Business Analysis Series Post 1: Learn

1 Why ROCE of 12.5% & growth of 10% are imp. threshold to define quality of a business

2 How declining ROCE/Margins & sales growth be used to shortlist companies

3 Case Studies: Steel, Banking, Telecom, Spinning, Export generic pharma(1/n)🧵

1 Why ROCE of 12.5% & growth of 10% are imp. threshold to define quality of a business

2 How declining ROCE/Margins & sales growth be used to shortlist companies

3 Case Studies: Steel, Banking, Telecom, Spinning, Export generic pharma(1/n)🧵

You might have heard the famous quote from Mr. Charlie Munger in which he says “Fish Where the Fish are” which simply means Invest where the profits/Cash Flows are clustered. (2/n)

All businesses are not equal, some are tremendously profitable (think: FMCG, tobacco, domestic pharma) & some businesses perpetually make low returns (Steel, airlines etc.)(3/n)

This is generally measured by using a combination of high ROCE & high Sales growth. As everyone would have read in the book coffee can Investing by Saurabh Mukherjea @MarcellusInvest .(4/n)

Let’s understand how to define high ROCE? Picking from Mr. Buffett dictionary a promoter needs beat his opportunity cost of capital.

The closet alternative to being an entrepreneur is being an investor. (5/n)

The closet alternative to being an entrepreneur is being an investor. (5/n)

Assuming you don’t know direct investing – Indexing is an option that does not require any knowledge of financial analysis or business analysis. (6/n)

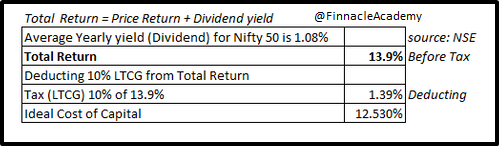

What if we tell you that this closet alternative (Nifty) has over a long period of time provided a return of 12.5% on after-tax basis? Now, how would you feel if your businesses perpetually generates returns less than this 12.5%? Bad right? Hence, the cut of ROCE of 12.5%. (7/n)

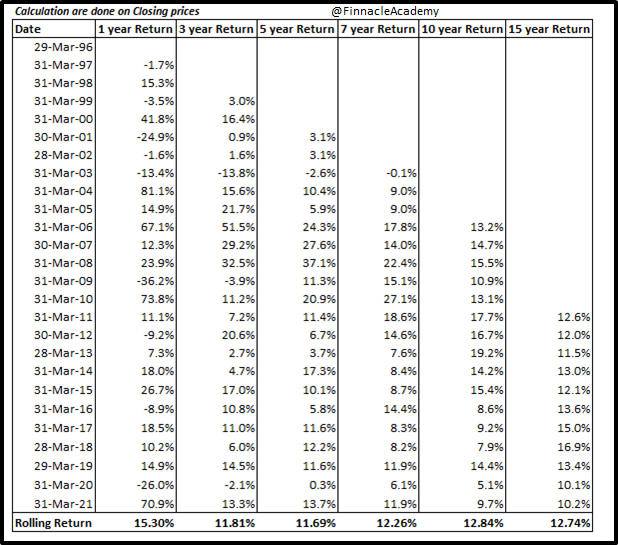

We measure Nifty returns we calculated rolling returns for various holding period: 5 years, 7 years, 10 years, 15 years. Why only long time periods you may ask? (8/n)

As we are figuring out opportunity cost of capital invested in a business and no promoter invests capital into the business with a shorter time horizon than 5 years at least. See observations of Nifty rolling return below: (9/n)

21 sets of 5 year rolling returns – Median return 11.69%.

19 sets of 7 year rolling returns – Median return – 12.26%.

16 sets of 10 year rolling returns – Median return – 12.84%.

11 sets of 15 year rolling returns: Median return – 12.74%.(10/n)

19 sets of 7 year rolling returns – Median return – 12.26%.

16 sets of 10 year rolling returns – Median return – 12.84%.

