ZOMATO - An Analysis

Lajawaab ya Beswad??? 🧐

Should you place an order for Zomato?

- A detailed 🧵 (1/n)

#sharemarket #Zomato #investing

Lajawaab ya Beswad??? 🧐

Should you place an order for Zomato?

- A detailed 🧵 (1/n)

#sharemarket #Zomato #investing

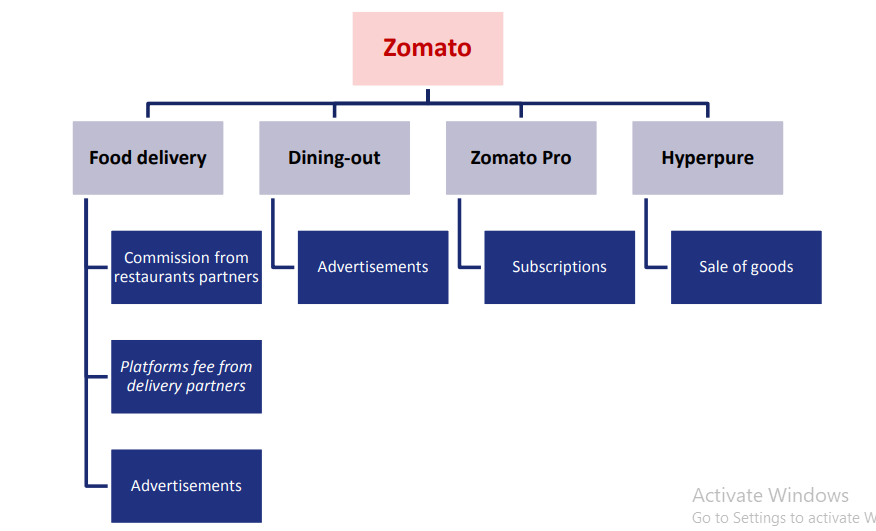

Business model of #Zomato:

Zomato is a food aggregator, it basically provides food delivery services to restaurants. It’s major sources of revenue are: (2)

Zomato is a food aggregator, it basically provides food delivery services to restaurants. It’s major sources of revenue are: (2)

Transaction Fees:

Zomato charges restaurants a percentage of the total order value, and most of the revenue of the company comes through transaction fees.

(3)

Zomato charges restaurants a percentage of the total order value, and most of the revenue of the company comes through transaction fees.

(3)

Advertising:

Restaurants that list on Zomato have to pay a fee to get listed, but some restaurants to get additional visibility to advertise themselves, for that they pay advertisement fees.

(4)

Restaurants that list on Zomato have to pay a fee to get listed, but some restaurants to get additional visibility to advertise themselves, for that they pay advertisement fees.

(4)

Another source of revenue is Subscriptions, Zomato offers a subscription service through Zomato Pro (previously known as Zomato gold ) under which consumers get discounts on food and faster deliveries.

(5)

(5)

The company discontinued Zomato gold after a lot of backlash from the restaurants, now it provides subscriptions through Zomato pro.

(6)

(6)

Most restaurants are not happy with the subscription plan & have abstained from partnering for these subscriptions and due to that, the sale of subscriptions is decreasing as according to Zomato’s RHP, revenue from the sale of subscriptions fell by almost 34% in FY21. (7)

Next is HyperPure, Zomato’s B2B product that supplies vegetables and other products to restaurants. While direct measures of revenues from HyperPure are difficult to come by, the revenues that the company shows under traded goods (which include HyperPure revenues)

(8)

(8)

Suggests that it accounts for about 10% of the total revenues. Although hyperpure’s topline has been growing consistently, the unit economics are not great and it still has a long way to go to achieve profitability.

(9)

(9)

Zomato has grown at exponential rates for much of the last decade, with a surge in the number of cities that it serves in India, especially in the last few years, from 38 in 2017 to 63 in 2018 to more than 500 in 2021, extending its reach into smaller urban settings.

(10)

(10)

Zomato does not have a disruptive business model as such, the company just delivers food from restaurants to the consumer, and due to that, the customer loyalty in the industry is almost negligible, as one can shift from Zomato to Swiggy just for a discount of Rs.10.

(11)

(11)

Although it is easy for customers to shift to other platforms, still we have two leading players in India, Zomato and Swiggy, one advantage that they have is of the network effect.

