🧵🧵A thread on Alicon Castalloy Ltd 🧵🧵

Alicon Castalloy (erstwhile, Enkei Castalloy Ltd) runs one of the largest aluminium foundries in India.

In a foundry typically, you manufacture metal cast components that find application in various sectors.

Alicon Castalloy (erstwhile, Enkei Castalloy Ltd) runs one of the largest aluminium foundries in India.

In a foundry typically, you manufacture metal cast components that find application in various sectors.

But wait…What’s special in a foundry business? There are apparently 5000 foundry units in India, 90% of them can be classified as MSME and 70% are of grey cast iron.

Let's find out what's special about ACL (if any)

Let's find out what's special about ACL (if any)

ACL is a combination of European engineering (Illichmann Castalloy) + Japanese quality (Enkei Corp) + Indian innovation (Alicon group). ACL provides aluminium casting solutions using Low-Pressure Die Casting (LPDC) and Gravity Die Casting (GDC).

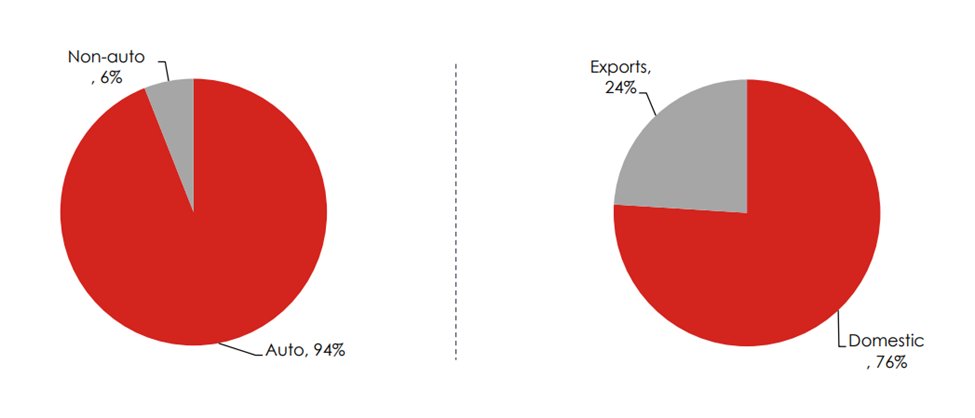

Diversified customers base: More than 90% of ACL's revenue comes from auto industry, it has managed to build a broad customer base.

Product portfolio:

Strategic growth pillars:

