How to evaluate risk of corporate loans blowing up P&L for a bank.

Example of IDFC 🏦 from my portfolio (feel free to apply it to a lender of your choice)

A step by step guide. Must read for ANY person invested in lenders. Please retweet if you find it useful. :)

🧵🧵🧵⤵️

Example of IDFC 🏦 from my portfolio (feel free to apply it to a lender of your choice)

A step by step guide. Must read for ANY person invested in lenders. Please retweet if you find it useful. :)

🧵🧵🧵⤵️

Outline:

Objective

Steps

Conclusion

Objective

Steps

Conclusion

Objective

First of all, why are we doing all this?

To understand what risk exists to our Bank's P&L & balance sheet blowing up.

First of all, why are we doing all this?

To understand what risk exists to our Bank's P&L & balance sheet blowing up.

Step 0:

The main source of all the data is zaubacorp.com

This contains all "charges" created by all companies by lender of our choice.

The main source of all the data is zaubacorp.com

This contains all "charges" created by all companies by lender of our choice.

Legal definition of a charge:

legalserviceindia.com

A charge means an interest or right which a lender or creditor obtains in the property of the company by way of security that the company will pay back the debt.

legalserviceindia.com

A charge means an interest or right which a lender or creditor obtains in the property of the company by way of security that the company will pay back the debt.

