHFL for 34,250Cr

They paid 14,700Cr Upfront cash and rest 19,550 Crores will be paid by issuance of NCDs (Non convertible debentures) at a coupon rate of 6.75%

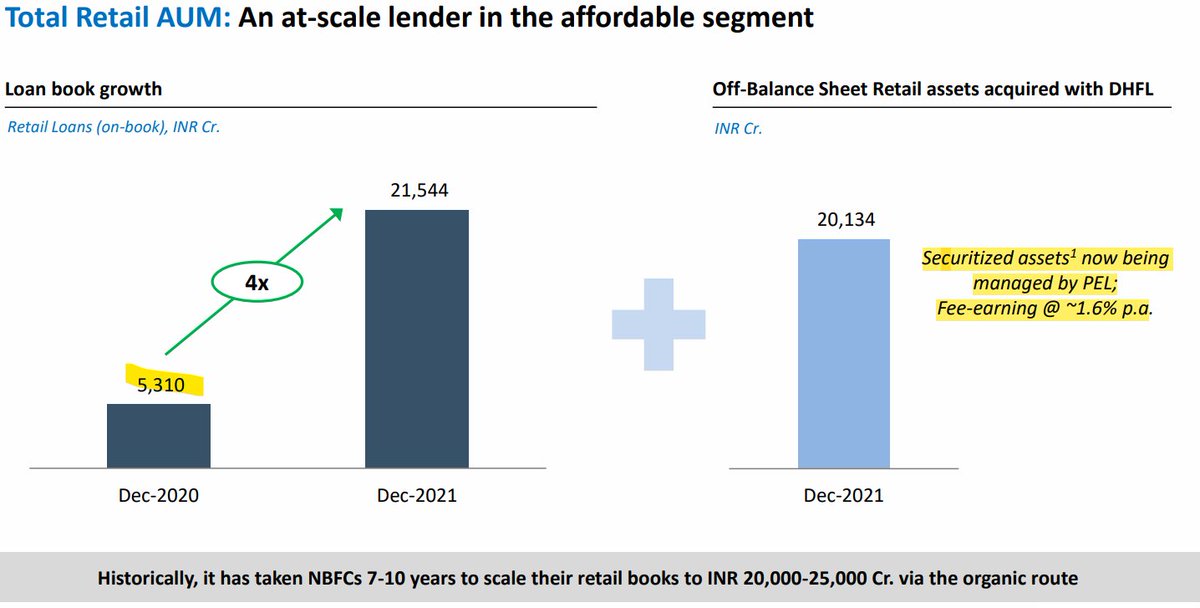

Their current loan book at around 60,640Cr with 36% being the retail including the DHFLs loan book.

Their current loan book at around 60,640Cr with 36% being the retail including the DHFLs loan book.

Before acquiring the book of DHFL, they had expanded their retail book to 5310Cr and the whole sale book came down to 39,365Cr by March 21.

They're acquired 21,544Cr book of DHFL and earn 1.6% FEE on 20,000Cr that was sold to other banks.

They're acquired 21,544Cr book of DHFL and earn 1.6% FEE on 20,000Cr that was sold to other banks.

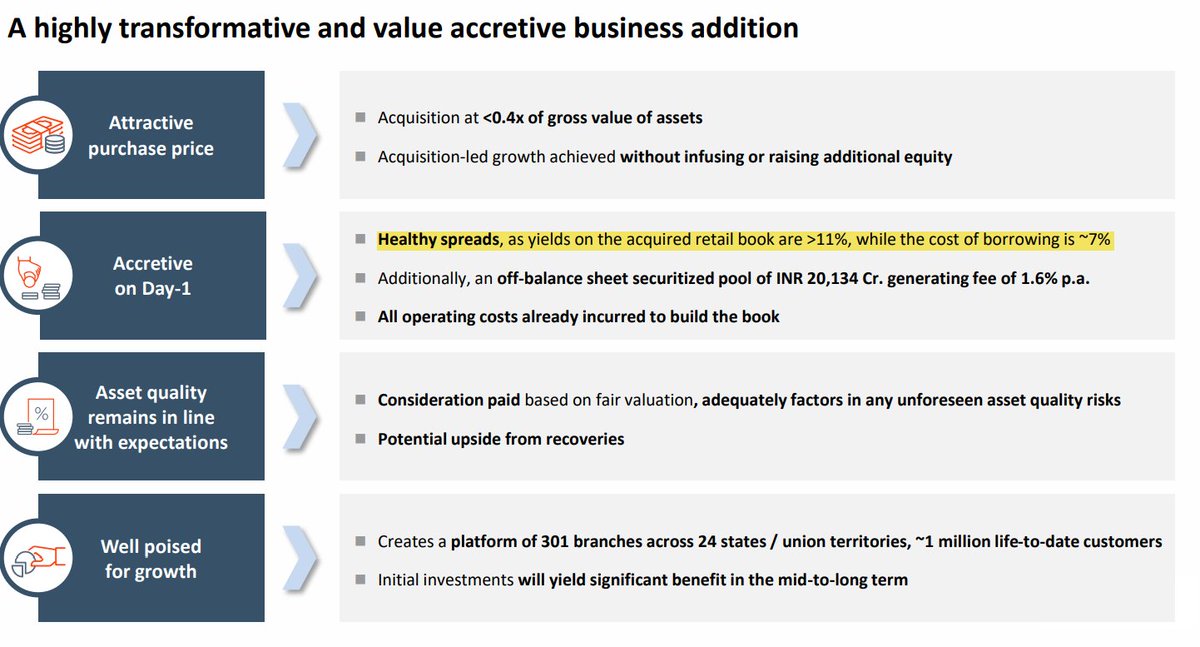

Acquiring DHFL helped them in expanding their retail presence by multifold.