(12)

(12)

Say you want Biryani from your favourite restaurant and that is listed only on Zomato, then you would have to use the platform. With having more restaurants and consumers these platforms create network effect.

(13)

(13)

Profitability or Top line growth? A tough choice to make!

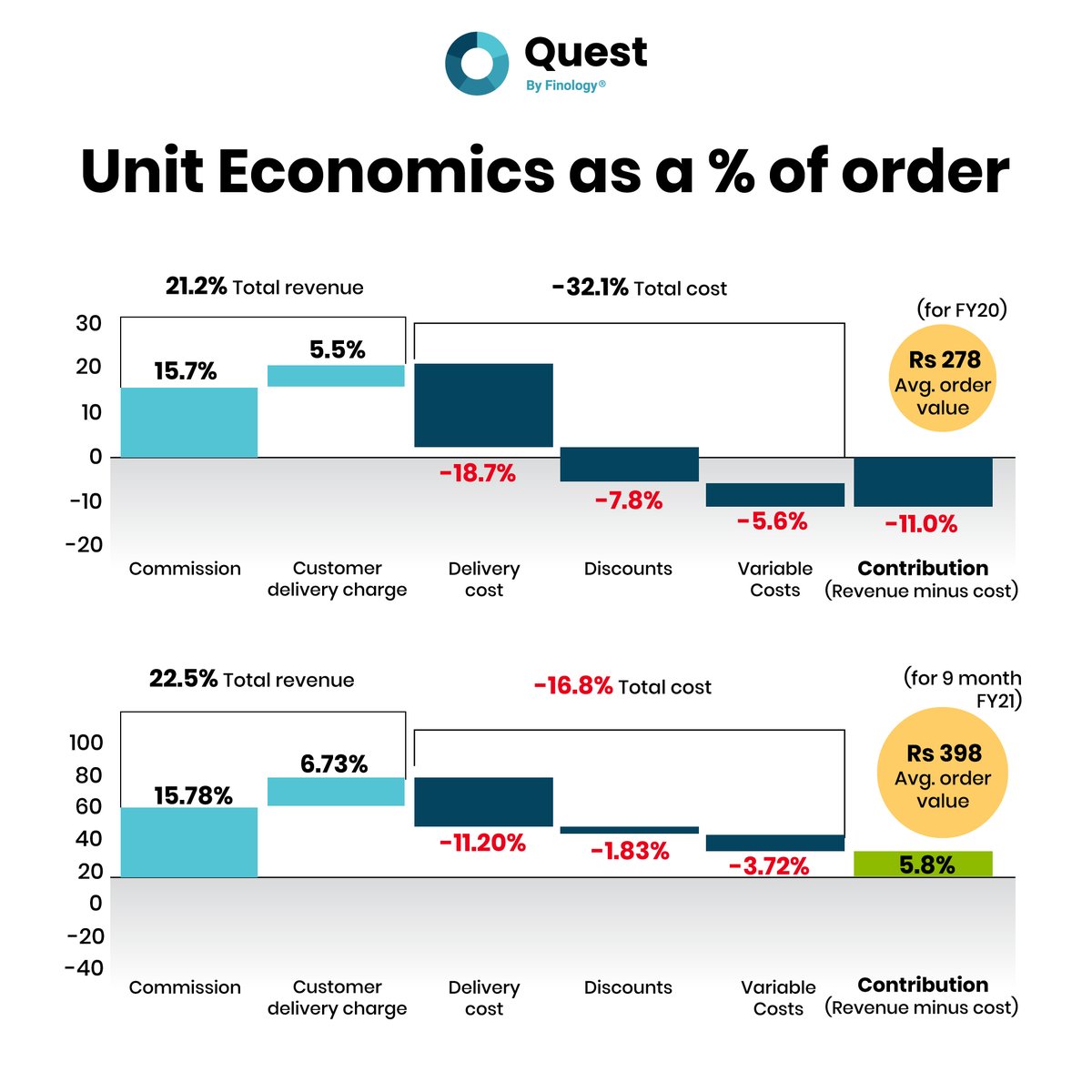

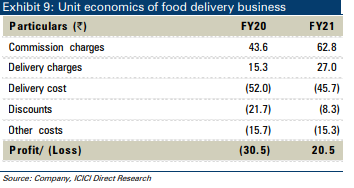

When it comes to the blooming start-up's investors are often concerned about the profitability of the company and in the case of food aggregators the metric that reflects the profitability is the unit economics.