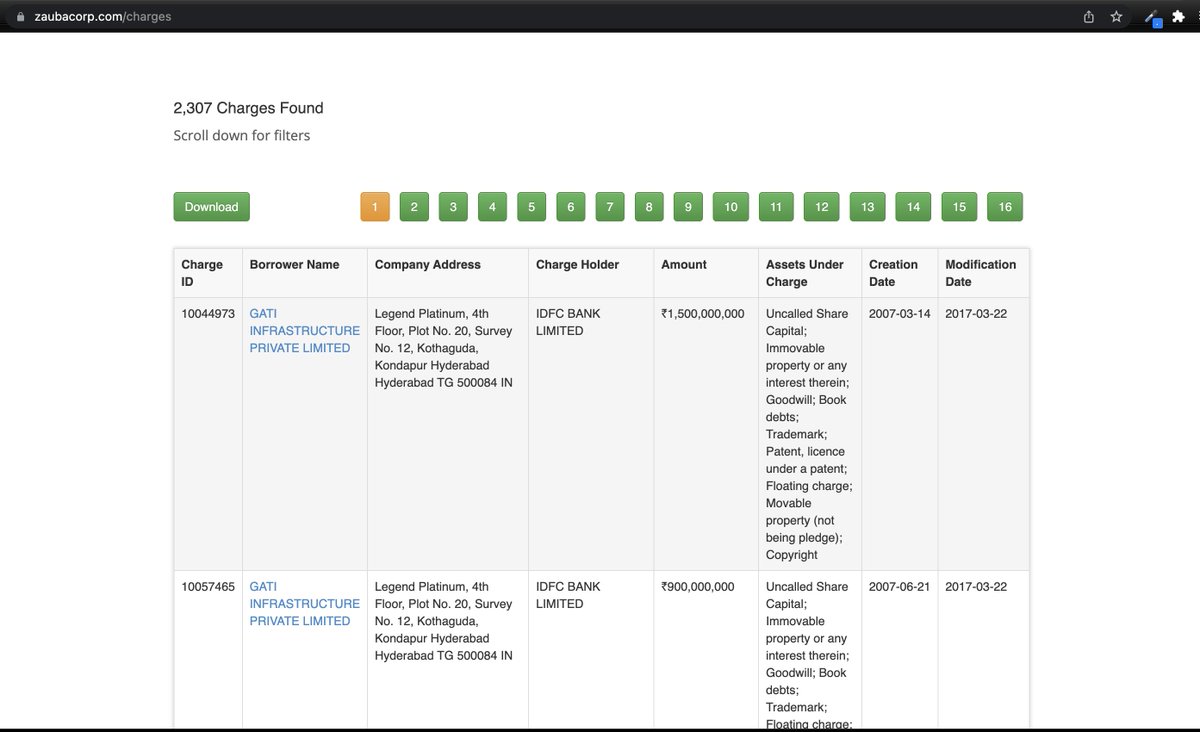

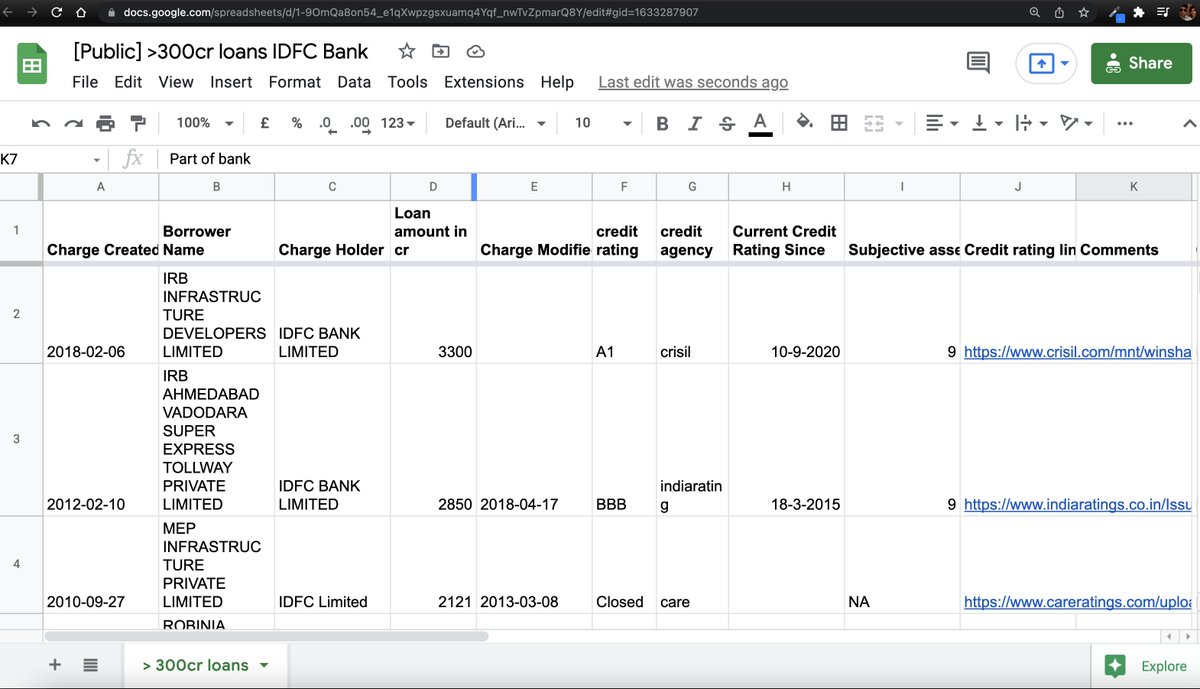

I had talked about this few days ago. Here is the raw data for IDFC bank:

How to obtain this data? Go to zaubacorp.com

: scroll downward until you reach the "search charges" section.

: scroll downward until you reach the "search charges" section.