No. of branches jumped 22x to 301

Customer base jumped to 1 Million

Presence in 24 States/UTs

No. of branches jumped 22x to 301

Customer base jumped to 1 Million

Presence in 24 States/UTs

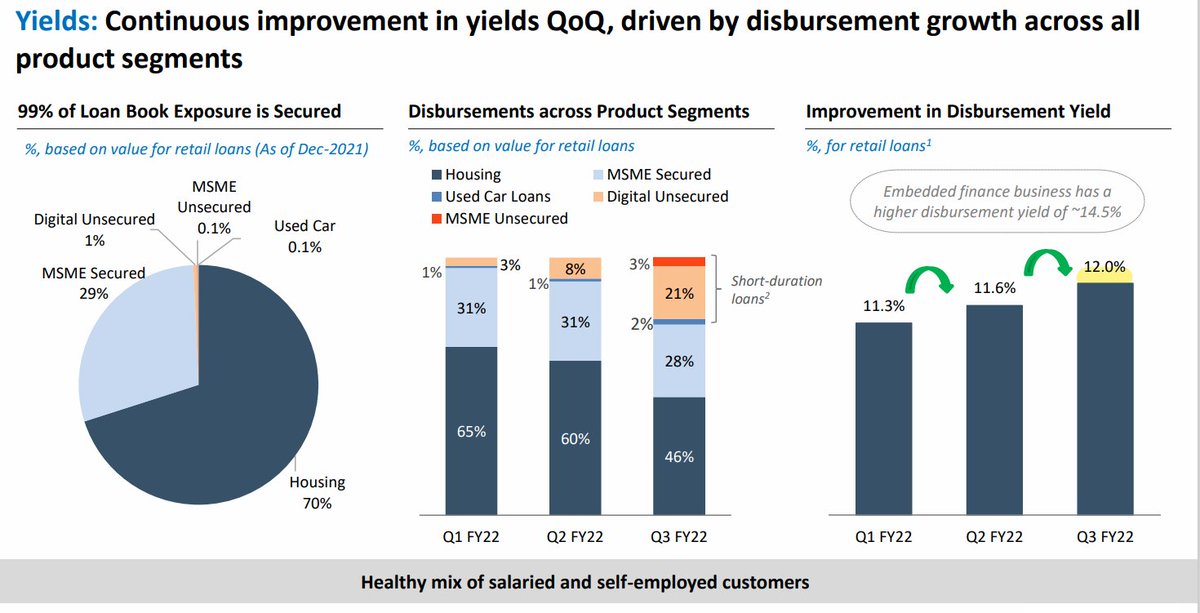

Yields on that book is around 11% while the cost of borrowing is around 7% for DHFL book.

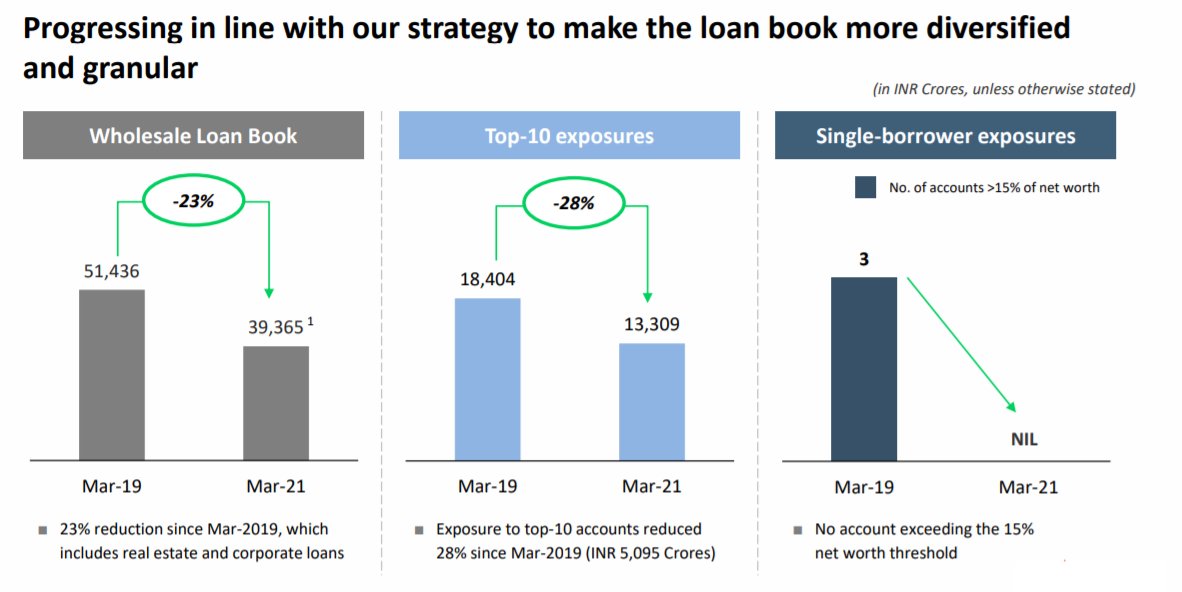

In their wholesale book the exposure to top 10 accounts is down to 12,494Cr from 18,404Cr in march 21.

No single borrower accounts for >10% of the net worth.

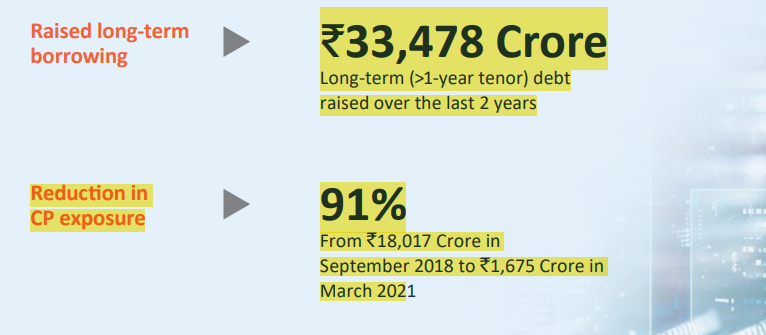

Commercial Papers exposure is down to 1,675Cr from 18,017Cr three years ago.

No single borrower accounts for >10% of the net worth.

Commercial Papers exposure is down to 1,675Cr from 18,017Cr three years ago.