(14)

When it comes to the blooming start-up's investors are often concerned about the profitability of the company and in the case of food aggregators the metric that reflects the profitability is the unit economics.

(14)

Unit economics is the profit a company earns per order. Let’s see how it is calculated for Zomato and how it measures its profitability.

Unit economics would be total inflows per order - total outflows per order.

(15)

Unit economics would be total inflows per order - total outflows per order.

(15)

Total inflows include the commission & other fees that Zomato charges from restaurants + the delivery charge. Total outflows include delivery costs, discounts and other variable costs. The difference of both would tell us how much money Zomato makes on each order. (16)

While most startups are focused on top-line growth, Zomato has understood the importance of profitability & it seems as if it is trying to improve its unit economics as in FY20 company was losing around Rs.30 per order, but in FY21 comp is making around Rs.20 per order.

(17)

(17)

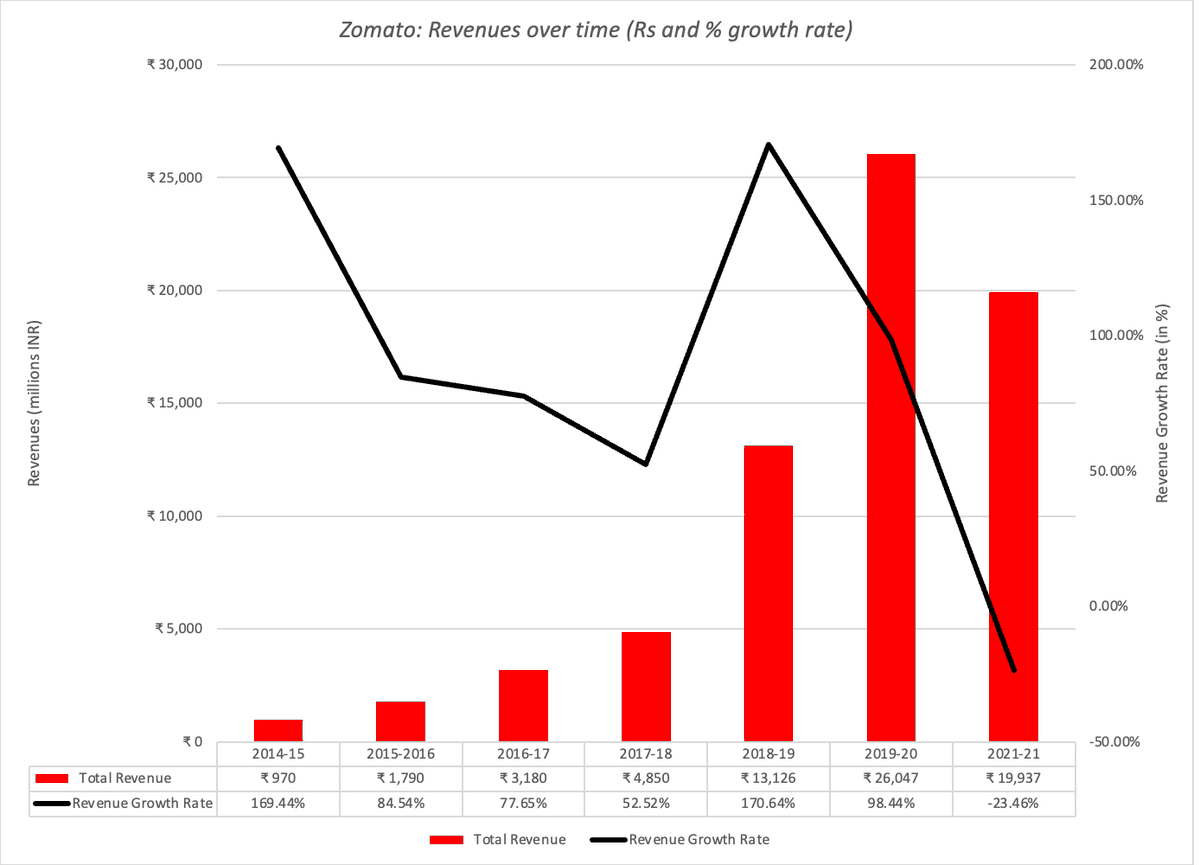

But positive unit economics for Zomato has come at the cost of its revenue. Let’s understand how, to increase its profits per order it reduced the discounts and increased the delivery charges which had a negative impact on the Zomato topline.