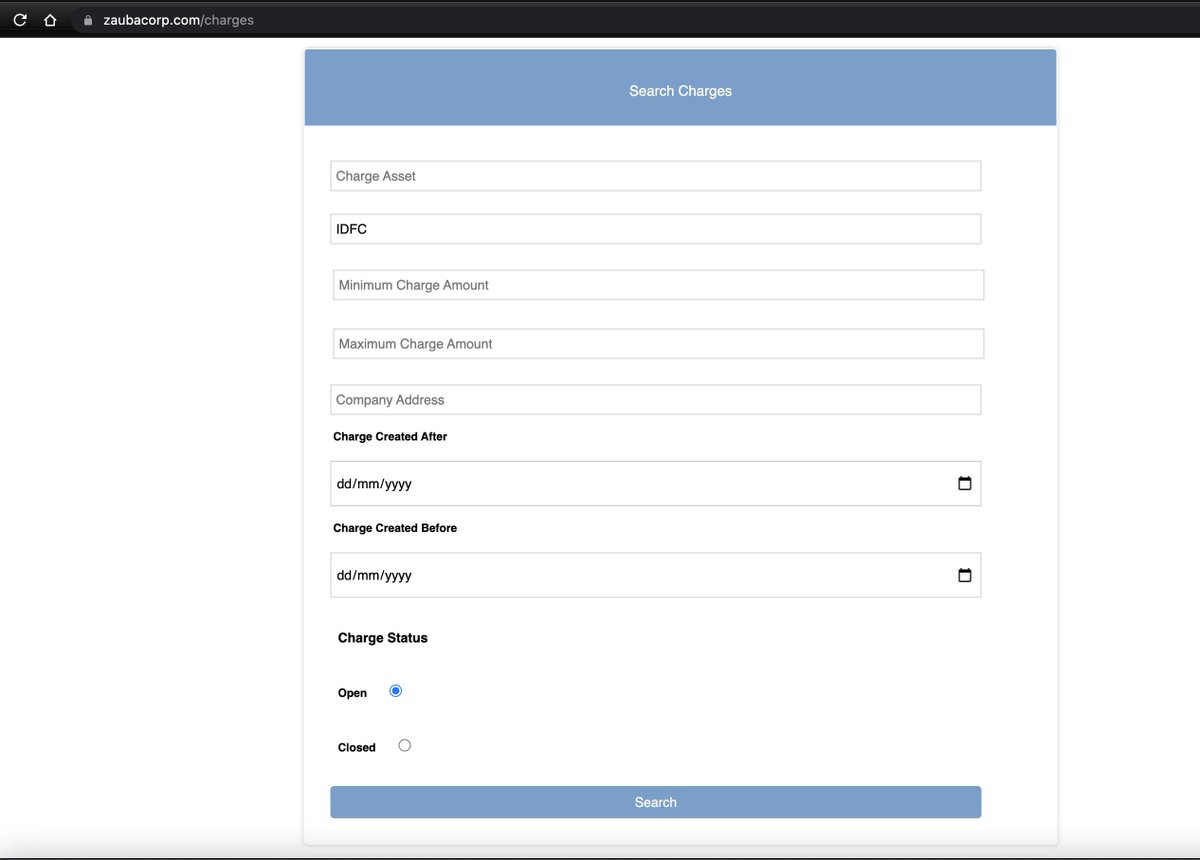

Enter name of your lender in "Charge Holder name" (eg: I enter "IDFC", since i want to see all charges: older pre-merger charges as well), put charge status as "open" (closed charges wont show us risks to current P&L). Hit "Search"

You will see all charges that are open as per Zauba. You can download these by clicking on "download" button & now the fun begins.

First of all, a word of caution.

List of open charges can be erroneous since this is based on MCA filings. Specially if a co goes bankrupt it might not be updating the charges.

My focus is to think about charges which represent loans which are risky but not yet bankrupt.

List of open charges can be erroneous since this is based on MCA filings. Specially if a co goes bankrupt it might not be updating the charges.

My focus is to think about charges which represent loans which are risky but not yet bankrupt.

All of this data is based on MCA filings by respective companies & are thus public info. The amount of charge might also be erroneous if company has not updated latest updated charge amount or updated closing of charge.

Step1:

List of charges for IDFC bank is here:

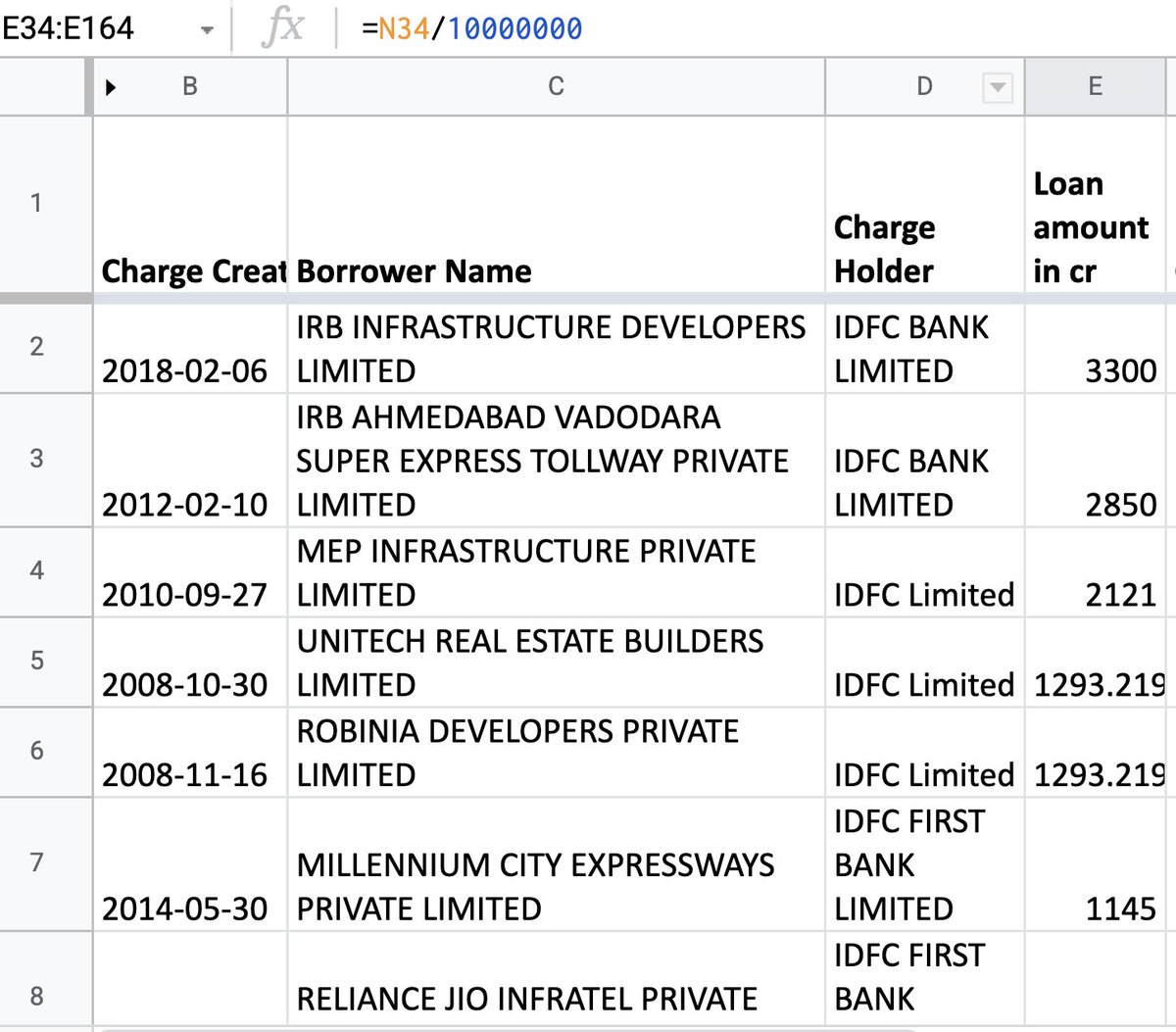

I sort all of these by the loan amount.

List of charges for IDFC bank is here:

I sort all of these by the loan amount.

Step 2a: Private Cos

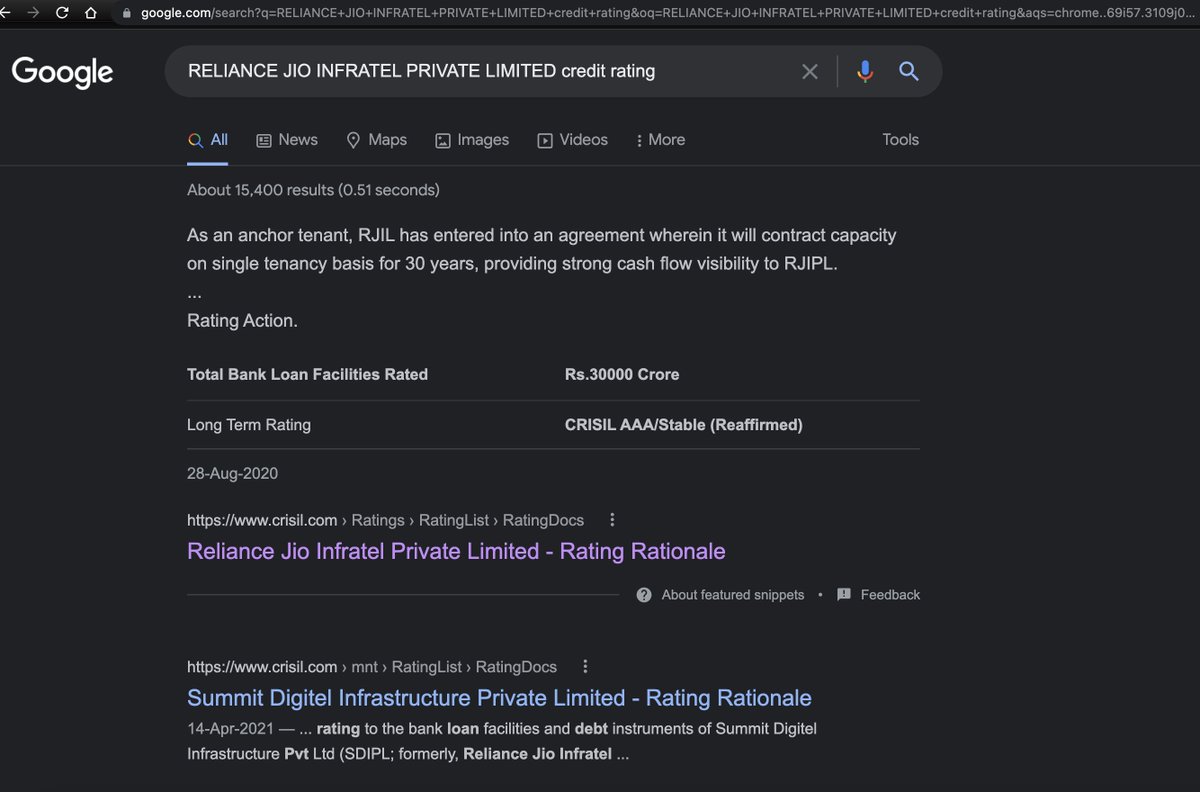

For private companies: I start by googling “RELIANCE JIO INFRATEL PRIVATE LIMITED credit rating” & try to find the latest one & go through it to understand the last known business health.

generally within 1st 4-5 links we find latest credit rating report.