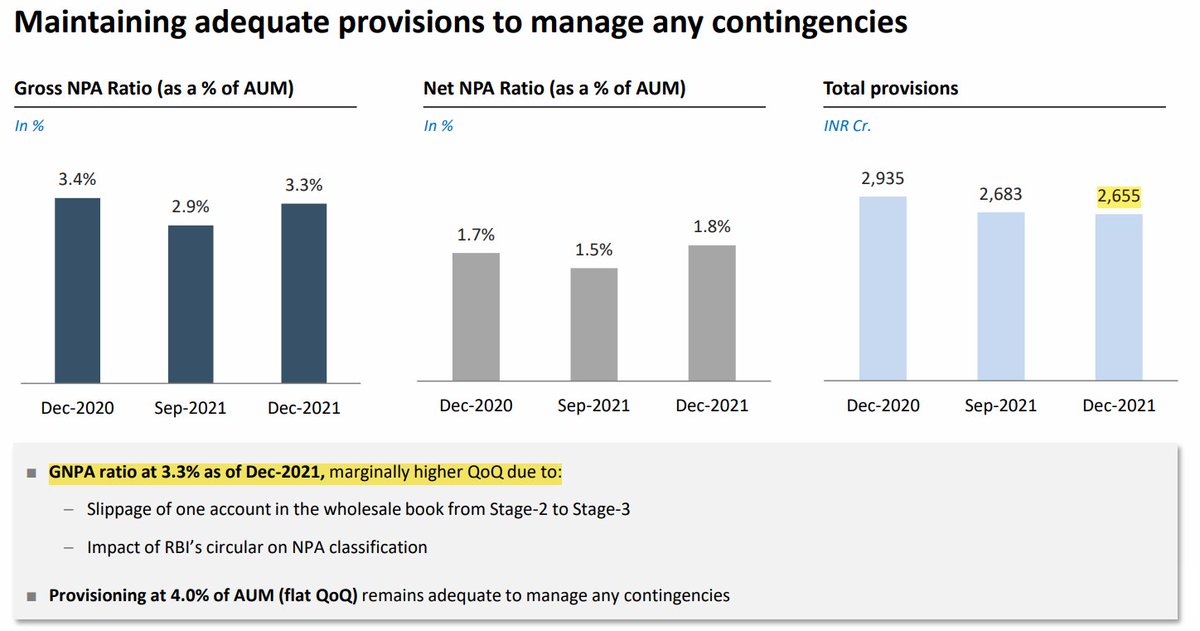

Asset Quality -

GNPA - 3.3%

NNPA - 1.8%

Total provisions - 2,655Cr (4% of the AUM)

CAR - 26%

Raised 33,000Cr debt and 18,000Cr equity.

GNPA - 3.3%

NNPA - 1.8%

Total provisions - 2,655Cr (4% of the AUM)

CAR - 26%

Raised 33,000Cr debt and 18,000Cr equity.

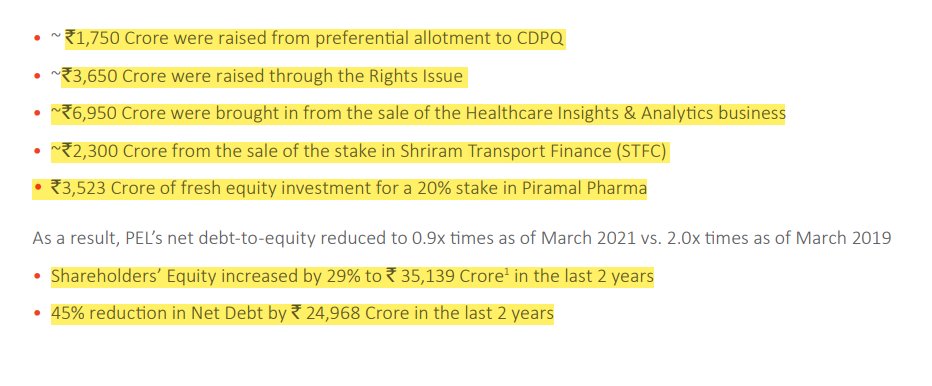

Have strategic investments in Shriram group -

20% Stake in Shriram Capital

10% Stake in Shriram City Union Finance

Did two rights issue in past 3 years.

Sold 20% stake in Pharma business to Carlyle.

Sold 20% stake in Shriram Transport Finance to build up the capital buffer.

20% Stake in Shriram Capital

10% Stake in Shriram City Union Finance

Did two rights issue in past 3 years.

Sold 20% stake in Pharma business to Carlyle.

Sold 20% stake in Shriram Transport Finance to build up the capital buffer.

If we take a look at the balance sheet, overall loan book is 60,640Cr partly funded by debt and partly funded by Equity.

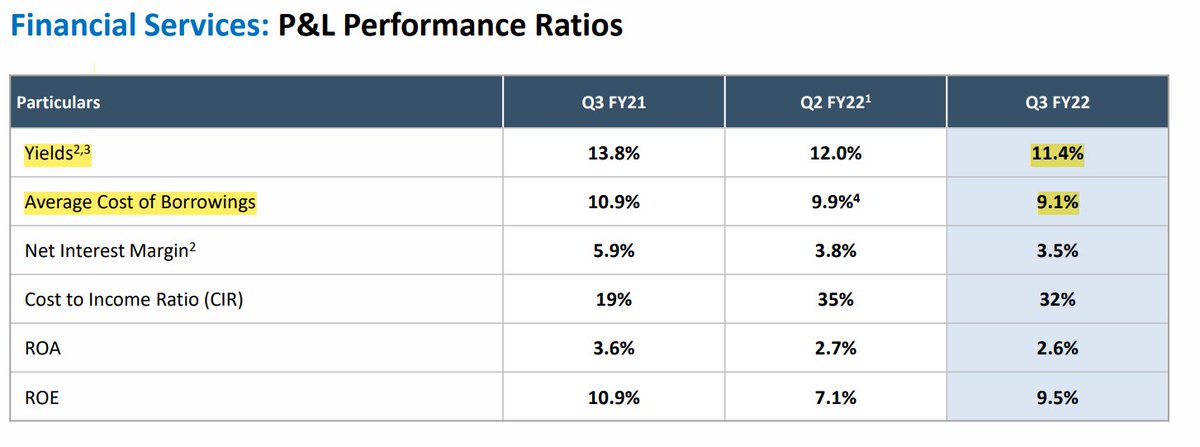

Return rations are not at all impressive with Cost of borrowing at 9.1% and Yields at 11.4% making the spread just 2.3%

(Canfin homes has cost of funds of around 6.5% and HDFC also have similar cost of funds)

(Canfin homes has cost of funds of around 6.5% and HDFC also have similar cost of funds)