11 sets of 15 year rolling returns: Median return – 12.74%.(10/n)

As you will read above you can pick any time duration median returns of Nifty over a long period will be around 12.5%. We also did adjustments for dividend yield, STT & LTCG. Check the image below: (11/n)

Coming to growth was simple if India being a 2.5 trillion $ country can grow at 6-7% in real terms(volume) a business which is much smaller in scale as compared to country as a whole should,at any cost,grow at 10% CAGR in nominal terms (volume+price hike) due to base effect(12/n)

Taking ROE or ROCE depends on sector you are analyzing, if we take steel or banking which majorly are debt driven businesses you need to work on ROEs whereas in FMCG companies which technically should have been debt free due to cash generating nature, you will check ROCE. (13/n)

This is actually contrary to textbook academics which conveys to use ROCE for debt heavy business

ROCE is taken because all companies have different Capital structure & if company has a low equity component in their capital structure then ROE boosts up due to more leverage(14/n)

ROCE is taken because all companies have different Capital structure & if company has a low equity component in their capital structure then ROE boosts up due to more leverage(14/n)

In no way we mean that you should only invest in such kind of businesses. There are abundant ways of making money. (15/n)

For example let's take the opposite. Good investment candidates can also be shortlisted from businesses which have been performing very poor or where performance has become so bad that the business has hit decadal lows in terms of ROEs, Margins & growth.(16/n)

Let's see the same thing happening with textile spinning companies around Q3FY20.They were quoting at decadal low margins. (Please note this was in Dec 19 quarter which was before impact of Covid even started in India).Please find below margin data of few spinning companies(17/n)

Also Look at the yearly margins to understand this were lowest margins seen in a decade (18/n)

The important thing to note is that this was in spite the fact that both of these companies has moved into value added products from just spinning to selling Yarn to selling fabrics. basically moving up the value chain which has higher margins.(19/n)

Even high margins products the margins were at the worst level of when they only used to do low margin commodity spinning work. This shows how hard margins of these companies were hit during last 2 quarters of FY20 and first quarter of FY21.(20/n)

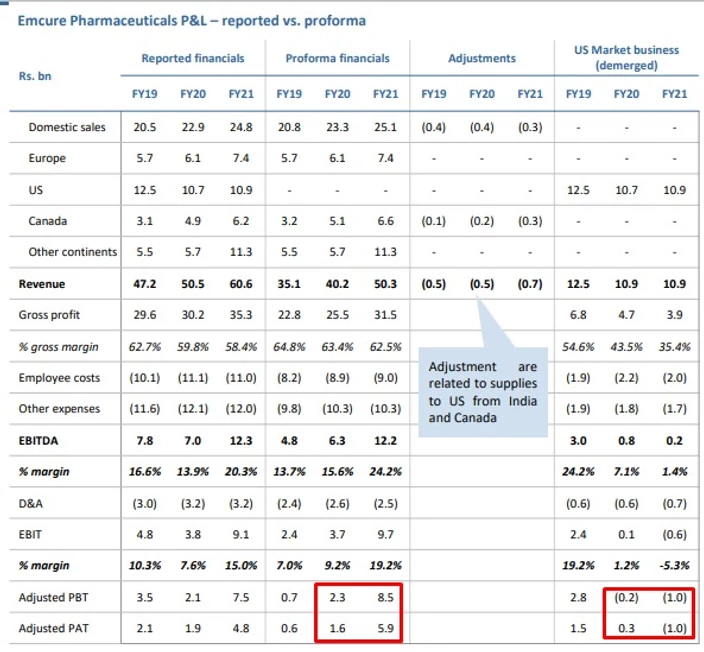

Even look at margins of US focused Pharma names. Companies coming for IPOs which have both Us based and domestic businesses are de-merging US based businesses to get high valuations in IPO 😀.

Case in Point: Emcure Pharma.(21/n)

Case in Point: Emcure Pharma.(21/n)

Same phenomena happened in telecom. Look at how badly the sales growth & margins of Bharti Airtel was hit in FY 19 leading to decadal low growth and margins. Intentionally we have taken only standalone numbers to focus on domestic telecom business.(22/n)

And than look at the turnaround in the business performance of Bharti Airtel. Below are the quarterly numbers since march 2019. A one way upward improvement in margins. (23/n)

Read about base rates here: finnacleshahclasses.com

Also check out this thread by @sahil_vi he has wonderfully taught how to use screener to generate names of such companies here: (24/n)

Also check out this thread by @sahil_vi he has wonderfully taught how to use screener to generate names of such companies here: (24/n)

Read Entire thread here:finnacleshahclasses.com

Watch our YouTube video explaining the entire thread in detail here:

youtu.be

To continue your learning and fun with finance follow us on Instagram: instagram.com

Watch our YouTube video explaining the entire thread in detail here:

youtu.be

To continue your learning and fun with finance follow us on Instagram: instagram.com

For readers on @MultipieSocial you can read the same here: multipie.co

@singhalrajk @NarangYashika @abhymurarka

@singhalrajk @NarangYashika @abhymurarka

Loading suggestions...