For private companies: I start by googling “RELIANCE JIO INFRATEL PRIVATE LIMITED credit rating” & try to find the latest one & go through it to understand the last known business health.

generally within 1st 4-5 links we find latest credit rating report.

Step 2b: Public Cos

For public companies I look at their balance sheet & P&L & try to see the interest / operating profit ratio see whether co can cover interest costs.

For public companies I look at their balance sheet & P&L & try to see the interest / operating profit ratio see whether co can cover interest costs.

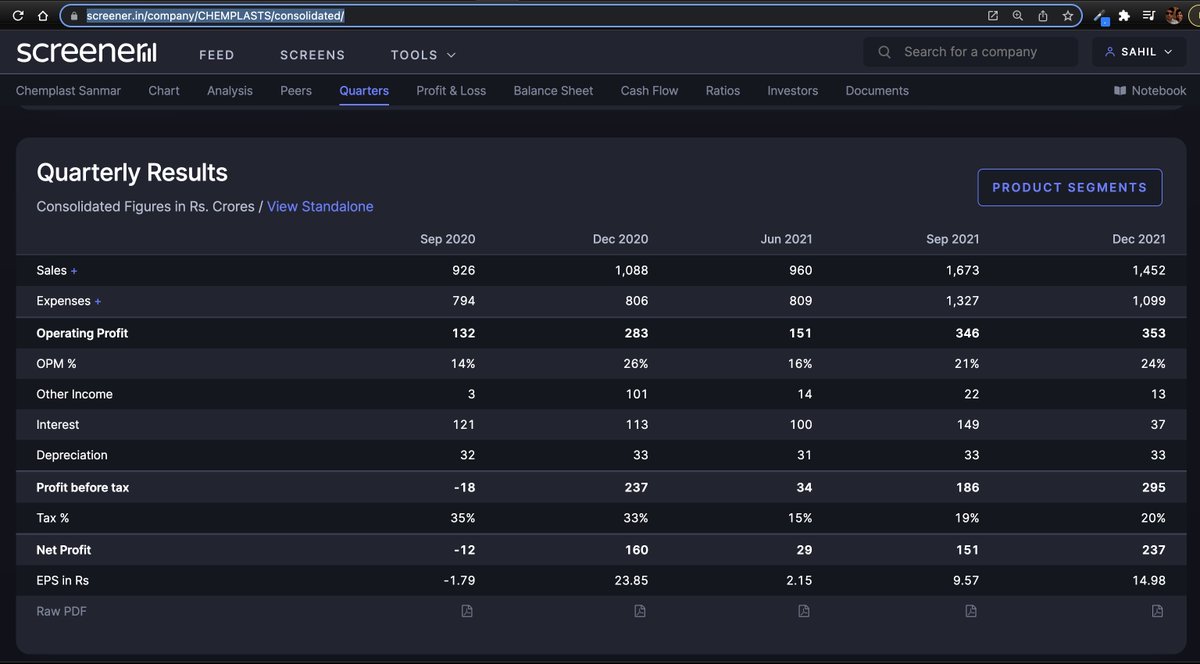

eg: for "CHEMPLAST CUDDALORE VINYLS LIMITED" you find from credit rating report crisil.com & from that wee know it is a 100% subsidiary of Chemplast Sanmar.

So from screener.in we find it's P&L & we can evaluate it.

Looks healthy enough. 37cr interest cost with 353cr operating profit. Nice!

Looks healthy enough. 37cr interest cost with 353cr operating profit. Nice!

Step 3:

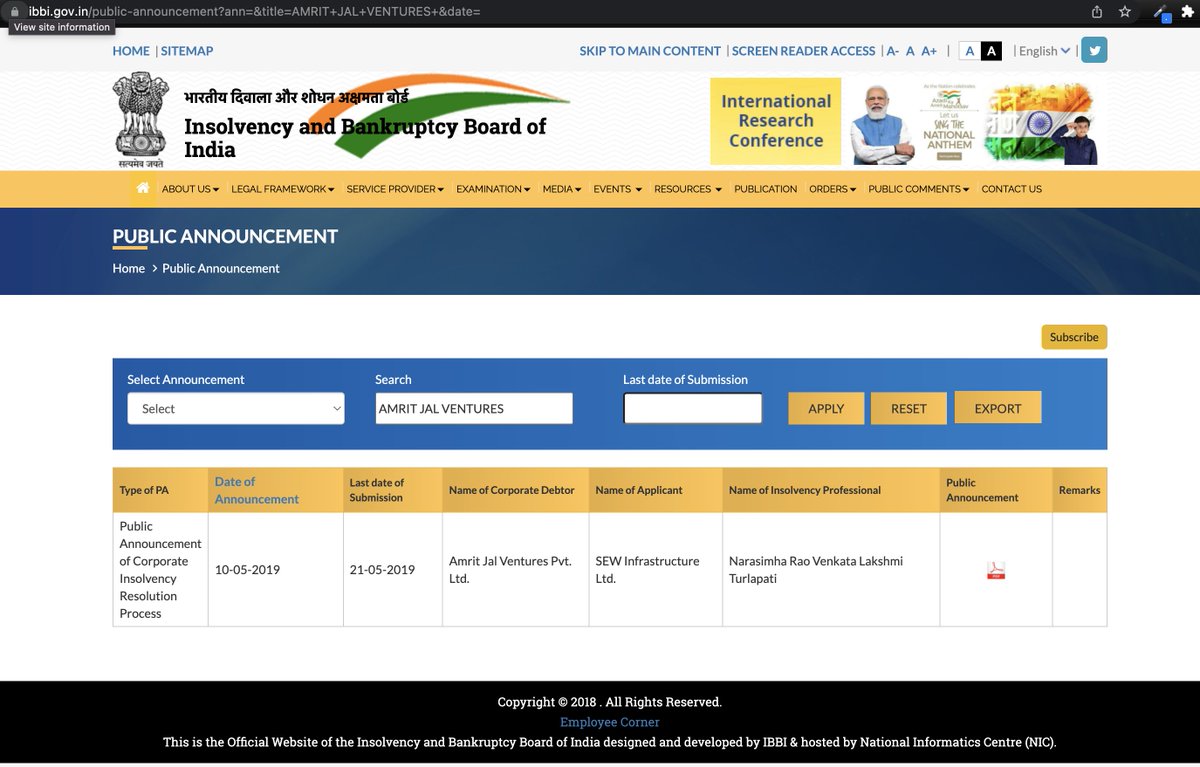

If i cannot find a credit rating report i look for the company on Insolvency and Bankruptcy Board of India. It can help us help us understand if a co has already had bankruptcy proceedings initiated against it.

Website:

ibbi.gov.in

If i cannot find a credit rating report i look for the company on Insolvency and Bankruptcy Board of India. It can help us help us understand if a co has already had bankruptcy proceedings initiated against it.

Website:

ibbi.gov.in

If so, I take it that this co presents no risk to bank because banks are required to recognise such cos as GNPA already.

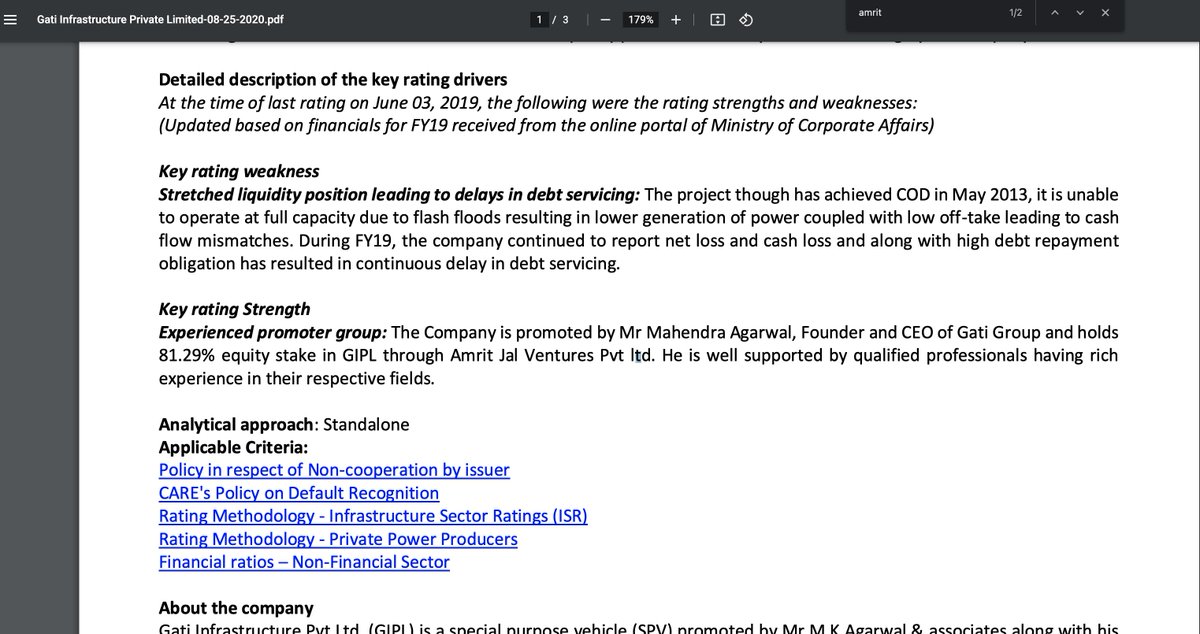

eg: see charge for "AMRIT JAL VENTURES PRIVATE LIMITED" & we see bankruptcy proceedings already initiated against it. So i dont need to worry about it.

eg: see charge for "AMRIT JAL VENTURES PRIVATE LIMITED" & we see bankruptcy proceedings already initiated against it. So i dont need to worry about it.