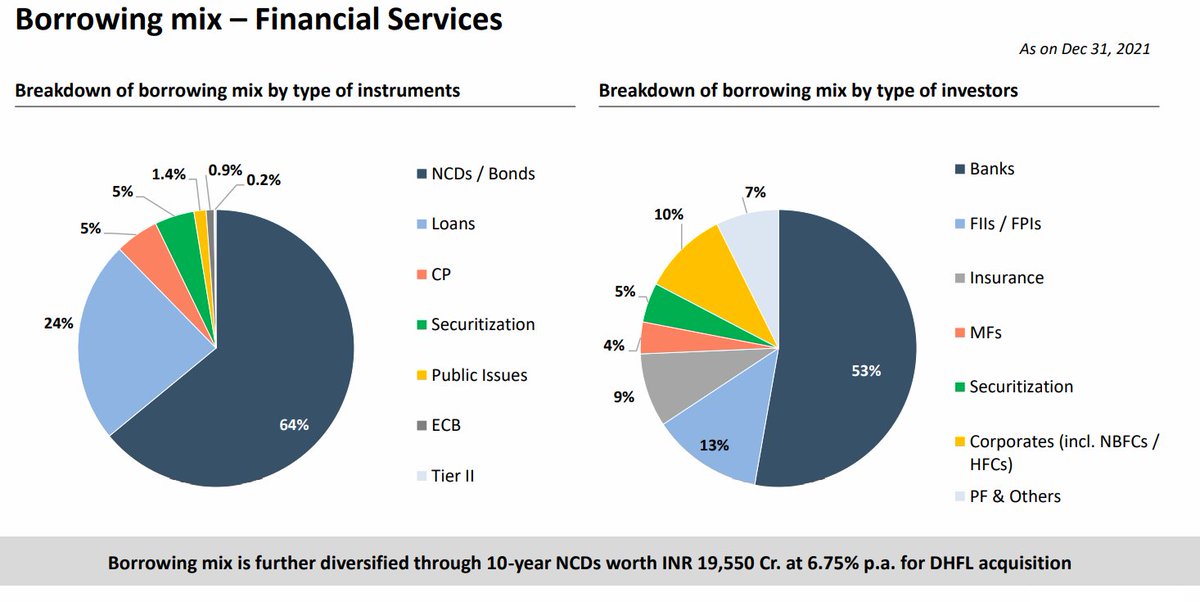

Borrowing mix improved after the IL&FS fiasco, now 64% of book is funded through NCDs and Bank Borrowings.

(Had very high dependence on Commercial paper which are very short term, decreased that dependence by 91/5 to 1,600Cr)

(Had very high dependence on Commercial paper which are very short term, decreased that dependence by 91/5 to 1,600Cr)

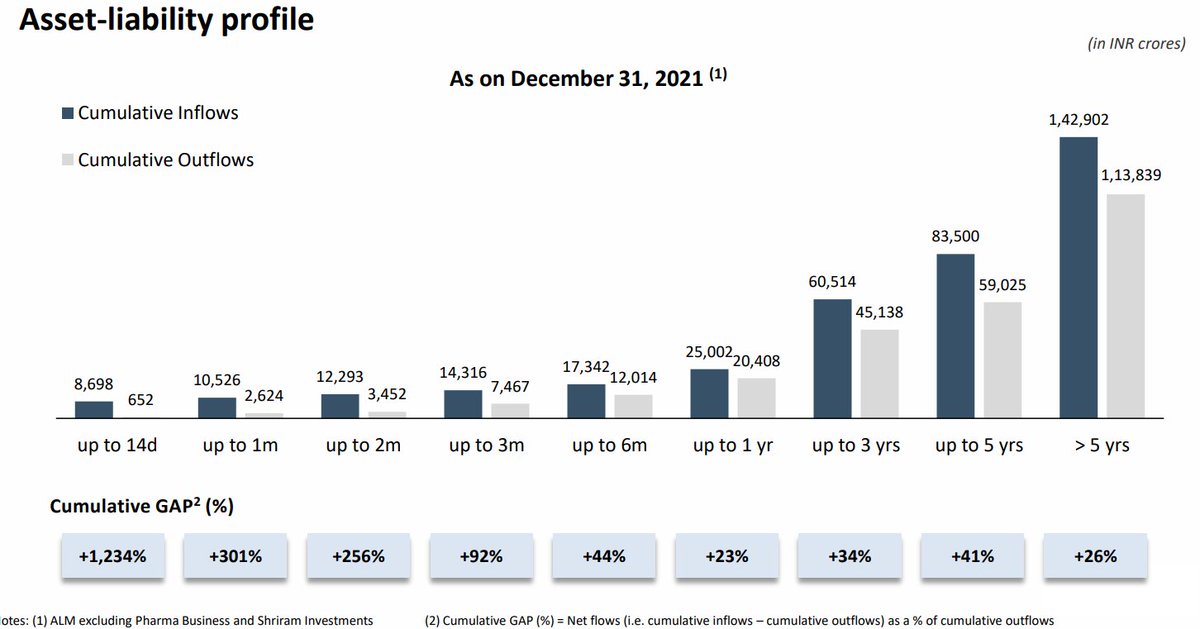

Asset Liability profile in a better positions, most of the inflows are for longer period as compare to outflows.

Future strategy? Focus on becoming a retail oriented NBFC.