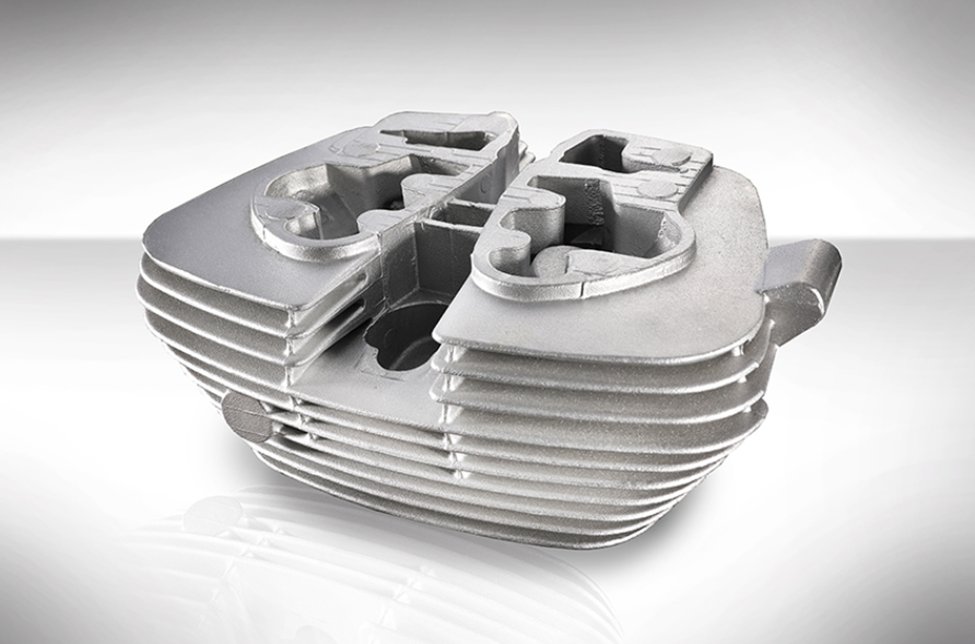

1) Auto sector: Supplying aluminium casting solutions to major auto OEMs. Cylinder heads are the flagship products. 42% of India’s cylinder heads are made by Alicon and 2.2 million 2-wheelers use ACL's cylinder heads.

1) Auto sector: Supplying aluminium casting solutions to major auto OEMs. Cylinder heads are the flagship products. 42% of India’s cylinder heads are made by Alicon and 2.2 million 2-wheelers use ACL's cylinder heads.

With the BS-VI regime, ACL is also supplying its customers with suspension parts, wheel hubs, bridge fork top, outer tubes and inlet pipes, in addition to cylinder heads. This provides more 'Alicon content per vehicle' to ACL.

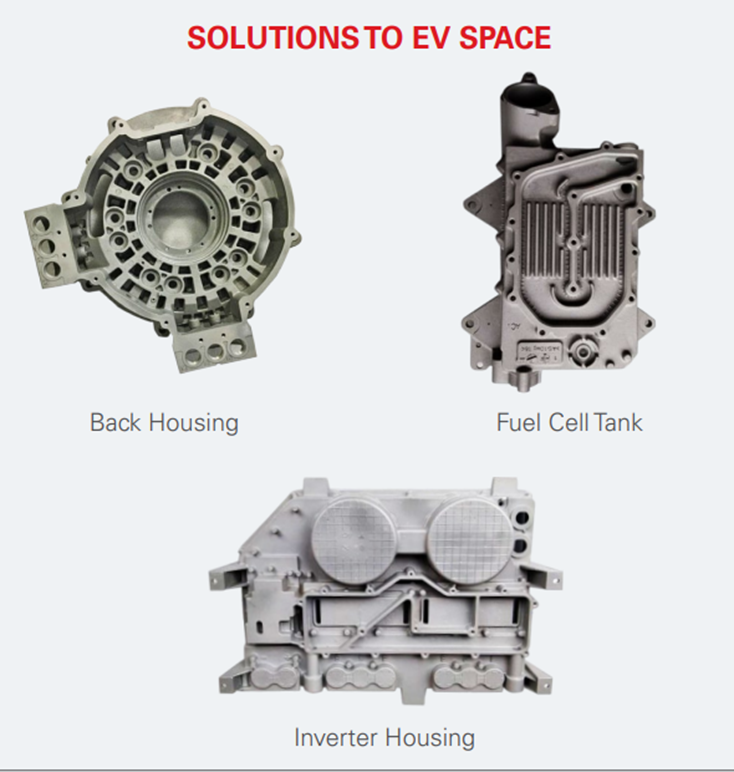

2) Electric Vehicles: Several ICE auto components that are in cast iron or steel fabrication or similar composite material, are likely to be converted into aluminium or other low-density material in the electric vehicle.

Aluminium and other low-density materials enable a weight reduction of the component as much as 46%, enabling EV efficiencies. Additionally, as vehicles are converted from ICE to EV platform, it is anticipated that aluminium usage will see a 2-2.5-fold increase per vehicle.

ACL is already supplying battery housing to Samsung who supply onward to JLR in the EV space. ACL has also received orders from Dana Corporation, Mahindra & Mahindra, Graziano and Ashwood for their e-mobility platforms.