Step 4:

For private cos I read through the credit rating report & try & understand the risk of insolvency/bankruptcy & take a subjective call (i could be wrong) that this blows up the bank P&L & balance sheet: this is in a column of the sheet: Subjective assessment score & comments.

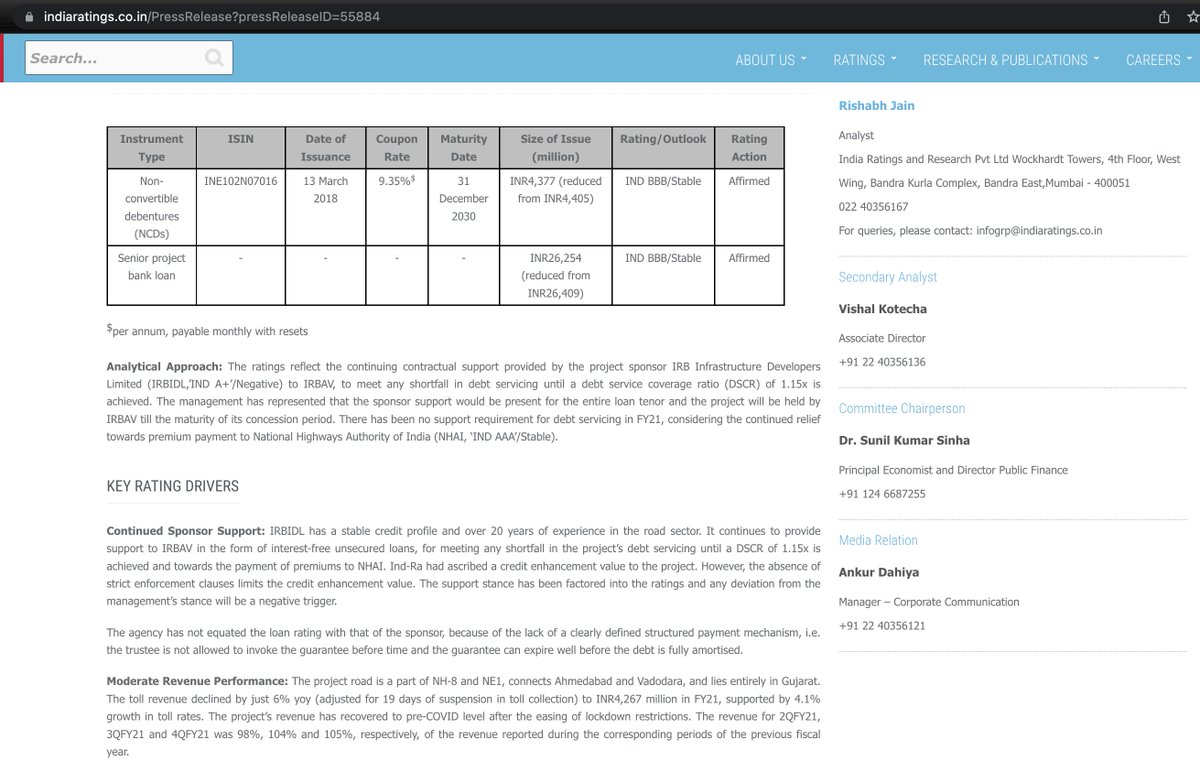

eg: for "IRB AHMEDABAD VADODARA SUPER EXPRESS TOLLWAY PRIVATE LIMITED" i go to its credit rating report indiaratings.co.in

And see its rating as BBB. I read that parent has contractual obligation to repay the debt etc.

And see its rating as BBB. I read that parent has contractual obligation to repay the debt etc.

Step5:

I repeat this for all loans that look significant to me. In this case I did it for 32 loans with charges that are >= 300cr in exposure (roughly equal to current profit size in a quarter for the IDFC bank).

I repeat this for all loans that look significant to me. In this case I did it for 32 loans with charges that are >= 300cr in exposure (roughly equal to current profit size in a quarter for the IDFC bank).

Some key conclusions:

1. Sometimes charges are there for many related companies: holding company, child company & so forth. Sometimes for same amount.

1. Sometimes charges are there for many related companies: holding company, child company & so forth. Sometimes for same amount.