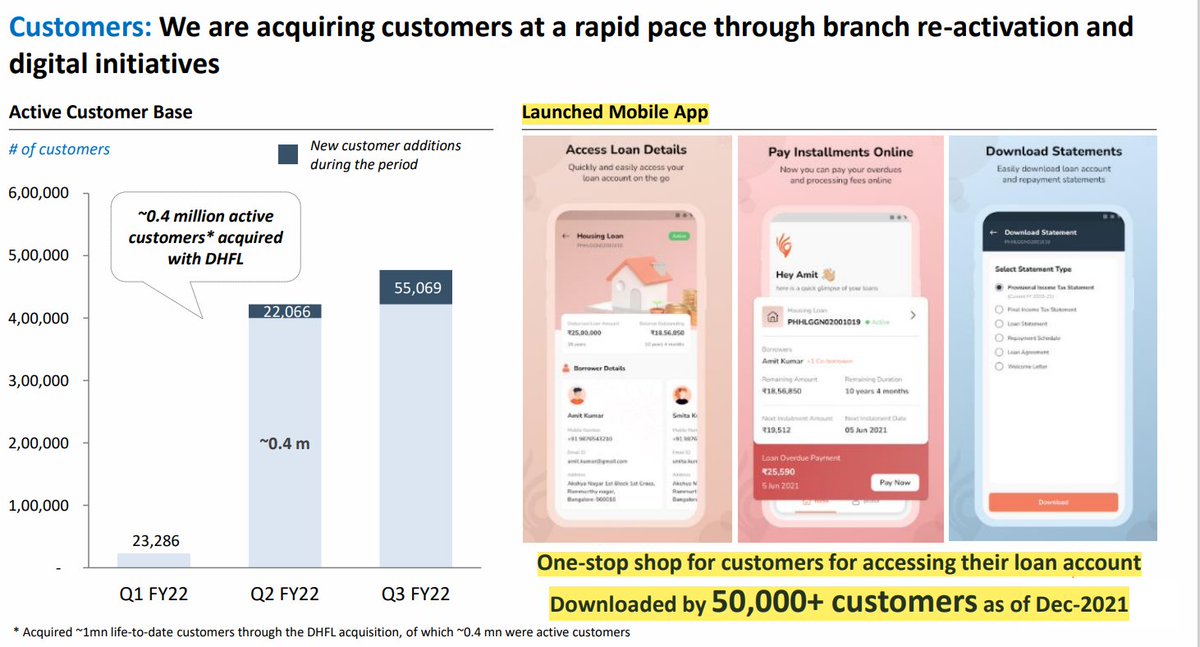

- Added 50K customers in Q3FY22

- Disbursements up 386% YoY to 739Cr

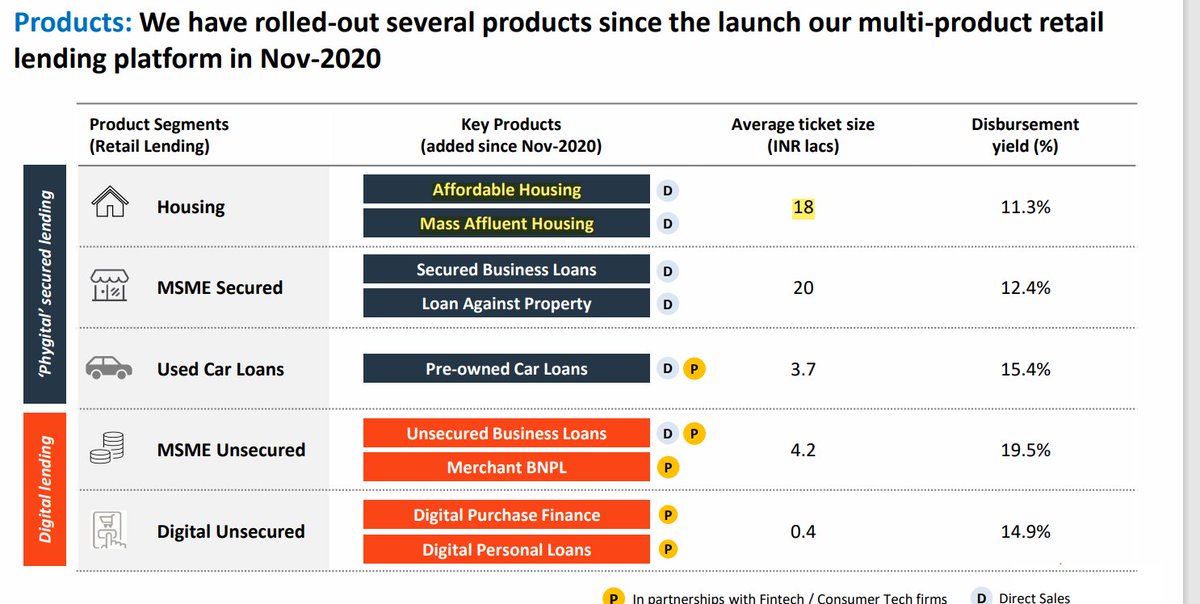

- Launched new products like Affordable housing ( 18 lakh ticket size, 11%+ yields)

- Added 50K customers in Q3FY22

- Disbursements up 386% YoY to 739Cr

- Launched new products like Affordable housing ( 18 lakh ticket size, 11%+ yields)

- Lunched Loan against property

- Used car loans

- Unsecured Business loans ( In partnership with Fintechs)

- BNPL

- Digital Personal Loans

- Launched it's own Mobile App

- Used car loans

- Unsecured Business loans ( In partnership with Fintechs)

- BNPL

- Digital Personal Loans

- Launched it's own Mobile App

- 99% loan book is secured

- Yields increasing to 12%

- With DHFL, cost of borrowing coming down

- Setup a Center of Excellence in Bangalore

- Hired 200 people on tech side

- Retained 3000 employees of DHLF

- Hired 2000+ more people taking the total count to 5000+

- Yields increasing to 12%

- With DHFL, cost of borrowing coming down

- Setup a Center of Excellence in Bangalore

- Hired 200 people on tech side

- Retained 3000 employees of DHLF

- Hired 2000+ more people taking the total count to 5000+

Current Transformation in a nutshell and future strategy.

My opinion - As the real estate cycle is turning up again, will help them to clean the mess in their Wholesale book

- Retail will take time to pick up and we currently don't know about how well they can handle the retail portfolio

- need to clean up the Mess in DHFL book

- Retail will take time to pick up and we currently don't know about how well they can handle the retail portfolio

- need to clean up the Mess in DHFL book

- Products like BNPL, Unsecured business loans can prove to be fatal.

Personally don't like the Financial services business at all but will all the transformation going on, don't mind owning it if i can get it cheap enough.

Personally don't like the Financial services business at all but will all the transformation going on, don't mind owning it if i can get it cheap enough.