3) Non-Auto Business: Die casting has found viability in multiple sectors ex. Indian defence sector refurbishing tank wheels with lightweight aluminium parts to lower the tank’s overall weight. Armed with Low-Pressure Die Casting process, ACL is the only Indian supplier.

ACL is also supplying cylinder heads for defence trucks. In agriculture, ACL’s aluminium components are being used by tractors.

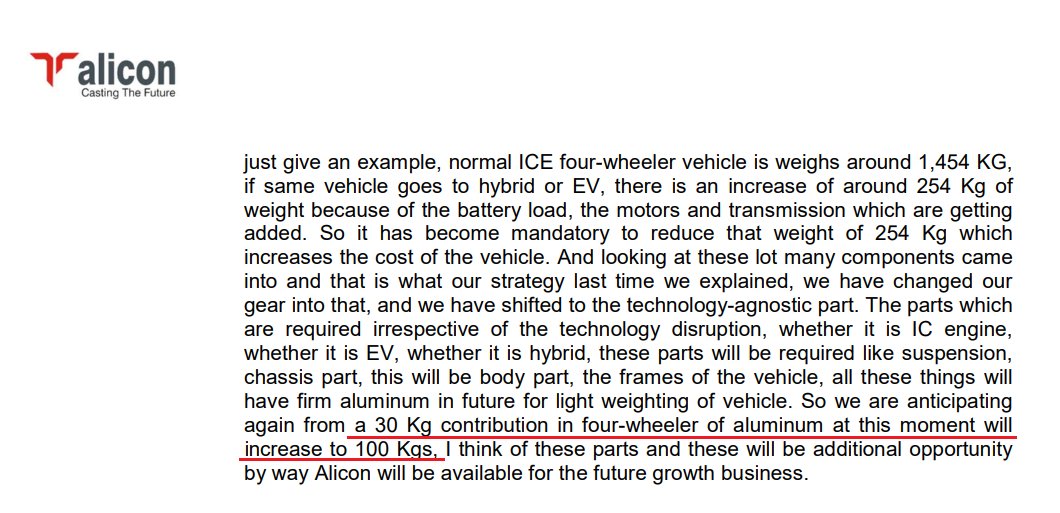

4) Technology Agnostic Solutions: Whether platform is ICE, EV or Hybrid, some components remain technology agnostic. Ex. material chassis and suspension components in ICE earlier made in forged steel are now being made in aluminium due to increasing focus towards lightweight EVs.

This may lead to aluminium contribution in a 4W vehicle from 30 kg to 100 kg. Q3FY21 concall excerpts:

5) Solution Provider: ACL has devised a thermal engineering solution for EVs that helps alleviate extreme heating in motors and batteries. ACL has partnered with Bosch and Samsung/ e-mobility technology leaders for these thermal management solutions.

ACL has also collaborated with Dana Corporation, a leading global supplier of electrified propulsion systems to develop ready-to-use technology. Such value-enhancing offerings make ACL the preferred partner of choice for customers across their ICE and EV initiatives.

🔍Huge orderbook: Company’s target share of EV business by 2025 is 36% (45% aspirational). It has been working with OEMs and tier-1 suppliers for scaling up EV business. Already have 65 parts related to EV in the portfolio.

Tata Auto comp who is supplying battery packs and motors for EV platform to Tata motors, used to source components from China, now has turned to Alicon with a new order worth 150 cr.

Exclusive supplier to Ather Energy. 3% of total revenue comes from Ather but its significant as Alicon’s content per 2W vehicle goes to 17 kg in EV from 2-3 kg in ICE.

Orderbook stands at 3250 cr, including orders worth Rs 810 cr from JLR Daimler, Samsung and MAHLE, Rs 1,100 cr from PSA, Toyota, and Renault, ~Rs 900 cr from Mahindra, Dana, Reml, Eaton, Rs 150 cr from TACO. Orderbook has 33% EV orders in last 9 months and 57% in Q3FY22.