These might not represent additive risks IMO & might be an optionality that co asks for (give me ability to take 800 cr in sub & parent i will pick how to utilize with what proportion).

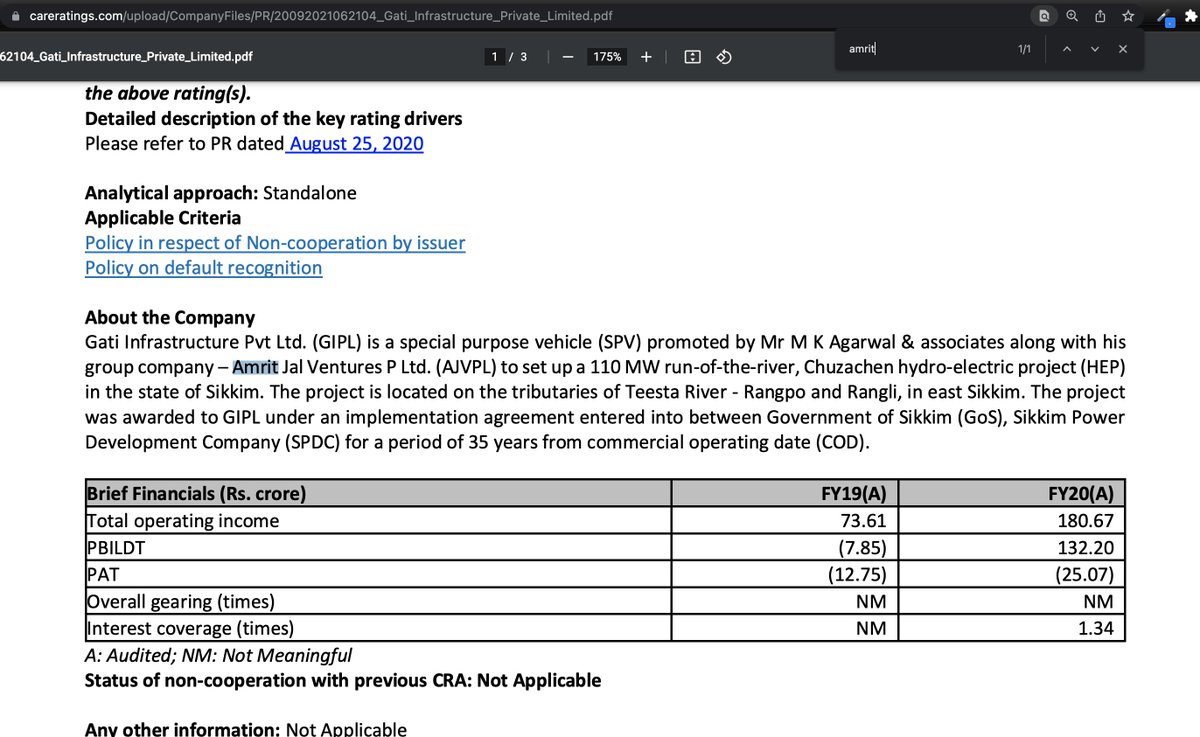

Eg: AMRIT JAL VENTURES PRIVATE LIMITED is the holdco for GATI INFRASTRUCTURE PRIVATE LIMITED we found this from a credit rating report.

2. 10 out of 32 charges have either been paid already (rating withdrawn) OR already insolvent/declared GNPA by bank (eg: the GVK JAIPUR EXPRESSWAY PRIVATE LIMITED is already declared GNPA by bank) & imo do not present any more risk. I exclude these from further calculations

3. 16 out of 22 exposures (73%) are rated A- & above. These are relatively less risky exposures.

4. 6 out of 22 (27%) are rated BBB/BBB+. These are where I have used my subjective judgement & deep dive most. As of the time of the rating report, I don't a very high default risk but definitely these are the ones to be cautious about. Eg: 3F INDUSTRIES LIMITED

5. If we look at loans given post merger (2019 & beyond): there are 10 such charges (totalling to 5000 cr). Only 1 of them is BBB (CAPFLOAT FINANCIAL SERVICES PRIVATE LIMITED) Rest (90%) are all A+ or already paid back.

We can see some merit in the statement of corporatee book being "pristine pristine" loan book by VV. These include many well known names like : IRB infra, JSL steel, credit access grameen, indigo airlines, tata power solar, reliance jio infratel, chemplast sanmar.

That's it, thats the thread.

Please consider following if you would like to read similar threads in the future. 🙏

A thread of all my threads:

Please consider following if you would like to read similar threads in the future. 🙏

A thread of all my threads:

Nothing on this thread is an investment advice. Do your own due diligence before making your investment decisions. I have tried to present all data correct to my abilities. Apologies for any mistakes.

Loading suggestions...