Now let's come to the Overall Financials of Piramal Enterprises -

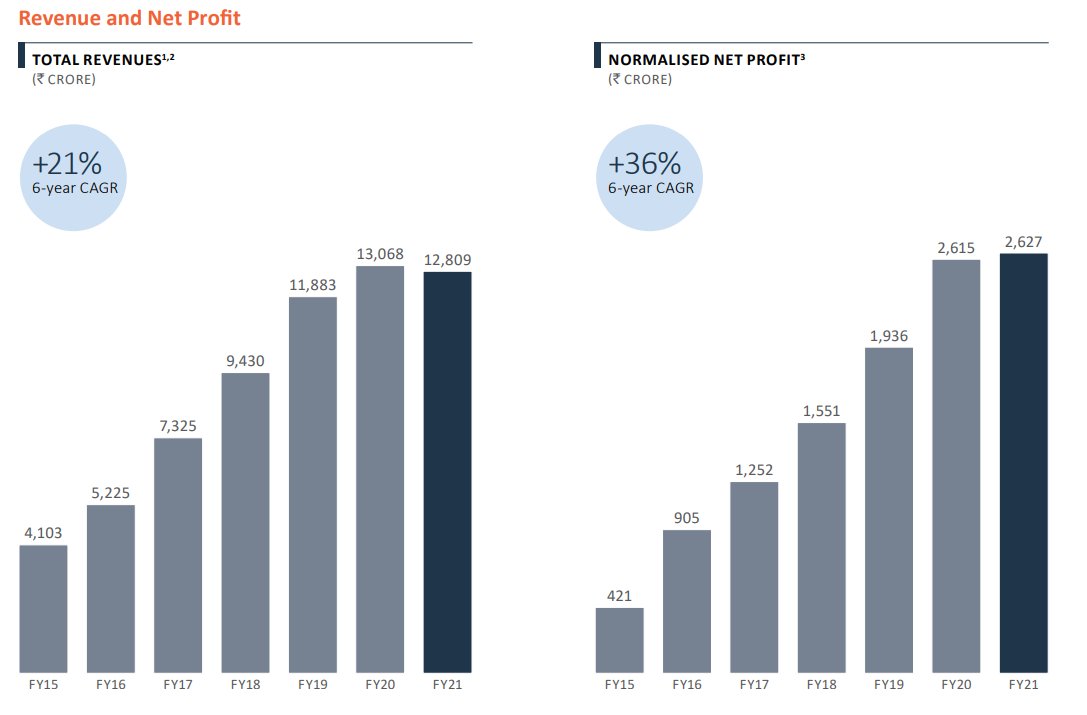

Last 30 year revenue CAGR has been 22% and Net Profit CAGR at 28%

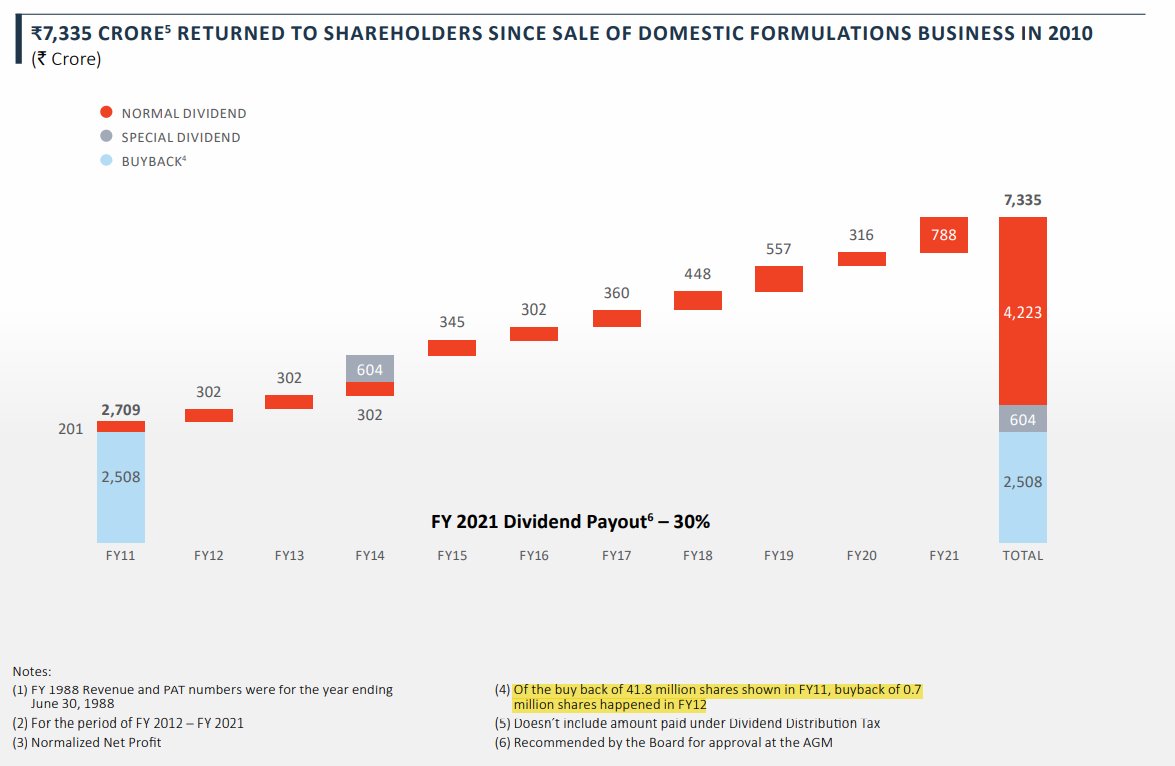

Has distributed 7,335Cr back to shareholders since the ABBOTT deal.

Last 30 year revenue CAGR has been 22% and Net Profit CAGR at 28%

Has distributed 7,335Cr back to shareholders since the ABBOTT deal.