(18)

(18)

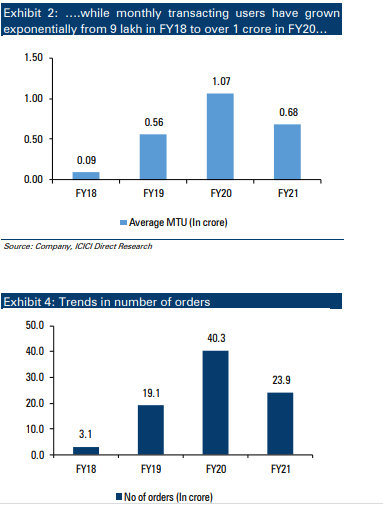

As we can see, both the number of transactions and orders on the platform has decreased. (19)

(20)

As can be seen, positive unit economics have come at a cost of reduced topline as its revenue has declined in 2021.

(21)

(21)

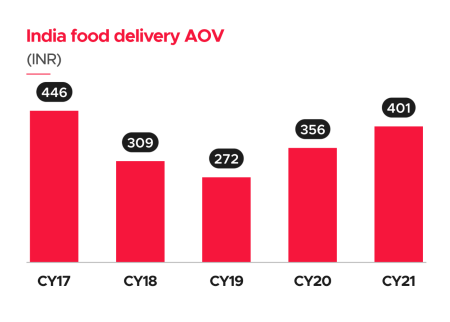

Average order value:

Cost of delivering an order for Zomato is more or less same, but it earns more on an order which is worth Rs. 500 than on an order of Rs. 100, & therefore higher AOV means more pfts for comp, AOV of zomato has risen drastically over the last few yrs.

(22)

Cost of delivering an order for Zomato is more or less same, but it earns more on an order which is worth Rs. 500 than on an order of Rs. 100, & therefore higher AOV means more pfts for comp, AOV of zomato has risen drastically over the last few yrs.

(22)

This rise in the AOV, may or may not be sustainable for Zomato, as the AOV has risen mainly because of two reasons.... (23)

- Due to the pandemic more high-end restaurants, which had a pricey menu also came on the app due to dine-in restrictions.

- People who generally order from Zomato are bachelors and people living away from home, now these people have shifted to their hometowns.

(24)

- People who generally order from Zomato are bachelors and people living away from home, now these people have shifted to their hometowns.

(24)

And now most people ordering from platform are families & due to that AOV has increased.

Indian food Industry is quite underpenetrated, as in India around 8%-9% of total food consumption is through restaurants, while in most nations like China and US it is around 45%.

(25)

Indian food Industry is quite underpenetrated, as in India around 8%-9% of total food consumption is through restaurants, while in most nations like China and US it is around 45%.

(25)

This implies #Zomato has a huge market to cater to. (26)

Zomato could face tough competition from Amazon, which has entered the industry and it seems that it is all set to disrupt the Indian food delivery market.

(27)

(27)

As it is currently charging restaurants quite less when compared with Zomato and Swiggy, they take around 20% - 25% of the gross order value, while Amazon plans to take around 10% of the restaurant revenues.

(28)

(28)

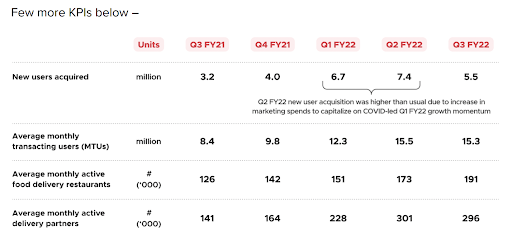

Also, the opening up of restaurants and the resumption of dining in services is affecting the food delivery business, as in the recent quarter the company witnessed a decline in the new users and monthly transacting users.

(29)

(29)

Even though the company boasted for huge orders on the new year’s night.

While #Zomato has a huge market to capture and potential to grow, there are some challenges it has to overcome in order to rule the Indian food delivery market.

(30)

While #Zomato has a huge market to capture and potential to grow, there are some challenges it has to overcome in order to rule the Indian food delivery market.

(30)

Loading suggestions...