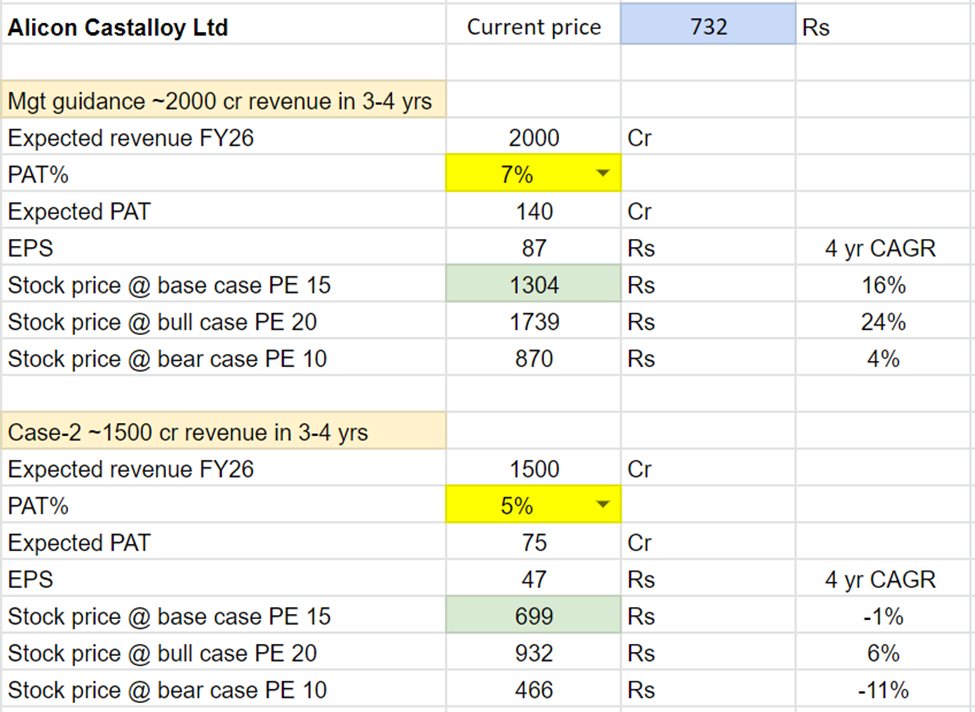

🔍CAPEX plans: ACL plans to carry out capex of about Rs 267 crore during FY22-24, which is expected to be funded largely by equity and internal accrual and marginally through debt. With net asset turn of 3x, this may translate into additional 800 cr revenue.

90 cr capex scheduled for FY22 was deferred due to uncertain macro environment and 55-60 cr out of it was deployed to value added finishing and machining processes.

🔍Key challenges: 4'C's as per ACL:

1)Covid-19

2)Cost based inflation

3)Chip shortage and supply chain constraints

4)Cost of new product development

Despite that ACL was able to hold 50% gross margins which suggests judicious material sourcing while alloy prices were obscene.

1)Covid-19

2)Cost based inflation

3)Chip shortage and supply chain constraints

4)Cost of new product development

Despite that ACL was able to hold 50% gross margins which suggests judicious material sourcing while alloy prices were obscene.