Equity has increased from 27000Cr in 2019 to 35,000Cr in March 21

Debt has come down from 55,122Cr in 2019 to 30,159Cr

- LAST 5 years Revenue CAGR - 21%

- Last 5 year Profit CAGR - 36%

Debt has come down from 55,122Cr in 2019 to 30,159Cr

- LAST 5 years Revenue CAGR - 21%

- Last 5 year Profit CAGR - 36%

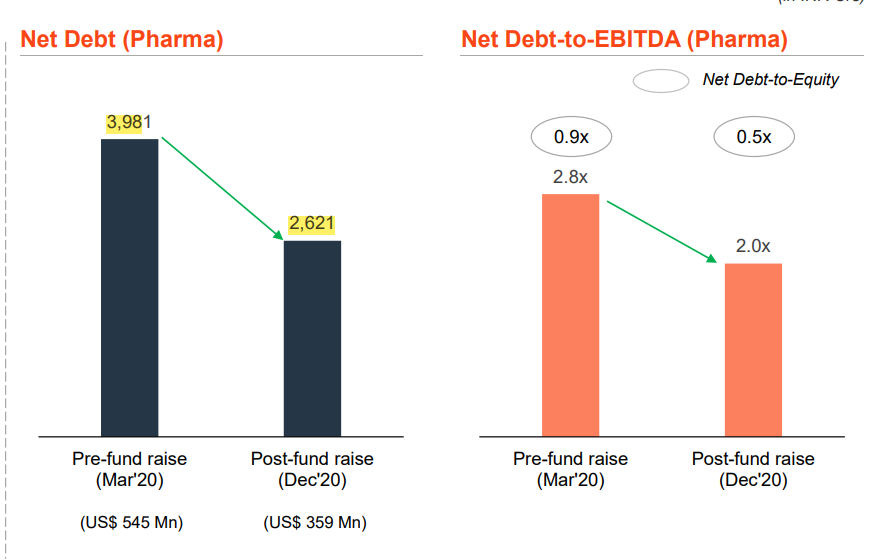

Post the fund raise and 20% Stake sale to Carlyle, Pharma segment debt has come down to 2,621Cr

- Net debt to equity - 0.5x

- Net debt to equity - 0.5x

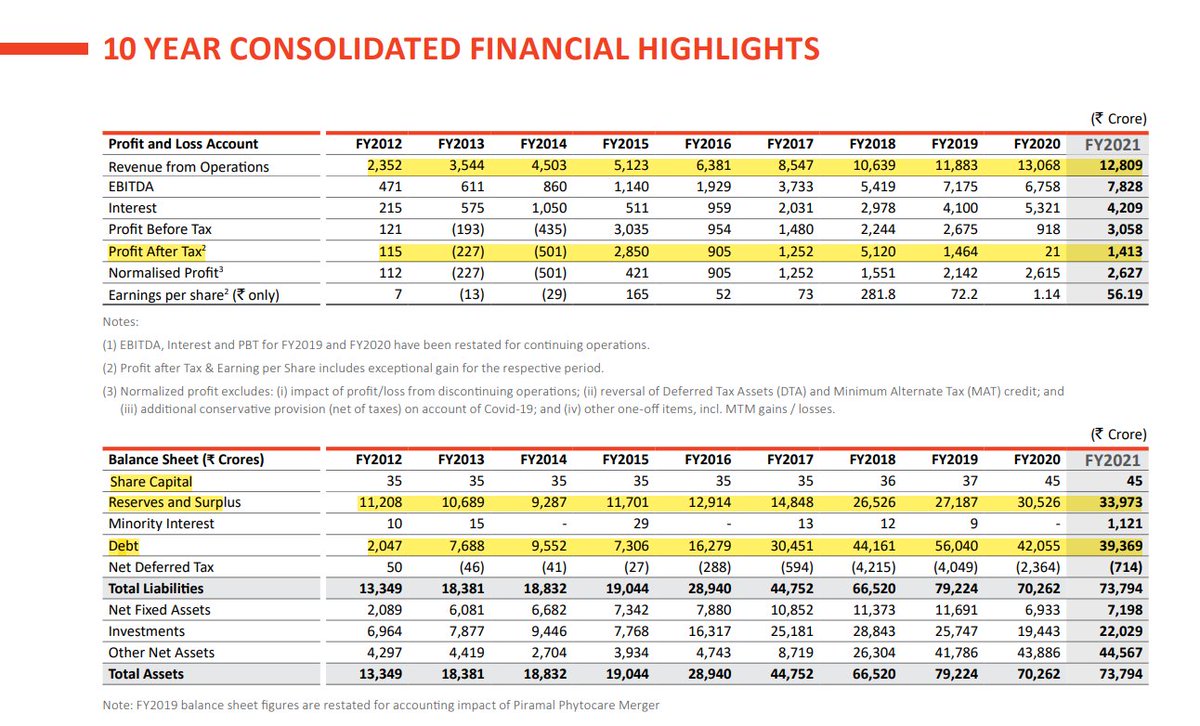

10 Year Consolidated Financial Highlights -

- Revenues increased from 2,352Cr in 2012 - 12,809r in 2021

- Net Profit from 115Cr to 1,413Cr

- Debt from 2,047Cr to 39,973

- Equity from 11,208Cr to 33,973 Cr

- Revenues increased from 2,352Cr in 2012 - 12,809r in 2021

- Net Profit from 115Cr to 1,413Cr

- Debt from 2,047Cr to 39,973

- Equity from 11,208Cr to 33,973 Cr

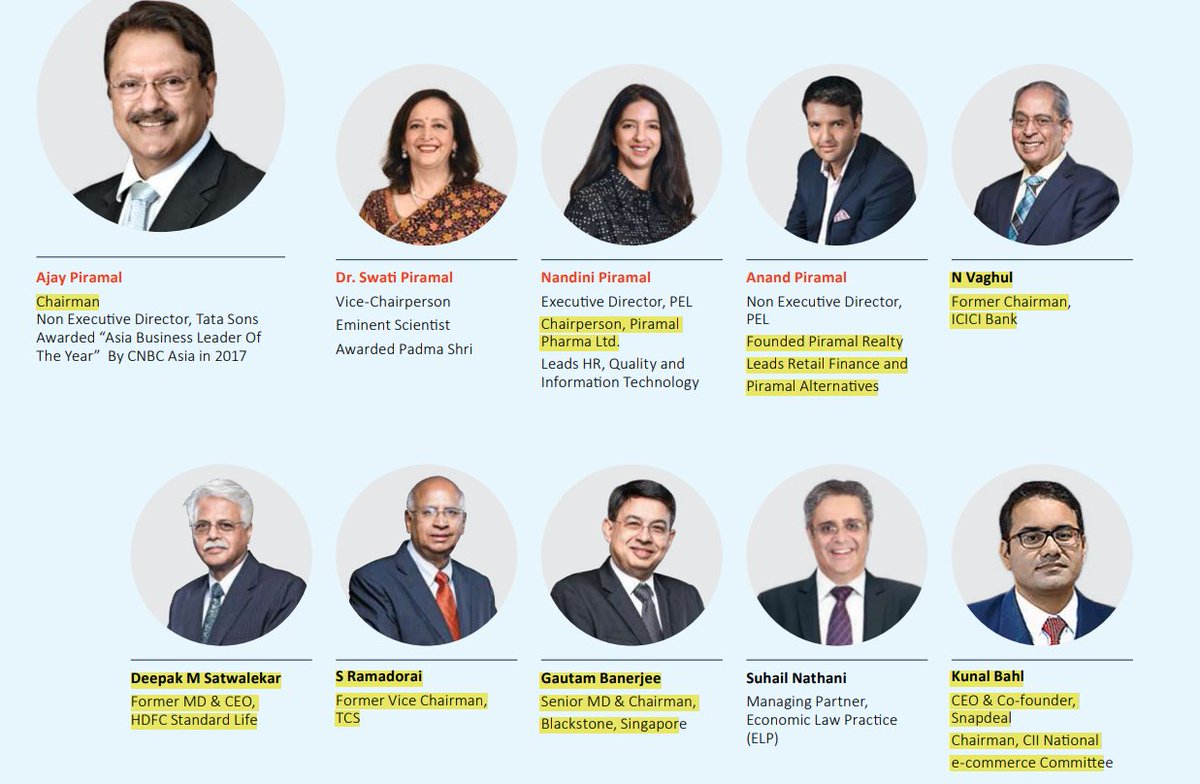

BOARD AND MANAGEMENT TEAM -

It's a family run business with Ajay Piramal being the Chairman of the group. He's also a Non executive director in Tata Sons

His wife - Dr. Swati Piramal is a scientist and Vice chairperson.

It's a family run business with Ajay Piramal being the Chairman of the group. He's also a Non executive director in Tata Sons

His wife - Dr. Swati Piramal is a scientist and Vice chairperson.

Pharma business is run by - Nandini Piramal

Piramal Realty - Anand Piramal

N vaghul - Former Chairman of ICICI

Deepak M Satwalekar - Former MD & CEO OF HDFC LIFE

Piramal Realty - Anand Piramal

N vaghul - Former Chairman of ICICI

Deepak M Satwalekar - Former MD & CEO OF HDFC LIFE

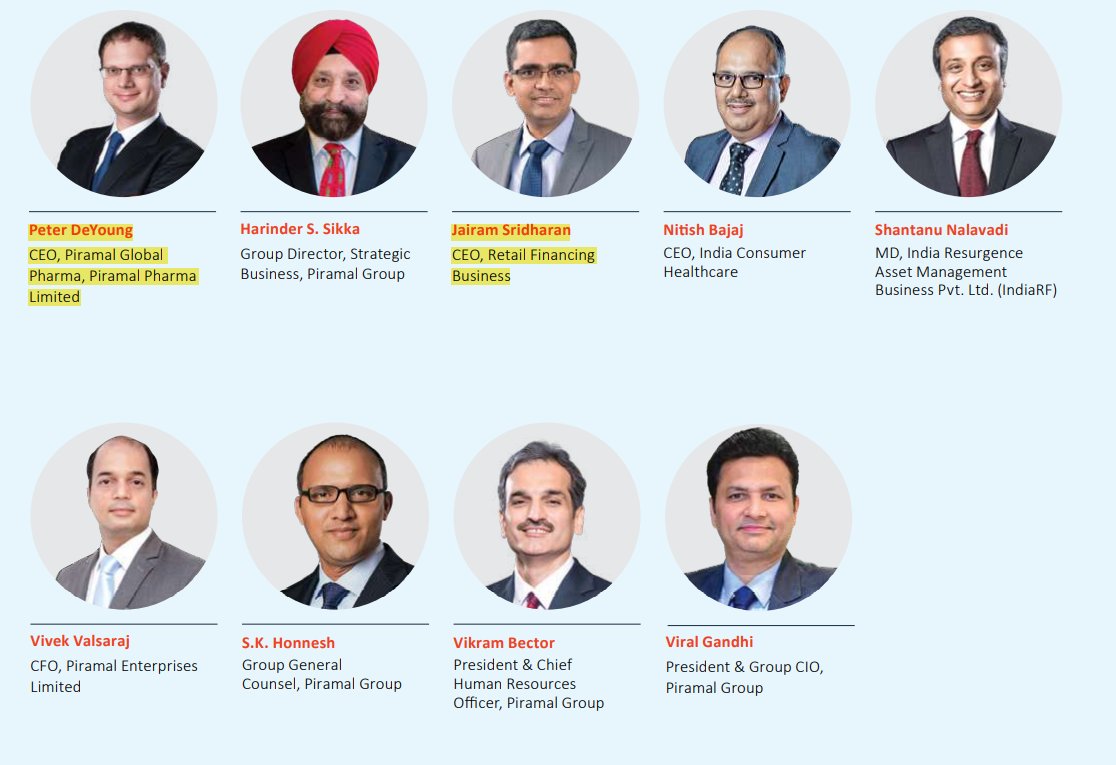

MANAGEMENT TEAM -

Peter DeYoung - CEO of Global division

Jairam Sridharan - For head of retail Financing in Axis bank

Peter DeYoung - CEO of Global division

Jairam Sridharan - For head of retail Financing in Axis bank

Thesis - De-merger of the Beauty from the beast ( Pharma and Financial services)

- Strong regulatory track record of pharma division

- Turnaround in Financial Services business

- Reasonable valuations

- Good corporate governance ( Investor friendly management)

- Strong regulatory track record of pharma division

- Turnaround in Financial Services business

- Reasonable valuations

- Good corporate governance ( Investor friendly management)

Anti Thesis - De-merger being delayed

- Regulatory risk in pharma (USFDA)

- Financial services business is shit

- High debt in Pharma

- Lots of mergers and acquisitions ( changes of disworsification)

- Chance of getting the company sold ( Just like 2010)

- Regulatory risk in pharma (USFDA)

- Financial services business is shit

- High debt in Pharma

- Lots of mergers and acquisitions ( changes of disworsification)

- Chance of getting the company sold ( Just like 2010)

If you enjoyed the thread and learned something

please like, share and Re-tweet the first thread.

@shubhfin @suru27 @ishmohit1 @soicfinance

@itsTarH @sahil_vi @badola_arjun @Arthavruksha12

please like, share and Re-tweet the first thread.

@shubhfin @suru27 @ishmohit1 @soicfinance

@itsTarH @sahil_vi @badola_arjun @Arthavruksha12

Loading suggestions...