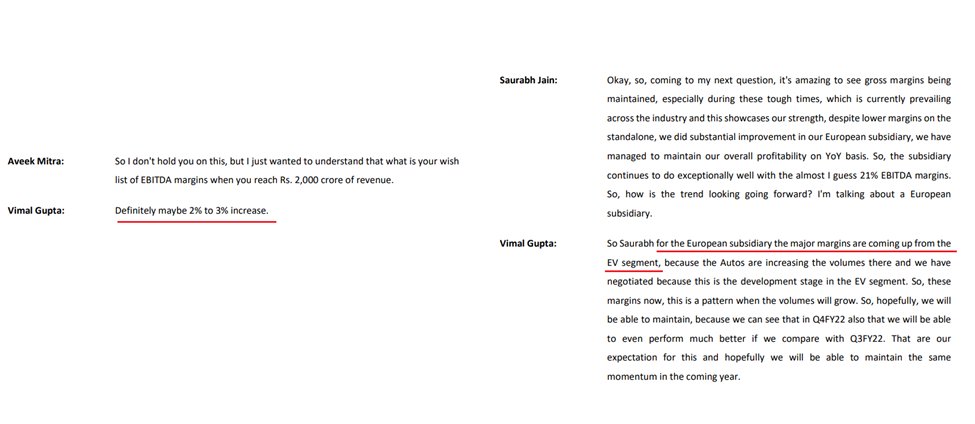

🔍Margin improvement: Focus on value products ex. higher machining, increasing EV orderbook, European subsidiaries doing well, suggest that future EBITDA margins should be higher than the historic margins. Despite recent turbulence, Q3FY22 margins remained over 12%.

🔍Key Risks:

1) 94% revenue comes from Auto industry at the moment and cylinder head is their flagship product. E-mobility is a threat to ACL’s key product as cylinder heads are not required in EVs.

1) 94% revenue comes from Auto industry at the moment and cylinder head is their flagship product. E-mobility is a threat to ACL’s key product as cylinder heads are not required in EVs.

Though E-mobility vehicles are expected to be 30-35% of the total lot by 2030 and co has been developing new products rapidly.

2) Al penetration in 2W industry is already very high. ACL is trying to cut 2W contribution down to 25% by FY25.

3) Working capital intensive business.

2) Al penetration in 2W industry is already very high. ACL is trying to cut 2W contribution down to 25% by FY25.

3) Working capital intensive business.

Highly dependent on prospects of auto industry

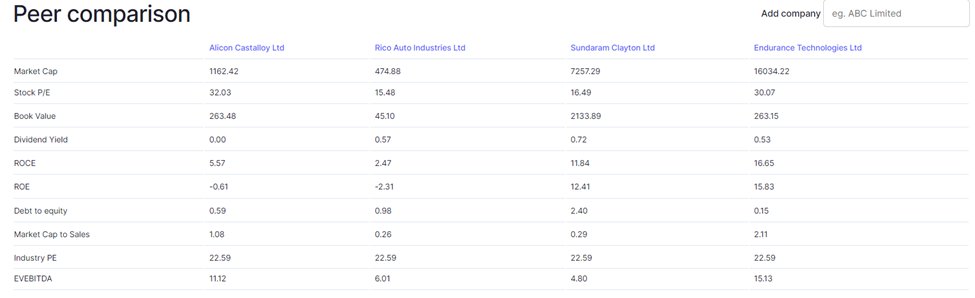

🔍Back of the envelope valuation: ACL’s top listed competition are Endurance tech, Rico Auto, Sundaram Clayton. ACL’s margins range in between Rico and Endurance tech and are similar to that of Sundaram clayton.

When it comes to market valuing these cos, ACL and Endurance tech stand out possibly due to two factors:

1) Low debt to equity

2) Visibility in orderbook for years to come

Market likes orderbook visibility for next 4-5 years but I am not comfortable giving is a bull case PE > 20

1) Low debt to equity

2) Visibility in orderbook for years to come

Market likes orderbook visibility for next 4-5 years but I am not comfortable giving is a bull case PE > 20

Disc : Not invested for two reasons.

1) I liked another aluminium story in Alufluoride more.

2) ACL's exposure to 2W is 50%. Aluminium has already high penetration in 2Ws. Reducing exposure in 2W by 50% and reaching 2000 cr revenue seem mutually exclusive.

🧵End of the thread🧵

1) I liked another aluminium story in Alufluoride more.

2) ACL's exposure to 2W is 50%. Aluminium has already high penetration in 2Ws. Reducing exposure in 2W by 50% and reaching 2000 cr revenue seem mutually exclusive.

🧵End of the thread🧵

Loading suggestions...